wildpixel

wildpixel

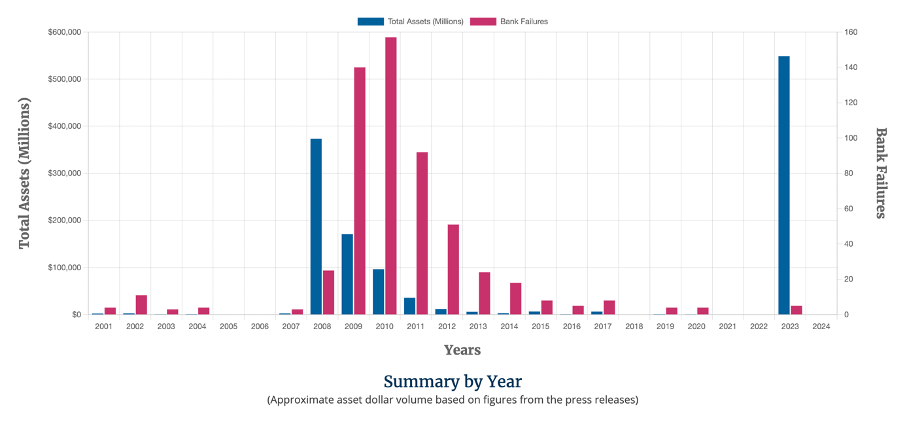

A little more than a year ago, the world was in shock as it seemed like the banking crisis suddenly returned. In total, 2023 saw 5 bank failures (according to the FDIC) and it was especially March 2023 that seemed dramatic due to two banks collapsing - Silicon Valley Bank collapsed on March 10, 2023 and Signature Bank collapsed on March 12, 2023. And while 5 banks collapsing in one year was the highest number of bank failures since 2017 the number is far away from 157 bank failures in 2010 (in the fall-out of the Great Financial Crisis). However, while only 5 banks failed in 2023 these banks had a combined $548.7 billion in assets – and this is the highest amount at least since 2001. And even when adjusting for inflation, the assets of the banks failed were higher than in any year during the Great Financial Crisis.

FDIC

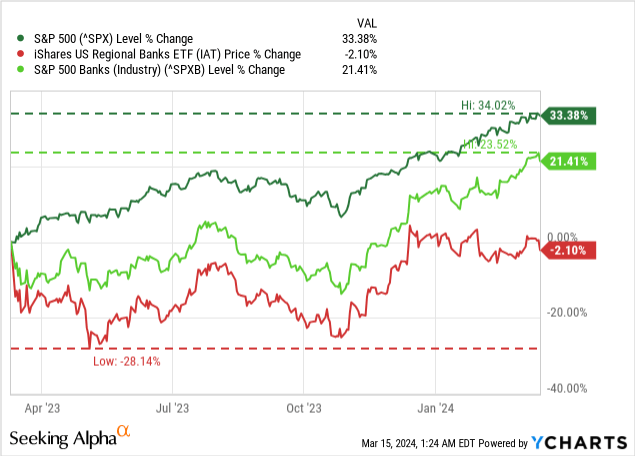

About a year has passed and it seems like the crisis was contained and a bigger banking crisis was averted. The sentiment among investors is visible when looking at the S&P 500 (SPY), which increased 33% since the collapse of Silicon Valley Bank and the S&P 500 Banking Sector Index (see chart) increased 22% in the same timeframe. However, the regional banks (IAT) clearly underperformed but kept up well and are now trading more or less at the same level as one year earlier.

But I think we are still trading in a false sense of security and the situation is not as good as it seems.

