AtnoYdur/iStock via Getty Images

Editor's note: Seeking Alpha is proud to welcome Fernanda Galvez Jalil as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

AtnoYdur/iStock via Getty Images

Thryv Holdings (NASDAQ:THRY) is a company whose core business is the forgotten and underutilized yellow pages. As one might expect, this business is declining each year and does not present itself as an attractive investment option. However, beneath this underperforming core business lies the development of a Software as a Service (SaaS) business that is growing at an annual rate between 20% and 30%. The future of the SaaS business looks significantly brighter than that of the core business, and recent results encourage us to think that the company could be a good potential investment.

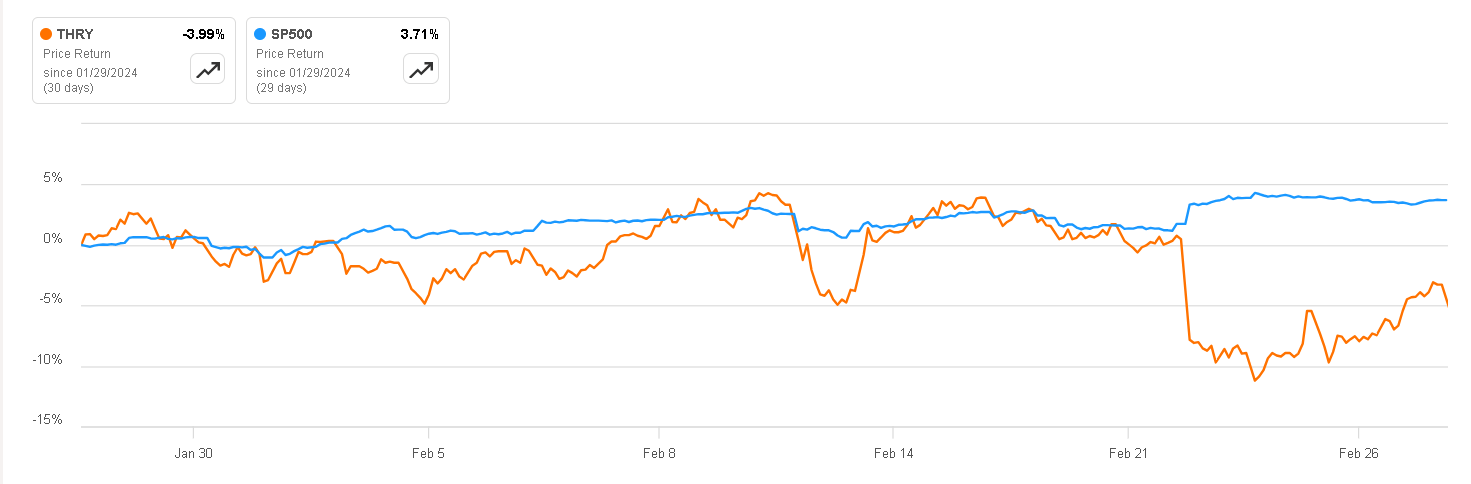

In this article, I will analyze precisely the Full Year 2023 results that the company shared last week, following which the stock experienced a 9% decline. My aim is to explain why I think that after analyzing the business model and recent results, Thryv represents an investment opportunity thanks to how well the development of the SaaS business is going and how cheap the company is at current price.

Share Price Drop (Seeking Alpha)

As I mentioned at the beginning, the company's revenue is divided into two main sources, which I am going to talk about in more detail to understand the opportunity that exists in each of them, because even though the core business is worse, it also has its "charm".

