Rost-9D

Rost-9D

TPI Composites (NASDAQ:TPIC) sells wind blades and assembly systems to OEMs worldwide. TPIC also offers field service inspection and repair services to wind farm owners and OEM customers. It accounted for 33% of all onshore wind blades sold worldwide, excluding China. TPIC recently announced its Q4 FY23 and FY23 results, which I will be analyzing in this report. In my opinion, it is quite risky to invest in it for now, and I will discuss the reasons behind it. I assign a hold rating on TPIC.

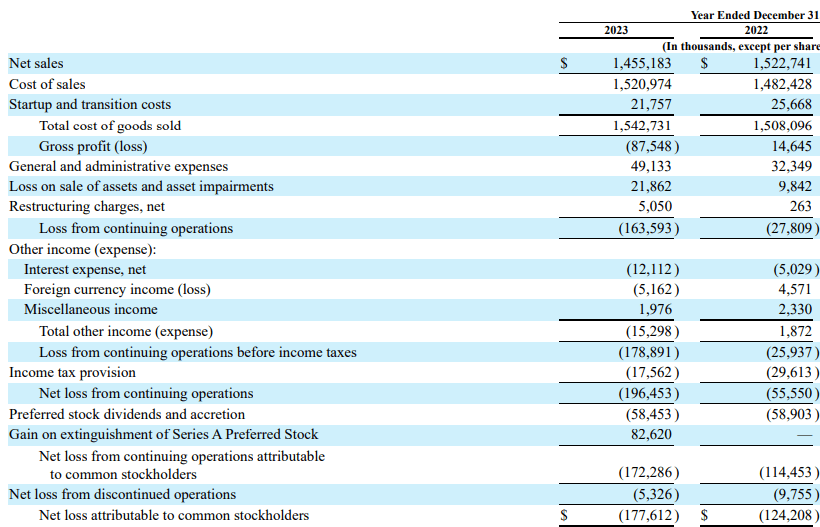

TPIC recently posted Q4 FY23 and FY23 results. The net sales for FY23 were $1.4 billion, a decline of 4.4% compared to FY22. The main reason behind the decline was underperformance in its automotive and field services segments. The automotive segment sales declined 48.2% in FY23 compared to FY22. The major reason behind the decline was Proterra's bankruptcy, which resulted in fewer composite bus bodies manufactured. The field services segment sales declined 30.6% in FY23 compared to FY22. The reason behind the decline was the increased focus on non-revenue generating repair and inspection activities. Its adjusted EBITDA for FY23 was $85.9 million, which was $37.9 million in FY22. The major reasons that contributed to the decline were the warranty campaign and higher repair costs. Its net loss for FY23 was $172.3 million, which was $114.5 million in FY22.

SEC Filings

The annual results were weak. But not only the annual, but the quarterly results were weak. The sales were down 26.2% in Q4 FY23, and the profitability also took a hit. Both annual and quarterly results showed weakness. Now, talking about FY24, I think there are some positives going into FY24. For example, in Q4 FY23, the company suffered a production slowdown due to an issue with its supplier, which has been resolved now. In addition, it has signed a supply contract with GE Vernova, extended an agreement with Vestas, and established two new production lines for Nordex, which will help it expand its reach in the European wind market. These are some positives for them going into FY24.

However, despite these positives, its FY24 sales guidance is around $1.4 billion, which is less than FY23 sales. So, the management is expecting its sales to decline in FY24, which is not a good sign for the company and its investors because its current financial condition isn't in a great position. Although TPIC has been struggling with profitability since FY19, one positive thing was its growing revenues. However, the guidance is a matter of concern because, with declining sales, its losses will widen, which can adversely affect its financial condition and share price. Even in the last quarter, its sales and profitability took a hit. So, the weak numbers in this quarter suggest that the company is now struggling, and I believe it might continue to struggle until it doesn't expand its customer base. The revenues of the company are made up of a few customers. So I think they should look to balance it out.

