Nikolay Pandev/E+ via Getty Images

Nikolay Pandev/E+ via Getty Images

Tiptree (NASDAQ:TIPT) reported its fourth quarter on Wednesday evening (Feb 28th). There were no real surprises, given that Fortegra had given an operational update during its January roadshow for the since-pulled IPO. I had written about the IPO process and its cancellation last month. This update covers Tiptree as a whole.

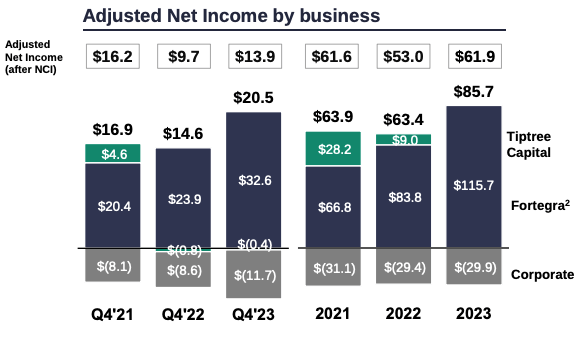

I still can't believe the Fortegra IPO failed. Fortegra is a beast. It earned $32.6 million in Q4, bringing the full year to $115 million with a 30.9 and 29.2% return on equity for Q4 and the year, respectively. That's around 40% growth. I don't want to jinx anything, but $115 million in 2023 quite easily becomes $150 million in 2024, even with a slowdown in the growth rate. Insurance is funny in that you have an idea of what the next 12 to 18 months are going to look like based on net written premium (assuming no tail risk events, to which Tiptree is not majorly exposed).

Tiptree's 76% stake in Fortegra translated to $25.9 million of after-tax earnings for the company. This being Tiptree, there are some mostly non-cash adjustments to earnings, like the almost $9 million ($.25/share) deferred tax issue related to Warburg's investment in Fortegra (which again, would only be triggered if Tiptree ever sells its stake). There are also some mark-to-market investment losses. I'll emphasize that these "losses" that run through the income statement are non-cash and, in my opinion, are unlikely ever to be crystallized/realized. They also benefit the company by sheltering income from taxes.

Corporate overhead remains too high. There were some specific bonus triggers the company hit this year that resulted in some incentive comp. I have a ton of respect for management, and they definitely create a lot of value, but overhead costs have been too high for a company this size. This overhead figure would stand out even more, if Fortegra were fully independent.

Tiptree Profits Breakdown (Q4 Presentation)

This part of the company remains very quiet. There was a loan that was a small legacy tied to the since-sold shipping business that the company had to recognize a loss on. Otherwise, the mortgage business is very quiet, as is activity on the investment side. This business has about $5/share of book value tied to it.

This company is all about Fortegra and has been for some time. It was very disappointing that the Fortegra IPO didn't happen. I think some poorly performing IPO's done by members of the syndicate group, weighed on sentiment among some potential investors. But I know there was a core group of people that really wanted to invest in Fortegra at the proposed deal range, including myself. Right now, the deal looks dead, but I doubt that interest has completely disappeared. I know I'm still interested.

The main risk here is a major deterioration at Fortegra or sell off in small caps. This is still a relatively illiquid stock and exposed to the vacillations of small cap land.

The stock sold off post the failed Fortegra IPO, but not terribly. It's still higher than where it was before the deal was announced. Perhaps the road show exposed just how much Fortegra value is embedded in this company, not even considering the near $5 of value from the rest of the business. I still think the stock could easily double, if Fortegra could achieve some sort of public market valuation. I have proposed ways to do that in the past. Until then, the value keeps building underneath the hood.