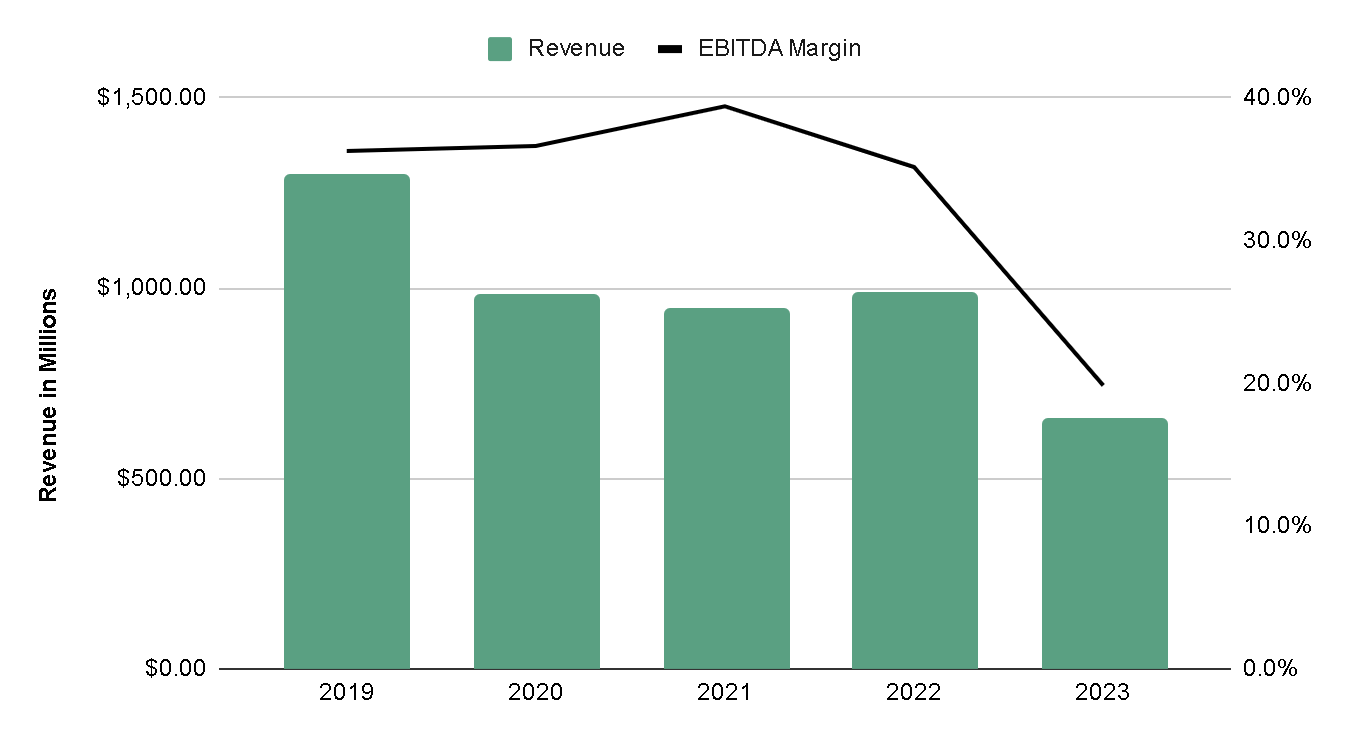

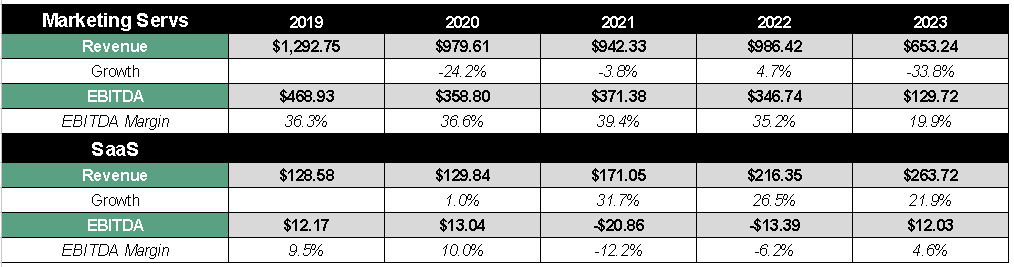

The core business is Marketing Services, in which the company offers printing of the famous Yellow Pages, which are telephone directories of businesses in which small local businesses pay to be advertised and consumers use the Yellow Pages to discover nearby businesses. This business is in decline due to the digitalization of advertising, however, it still generates a fairly chunky EBITDA, with margins that used to average 35% and although the year 2023 was somewhat bad, management's expectation is to generate margins again around 25% again.

