Kyryl Gorlov

Kyryl Gorlov

I don't know about you, but my preference when it comes to companies I buy into is to focus on enterprises that have relatively simple business models. Instead of focusing on high tech growth firms, I tend to prefer companies that are easy to comprehend. One example of this can be seen by looking at Enerpac Tool Group (NYSE:EPAC), a business that's focused on providing customers with industrial tools, services, technology, and solutions free variety of industries. The company has been around for a long time, since 1910. While far from being the oldest publicly traded firm out there, it certainly is quite old.

Operationally speaking, the business does seem to be rather solid. And because of this, I have no doubt that it will still be here many years from now. But this doesn't necessarily mean that it makes for an attractive opportunity. Recent financial performance has been rather mixed and management expects that trend to continue. Add on top of this how pricey shares are, both on an absolute basis and relative to similar firms, and I believe that there are better opportunities to explore at this time. Of course, I could always be wrong.

The fact of the matter is that management is slated to report financial results on March 21st, before the market opens. Those results should cover the second quarter of the company's 2024 fiscal year. If that data comes in stronger than anticipated and if guidance for the year is revised higher, my attitude on the matter could change. But for now, I think that a "hold" rating is what makes the most sense at this time.

As I mentioned already, Enerpac Tool Group is an old business that's focused on industrial tools, services, technology, and solutions. This is incredibly vague. Because of this, it's probably better to dive deeper into what exactly it provides. The main products sold by the business are, according to management, branded tools, cylinders, pumps, hydraulic torque wrenches, and highly engineered heavy lifting technology solutions. The high force hydraulic and mechanical tools that the business produces "allow users to apply controlled force and motion to increase productivity, reduce labor costs, and make work safer and easier to perform." Some of them can handle as much as 12,000 per square inch of pressure while being used.

Outside of the tool space, Enerpac Tool Group also provides customers with services. For instance, it makes available its technicians for the purpose of maintenance and manpower services. Specific needs addressed include, but are not limited to, bolting, machining, and the insurance of joint integrity. Lastly, the firm has other units that focus on the production of synthetic ropes and biomedical textiles. But those are just disclosed under the "Other" segment.

Author - SEC EDGAR Data

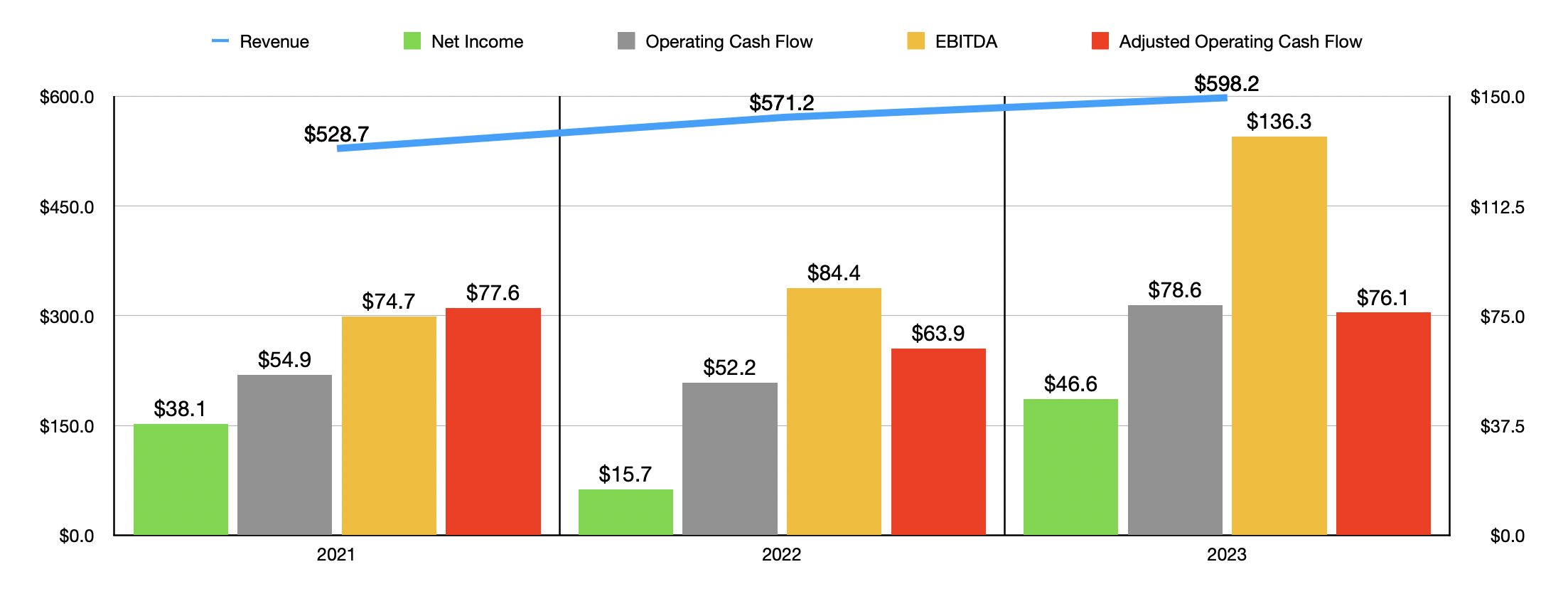

Over the past few years, management has done a decent job of growing revenue. Sales increased from $528.7 million in 2021 to $598.2 million in 2023. Sales growth would have been higher had it not been for foreign currency fluctuations. For instance, in 2023, foreign currency negatively impacted revenue by $11 million. The company also saw an asset divestiture that hit sales by $6 million.

