Thinkstock

Thinkstock

This article was coproduced with Leo Nelissen.

It's time to talk about a very important topic: value investing in the oil and gas industry.

Generally speaking, we have become much more conservative when it comes to growth versus value investments, as the market has run hot in recent months.

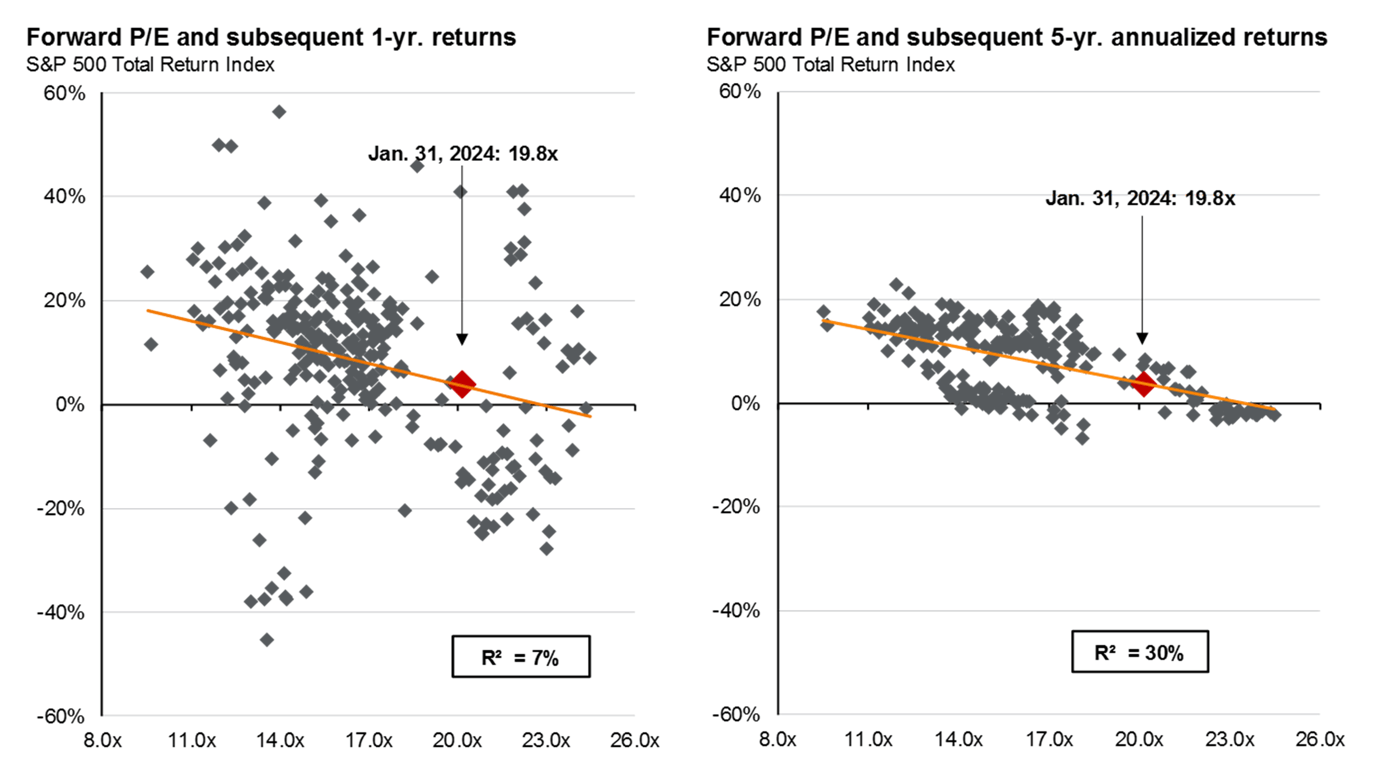

Using the JPMorgan (JPM) data below, we see that going into this month, the valuation of the S&P 500 (SP500) was rather stretched, indicating subdued longer-term returns.

JPMorgan

The reasoning behind this is quite simple. The higher the valuation, the less attractive an investment becomes. This hurts demand and the longer-term performance of the asset.

In today's market, this favors value stocks.

Why?

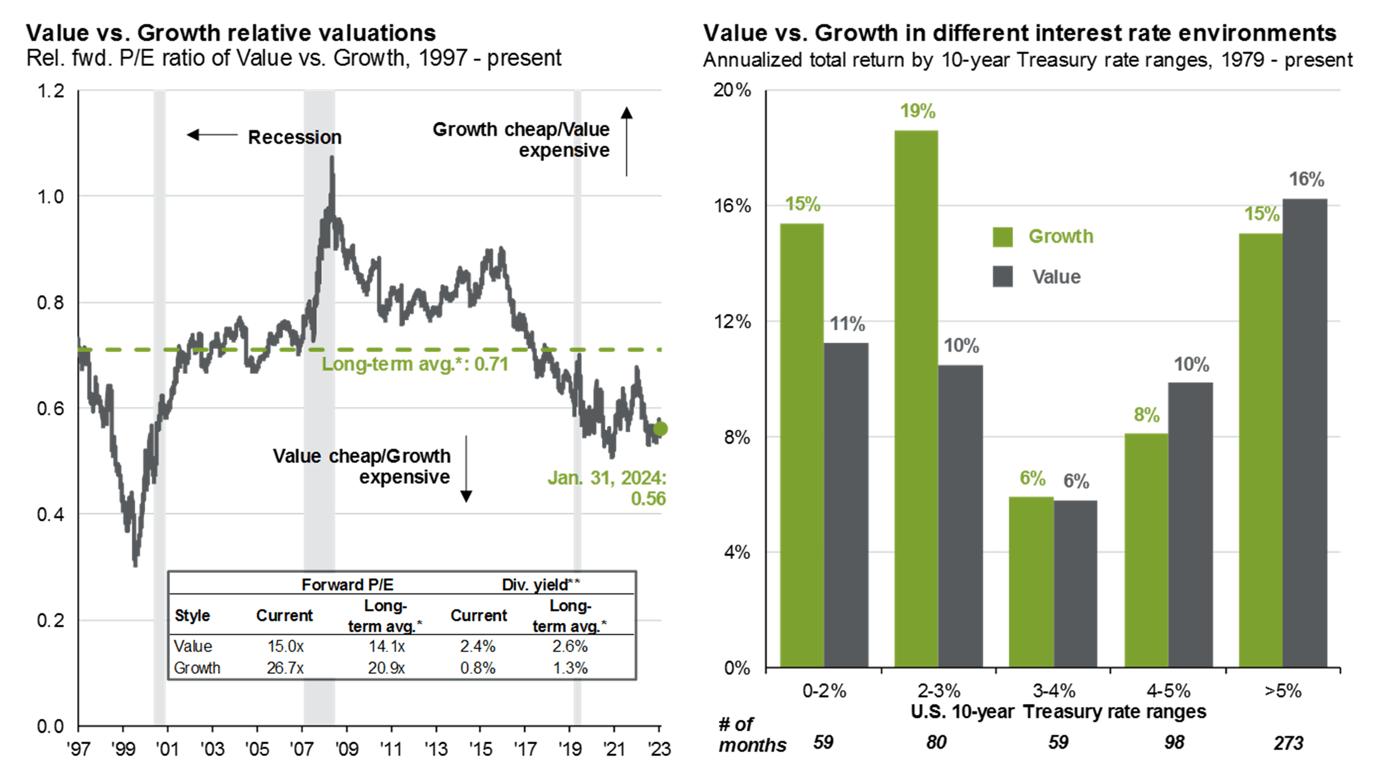

Looking at the chart below, we see that the relative performance of value compared to growth stocks has hit one of the lowest levels since the Dotcom selloff. Only the pandemic caused a worse relative performance.

JPMorgan

The chart above also shows that the higher interest rates are, the more the market tends to favor value stocks. This makes sense as well, as elevated rates and inflation favor companies that have elevated cash flows instead of companies that are expected to generate elevated free cash flow at some point in the future.

In general, discounting future cash flows becomes much more attractive when rates and inflation are low.