Author's Representation

Additionally, the company has digitized this business through pages such as Yellowpages.com or Dexknows.com, with the intention of continuing to generate additional income through this means, although this may not be the most popular, given that businesses typically prefer to advertise on Google Ads and Facebook Ads, so we cannot expect that this digital product alone will change the course of business deterioration.

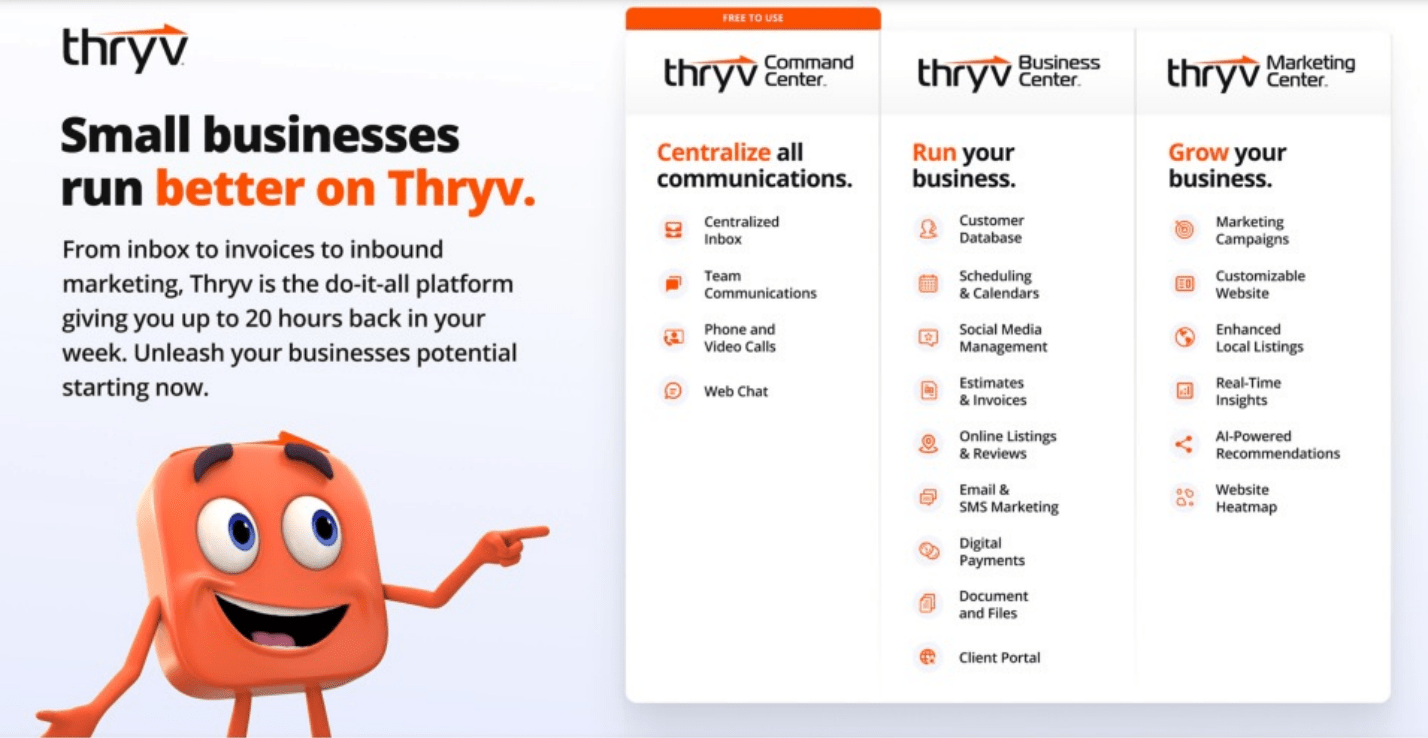

In short, Thryv Holdings had a legacy business that was in absolute decline, but was quite profitable. So, in an act of foresight and tenacity, they decided to take advantage of the solid relationships they had with small and medium-sized businesses to offer them software with considerably more added value than a simply yellow page, taking advantage of having the contacts and trust they created to make them transition towards this new platform, called Thryv.