In general, though, the increase in revenue is nice to see. And according to management, most of the increase in recent years has been driven by price increases on the product side. Unfortunately, there has been some weakness when it comes to services. The company's decision to cut back on certain projects by region was at least partially responsible for service revenue dropping by 8% year over year in 2023 compared to 2022.

With the increase in revenue, we have seen an improvement in the bottom line. But the ride has been quite lumpy. Net income went from $38.1 million in 2021 to $15.7 million in 2022. But then, in 2023, it popped up to $46.6 million. Other profitability metrics have seen similar volatility. The first chart in this article shows what these have been. Even if we adjust for changes in working capital, for instance, adjusted operating cash flow of $76.1 million came in lower in 2023 than the $77.6 million reported two years earlier. In fact, the only profitability metric that has consistently improved has been adjusted EBITDA from continuing operations. It has moved up from $74.7 million to $136.3 million.

Author - SEC EDGAR Data

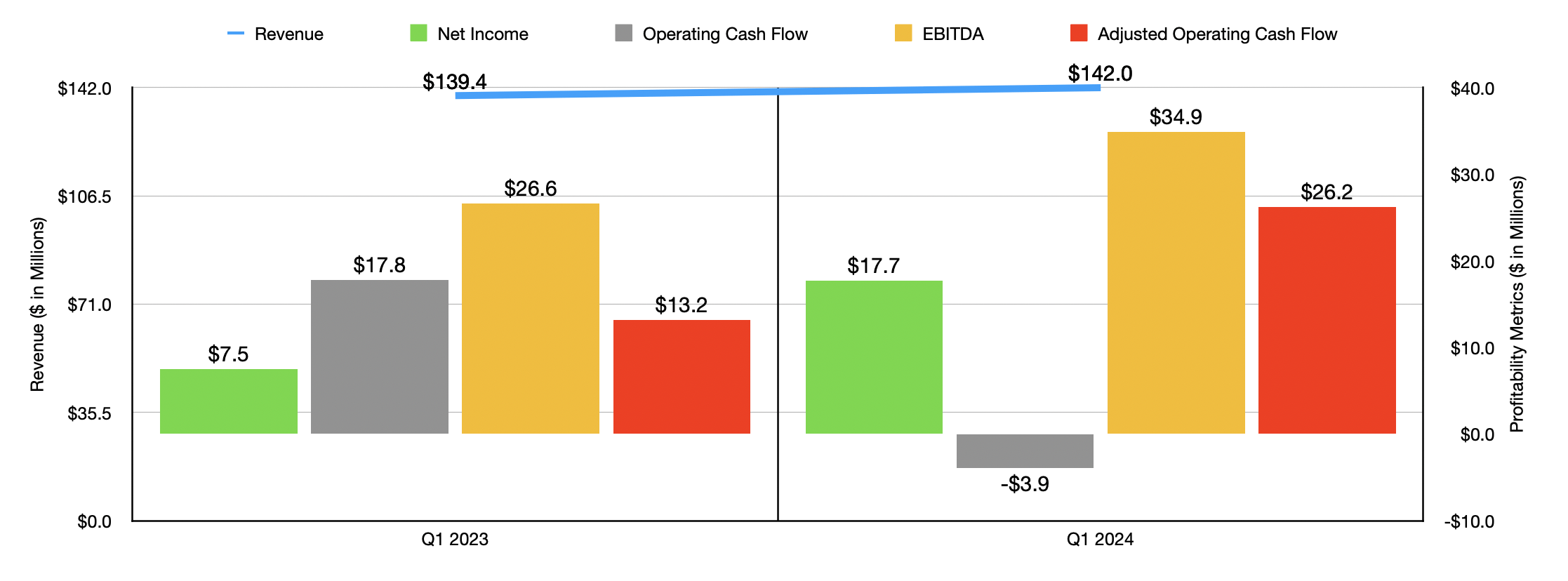

When talking about the 2024 fiscal year, we do have some data to enjoy. And this data is, for the most part, quite favorable. Revenue for the first quarter totaled $142 million. That's up marginally compared to the $139.4 million reported one year earlier. Most of that increase, however, came from a $2 million benefit associated with foreign currency fluctuations and because of a 13% rise in service sales that was driven by a 10% increase in organic demand growth.