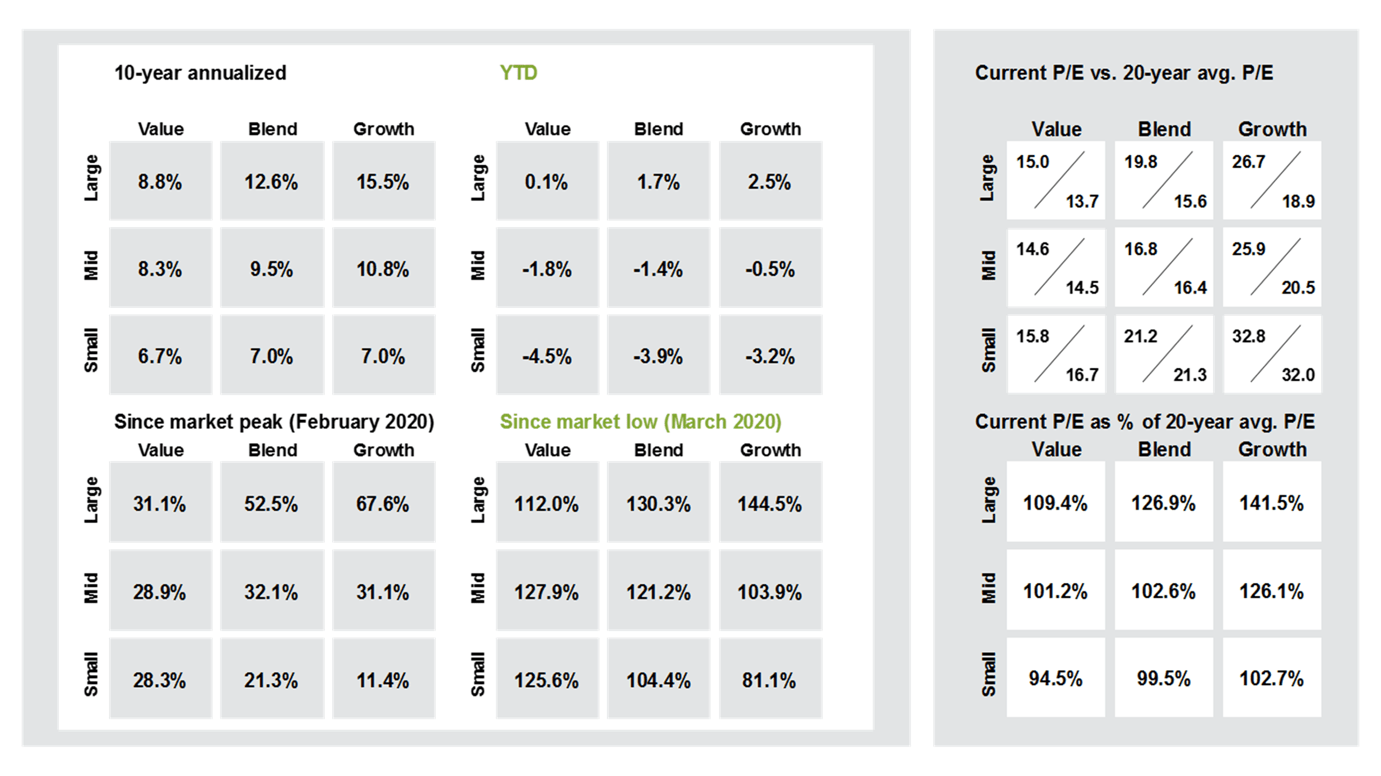

Furthermore, as we can see below, value stocks are trading close to their 20-year average valuation. Growth stocks trade up to 42% above their 20-year average valuation.

The cheapest stocks on the market are small-cap value stocks.

JPMorgan

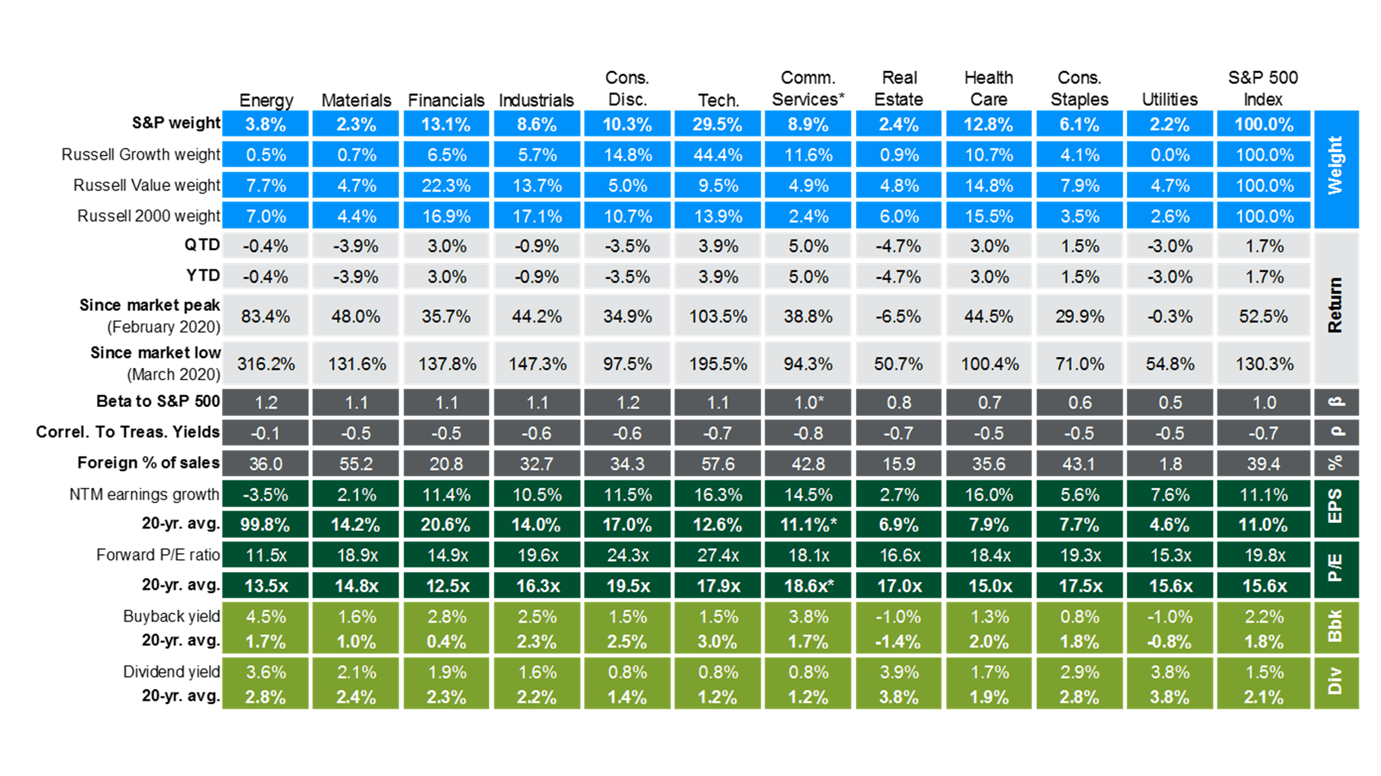

Right now, my favorite value sector is energy, the cheapest sector in the S&P 500 with a forward P/E ratio of roughly 11.5x, 15% below its 20-year average!

Meanwhile, it has a buyback yield of 4.5%, 2.8 points above its 20-year average, and a dividend yield of 3.6%, 0.8 points above its 20-year average.

JPMorgan

However, it's also the only sector with negative earnings growth, which is due to the decline in oil prices from elevated levels, which makes the sector look worse than it actually is.

The moment earnings growth improves, energy becomes even more attractive than it already is.

The energy industry is huge!

According to Kings Research, the global oil and gas market was worth $6.6 trillion in 2022, with North America being the biggest market and APAC nations providing the most growth.

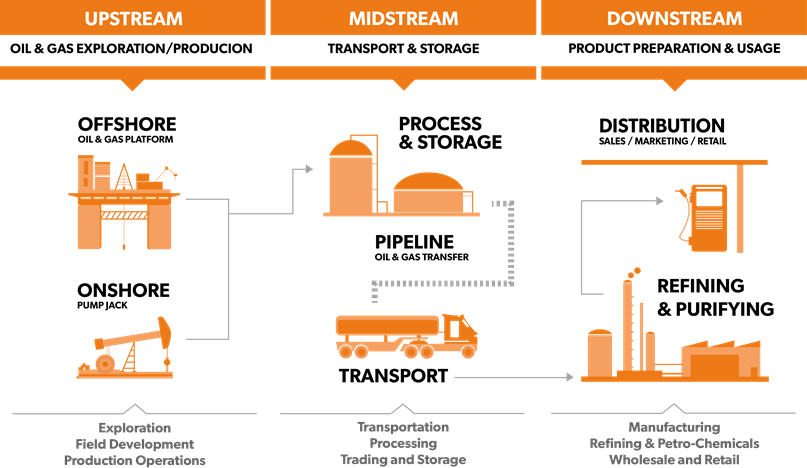

Size also comes with complexity.

After all, there are many industries in the energy sector.

Eland Cables

But wait, there's so much more!

The market also includes companies like Helmerich & Payne (HP) that provide drilling rigs for oil and gas production, companies like SLB (SLB) that support a wide range of drilling services, and companies that own land or mineral rights allowing companies to produce oil in the first place.

After covering a wide range of companies in upstream and midstream, this article focuses on companies that own land and mineral rights, a great place to buy income and growth.

A royalty interest in the oil and gas industry involves owning a share of resource ownership or revenue without having to deal with operational costs.

Essentially, it means getting a share of the pre-expense revenue from a barrel of oil or equivalent produced by an upstream company.

It's comparable to the music industry, where people can buy music royalties, making a few pennies whenever their song is played on the radio or streamed.

According to Investopedia, unlike a working interest, which requires investment in operational expenses, a royalty interest covers only an initial investment with no ongoing liabilities.

Typically, smaller companies lacking resources or technology to develop oil fields opt for royalty-interest agreements.

These agreements benefit both parties, with the producer paying the field owner royalties once resources are developed and sold.

Using Pheasant Energy data, typical royalty rates are 20% to 25% in Texas. The Texas/New Mexico Permian and North Dakota Bakken basins have royalty rates between 18% and 20%.

Most Western states charge royalties of 17%.

With that in mind, when it comes to royalty investments, I care for two things:

In other words, I want royalty plays that can benefit from output growth on the land they own or have mineral rights to.