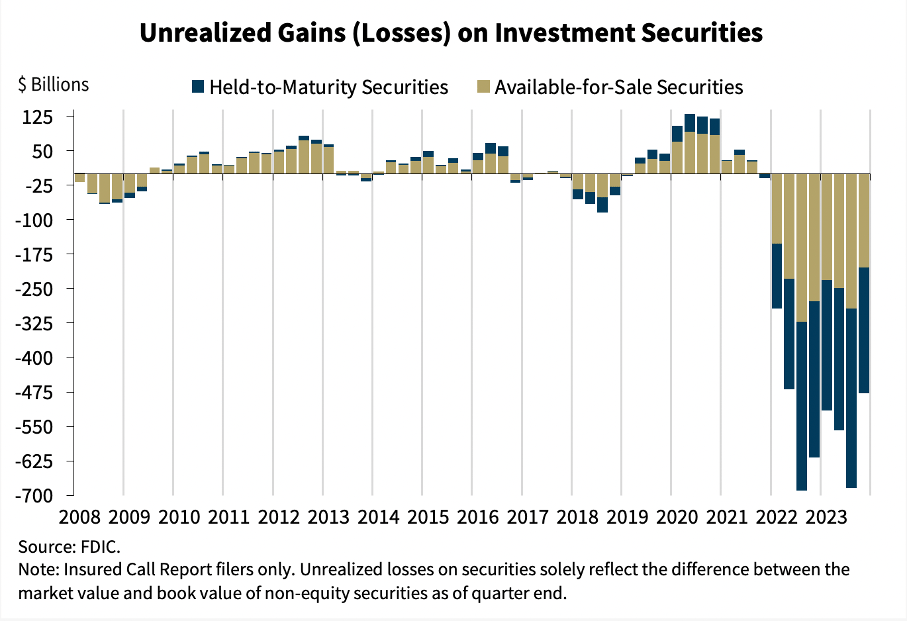

In my opinion, when looking at the banks in the United States, it is difficult to be optimistic. But let’s start with some positive news. According to the latest FDIC Quarterly Banking Profile, the amount of unrealized losses on investment securities got lower again. The amount is still way worse than at any point during the Great Financial Crisis, but in Q4/23 banks had only $478 billion of unrealized losses on their books compared to $684 billion one quarter earlier.

FDIC Quarterly Banking Profile

Another good sign is the increase in deposits. After six consecutive quarters of declining deposits, banks actually increased their deposits by $260 billion compared to the previous quarter. And outflows are adding fuel to the fire: If there should be a liquidity crisis for any bank, cash outflows obviously make the situation worse.

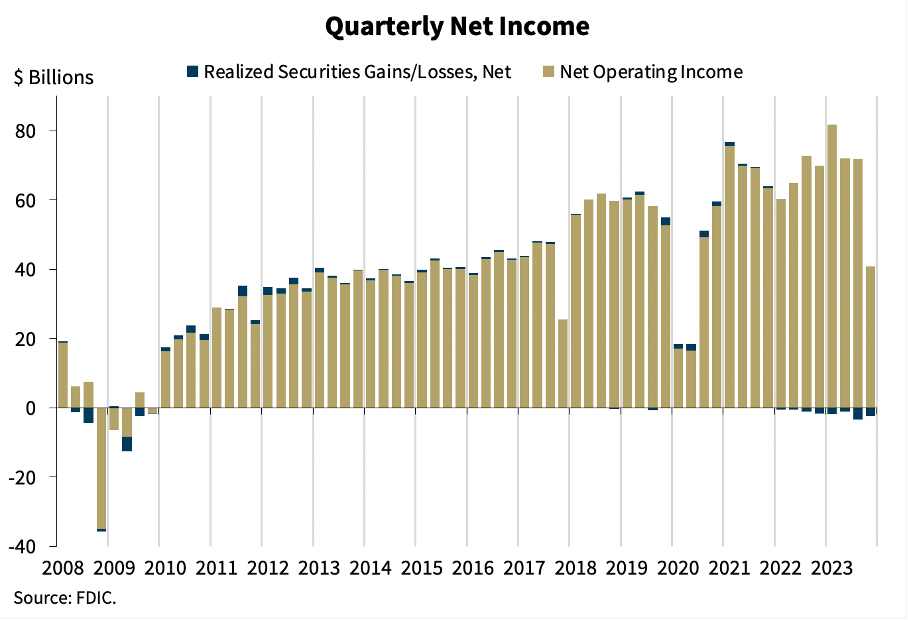

However, many other metrics are continuing to get worse. When looking at the full-year net income, banks earned about $266 billion – more or less the same as in 2022 and 2021. However, when looking at the quarterly net income, it fell off a cliff. In Q4/23, banks generated $40.8 billion in net income, which is not only below the previous quarter ($71.8 billion in Q3/23) but also below the same quarter last year ($69.9 billion in Q4/22). It was the worst result since early 2020, when banks took huge provision for credit losses in the early weeks of COVID-19. Additionally, banks reported $2.4 billion in realized security losses following $3.4 billion in security losses in Q3/23 – the biggest quarterly losses since 2009.