Thryv offers small and medium-sized business owners control of their day-to-day operations, with features such as customer relationship management, appointment scheduling, invoice creation, payments management, social media content, among others. And to continue making their platform attractive, they recently added the "Command Center" section in which clients can centralize their means of communication, for example, have WhatsApp, Gmail, Instagram and Skype, all in a single interface so that the communication process is smoother.

Thryv Platform (Thryv Investor Presentation)

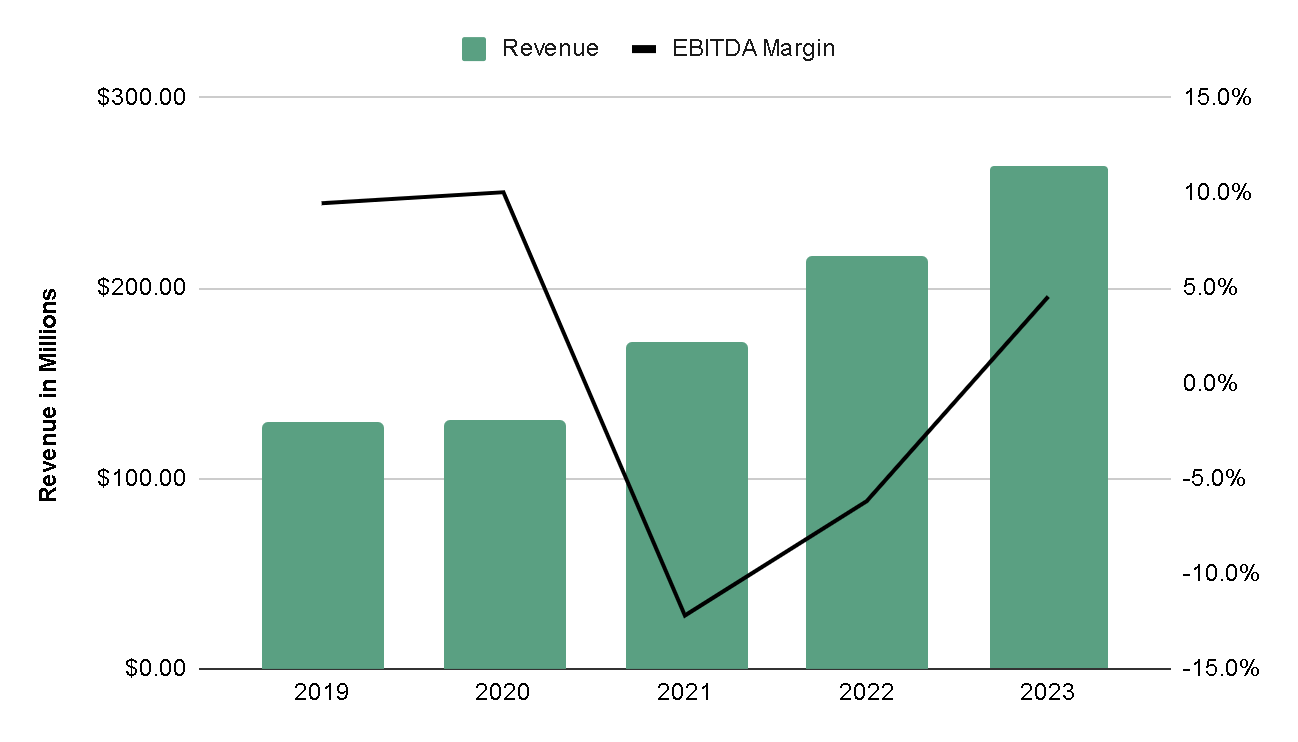

This business seems to be having success and revenue has grown 25% on average over the last few years and, as we will see later, it is already generating positive EBITDA, so the typical operating leverage of a software business is already beginning to be reflected.

According to the figures from the latest annual report, Thryv software has Monthly Active Users of 40,000, who on average spend approximately $6,500 dollars annually. Furthermore, the company estimates that its potential market is made up of nearly 4 million small and medium-sized businesses in the United States alone and 8 million internationally, so the market opportunity is at least 100 times greater than what they have generated so far. This is why this new segment of the business seems so attractive and makes the company's thesis promising.