The rise in revenue brought with it an improvement in the bottom line. Net income of $17.7 million dwarfed the $7.5 million generated one year earlier. Part of this benefit was attributable to an increase in the company's gross profit margin from 48.8% to 52.1%. That, management said, was because of operational improvements as the company works on transforming itself and because of both a favorable sales mix and higher pricing.

Even more impressive was the decline in selling, general, and administrative costs from 38% of revenue down to 29.6%. An $8 million reduction in transformation program costs, as well as a reduction in personnel costs and other items, was mostly responsible for this.

Enerpac Tool Group

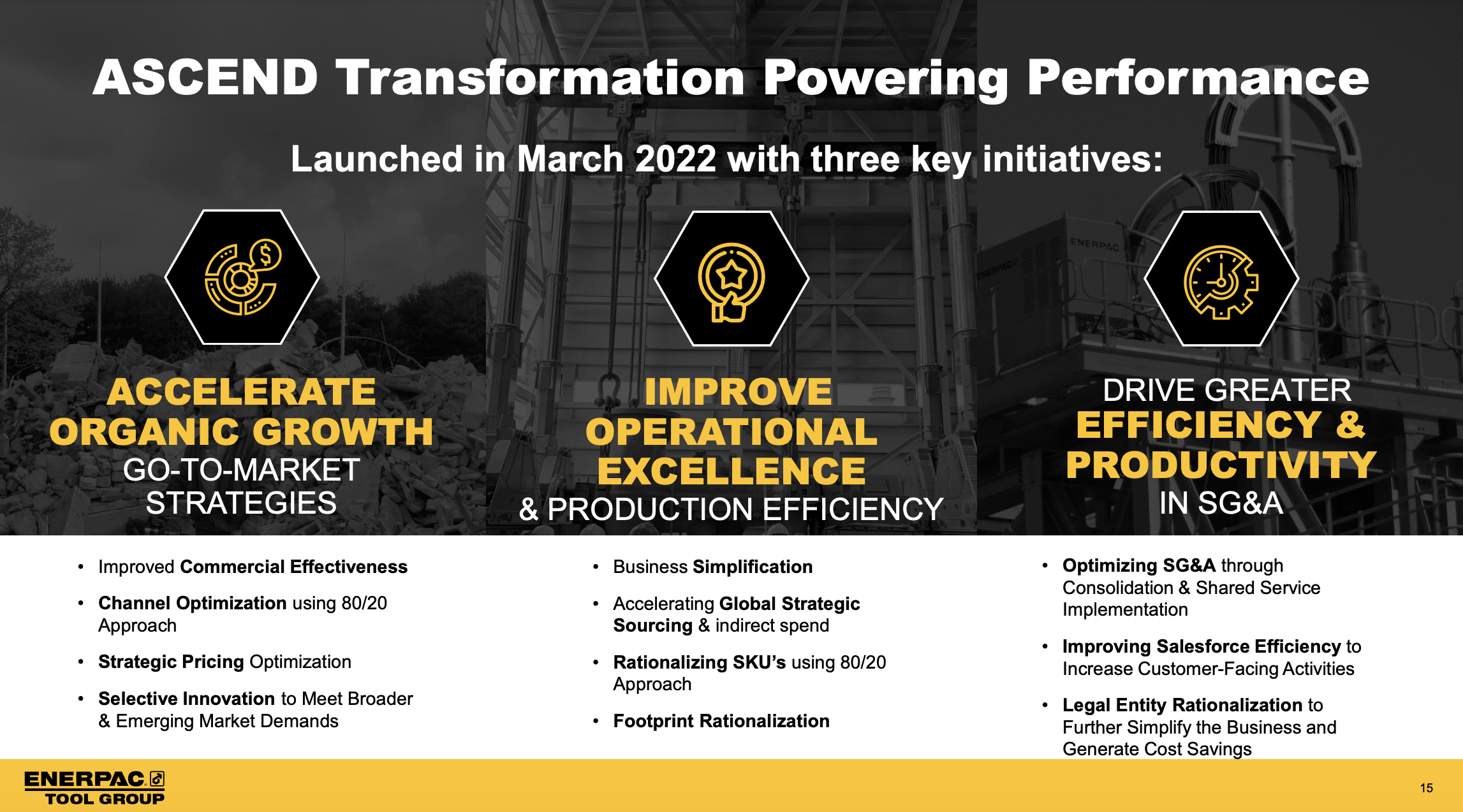

Already a couple of times, I have mentioned the company's transformation program. The name that management gave this is ASCEND, and it was launched in March of 2022. It's really centered around three primary themes. The first is to accelerate organic growth by optimizing its sales channels, engaging in strategic pricing, and being selective about innovation.

The second is to improve operational performance for the purpose of driving efficiencies, including production efficiencies. Management has been working to simplify the company's organizational structure and physical footprint. They are also working on sourcing and reducing indirect spending while rationalizing certain assets and goods and services that they provide.

And lastly, the company is working to improve efficiency and productivity when it comes to selling, general, and administrative costs. This involves consolidation for the most part.