I'm also expecting longer-term higher oil prices. If I did not expect that, I would put my money in other areas with elevated yields that do not rely on the price of oil. After all, the higher the price of oil, the higher the royalty payments will be.

I don't have to buy oil and gas royalties to buy income.

For example, I own Antero Midstream (AM), which owns the natural gas infrastructure of Antero Resources (AR) and pays 7% per year. This comes with limited commodity price risks.

I can also buy high-yield stocks like Realty Income (O) that yield 6% without any cyclical risks.

The reason why I started buying oil and gas royalties on top of my upstream and midstream holdings is my belief that some offer the perfect mix between pricing and volume tailwinds.

For starters, on November 21, we published an article on our Investing Group titled "2 Special Dividend Energy Plays We're Buying Hand Over Fist."

In that article, I explained why I have become very bullish on oil prices starting in 2020.

Furthermore:

"Now, the shale revolution is running out of steam. Although we are not even close to a scenario where the U.S. is running out of reserves, we're beyond peak growth, which is one of the reasons why WTI crude oil is still trading above $70 despite economic challenges.

This is also great news for OPEC, as it has regained pricing power.

Estimates are that without additional drilling, non-OPEC production will see a rapid decline through 2030!"

Generally speaking, the outlook of peaking production growth isn't great for (SOME) royalty plays. After all, we want to buy companies in areas with rising output to benefit from both volumes and pricing!

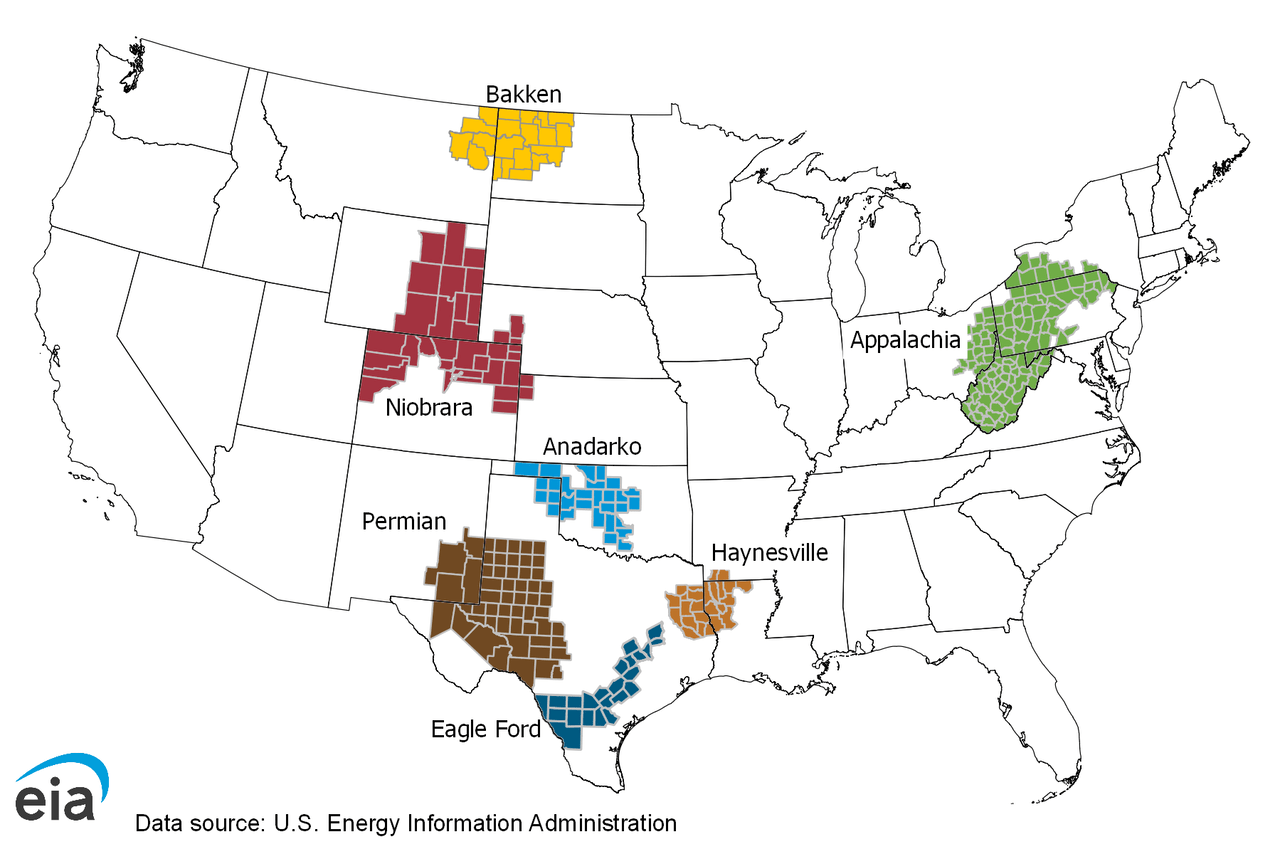

That's where the Permian comes in.

Energy Information Administration

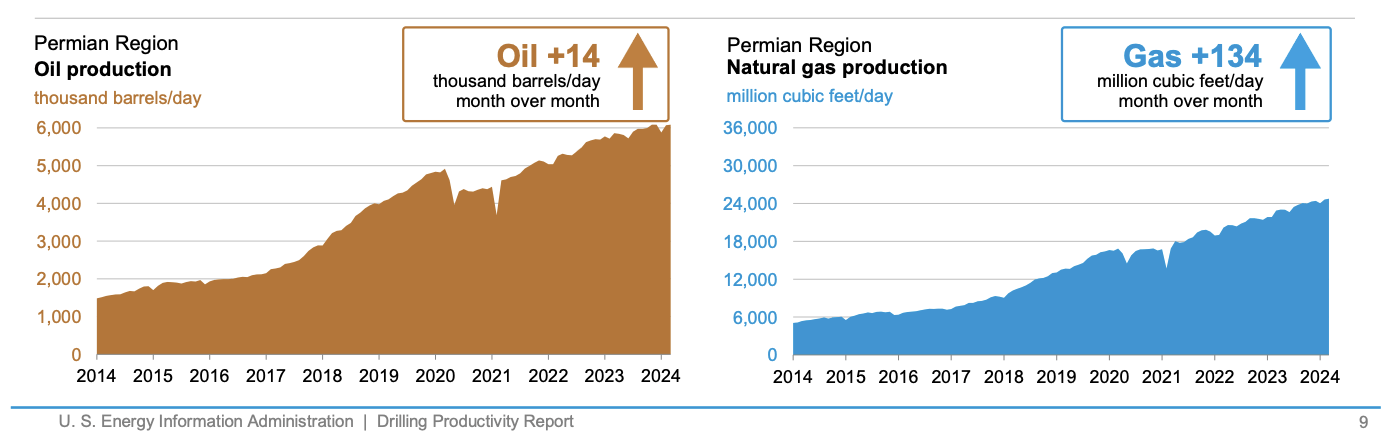

The Permian is the largest oil basin in the United States and the only basin with production growth capabilities left.

Energy Information Administration

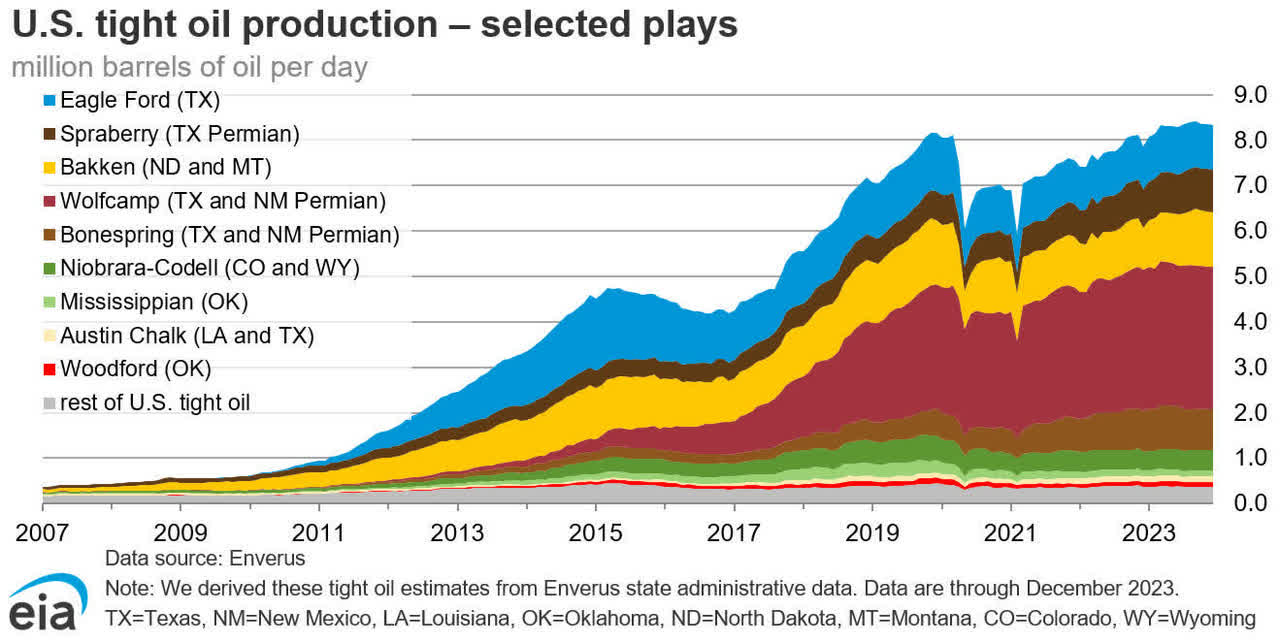

Last year, Pioneer Natural Resources (PXD) came out making the case for 7 million barrels of daily production in the basin in 2030, down from prior expectations of 8 million barrels.