FDIC Quarterly Banking Profile

One of the reasons for the lower quarterly net income are the increased provision for credit losses ($5.2 billion during the fourth quarter). But it can be interpreted as a good sign that banks are getting more cautious and are building reserves for potential losses and defaults. But as we will see later, $5.2 billion might be pocket change compared to the amounts at stake for default.

A few weeks ago, the Fed also announced the stress testing scenarios for 2024 and four additional criteria where added. The Fed wrote in a press release:

This year's exploratory analysis includes four separate hypothetical elements that will assess the resilience of the banking system to a wider range of risks. Two of the hypothetical elements include funding stresses that cause a rapid repricing of a large proportion of deposits at large banks. Each element has a different set of interest rate and economic conditions, including a moderate recession with increasing inflation and rising interest rates, and a severe global recession with high and persistent inflation and rising interest rates.

The other two elements of the exploratory analysis include two sets of market shocks that will be applied only to the largest and most complex banks. These shocks hypothesize the failure of five large hedge funds, with each under a different set of financial market conditions. Those conditions include expectations of reduced global economic activity with a negative outlook for long-term inflation, and expectations of severe recessions in the United States and other countries.

Results for the stress test are expected in June 2024, but a lot can happen until then. And of course, this is rather anecdotal and not really proof that banks are in bad shape. We can also pick numbers and metrics to fit a certain bias and we should always be careful not to become a victim of confirmation bias (looking only for evidence or paying attention to the evidence that is fitting the narrative).

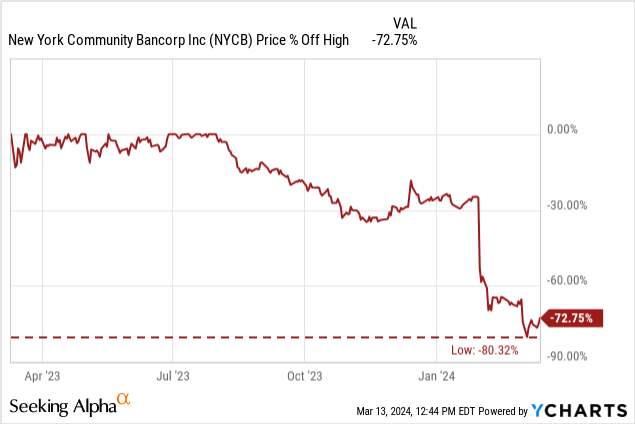

And another aspect that can be seen as rather anecdotal is the current situation of New York Community Bancorp (NYCB). So far, we didn’t see any bank failures in 2024 but the risk is rather high for this bank to be the first victim. Since the temporary peak in August 2023, the stock has declined about 73% as I believe investors are clearly fearing the bank might go under (by the way, the stock price peaked at $35.12 almost 20 years ago).

On the surface it doesn’t look good for the bank, but on the other hand, the company slashed the dividend to only one cent per share and several institutional investors put up $1.05 billion in additional capital for the bank. The capital raise will increase the common equity tier 1 ratio to 10.3% (on a pro forma basis). As a result, Moody’s switched the direction of its review to a possible upgrade from a possible downgrade.

Nevertheless, New York Community Bancorp might be the current warning signal that a potential banking crisis is not just a far-fetched theory.

One of the problems we are still faced with are the higher interest rates. Of course, current interest rates are not extremely high compared to previous decades. The problem is rather the high pace of interest rate increases and how quickly the picture changed from a zero-rate environment to mid-single digit interest rates (of course, this is depending on the type of loan).

The huge risk here is that rising interest rates could bring banks (as well as companies) to their knees – as it was the case one year ago when Silicon Valley Bank collapsed. And the outlook is rather bleak if interest rates and inflation are staying high – especially if the economy stagnates as well.

