Scott Olson

Scott Olson

Tapestry, Inc. (TPR) is buying Capri Holdings Limited (NYSE:CPRI) for $57 per share. This deal was announced in August 2023, but has unfortunately been subjected to a 2nd request (I covered the 2nd request here). The deal is trading at a very wide spread as if it is pretty likely it will fail. Capri shares are trading at $46.86. If the deal closes as planned, the upside is 21.63% from here. The EU regulator has set a deadline for a decision on whether the deal needs a phase II investigation on 15-4-2024.

The vast majority of deals aren't burdened by a phase II investigation (~90%). However, this is a relatively large deal and these are obviously much more often scrutinized. Because the company already received a 2nd request (although I'm not sure why) the odds are likely a bit higher.

I'm aware that the administration has stepped up its activity even if only as a deterrent for potential dealmaking activity. However, these parties were aware of that went the deal was agreed to. I expect the parties to be prepared to face a few hurdles along the way.

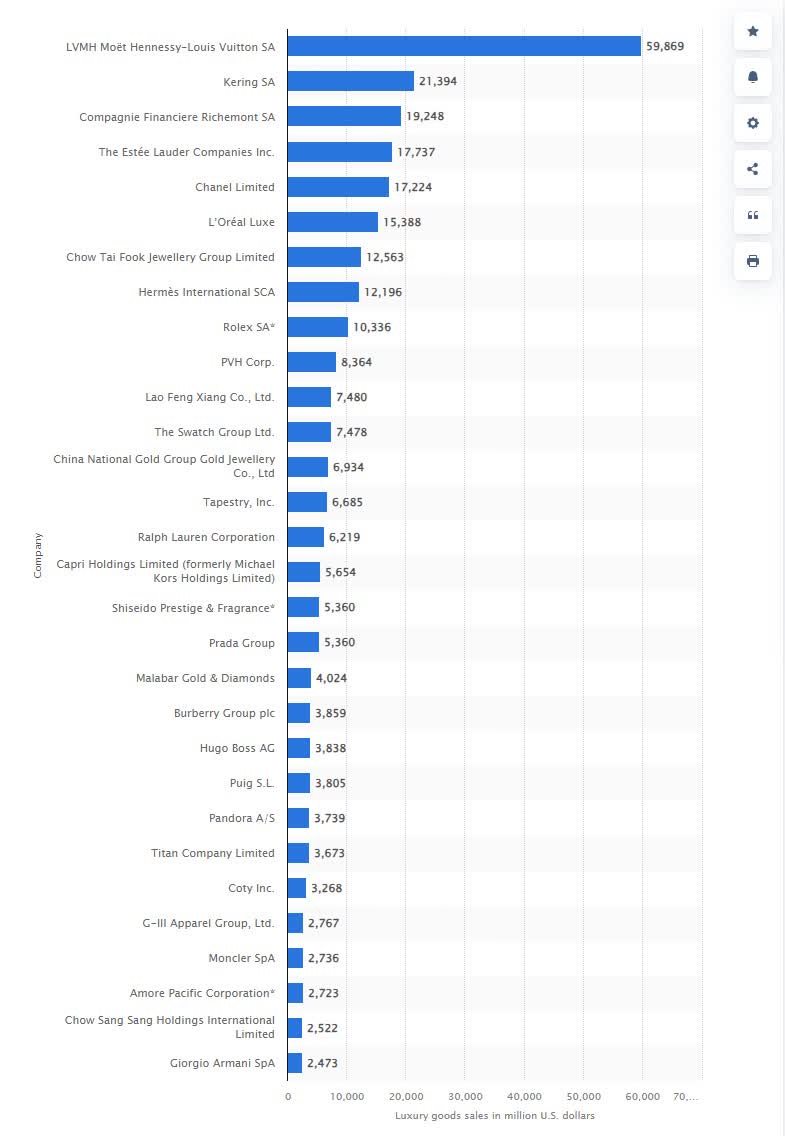

The luxury goods market consists of many small players and a few big ones. In my opinion, it isn't an easy market to define or quantify. This merger is between two relatively small entities. Together, they are expected to make up the fourth-largest luxury goods company. Their combined market share is expected to be around 5%. In a previous article, I've said that the only potential concern I can envision would be a practice where brands lean on retailers to prevent them from discounting.

China approved the deal. The other important regulatory approvals required are in the U.S. and Europe. I don't believe a phase 2 in Europe is likely, but I could be wrong.

The two main reasons I don't agree with the skepticism expressed by the market are, first, because I don't know about any luxury deal that was ever blocked by regulators. Conglomerates like LVMH Moët Hennessy - Louis Vuitton, Société Européenne (OTCPK:LVMHF), Compagnie Financière Richemont SA (OTCPK:CFRHF), and Kering SA (OTCPK:PPRUF) were all built through many acquisitions. LVMH was allowed to buy Tiffany's in 2020 even though its presence in luxury markets is much greater.

Luxury market revenues (Statista)

Second, because it doesn't make a lot of sense to block this deal. Luxury consumers don't need protection from high prices and the market is simply not that concentrated. You could even argue it increases competition as it combines two small-sized entities into the 4th largest.