Currently, the basin produces roughly 6 million barrels per day, with both oil and gas output being in a steady uptrend.

Energy Information Administration

In the Permian, we see that the "big guys" like Chevron (CVX) are boosting output.

Chevron targets 10% output growth this year, which is twice the output growth of independent producers in the area, targeting 1 million barrels of output in 2025!

Meanwhile, Exxon Mobil (XOM), which is in the process of buying Pioneer Natural Resources, grew in-basin production by 12% last year, exceeding 600 thousand barrels of production per day.

With all of this in mind, I added a new stock to my portfolio in February, which is one of the three royalty plays I prefer in this industry.

So, let's dive into our picks!

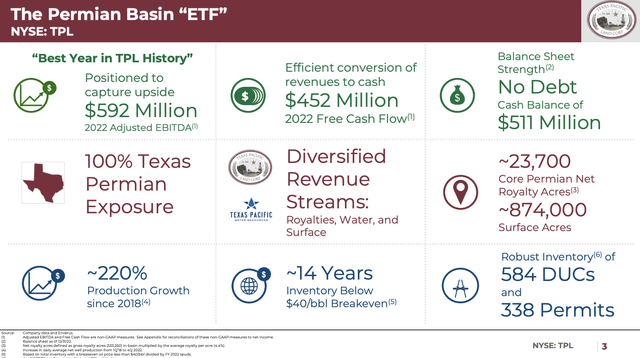

Texas Pacific Land is a fascinating company. Unlike most peers, it does not just have mineral rights, but it actually owns its land. It's a mix between an energy and a real estate stock.

Before 2021, the company was actually a REIT before it transitioned to a C-Corp.

The company, whose history dates back to 1888, benefitted from the bankruptcy of the Texas & Pacific Railway, whose assets were put into a trust for bondholders.

Now, it's one of Texas' largest landowners, owning more than 870 surface acres and close to 24 thousand net royalty acres. These assets hold roughly 14 years' worth of inventory breakeven at $40 WTI in the Permian.

Texas Pacific Land Corporation

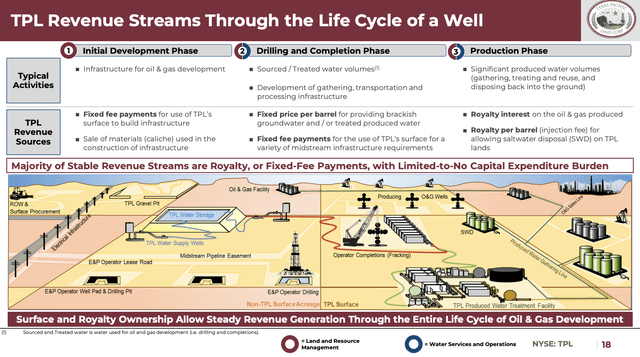

What makes TPL so special is that it benefits from every stage of the oil and gas production process.

TPL's revenue streams are multifaceted, including royalties, water, and surface income.

Its strategic positioning along the oil and gas development value chain enables the company to generate revenue across various stages of production. From fixed fee payments and material sales during initial development to royalties from oil and gas production, TPL's revenue sources are highly diversified.

Texas Pacific Land Corporation

In addition to its core operations, TPL explores alternative revenue streams, including wind and solar power projects.

Collaborating with leading developers, TPL aims to exploit renewable energy opportunities on its properties, further supporting its revenue potential and contributing to sustainable energy initiatives.

It also benefits from potential data centers on its land, pipelines, and everything related to the modern energy landscape.

Its largest customers are Occidental Petroleum (OXY), Chevron, Exxon, EOG Resources (EOG), and many others.

Essentially, it focuses on super-majors that look for consistent growth, including midstream giants like Energy Transfer (ET) and Enterprise Products Partners (EPD), which are looking to expand their pipeline network to support higher Permian production.

Texas Pacific Land Corporation

While the company has a sub-1% dividend yield and no official commitment to special dividends, there are benefits.

The company has no debt and more than $720 million in cash (6% of its market cap). It does not hedge oil production and benefits from consistent output growth.

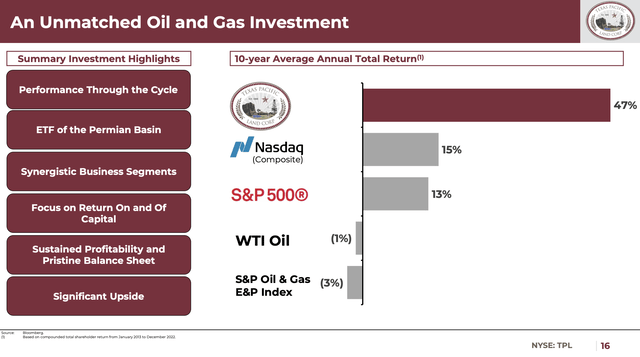

Even better, since 2004, the company has returned 28.2% per year!

Between 1Q13 and 4Q22, it has returned 47% per year despite falling oil prices during this period.

Texas Pacific Land Corporation

This is what Horizon Kinetics, the company's largest shareholder, wrote in its January report:

"There are maybe a dozen or so companies in the world like TPL, which require minimal or near-zero reinvestment of earnings in order to sustain a high and extended rate of financial return. They are tied directly to the hard assets that figure centrally in the developing global supply/demand equation."

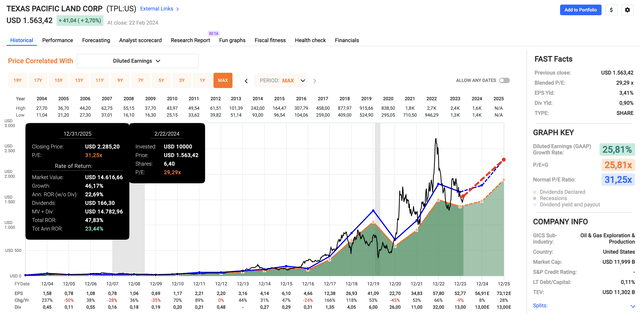

Valuation-wise, the company is trading at a blended P/E ratio of 29.3x, which may seem lofty. However, it's below its longer-term normalized multiple of 31.3x.

This year, analysts expect earnings per share growth of 8%, potentially followed by 28% growth in 2025.

This could pave the way for annual returns north of 20%.

FAST Graphs

The only major drawdown - on top of commodity-price risks - is that some investors dislike TPL's management.

While the dust is settling a bit, investors were displeased that TPL sued its largest shareholder for disagreeing with its plans to increase the number of authorized shares (mainly through a stock split).

Although TPL is not expected to dilute shareholders, some investors do not trust it to make prudent decisions with the opportunities it has.

I disagree with that, as I liked the recent earnings call and the company's decision to carefully weigh all options to improve total returns, including special dividends, buybacks, and strategic investments where needed.

As a result, I have made TPL one of my largest dividend investments.

With that said, stock number two is different yet similar.