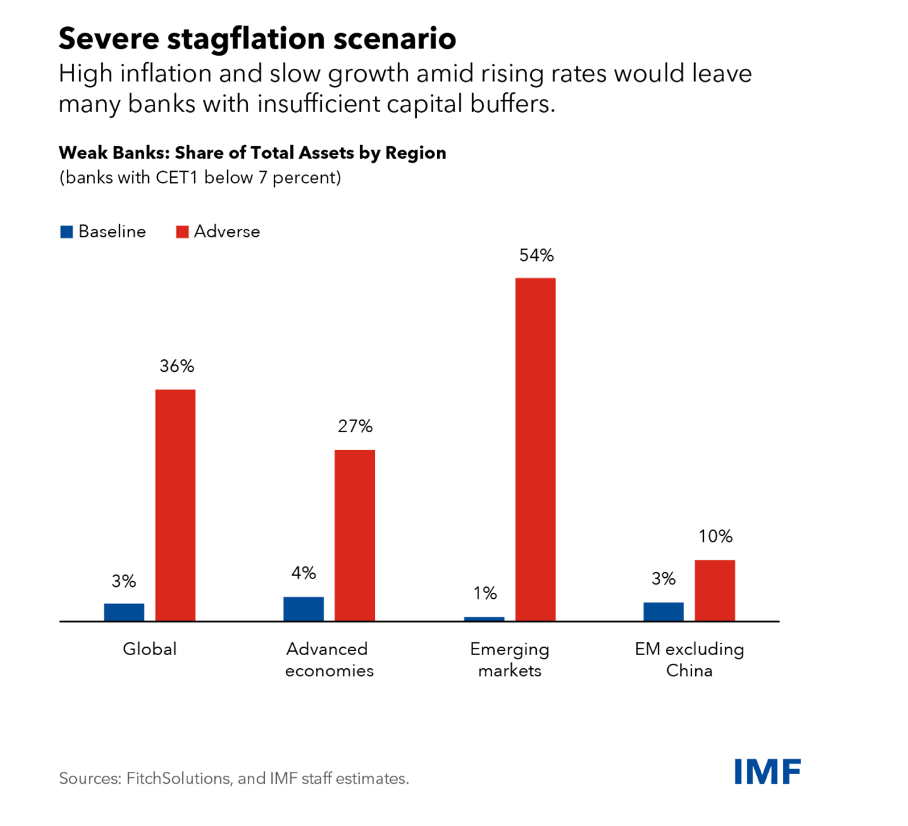

In October 2023 the IMF wrote in a blog article:

But if beset by severe stagflation—high inflation with a 2 percent global economic contraction—coupled with even higher central bank interest rates, the losses would be much greater. The number of weak institutions would rise to 153 and account for more than a third of global bank assets. Excluding China, there are many more weak banks in advanced economies than in emerging markets.

The article is showing that in this adverse scenario, about 27% of total assets in advanced economies are at risks as the banks have insufficient capital buffers. In emerging markets, it would even be 54% with the problem being concentrated especially on China (the biggest economy among the emerging markets countries).

IMF Blog

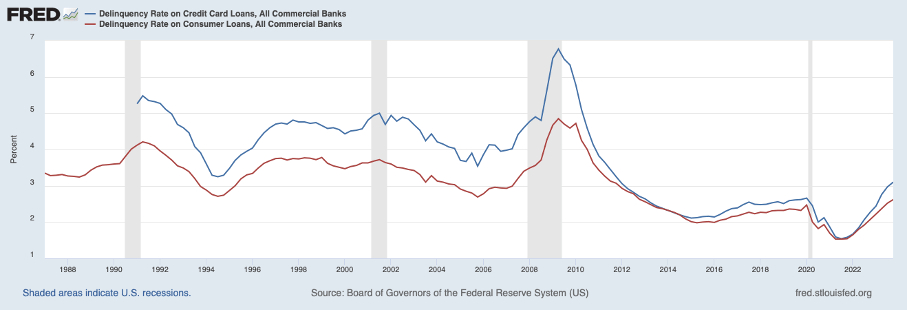

One of the problems we usually see due to rising interest rates are higher delinquency rates. As long as we are dealing with loans that have a fixed interest rate the problem does not appear right away. Especially problematic are loans where the interest rate is fluctuating heavily – credit card loans for example. And here we see delinquency rates constantly rising.

FRED

And while we saw higher delinquency rates during the Great Financial Crisis and also mostly during the 1990s and early 2000s, we can’t deny that delinquency rates keep rising from quarter to quarter, which is not a good sign.

