Art Wager

Art Wager

The residential real estate market has fundamentally changed over the past several years. Following the pandemic, a series of changes around interest rates reshaped the landscape for home buyers. The impacts were lengthy, but boil down to the highest cost of homeownership in years. As a result, the residential real estate market has virtually frozen over the past 12 months, as both buyers and sellers attempt to digest the information.

Redfin (RDFN) provides comprehensive coverage of residential brokerage trends. In a recent article, Redfin described the slowing conditions.

Redfin

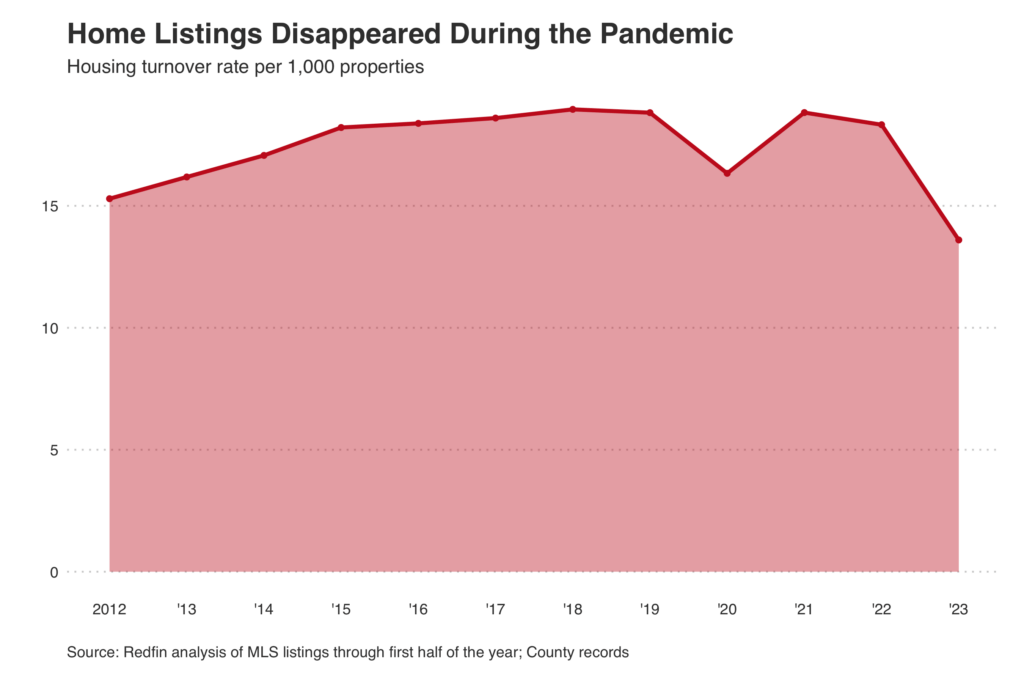

Roughly 14 of every 1,000 U.S. homes changed hands during the first six months of 2023, down from 19 of every 1,000 during the same period of 2019 and the lowest turnover rate in at least a decade. That means prospective homebuyers have 28% fewer homes to choose from than they did before the pandemic upended the U.S. housing market.

While the storm continues as buyers and sellers attempt to understand the new developments, there is clear opportunity as the demand for single family homes remains high. Homebuilders continue to perform remarkably well amidst a challenging financial environment. As listings have nosedived over the past year, demand for newly constructed homes has elevated as buyers continue to trend towards single family home ownership.

Single family home development rates are showing signs of recovery as stabilizing mortgage rates and a lack of inventory are catalyzing a gradual upward trend, according to the latest findings from the National Association of Home Builders. Broadly speaking, new developments are trending upwards for single family, following several hot years of multifamily development. According to NAHB Chief Economist Robert Dietz,

“Single-family construction showed gradual growth across much of the nation in the fourth quarter compared to the previous quarter, and this positive movement corresponds with our latest builder surveys. Meanwhile, new multifamily building in large, metro suburban counties posted a negative growth rate of 20% in the fourth quarter, reflecting the tail end of an apartment building boom that reached its highest level in more than 50 years.”

The annual growth rates for single family markets had been trending positively throughout 2023 following a dramatic drop off. In the multifamily sector, growth rates were negative or stagnant in primary and secondary markets, while growth rates exhibited the strongest readings in lower density areas.

Homebuilders have advanced over the past year as rising home prices and solid new demand for homes drove performance in an unaccommodating environment. Several trends helped push demand for new supply amid market transformations stemming from the pandemic.

Changing labor patterns stemming from remote work have been a significant catalyst in the homebuilding industry. Higher demand emerged in areas that were further from urban centers, as workers sought other amenities including more space and room for leisure.

In addition, the number of families or people seeking to buy their own home grew as a result of lower financing costs and increased household net worth. The elevated demand outpaced the supply of new housing being built during the same period.