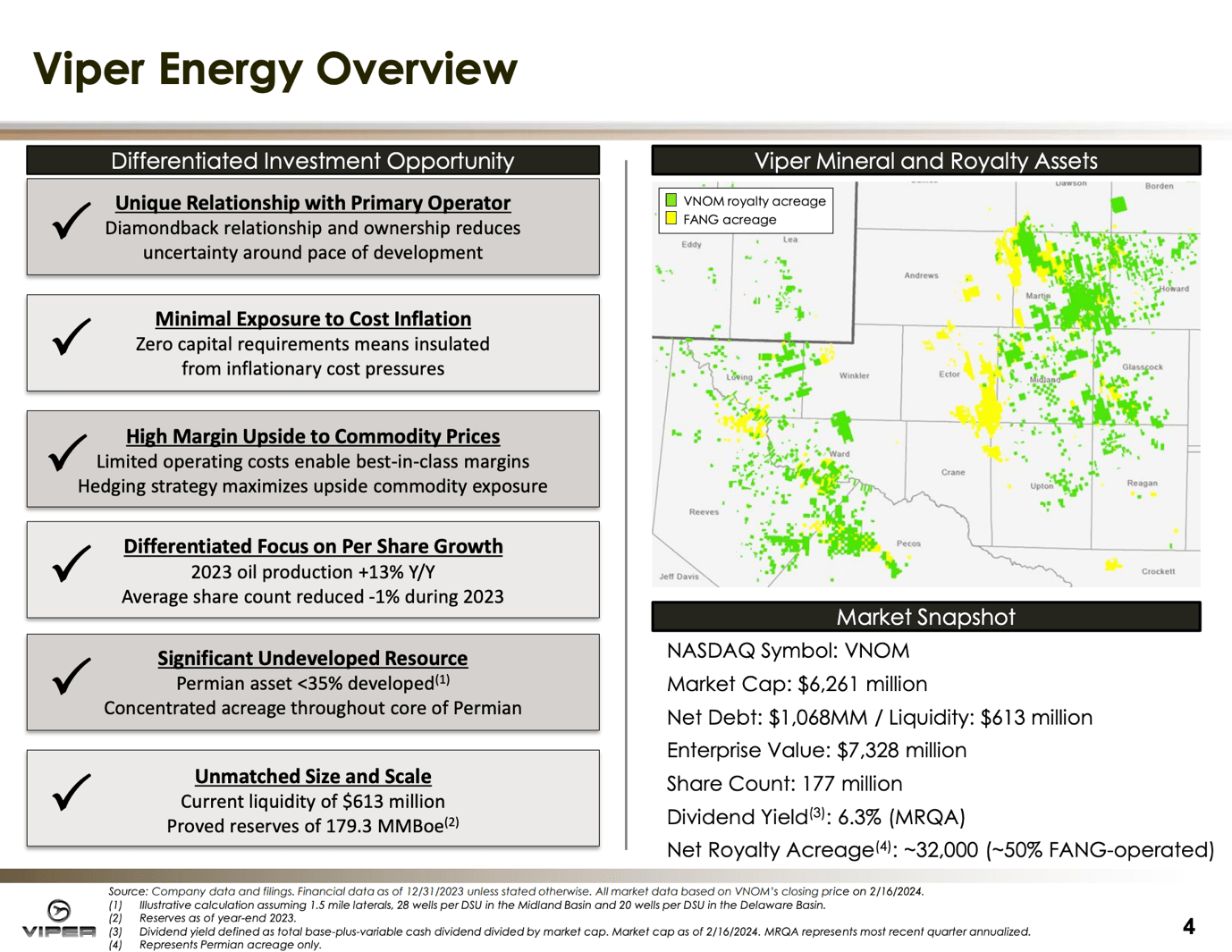

With a market cap of $2.5 billion, VNOM is much smaller than TPL. However, it is a great option for income-focused investors.

VNOM is a Delaware corporation specializing in the ownership and acquisition of mineral and royalty interests in oil and natural gas properties, primarily within the Permian Basin.

In other words, it does not own the land. It owns the mineral and royalty interest that drillers need to produce oil and gas.

The company's core objectives are focused on delivering value to shareholders by focusing on its core business, generating robust free cash flow, reducing debt, and safeguarding its balance sheet, all while maintaining a top-tier cost structure.

Viper Energy

Going into this year, the company owned roughly 32,000 net royalty acres. 50% of these were operated by Diamondback Energy (FANG), a major onshore producer.

Diamondback owns 56% of the company's total shares outstanding (including all class-B common stock).

Essentially, VNOM started as a Diamondback spinoff and could benefit from future royalty sales from FANG.

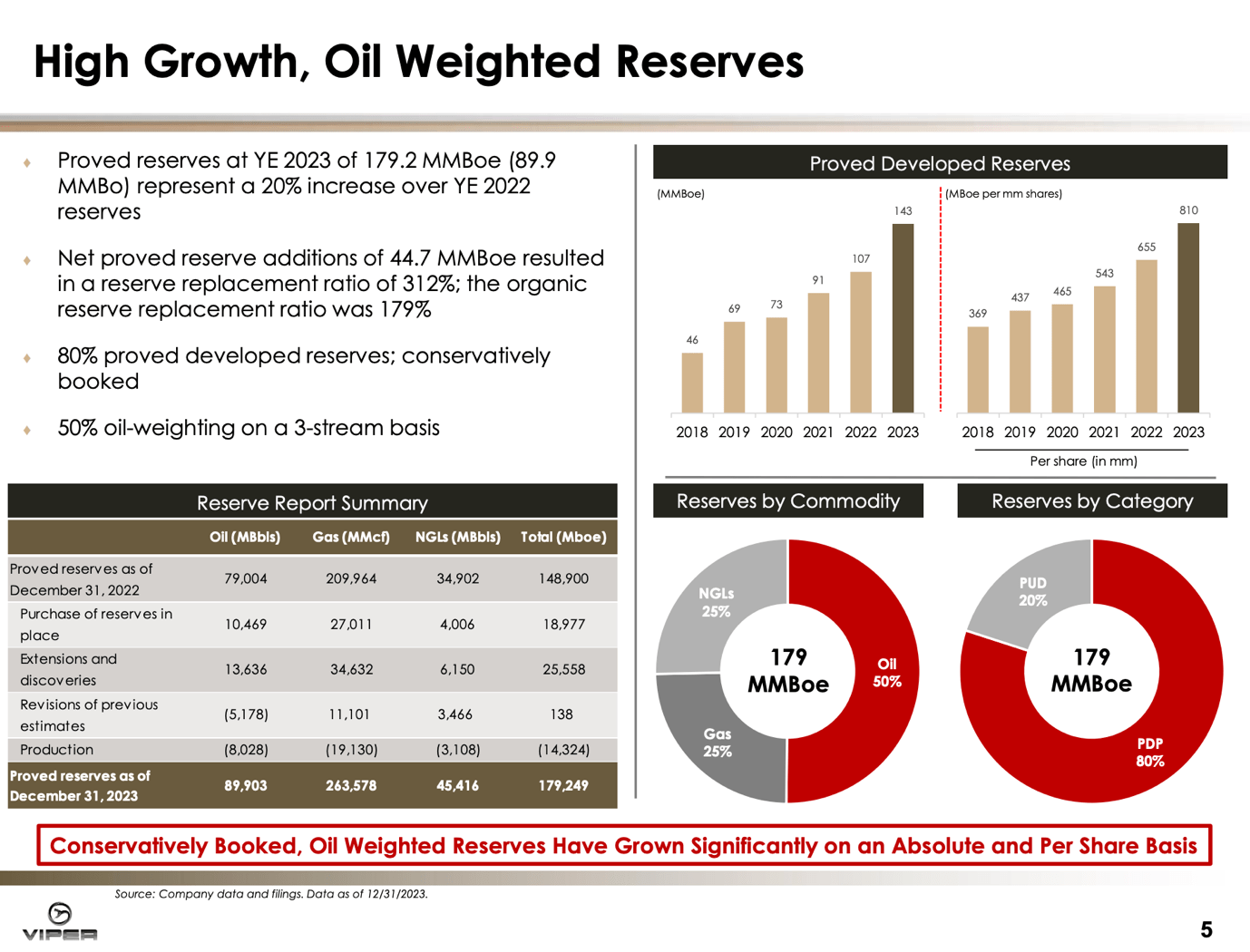

Moreover, the company has rapidly rising reserves. In 2023, reserves ended at 143 million barrels, up from 107 million barrels in 2022. Half of this consists of oil, which is beneficial for margins, as oil prices tend to be more favorable than natural gas prices.

Viper Energy

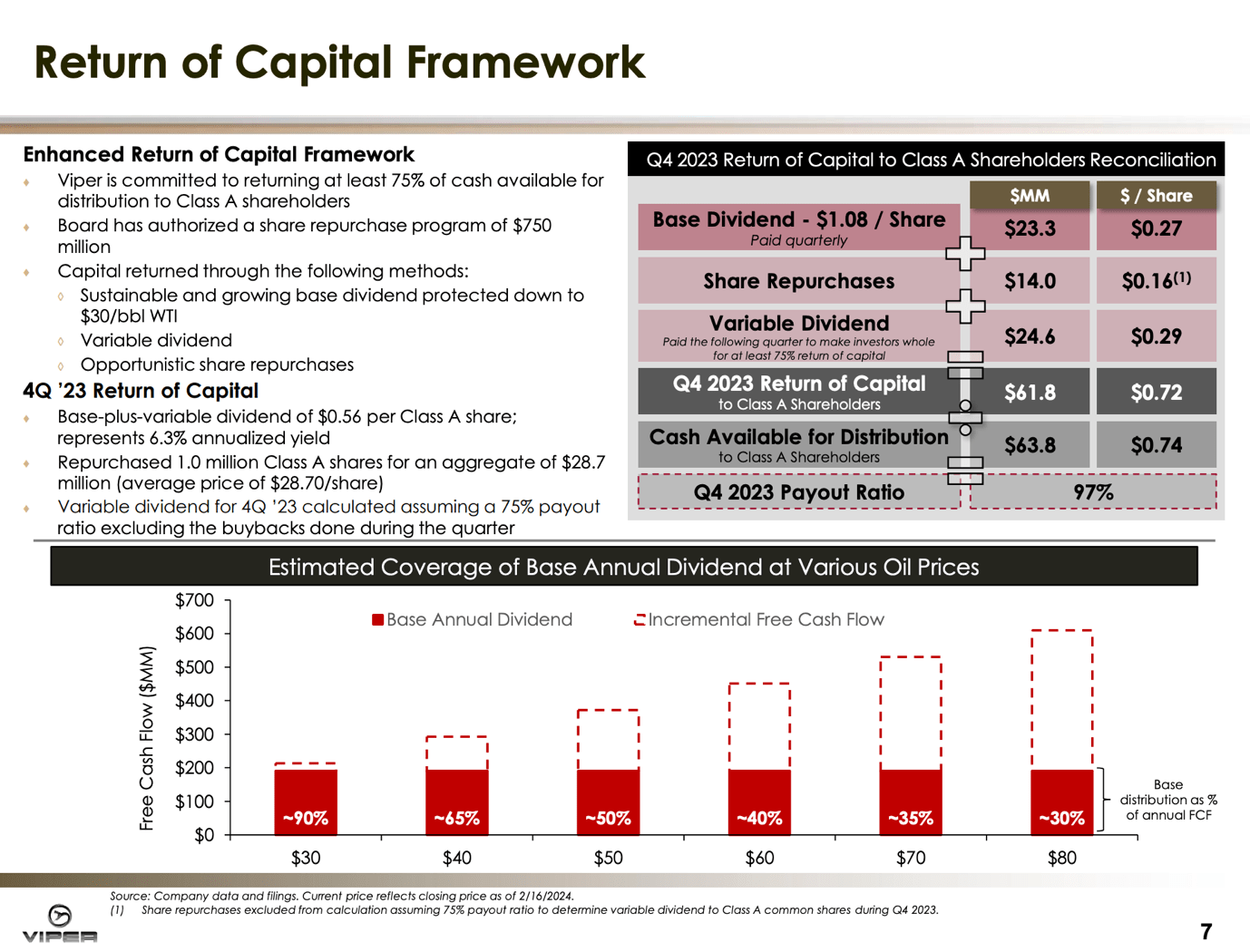

Moreover, unlike TPL, VNOM has a clear capital return framework.