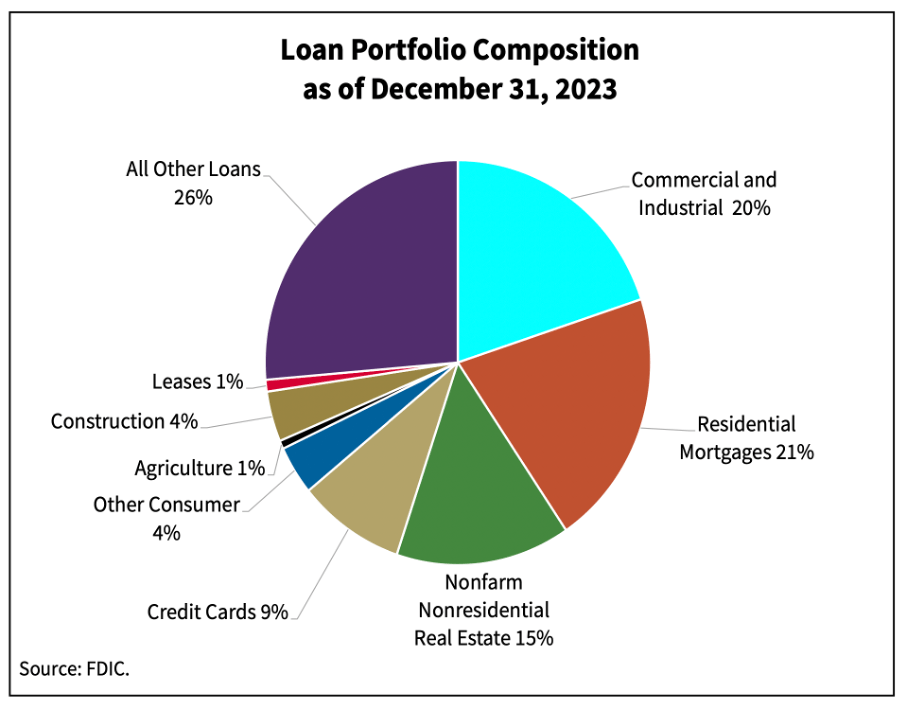

A second problem that is almost always playing a role in major banking crises is real estate. And while credit card loans make up 9% of the total loan portfolio of banks (should not be ignored as this is large enough to cause major damage), residential mortgages alone are making up 21% of loans. We can add another 4% of construction loans and within “Commercial and Industrial” loans there are also loans associated with real estate.

FDIC Quarterly Banking Profile Q4/23

This is demonstrating why the housing market and residential loans have the potential to cause immense damage to banks and the financial sector. And it seems like several people are warning about the real estate market once again. Among the people warning about the real estate market, the most prominent voice is probably Fed chairman Jerome Powell who said a few days ago that there could be more bank failures. The identified problem – according to Powell and others – lies in the commercial real estate loans. The major problem here is the work from home trend that had huge negative impact on the office rent industry.

Names circulating in this context are the above-mentioned New York Community Bancorp, but also Truist Financial Corp. (TFC) with outstanding CRE loans of $53.1 billion and U.S. Bancorp (USB) with $52.9 billion in total outstanding CRE loans.