Author's Representation

On February 22, Thryv Holdings presented results for fiscal year 2023 and stock ended up falling 9%. The presented results for Q4 were as follows:

So far, so good, you might be thinking. However, the problem arises when we look at the unadjusted EBIT, which was -$242 million, compared to the $32.5 million that analysts were expecting. In other words, the company earned $274.5 million less than what was expected.

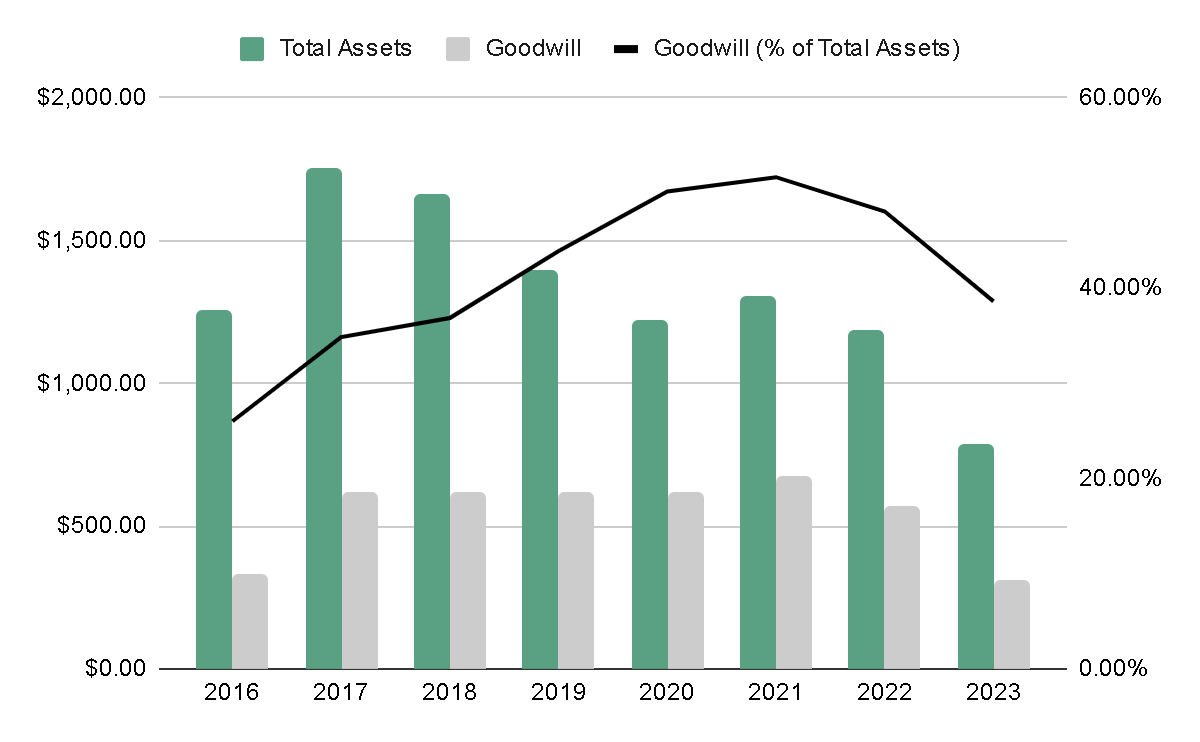

The main reason for this significant difference was an impairment charge to goodwill of approximately $269 million. This is something quite recurrent in the company because the yellow pages legacy business deteriorates more every day, and the company has also made numerous acquisitions of businesses related to this segment. Since 2019, the company has had to make impairment charges totaling $400 million. However, they had never made one as large as this year's, which represented 34% of total assets.