Enerpac Tool Group

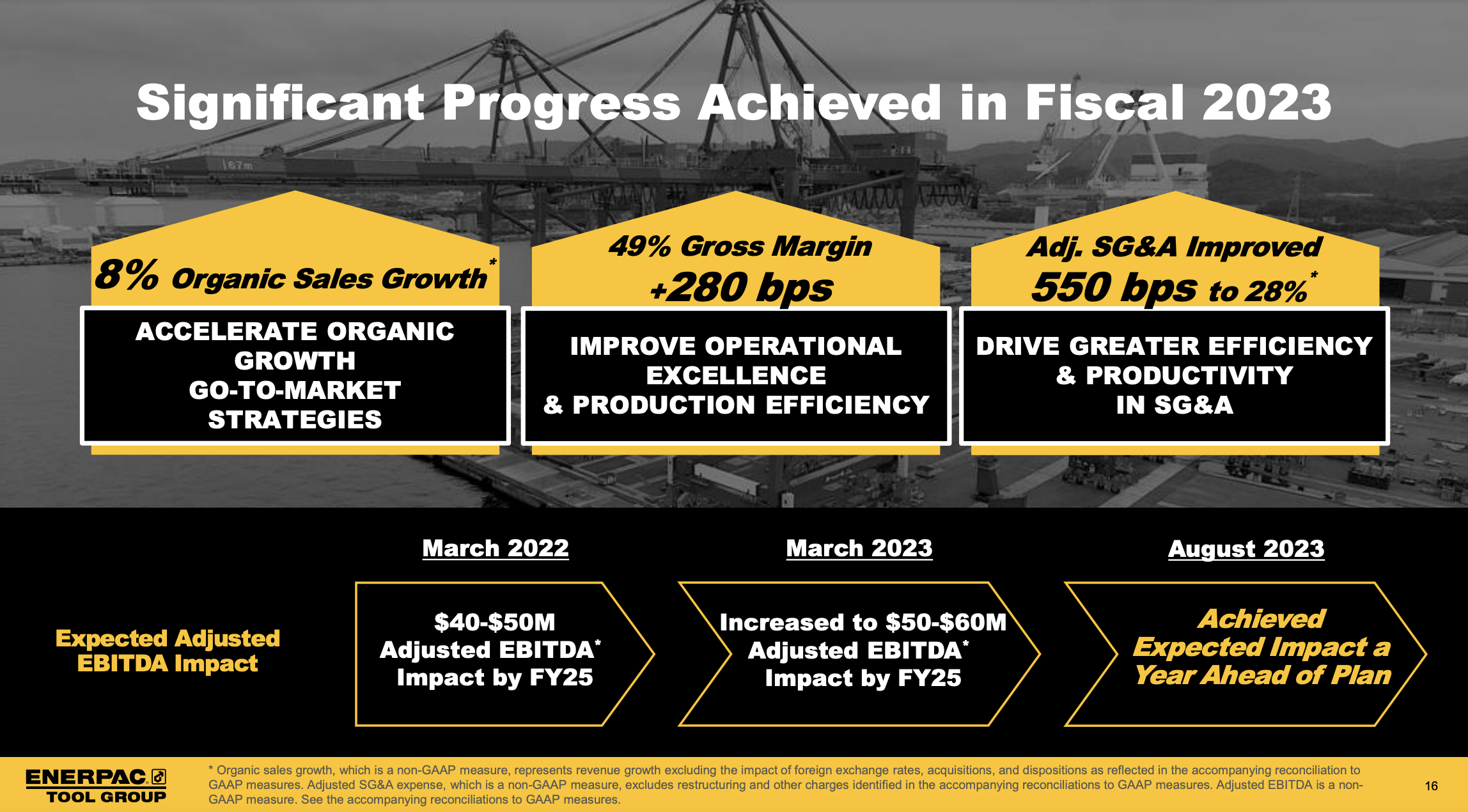

The progress achieved from this initiative has already proven to be effective. The original plan was to boost EBITDA by between $40 million and $50 million by the 2025 fiscal year. That was later revised higher to between $50 million and $60 million in March of 2023. But then in August of that year, management said that they achieved the desired results approximately one year ahead of plan. Obviously, other profitability metrics have benefited. While operating cash flow did decline from $17.8 million to negative $3.9 million, the adjusted figure for it nearly doubled from $13.2 million to $26.2 million. And lastly, EBITDA for the firm grew from $26.6 million to $34.9 million.