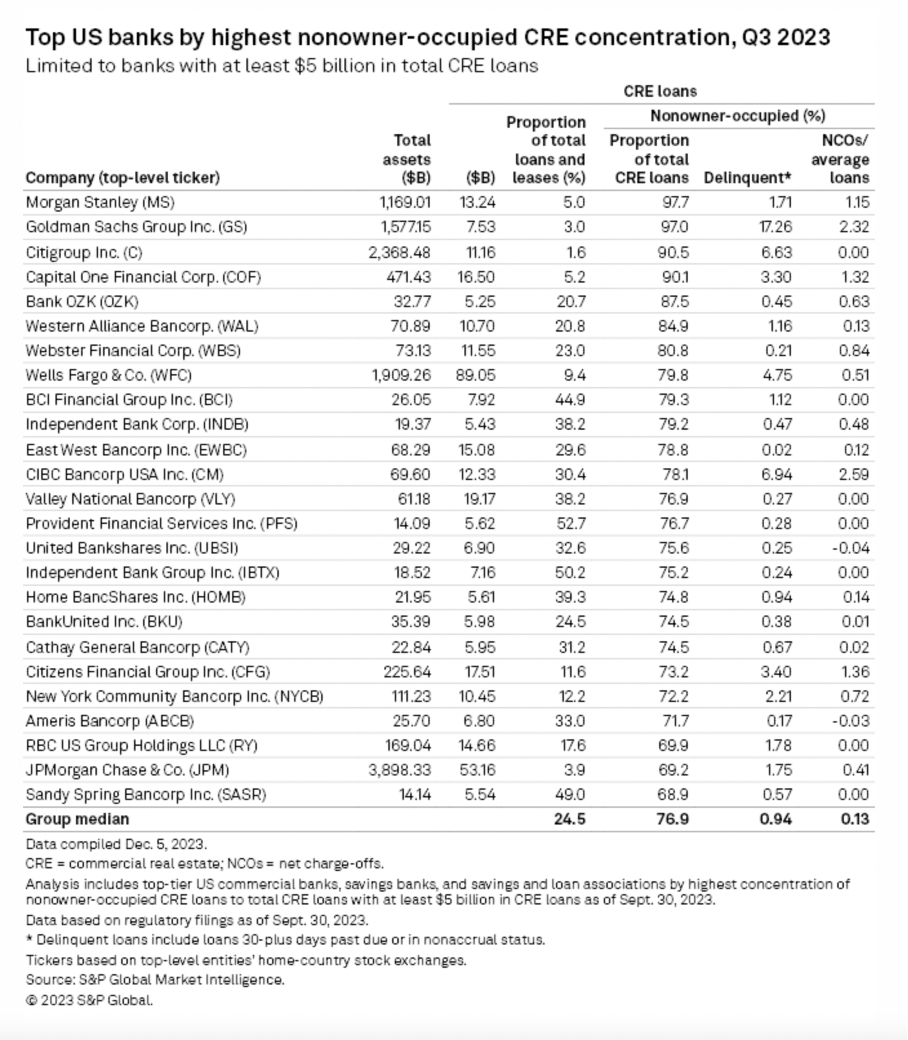

One can now argue that banks are increasing provisions for credit losses again and are therefore preparing for what might come. But according to a FT article, bad commercial real estate loans are now bigger than loss reserves – especially at the biggest US banks. In February 2024 the delinquent loans tied to offices, malls, apartments, and other commercial properties more than doubled. A year ago, the volume was $11.2 billion, now it is $24.3 billion. Bloomberg is reporting that 8.6% of $80 billion of CRE CLO loans (these are commercial real estate loans bundled into collateralized loan obligations) are in distress (meaning here 30 days or more delinquent). S&P Global also pointed out that some of the larger banks have a high nonowner-occupied CRE concentration.

S&P Global

And some of the major banks are also reporting high distress rates (30+ days past due) for these types of loans – especially Goldman Sachs (GS) (17.26% delinquent), CIBC Bancorp USA (6.94% delinquent), Citigroup (C) (6.63% delinquent) and Wells Fargo (WFC) (4.75% delinquent) are standing out here. (Side note: I assume that data for Q4/23 will be available in the next few days).

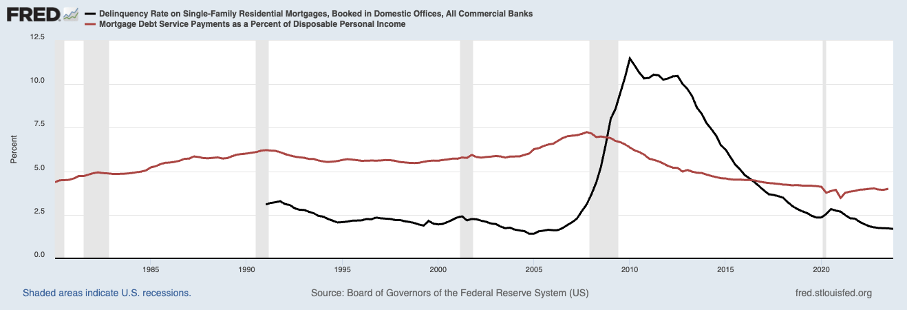

It seems like commercial real estate might be the bigger problem this time. On the other hand, residential mortgages are holding up quite well (at least until now) with a default rate of 1.69% - one of the lowest in the last 30 years. And the percentage of disposable income necessary for mortgage debt service payments is still one of the lowest since the 1980s (however this metric did not increase dramatically before the Great Financial Crisis).

FRED

Another problem could arise from student loans. When looking at the metrics for student loans, we see the indices for 30+/60+/90+ days delinquency improved again in the last few quarters, but they are all still at high levels. And especially the trailing 12-month constant default rate index is at over 5% - by far the highest since early 2006. Of course, student loans are making up “only” $1.7 trillion in total debt and might therefore not be such a huge problem.