Author's Representation

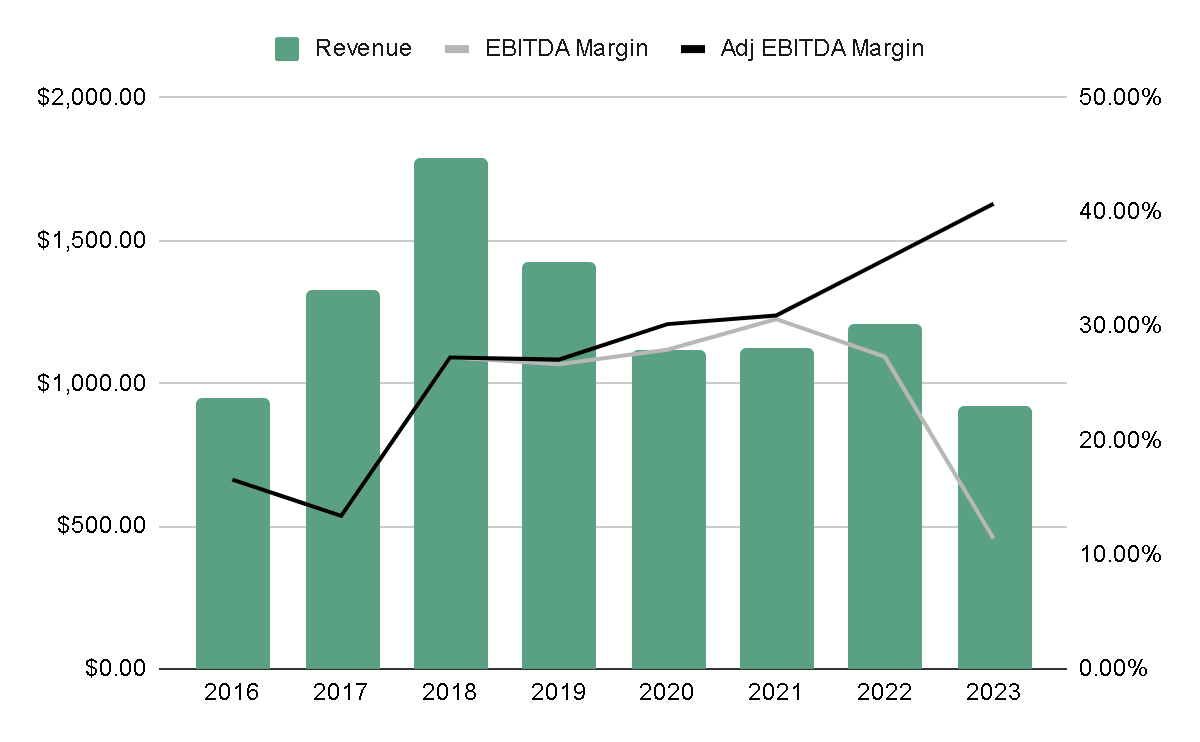

If we contextualize these figures, we can notice a drastic decrease in revenue during this year—specifically, it decreased by almost 24%. The explanation for this decrease comes, on the one hand, from the structural condition of the Yellow Pages business, which still represented 70% of the revenue. It is notable, however, that the revenue of this segment was better than the guidance provided during Q4 of 2022, where they provided a high range of $649 million compared to the reported $653 million.

For the full year 2023 we expect marketing services revenue in the range of $635 million to $649 million and adjusted EBITDA in the range of $185 million to $187 million.

On the other hand, the segment that really interests us, Software as a Service, grew by over 20% and already generated a positive Adjusted EBITDA margin of 5%. This also exceeded the company's guidance and seems to be the most notable point of the thesis. Even in a difficult year, they managed to maintain high growth, and the fact that the SaaS segment already generates positive EBITDA could mark a turning point in the consolidated EBITDA of the company. Now, the decrease in profits from the legacy segment will be offset by the growth of the SaaS segment.

For the full year 2023 we expect SaaS revenue in the range of $257 million to $259 million, which implies SaaS revenue growth of 19% to 20%. We expect SaaS to be adjusted EBITDA positive.

Q4 2022 Conference Call

If we adjust the EBITDA by only adding back the impairments made in recent years, the margin would have reached 40% (compared to the reported 11%). Despite the distortions of the impairments, the underlying business continues to improve its fundamentals.