The company is committed to returning at least 75% of cash available for distributions to class-A shareholders.

In 4Q23, the company returned roughly $58 million through its base dividend and special dividends. It also returned $14 million through buybacks, bringing the total payout ratio of 97%!

Viper Energy

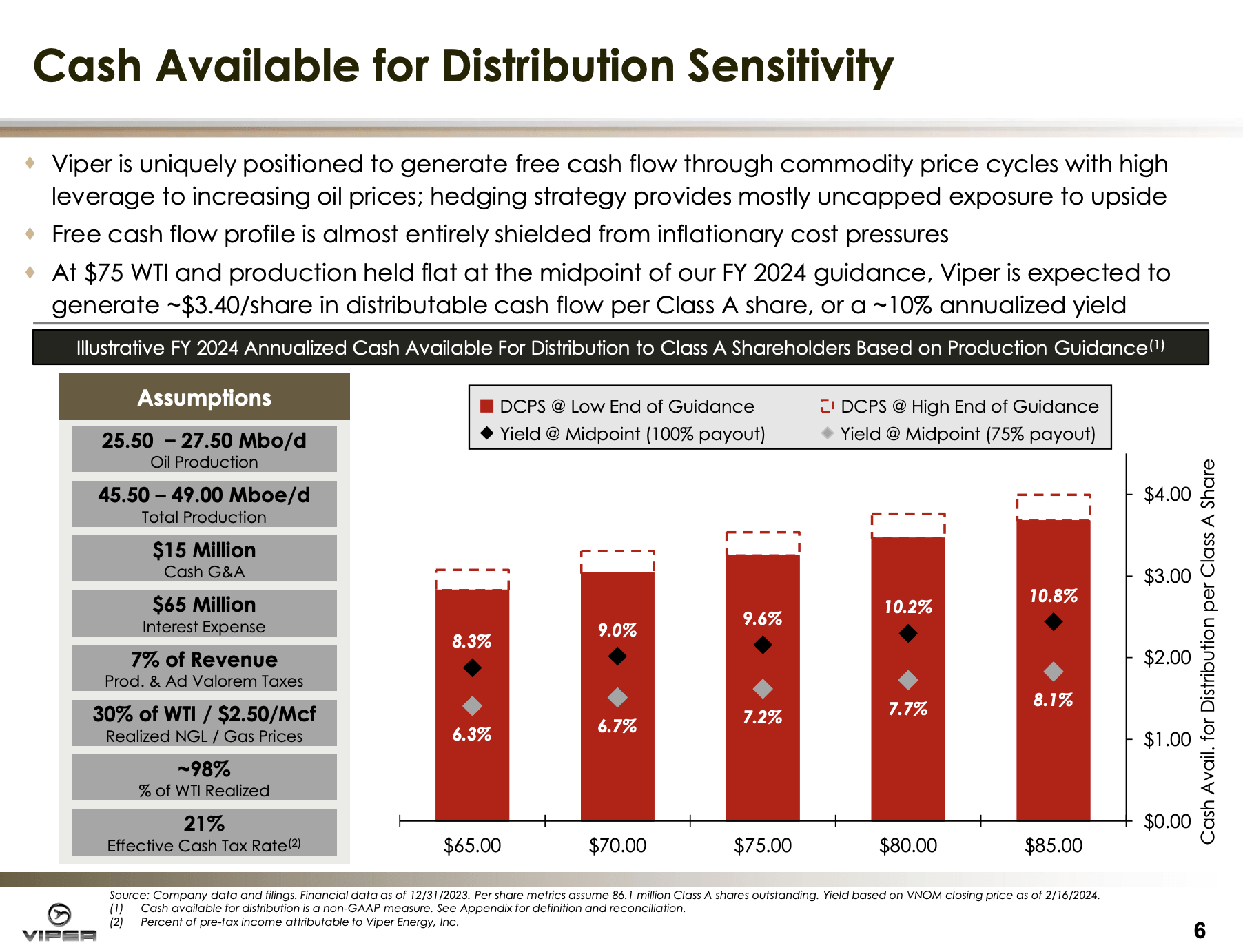

Furthermore, the company is so efficient that even at $75 WTI, it has a distribution yield of roughly 9.6%. Applying a 75% payout ratio translates to a 7.2% yield at $75 WTI.

At $85 WTI, these numbers rise to 10.8% and 8.1%, respectively.

Viper Energy

Moreover, the company is highly attractively valued.

The company currently trades at a blended P/OCF (operating cash flow) ratio of just 4.1x.

Even using conservative estimates, the company seems to be at least 20-30% undervalued in an environment of moderate oil prices ($75-ish WTI).

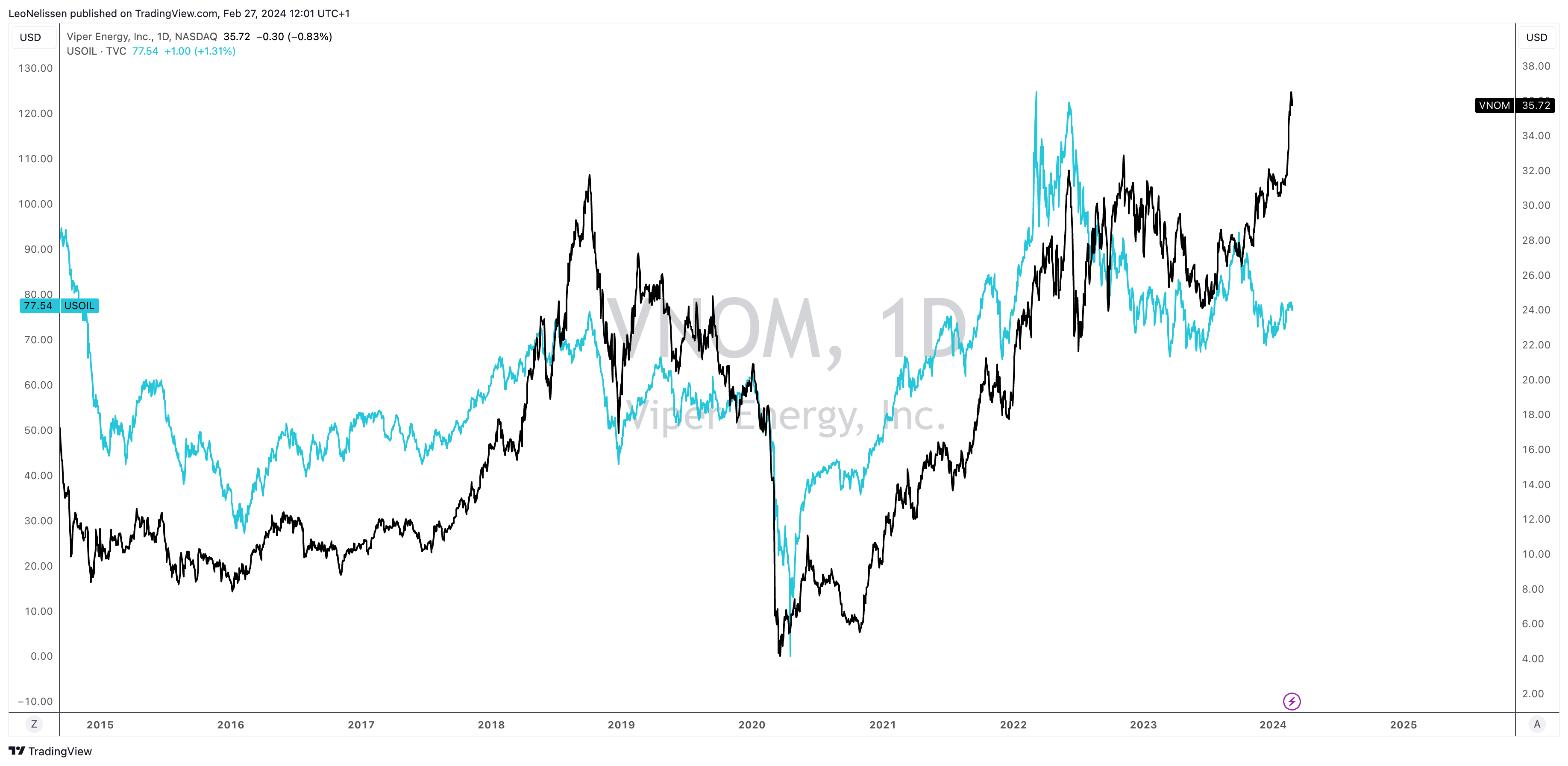

The chart below shows the total return of VNOM (the black line) compared to the price of oil.

