Darren415

Darren415

Welcome to another installment of our BDC Market Weekly Review, where we discuss market activity in the Business Development Company ("BDC") sector from both the bottom-up - highlighting individual news and events - as well as the top-down - providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the third week of March.

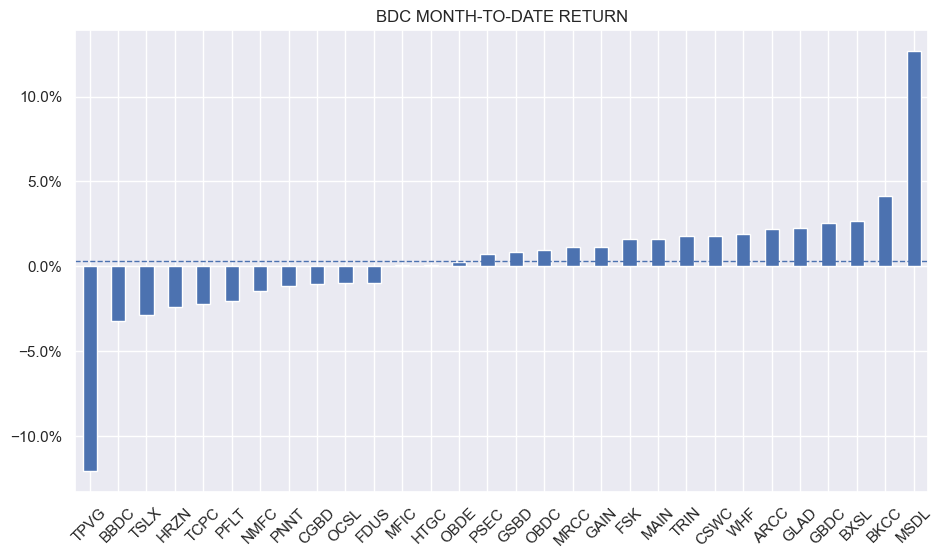

BDCs finished flat on the week which was better than nearly all other income sectors as both equity prices and Treasuries fell on the back of higher than expected inflation. MSDL had a freakish rally late in the week which has now mostly been erased after hours. Month-to-date, TPVG is by far the worst performer - something we highlight below.

Systematic Income

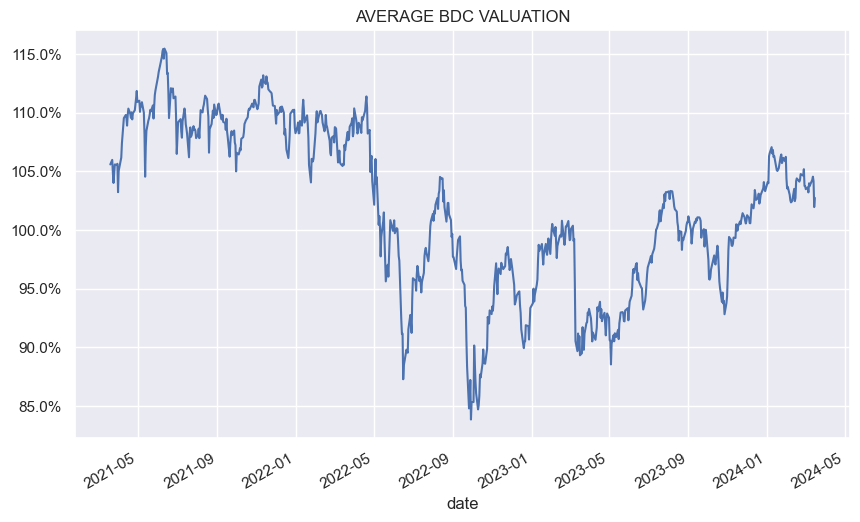

The average sector valuation has come off a bit though some of that is due to a heavy number of ex-div dates in mid-March which have pushed prices lower by 2-3%. Recall that the convention for BDC valuations is to keep NAV fixed which means that ex-div dates will lower valuations by the amount of the dividend which will then creep higher over time as the dividend is accrued in the price.