Author's Representation

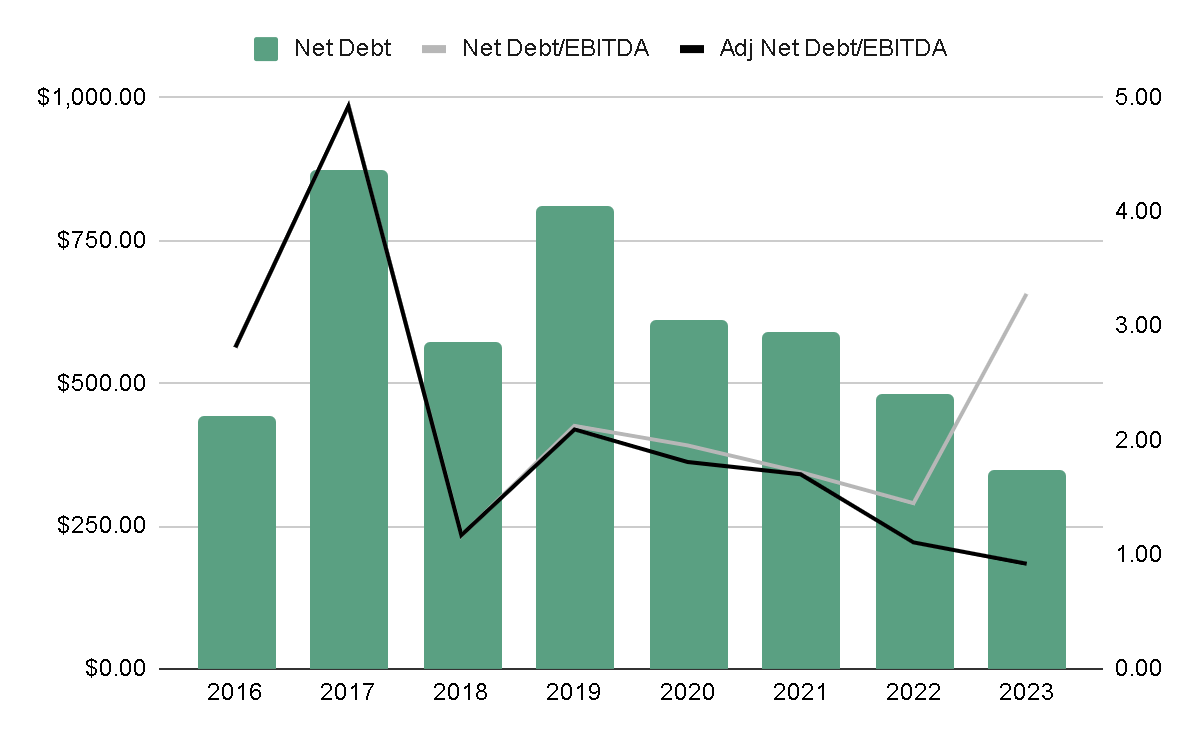

Another aspect that I think is relevant to mention is the fact that during the year the company made great efforts to reduce debt. Specifically, the net debt went from $477 million to $343 million, that is, they reduced the debt by 28% during this year.

Although this is not reflected in the Net Debt/EBITDA ratio, for the aforementioned reasons that compressed EBITDA, if we use the Impairment Adjusted EBITDA, the leverage ratio would have already been reduced to 0.9x. This is a totally manageable ratio and is the minimum we could expect from a company with a core business that deteriorates more every year, but what it needs most is time to continue developing its SaaS business.

Author's Representation

After delving into the results and realizing that the business is not as bad as it might seem at first glance, the interesting question arises: How much is the business worth?