TradingView - VNOM, WTI Crude Oil

Stock number three is a Canadian royalty play that has relationships with some of my favorite Canadian upstream players.

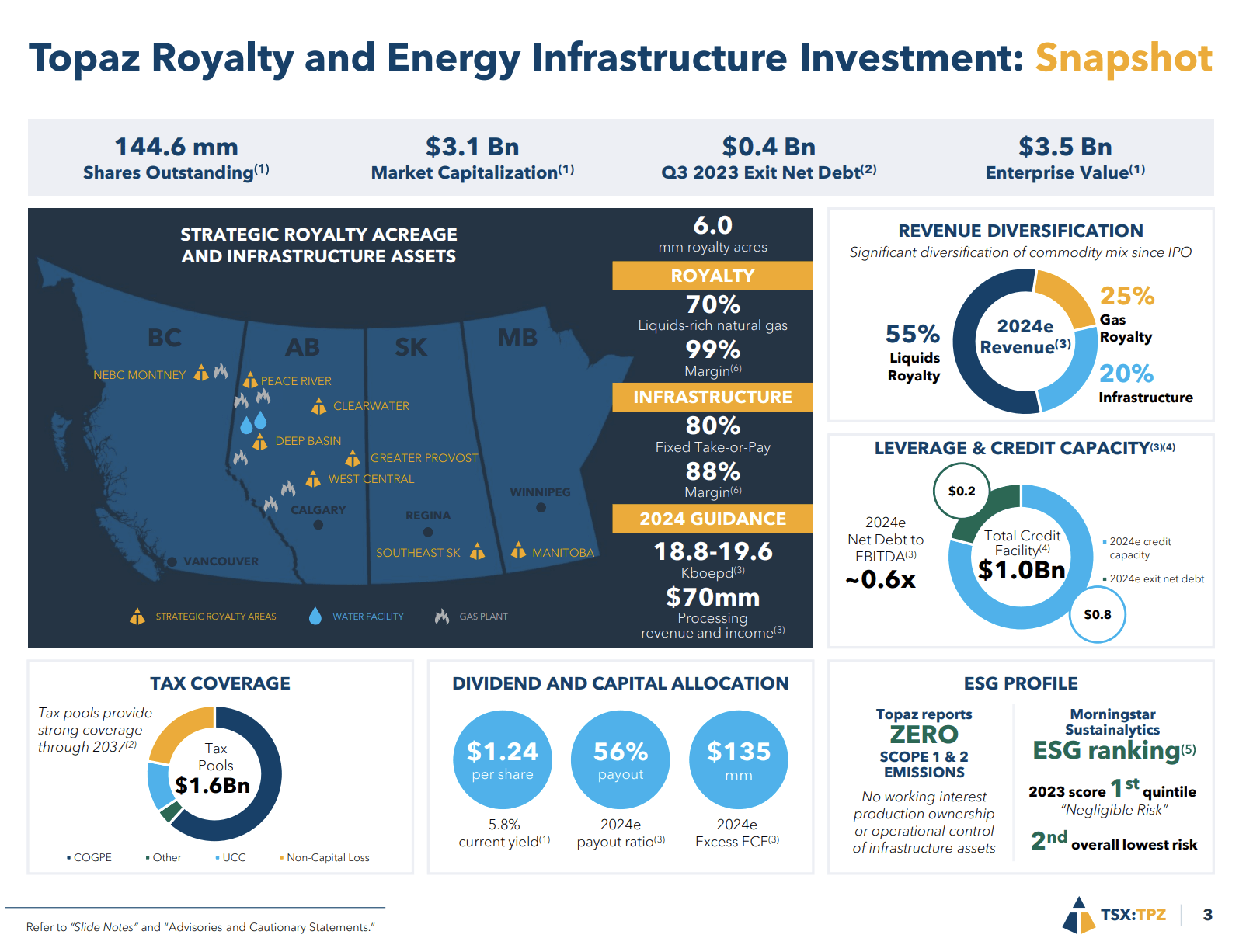

With a market cap of C$2.9 billion, Topaz is to Tourmaline Energy (TOU:CA) what Viper Energy is to Diamondback Energy.

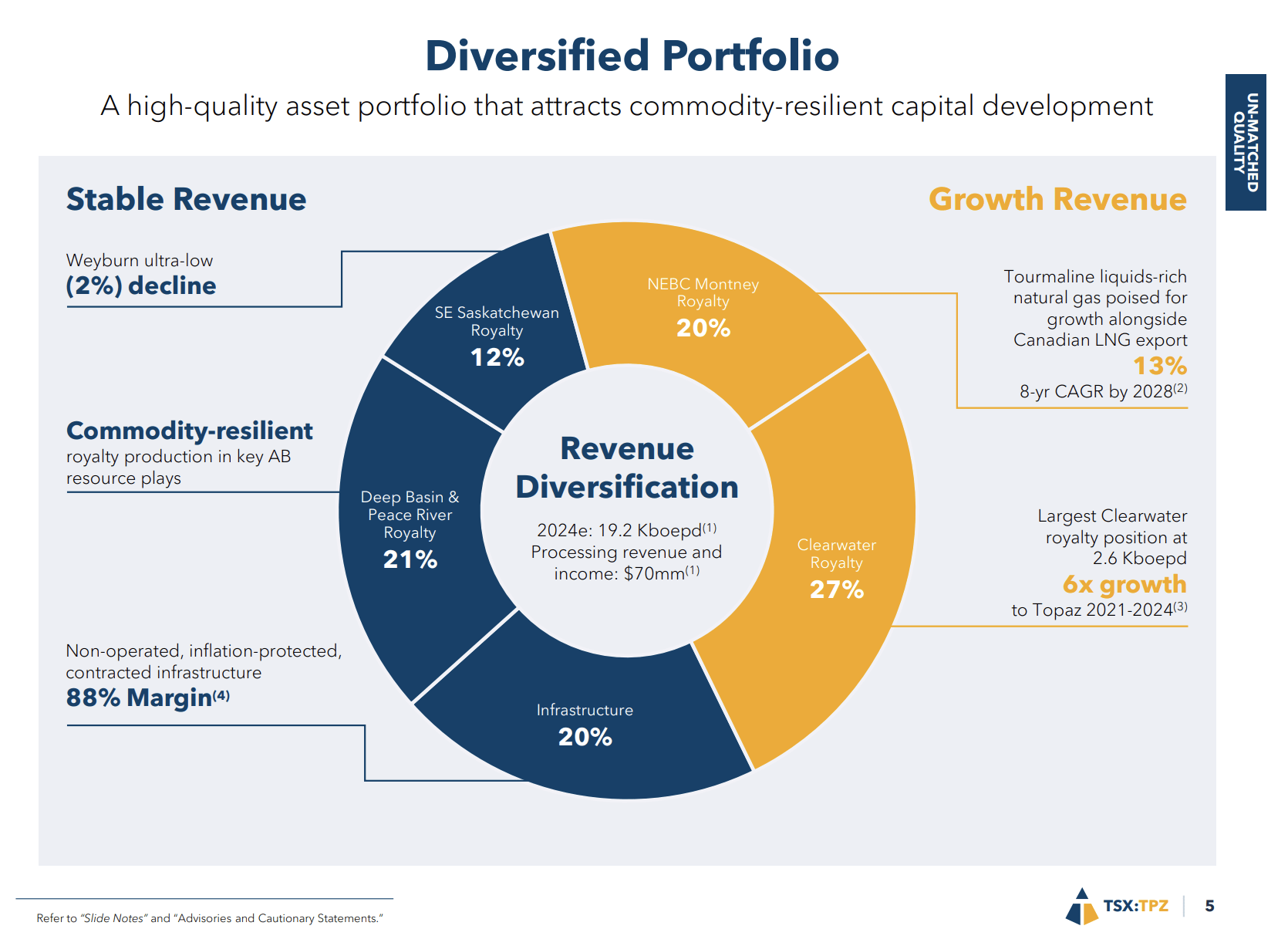

The company, which owns both land and mineral interests, is one of the largest royalty plays in Canada, a nation known for having the third-largest oil and gas reserves in the world! Tourmaline alone has more than 40 years' worth of proven reserves.

This year, the company is expected to generate 55% of its revenue from oil and NGL royalties, followed by natural gas and infrastructure income.

Its operations span 6 million royalty acres, filled with liquids-rich natural gas and the need for infrastructure to increase output.

It has 99% royalty margins and 88% infrastructure margins.

Topaz Energy Corp

Because of its network, the company expects to see between 30% and 40% production growth by 2028 without additional capital requirements!

On top of that, its income is not only benefitting from high margins but also from low decline rates, which is typical in Canadian operations. Even better, its NEBC Motney royalty operations are expected to benefit from 13% annual output growth thanks to Tourmaline's aim for higher growth.