I guess it is possible to argue the companies would have a larger market share in a subset of luxury. Coach and Kate Spade (two brands involved in this deal) aren't necessarily true luxury brands. I'd qualify these as "premium." But it would appear to me that if competition agencies go down that road, competition mostly increases. As Fflur Roberts of Euromonitor recently told the WSJ:

...the luxury market is a lot more consolidated at the high end...

...the market is a lot more competitive in the midtier, especially for Gen Z shoppers who favor smaller, more niche brands...

Seeking Alpha reported Jefferies sees a 70% chance the deal closes. Its analyst points to concerns in the market about relevant market size. Most importantly Helgans sees a downside to the mid-$20s if the deal were to break. Pre-deal, the company was trading at around $34.

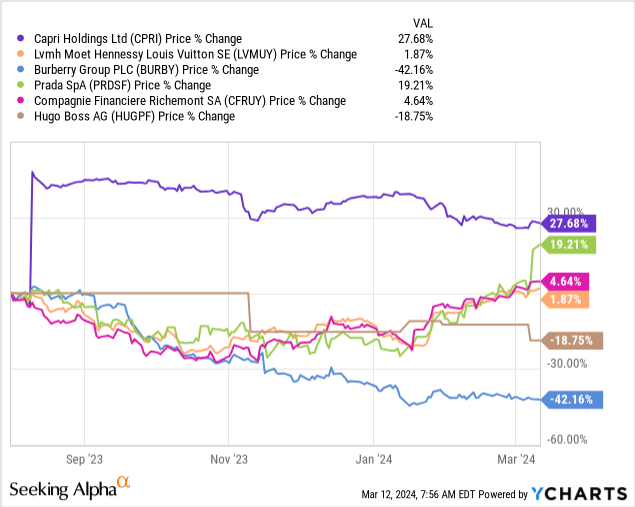

and the entire sector has performed very weak:

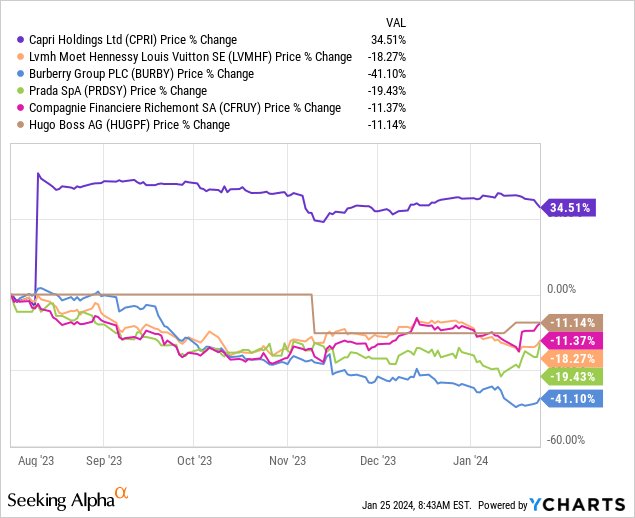

However, when I reviewed this deal in January, performance was much worse across the board:

Luxury company performance figures (YCharts)

The big names have rallied hard year-to-date.

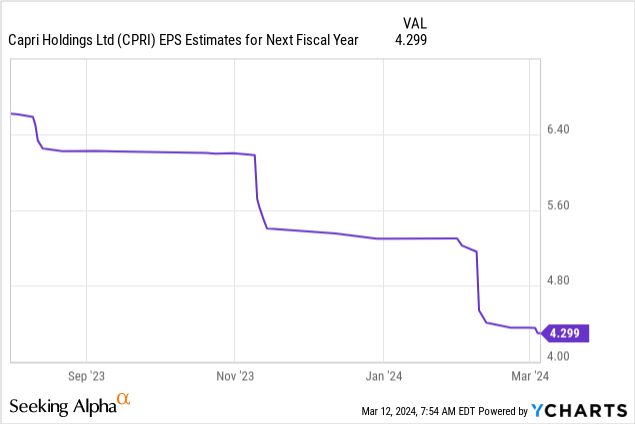

This doesn't necessarily translate to Capri Holdings. Analysts aren't upgrading Capri's earnings profile at all. Big picture, it is an improvement from the bleak picture where all the luxury names were selling off back in January. There is also a sizeable 3% break fee.

The outside date for this is in August. Then two extensions of 3 months can be used. Even if these extensions are necessary, the return is still good here. If the deal isn't contested much by regulators, it could be closed by May.

In my last article, I was quite fearful of the downside because I do think it will drop to between $20 and $35 on a deal break. The stock was also trading higher, leaving less upside. At the time, I figured it could be reasonable to go long a June $50 call and sell a June $57.5 call. At the time I only needed a probability of the deal closing above ~50% to break even on this "bet."

When I review options markets today (and they aren't very liquid so take this with a grain of salt), it looks like the market isn't that much more bearish on the deal closing. A June $50 call is ~$2.6. Keep in mind the market was already bearish. However, the options increasingly seem to indicate it could take until August to wrap up (if it does).

If I wanted to take a position today, I'd be more interested in a stock position. With stock, it matters less when the deal closes, but it matters more than it ultimately does. Alternatively, I'd be looking to sell an April or May at-the-money put. An April $45 put trades at around $1.60. Put selling can result in very large losses, though, so always keep that in mind. As I already hold June/August call spreads, I'm sticking with these as they aren't very liquid. Switching my position around would likely result in quite sizeable transaction costs offsetting potential benefits.