Despite a strong fundamental market, homebuilders faced several significant headwinds during the year. Increasing interest rates sent the average mortgage rate to the highest level of the 21st century. Elevated mortgage rates made financing more difficult or expensive for new buyers, limiting the demand for homes. Additionally, homeowners with low rate, fixed debt are reluctant to sell and move to a more expensive mortgage. Finally, inflation also weighed heavily. The price of building materials rose and lumber prices surged as inflation raged. Luckily, costs have since moderated. A difficult labor market growth also led to higher costs. Homebuilders struggled to find talent amid rising wages and labor shortages, particularly in low skilled labor.

Despite these challenges, low inventories of current listings benefited homebuilders significantly. Lower supply led to elevated prices, supporting healthy margins for builders. Elevated margins permitted homebuilders to offer discounts to new buyers while maintaining positive margins.

This industry appears strong as large institutions also appear bullish. Let’s explore recent developments.

Blackstone (BX) and Tricon Residential (TCN) entered into an agreement under which Blackstone Real Estate Partners X and BREIT will acquire Tricon. The pricing of the transaction represents a 42% premium over the VWAP of the previous 90 trading days, corresponding to a $3.5 billion equity transaction value. BREIT will hold its approximately 11% ownership stake after close.

Tricon builds homes and apartments for rent in primary markets such as Atlanta, Charlotte, Dallas, Tampa and Phoenix. In addition to an SFR housing portfolio, Tricon has an SFR development platform in the U.S. with approximately 2,500 units under development. Additionally, Tricon holds land banks to support the future development of over 20,000 units. Under Blackstone’s ownership, the Tricon plans to follow through on its $1 billion domestic development pipeline.

We believe Blackstone’s acquisition of Tricon is a clear sign that BX anticipates a broad recovery in the residential real estate space. BX continues to favor the trend towards single family rentals as home affordability continues to plummet across the nation.

Stock buybacks are important. Buybacks reduce shares outstanding, which drives up earnings per share in isolation. Buybacks are easily accretive, offering a low risk way to enhance share metrics.

Beyond the attractive economics, buybacks are an important gauge of management sentiment. Boards and management teams generally initiate buyback programs when shares appear undervalued. Homebuilder activity and residential brokerage are largely fueled by monetary policy and the availability of capital. Buybacks are a mechanism to deliver returns in a challenging environment where the public could struggle to transact on newly delivered units. In other words, buybacks allow homebuilders to remain productive even during slower periods.

Let’s explore three homebuilders with large share repurchase programs.

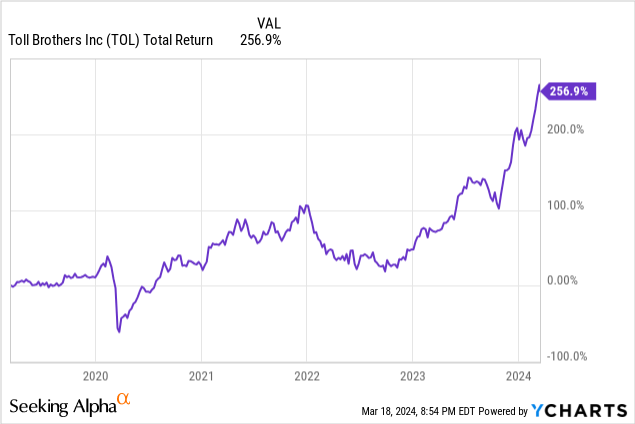

Toll Brothers is a national homebuilder specializing in designing, constructing, and selling various types of homes. Their home models include attached and detached homes throughout the United States. TOL also develops a range of condominiums through a business unit called Toll Brothers City Living. TOL also designs and delivers interior design products such as flooring, wall coverings, cabinetry, lighting, and home automation. Today, TOL is one of the largest homebuilders in the United States with over $10 billion in annual revenue.

At the end of 2023, the homebuilder approved a 20 million share repurchase program corresponding to about 18% of shares outstanding. That number is significant and will certainly move the needle at the share level. A large buyback program could have a meaningful impact. If the share count is reduced by 20 million shares, earnings per share will increase assuming performance does not decline elsewhere.

TOL also recently announced the upsize of their share repurchase program on a recent quarterly earnings call:

In addition, as I mentioned earlier, we received $181 million in cash from a land sale at the start of our second quarter. As a result, we are increasing the amount we are budgeting for fiscal 2024 share repurchases from $400 million to $500 million. Longer term, we continue to expect buybacks and dividends to remain an important part of our capital allocation priorities.

The share buybacks and strong performance of TOL also led to an increase to the dividend. TOL’s most recent quarterly dividend was $0.23 per share, a 9.5% increase over the prior quarter.