Systematic Income

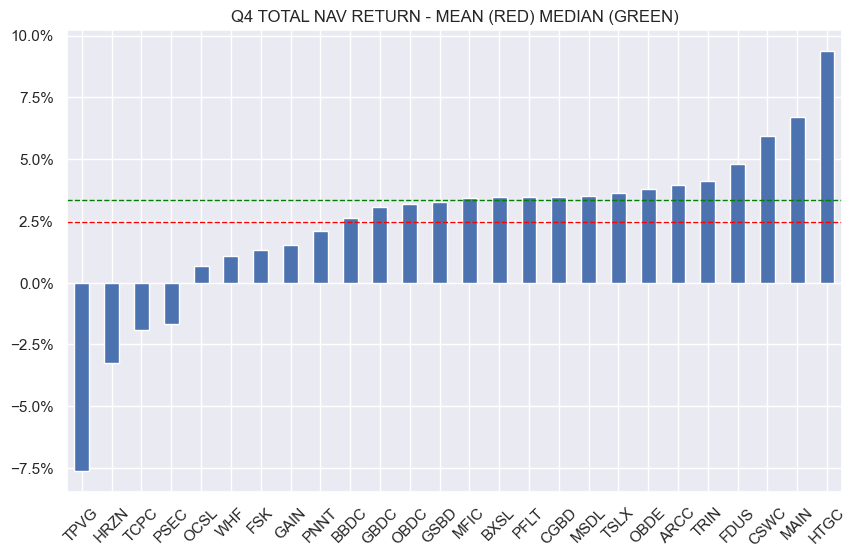

We have now processed nearly all Q4 results in our coverage. Overall, it was a strong quarter for BDCs as the average total NAV return was around 2.5% with the median being slightly higher - good enough for a double-digit annualized pace.

Systematic Income

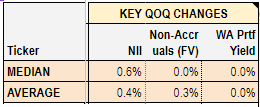

Checking in on the key quarter-on-quarter metrics from our BDC Tool, we see that net investment income or NII managed to increase from Q3 with the median figure rising by 0.6%.

Systematic Income BDC Tool

There was huge variation during the quarter from -14% to +16% with outliers driven more by unusually high repayment fees or a change in non-accruals. Going forward, net income is going to face two headwinds - a likely series of cuts in the Fed Funds rate as well as a continued refinancing of fixed-rate liabilities to higher coupons. On the plus side, BDC fee income should support net income levels once deal flow picks up.

The average level of non-accruals rose by 0.3%. A rise in sector non-accruals has been a trend for several quarters. The average non-accrual figure remains modest at 3.1% (with the median lower at 1.7%). However, that is not representative of overall portfolio stress as some non-accruals have turned into net realized losses. As we discussed in our last Weekly, BDCs are diverging on portfolio quality with some holding in well and others not. So long as short-term rates remain high, we expect non-accruals to increase overall.

Finally, the weighted-average portfolio yield was flat over the quarter. This makes sense as short-term rates have leveled off. Perhaps more importantly however, net portfolio yield will fall over the medium term as an increase in interest expense rises relative to asset yields. That said, both asset yields and net yields are relatively high historically which provides a decent cushion for them to fall.

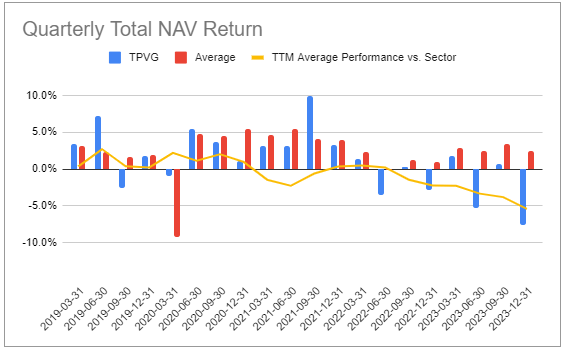

TriplePoint Venture Growth (TPVG) is hurting. The company has delivered a -10% total NAV return in the past year and a +1% return over the last 3 years. That is not good.

Systematic Income BDC Tool

We had an article on the company about six months ago with the title talking about its "wheels coming off". As if on cue, its performance collapsed from that point on. Forget that it underperformed in 13 of the last 14 quarters - its net realized loss sums up to around 32% over the last 6 quarters - a mind-boggling result.

When many investors are faced with underperformance the instinctual question is - is the dividend safe. The short answer is no - not at this rate. Its leverage is 1.8x - extremely high for a BDC. A normalization in leverage to a more reasonable level of 1-1.2x would result in a big drop in net income. Unlike the rest of the sector, the company’s net income has not grown much since 2022 which is a result of its portfolio credit issues. With coverage around 115%, several Fed cuts could likely result in a cut. And unless credit issues miraculously vanish, it’s not far off below-100% coverage.

A more important question than is the dividend safe is - is this a good investment? A common investor conceptual flaw is to compartmentalize the dividend from the principal. Ultimately, the principal is used to drive the dividend - they are not entirely distinct. Over the last 3 years, TPVG has generated practically no wealth for investors - nearly all of the dividend has simply come out of the principal. Worrying about TPVG dividend safety is like worrying about portion sizes in a terrible restaurant.