Enerpac Tool Group

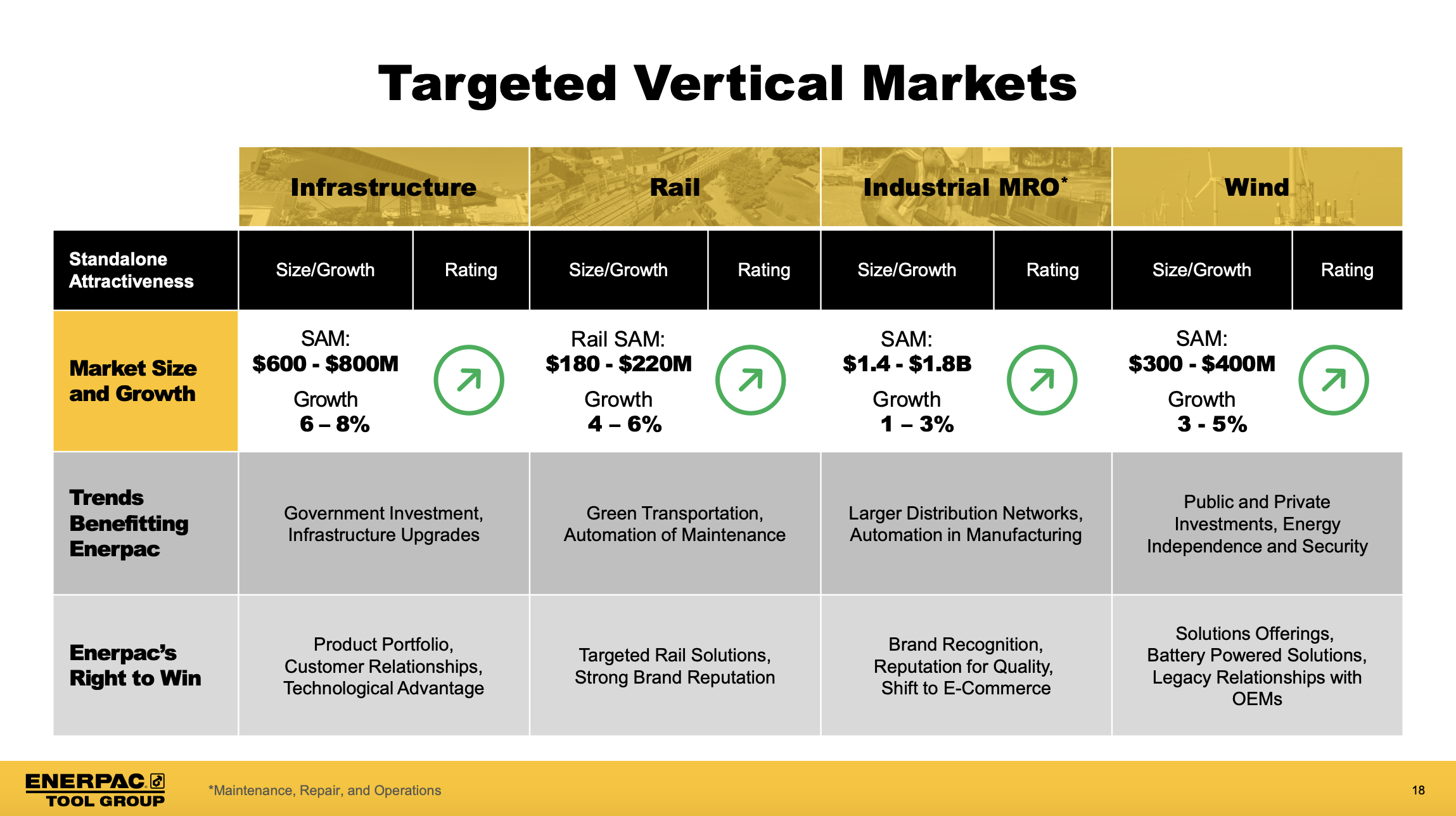

Longer term, management has some rather ambitious objectives. They want to achieve organic revenue growth of between 6% and 7% annually through 2026. This will involve a variety of efforts, including expansion in certain vertical markets, investments to make the company more digital, innovations based on customer needs, and a concerted effort to expand operations into the Asia Pacific region.

Because of how the company breaks down its geographical revenue data, we don't know exactly how much in sales it brings from that region. But we do know that it's at least 7.1% of overall revenue.

Speaking of the vertical markets that the company wants to get into, management is looking at infrastructure, which has a serviceable addressable market of between $600 million and $800 million. The rail market is estimated to be worth between $180 million and $220 million. The industrial MRO market is far larger between $1.4 billion and $1.8 billion. And the wind market that they are looking at is worth between $300 million and $400 million.