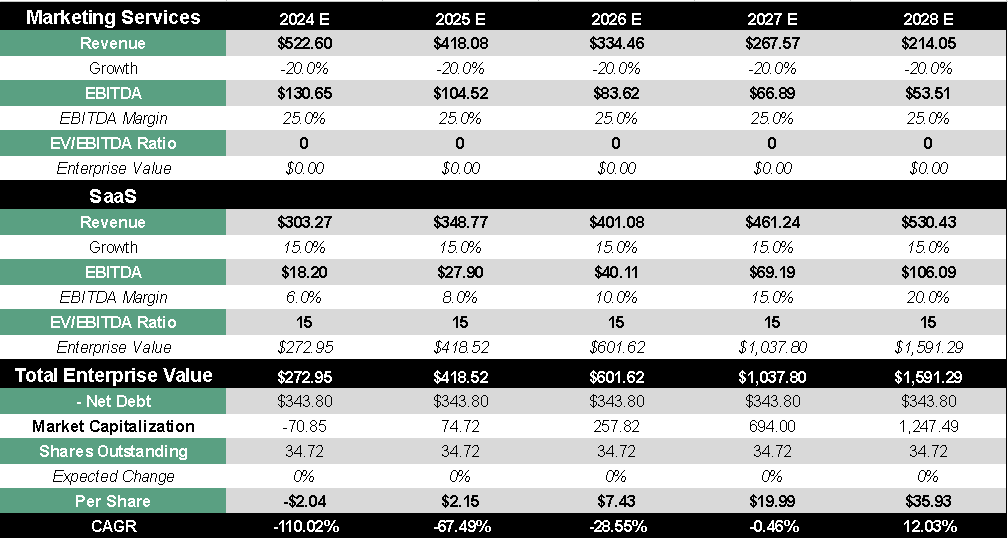

To answer this question, I will project the growth of each segment, value it individually due to its drastically opposite characteristics and then perform a sum-of-the-parts. To begin with, we can note the obvious: The Marketing segment (legacy business) is not growing. In fact, management comments that they expect it to continue decreasing by close to 20% annually, which is to be expected.

Our Marketing Services revenue is declining every year in the range of 20%. We are being proactive in retaining clients for the long-term by offering them a viable product, a software platform that prepares them for the future. Upgrading them to our platform can address their current and future needs.

On the other hand, the SaaS segment has been experiencing annual growth rates between 20% and 30%. The expectation is to achieve $1 billion in revenue within the next 5 years, which seems feasible given the significant market opportunity. However, to err on the side of caution, I will conservatively estimate a growth rate of 15% annually, a figure that remains both realistic and achievable.

Author's Representation

So, instead of reaching $1 billion in revenue, I estimate that the SaaS segment will only generate ~$500 million within five years, with an EBITDA margin of 20%, and assigning an EV/EBITDA multiple of 15x. Then, we will assign a value of zero to the rest of the business, as an experiment, considering that it is a deteriorating business and that we cannot expect much from it. This would result in a total Enterprise Value of $1.6 billion within five years. If we discount the debt and divide it by the outstanding shares, we would obtain a price per share target of ~$36 USD within five years, or a compound annual return of 12%. In my opinion, this is very good, considering that we are only valuing the SaaS segment, and we do not even estimate that it will reach the revenue projected by management.

On the other hand, if we assign a multiple of only 4x to the Marketing Services segment, because although it is not an attractive segment, it still generates wide EBITDA margins, the expected return would be approximately 16% annually. In other words, even with the least optimistic and most cautious assumptions, the return on our investment could be double digits.

Author's Representation

If we talk about risks, I think it is important to highlight that this is a high-risk venture capital-style investment, because we are literally trusting our entire investment on the success of the new SaaS business, as the legacy segment alone is not a strong performer. So, if the company does not succeed in developing the SaaS segment correctly, our investment in Thryv may not be successful either.

I also think that the SaaS business presents quite strong competition, since product differentiation of this style is not much. In fact, IDT Corporation is also developing similar software focused on small and medium-sized businesses, which tells us how relatively easy it is to compete. Of course, few competitors have the personal relationships that Thryv has, so this could be its greatest competitive advantage.

After analyzing the results and delving deeper into the business, it seems to me that the market's reaction to the results was excessively negative. Personally, I perceive a company whose relevant segment continues to grow and demonstrate acceptance by its potential customers, is already profitable, and that, by valuing this segment with conservative assumptions alone, we could obtain a double-digit annual return.

So, considering risks and potential benefit, I think that at the current valuation the company is a 'buy'.