Corporate level performance was similarly strong for TOL. In the first quarter of their fiscal year, TOL delivered 1,927 homes at an average price of around $1 million, corresponding to $1.93 billion in revenue. The performance was a record for fiscal Q1 and is a 10.4% increase over the prior year’s quarter. TOL also beat on gross margin coming in at 28.9%, beating guidance and the prior year's quarter by 0.9% and 1.4%, respectively.

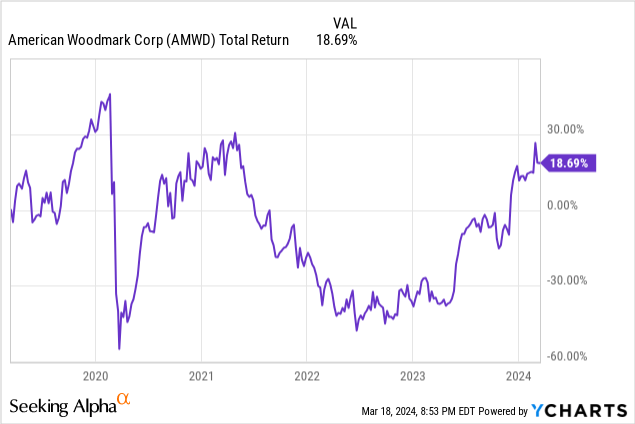

AMWD is a homebuilder-adjacent company that manufactures products for remodels and interior design segments. AMWD manufactures kitchen, bath, home office, and hardware products including cabinetry, closets, ceiling fans, and other fixtures. The company operated by selling products through an extensive network of dealers and service centers including Home Depot (HD) and Lowe’s (LOW). Common banners of AMWD products include Hampton Bay, Glacier Bay, Allen + Roth, and Home Decorators Collection.

AMWD remains strong despite challenges to its business model. Obviously, homeowners generally don’t need to mortgage a remodel, however many also do not pay cash. In fact, remodels are commonly financed with HELOCs or other floating rate loan vehicles which have been heavily impacted by rising rates.

As previously mentioned, homeowners don't need a mortgage to remodel, but they may need to take out a loan against the equity in their home – a home equity loan – and higher mortgage rates mean higher home equity loan rates, which could tamp down demand on remodeling. Last year still emerged as a record year with the highest reported net income ever. AMWD is capitalizing on their strong performance. Since May 2023, AMWD has repurchased nearly 6% of shares outstanding.

Management detailed the repurchase program on their most recent earnings call:

Under the current share repurchase program, the company purchased 19.6 million, or approximately 216,000 shares, in the third quarter, representing about 1.3% of outstanding shares being retired. For the first nine months, we have repurchased 71.8 million of the company's common shares and have 105.4 million of share repurchase authorization remaining.

AMWD has plenty of dry powder locked and loaded to continue repurchasing shares. Additionally, AMWD does not pay a dividend, meaning there is extra cash available to support the repurchase of shares.

AMWD’s underlying industry was slower as compared to direct homebuilders. Revenue for their products has slowed following a boom stemming from the pandemic and subsequent construction and renovations. Net sales for the last quarter were $422 million, a 12.2% decline over the prior year’s quarter. However, EBITDA decreased by only 0.7%, offset by improvement in product mix and manufacturing efficiencies. Despite challenges, the improvements boiled down to a 3.5% improvement to AMWD’s profit margin, increasing to 19.2% for the prior quarter.

Looking forward, AMWD anticipates additional decline as the industry-wide slowdown continues. Despite the slowdown, AMWD remains well capitalized with ample liquidity and conservative leverage. Additionally, the slowing performance still leaves room for AMWD to continue buying back shares.

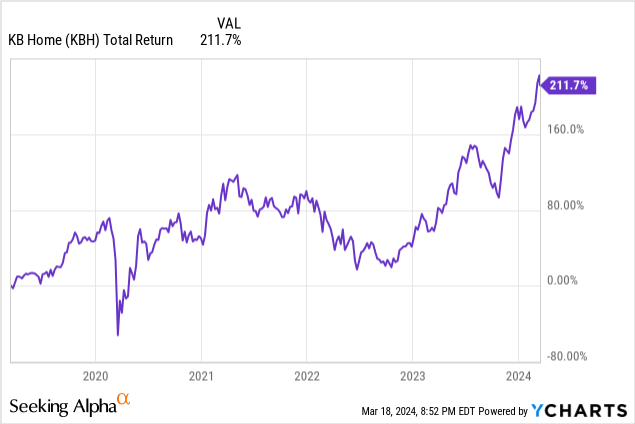

KB Home is one of the nation’s largest and oldest publicly traded homebuilders. Founded in 1957, KB Home constructs attached and detached homes throughout the United States. KBH sells attached and detached units including manufactured homes. KBH targets a variety of market segments and builds throughout most of the continental Unites States.