Enerpac Tool Group

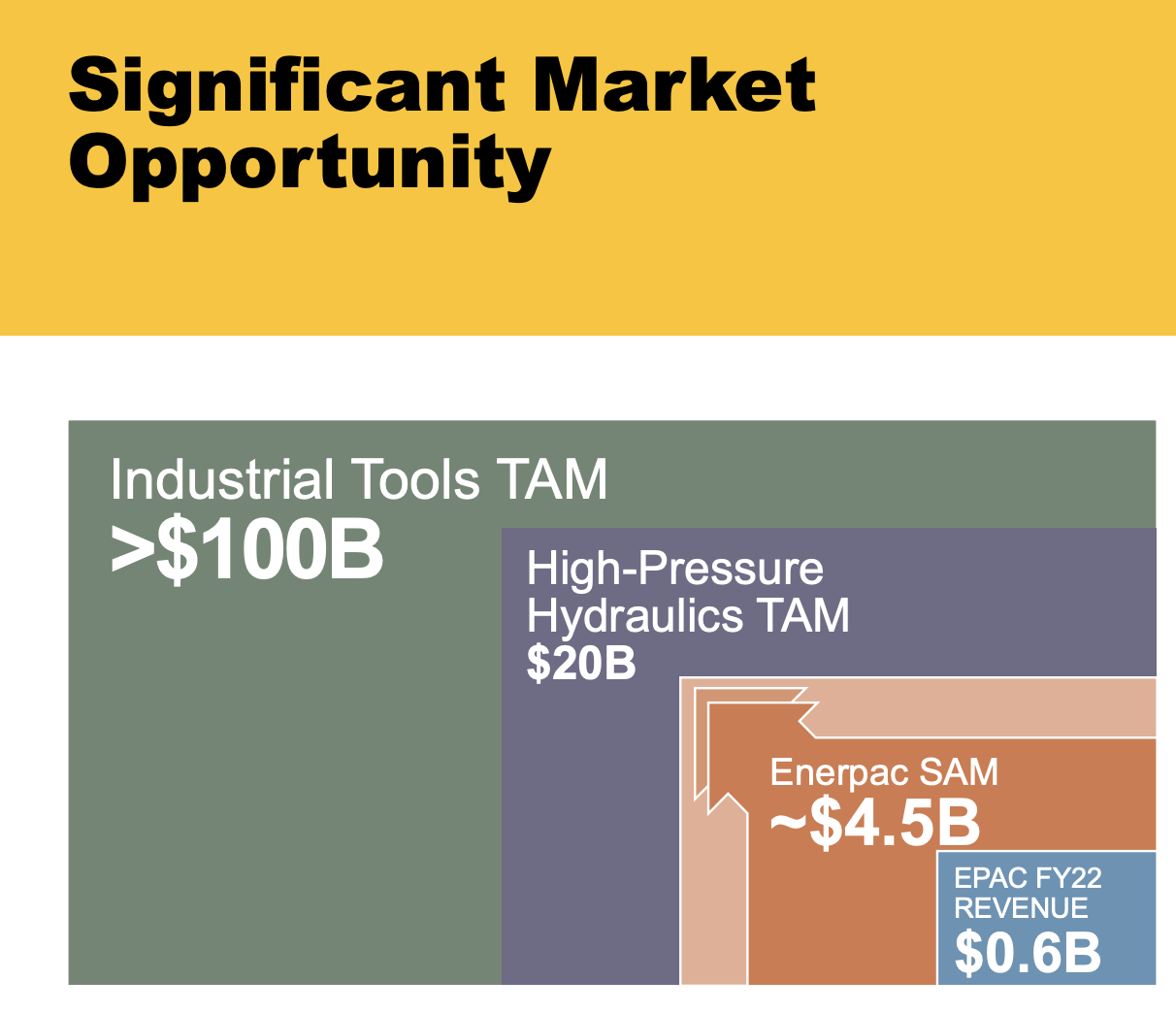

At this time, the entire markets in which Enerpac Tool Group operates is estimated to have a serviceable addressable market of around $4.5 billion. That does seem to offer significant upside potential for shareholders in the long run. And even at the company were to achieve saturation in that space, there are other large opportunities to consider. Moving into the high-pressure hydraulics market would offer a total addressable market, or TAM, size of around $20 billion. And the industrial tools market is even larger at more than $100 billion.