My goal is always to avoid spreading panic because similar to every other emotion, panic is not helpful when dealing with financial markets – and I hope this comes across in my articles. But I think we should try to be prepared and take into account negative scenarios. And I will only repeat what I wrote about one year earlier in my article Banking Crisis: The Next Domino Is Falling:

My knowledge of the banking system is much too limited to foresee what ripple effects can occur. However, I know that the banking system, the stock market, and the economy are complex, non-linear systems with thousands of nodes and links intertwined in a complex system and that knowledge is enough to make me cautious. I don't know what will happen, but I can see what could happen in a complex, non-linear system and knowing what could happen is enough to make me very cautious.

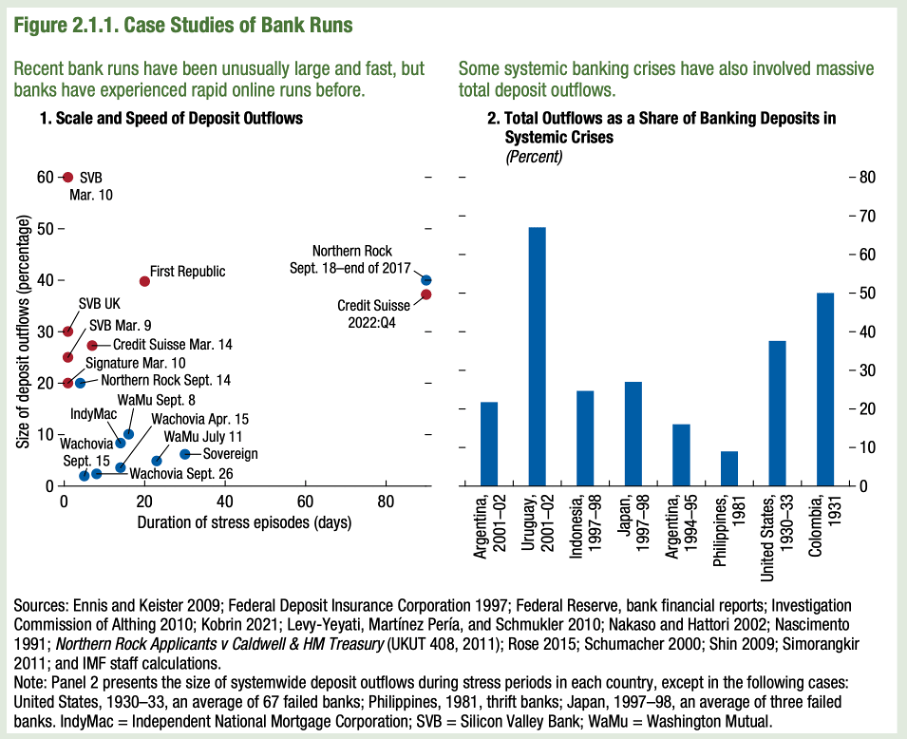

And as sociologist by training, I think I understand a little bit how society works and especially what role trust and confidence is playing in financial markets (and especially when dealing with banks). In the above-mentioned article I also wrote that the situation can change within a few days. The Global Financial Stability Report (October 2023 version) by the IMF is making that point quite well. In a chart it is showing the scale and speed of deposit outflows and how quick bank runs can happen.

IMF Global Financial Stability Report 2023

The authors wrote in the Global Financial Stability Report 2023:

The March 2023 bank runs in Switzerland and the United States were unusually large and fast, with their speed and size facilitated by rapid online deposit withdrawals and the rapid spread of worries among important groups of depositors via social media and other digital channels. This has rightly prompted consideration of possible policy lessons, but the most recent runs also have important similarities with previous bank runs. Although the runs were not as severe and fast as the run on Silicon Valley Bank, banks have experienced rapid online runs before. The 2007 deposit run on the UK bank Northern Rock took place mostly via the internet: The bank lost almost 60 percent of its retail deposits in 2007, including 20 percent over just five days (between September 13 and 17).

Not only is the data showing that bank runs were already happening very quickly in some cases in past decades (we are usually talking about a few days, maybe a few weeks max) but I think the ability to withdraw funds online within seconds is making the risk of bank runs larger in the years to come and could also make it much more difficult to contain such a problem.

And as usual before a big crisis, we are seeing appeasement everywhere. While some people are admitting there could be a crisis on the horizon, such a crisis is often labeled “manageable”. And when admitting that there might be a recession, it is always a soft landing. Powell for example is now also talking about future bank failures and the Fed is admitting additional scenarios to the 2024 stress test (see above), which I believe could be a sign that the Fed is gradually preparing the market for a banking crisis.

We will see what will happen in the coming months and quarters.