Topaz Energy Corp

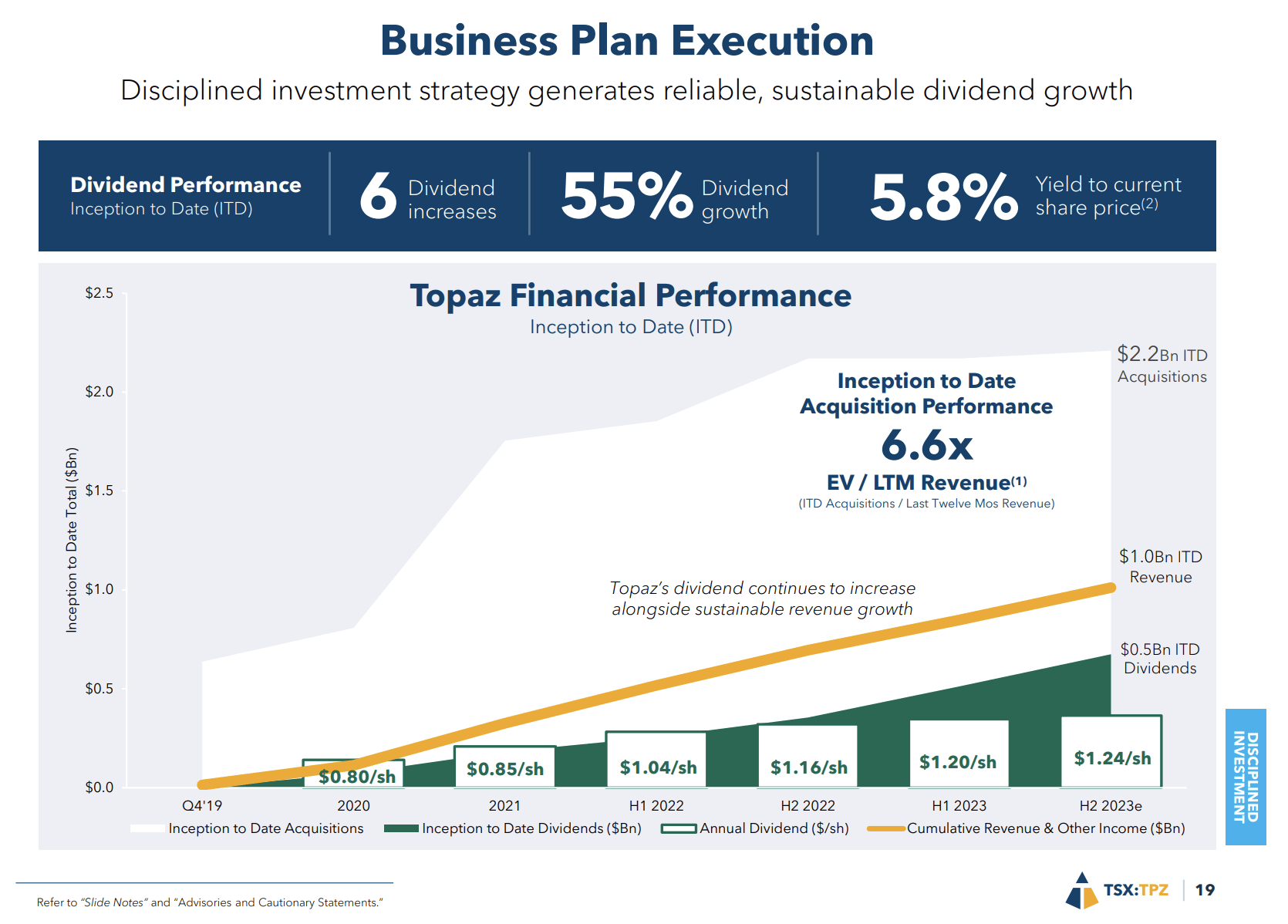

When it comes to capital allocation, the company aims for a payout ratio of 60% to 90%. It has full-dividend coverage at $55 WTI and C$0.50 AECO.

The AECO spot price is currently at C$1.55.

Speaking of its dividend, Topaz currently pays C$1.24 per share after six consecutive dividend increases with a 55% payout hike. It currently yields 6.1%. It has a 2024E payout ratio of just 56%!!

Topaz Energy Corp

The company, which currently trades at a blended P/OCF ratio of 10.1x, is expected to grow its OCF by 4% this year, potentially followed by 10% growth in 2025.

While these numbers are subject to changes in oil and gas prices, analysts are upbeat, applying a consensus price target of C$26, which is 27% above the current price.

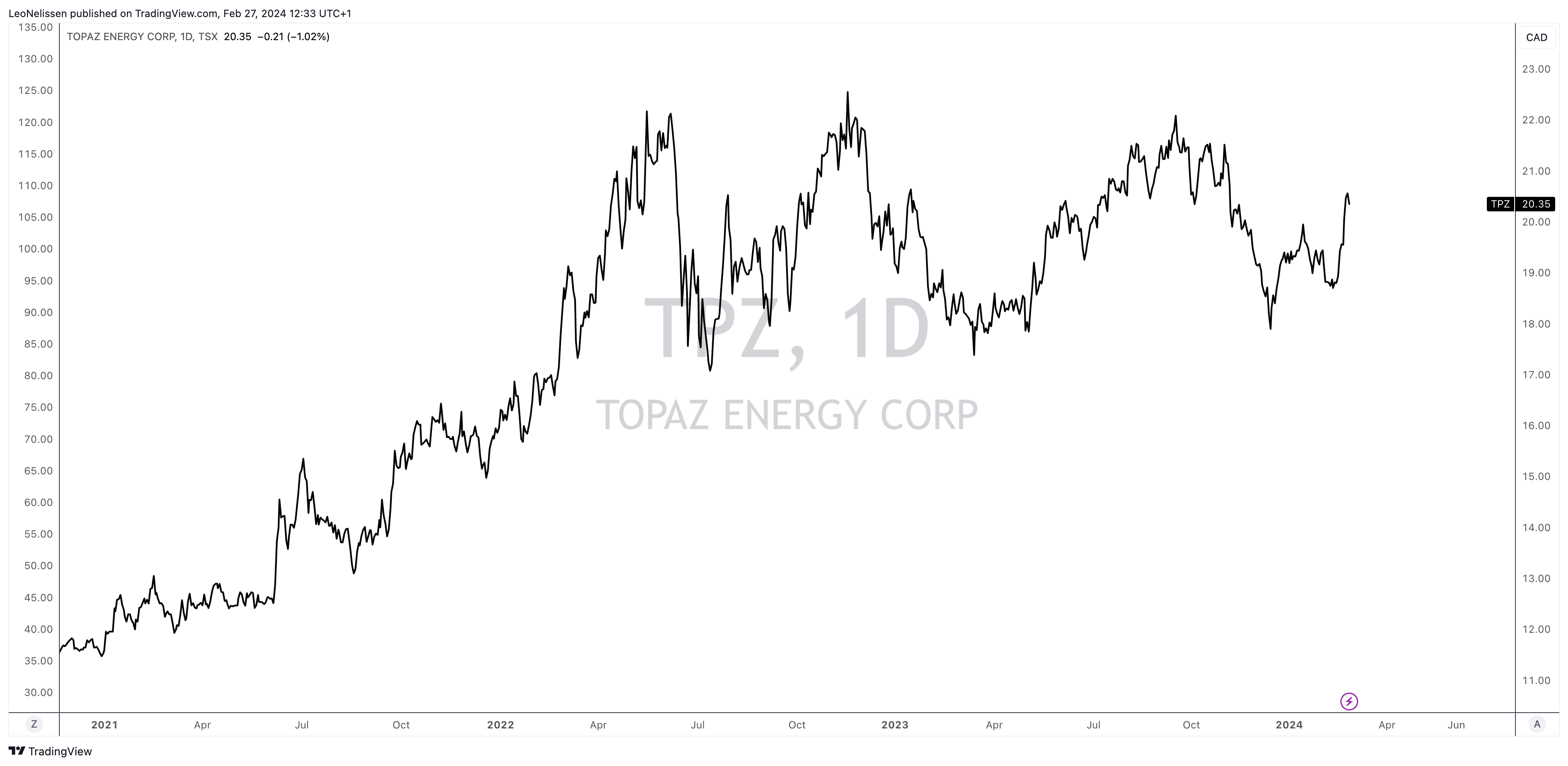

TradingView - TPZ:CA

In light of its fantastic position in the Canadian oil and gas industry, I believe TPZ is a perfect fit for portfolios looking for exposure beyond the Permian.

Investing in value stocks presents an appealing risk/reward proposition, especially amid stretched market valuations.

Especially energy stands out as a highly attractive sector thanks to its valuation.

In this case, I'm looking for royalty exposure.

Royalties in the oil and gas industry offer a unique investment angle, providing passive income without operational involvement. These agreements grant investors a share of resource revenue, typically without the burden of elevated operational expenses, making them particularly attractive in regions like the Permian Basin with projected production growth.

Three stocks stand out.

All things considered, these stocks are in a fantastic spot to deliver elevated long-term total returns in a highly attractive sector.

Going forward, we will continue to focus on this area with more in-depth research.

I am long TPL.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.