Enerpac Tool Group

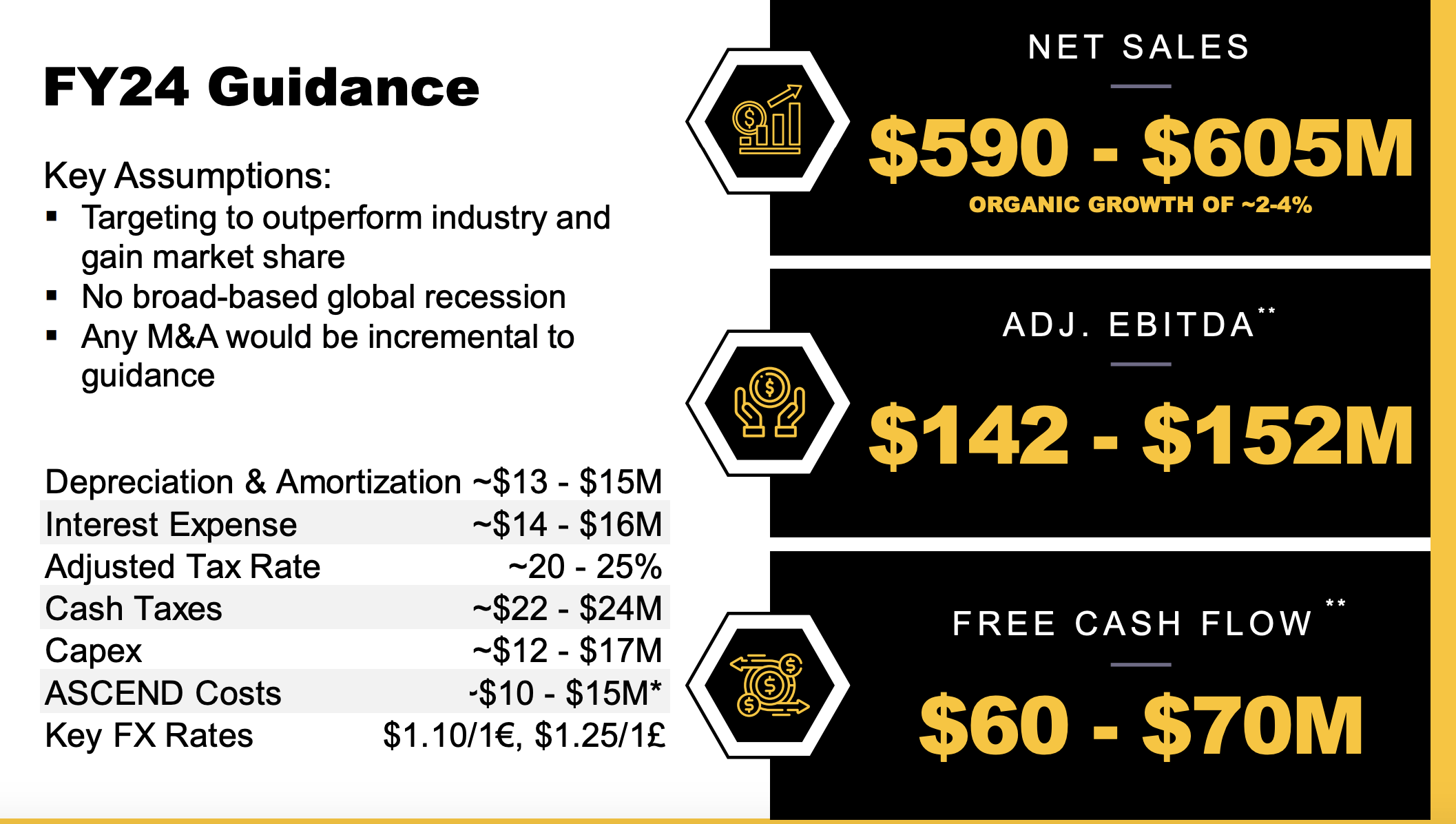

Naturally, this will all take time. For 2024 as a whole, for instance, management is forecasting revenue of between $590 million and $605 million. That's based on organic revenue growth of between 2% and 4%. Meanwhile, EBITDA is expected to be between $142 million and $152 million. No guidance was given when it came to adjusted operating cash flow. But based on my estimates, it should come in somewhere around $82.1 million. Using these results, it's easy to value the company.