Trading View

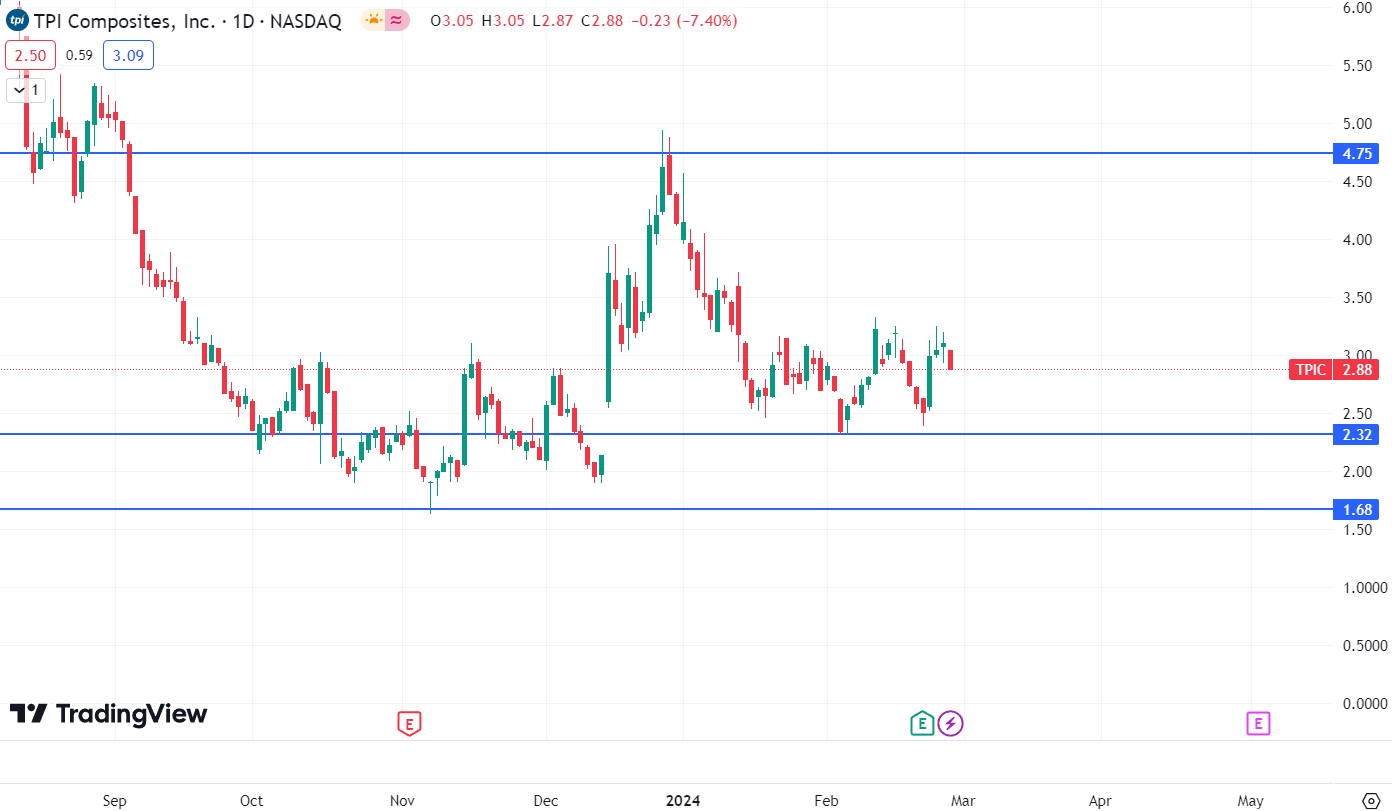

At one point, it was trading at $81, but now it is trading at $3. The chart of TPIC looks awful. It is in a continuation pattern in the long term. It forms a base first and consolidates for a while, and after consolidating, it gives a breakdown. This has been the case since 2022. Right now, it is consolidating and looking to form a base around $1.9. However, looking at the past price action, I think it cannot be assured that the stock price will stop falling. So, it might look like it has formed a base near $1.9, but there is a high possibility that it might breach the $1.9 level and continue to fall further. Hence, I believe it is best to avoid it.

The financial condition of TPIC looks weak. It has posted weak results, and the guidance for FY24 is weak. So, there is a high possibility that its financial condition might deteriorate in FY24. Its share price has fallen significantly over the past few years, and there is a possibility that it might continue to fall. Hence, I think investing in it might be risky. So, I am assigning a hold rating on TPIC. I think there is a lot of work to do for TPIC. First, I think they should work to reduce their total debt, which is around $624.3 million which also includes operating leases, and the market capitalization of TPIC is around $141.2 million. So, the debt is a problem here, and considering its financial performance, the debt becomes a major red flag.

Trading View

There are two reasons I am not assigning a sell rating to it. The first is, although its price chart is bearish now. In the weekly time frame, $1.9 is the last support level, but in the daily time frame, there is another support level before $1.9, and that is $2.32. There is a possibility that the share price might create a double-bottom pattern near the support zone of $2.32; if it does, there is a possibility of a turnaround because the stock has already fallen quite a lot. There might be a possibility that the market might have already factored in all the negatives. The second reason is that TPIC is trading at a Price / Sales ratio of 0.09x, which is quite low.

They get almost all of their income from three wind-blade customers. For the year ending December 31, 2023, GE Vernova, Vestas, and Nordex accounted for 24.6%, 35.8%, and 30.3%, respectively, of their total net sales; In FY22 the percentages were 20.8%, 36.2%, and 32.6%. As a result, they rely heavily on their present wind blade clients to stay in business. Their business, financial situation, and operational outcomes could be significantly impacted if one or more of their Windblade customers decided to cut back on or postpone placing orders or declare bankruptcy.

TPIC looks quite risky now. The results were weak, and the guidance suggests weakness in FY24. In addition, the technical chart is also bearish. Hence, I think one should avoid trading in TPIC unless we see a turnaround in its financial condition. For now, I assign a hold rating on TPIC.