KBH has been a successful homebuilder for decades, however momentum has recently mounted. With significant tailwinds, KBH has changed its financial position significantly and capitalized through an aggressive share buyback program. Starting in 2021, KBH has been aggressive in repurchasing shares. Since, KBH has repurchased over 20% of outstanding shares for $750 million. Management notes that this is approximately the same amount returned to shareholders through dividend payments.

Our balance sheet is in excellent shape and we intend to continue allocating our strong operating cash flow toward reinvestment in growth and return of capital to our shareholders in 2024. Since we began our share repurchase initiative in our 2021 third quarter, we have deployed approximately $750 million to buy back over 20% of the outstanding shares at that time at an average price of $39.79 per share, which has been significantly accretive to both our book value and diluted earnings per share. During the same timeframe, included in our regularly quarterly dividends we've returned roughly $885 million to shareholders.

During the fourth quarter, we repurchased approximately 3.6 million shares of our common stock at a total cost of $162 million. For the year, we repurchased 9.2 million shares at an average cost of 11%, below our year-end book value per share. With $164 million remaining under our current common stock repurchase authorization, we intend to continue to repurchase shares with the pace, volume, and timing based on considerations of our operating cash flow, liquidity outlook, land investment opportunities, and needs, the market price of our shares, and the housing market and general economic environments.

With room to run under their current authorization, KBH has the dry powder necessary to continue moving the needle. As one of the most respected homebuilders in the business, KBH will continue to be a bellwether for the industry.

KBH noted strong performance for the past quarter in their homebuilding segment. KBH noted fourth quarter housing revenue of $1.66 billion, reflecting a decrease in both the number of homes sold and a decline in selling prices. KBH notes that economics are tightening around home sales, leading to larger discounts and concessions being provided to incentivize buyers to close transactions. Despite the slowing performance for KBH, the company was still able to repurchase over 10% of outstanding shares earlier this year, fueling book value per share growth of 15%. In addition, KBH notes $150 million in debt repayments as the company continues to reduce operating leverage.

At this point, the sentiment around the future of homebuilding is very clear. Investors across the real estate industry seem to feel as though homebuilding is a safe industry for years to come. With institutional investors of all shapes and sizes looking towards shares of publicly traded homebuilders, we can see that there is clear favor within the segment. Acquisitions and share buybacks are a leading indicator that the current valuation of these companies may be low. As demand remains strong and trends towards single family home occupancy continue upward, homebuilders are a viable investment strategy to take advantage of the situation.

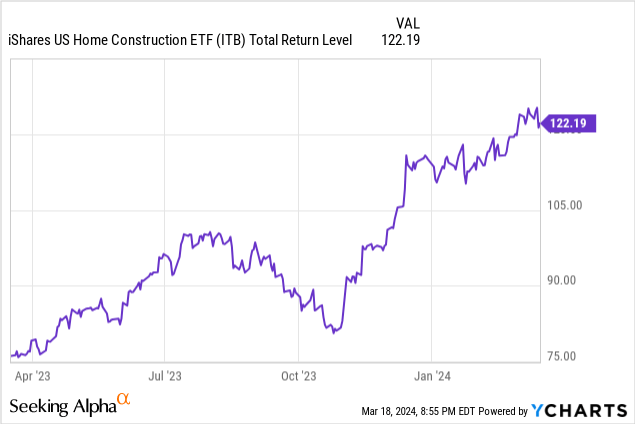

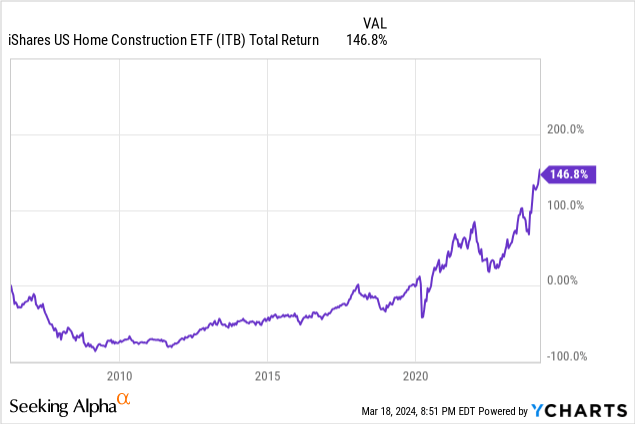

Investors looking to capitalize can dive straight into a homebuilder of their choosing. However, iShares also has a homebuilder ETF called iShares U.S. Home Construction ETF (ITB). ITB is uncharacteristically expensive for an ETF from BlackRock (BLK), charging 40 bps. However, the fund is still a viable vehicle for an indexed approach to the homebuilding industry.