Author - SEC EDGAR Data

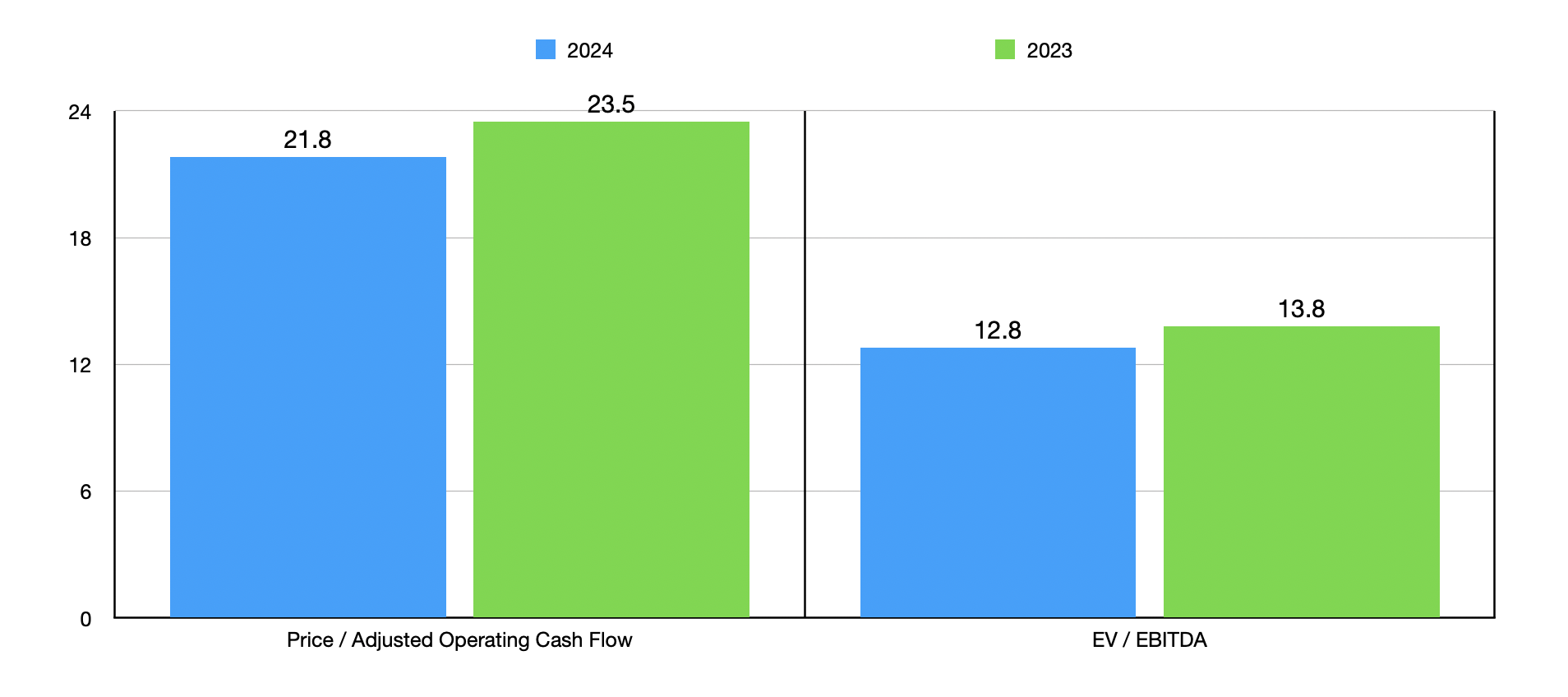

As shown in the chart above, shares do look quite pricey relative to cash flow. However, they are more reasonably priced when using the EV to EBITDA approach. Relative to other players in the space, however, they are quite expensive. In the table below, I compared Enerpac Tool Group to five similar firms. On a price to operating cash flow basis, I found that Enerpac Tool Group ended up being the most expensive of the group. However, this ranking does decline to where there are only three firms that are cheaper than it when using the EV to EBITDA approach.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Enerpac Tool Group | 23.5 | 13.8 |

| Barnes Group (B) | 17.1 | 14.9 |

| Hillman Solutions (HLMN) | 8.1 | 14.3 |

| Kennametal (KMT) | 6.8 | 8.2 |

| Standex International (SXI) | 19.9 | 10.5 |

| Tennant Company (TNC) | 11.1 | 11.4 |

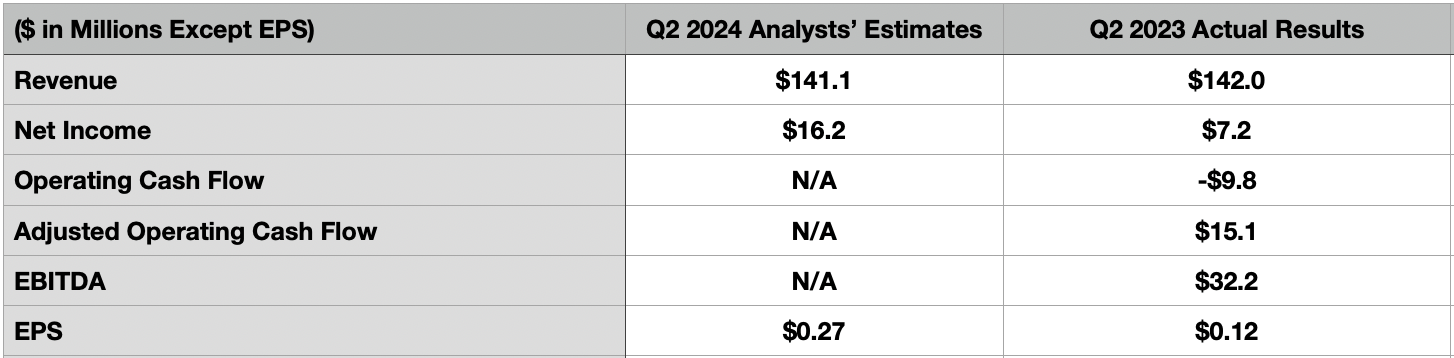

It's also imperative to understand that the picture can change, especially during times of economic uncertainty. That's why investors should be paying careful attention to when management reports results for the second quarter of the 2024 fiscal year. That's expected to occur on the morning of March 21st, before the market opens.

At present, analysts are actually forecasting revenue to come in a bit weak at about $141.1 million. That would be down marginally from the $142 million generated the same time of the 2023 fiscal year. On the bottom line, the picture is expected to be quite a bit different. Profits per share are forecasted at $0.27. That's more than double the $0.12 per share generated in the second quarter of 2023.

If this comes to fruition, it would take net income from $7.2 million last year to $16.2 million this year. No estimates were provided when it came to other profitability metrics. But in the table below, you can see what these looked like for the second quarter of 2023.

Author - SEC EDGAR Data

All things considered, Enerpac Tool Group is an interesting company and one that is undergoing some meaningful changes. I'm definitely happy to see that. In the long run, I suspect that the company will continue to expand and will create value for shareholders.

On the other hand, analysts are a bit uncertain about near-term revenue, and Enerpac Tool Group Corp. shares don't look attractively priced even if we assume that management's forecasts are accurate. Given these factors, until we see something else develop, I believe that a "hold" rating is what makes the most sense.