Ashley Cooper/The Image Bank via Getty Images

Ashley Cooper/The Image Bank via Getty Images

In a sense, value investing is very much about being a contrarian. During difficult times, the market reacts by pushing shares of businesses down. The very investor, in cases where the downturn is almost certainly temporary, swoops in and buys up the stock at a rather cheap price. The end result, if all goes well, is an eventual recovery that should lead to meaningful upside in the price of units. In an ideal world, investors would not need to wait very long for this to play out. But unfortunately, the world is not perfect. Sometimes, additional patience is required in order for a play to turn out well.

One company that I could point to as an example of this is The Manitowoc Company (NYSE:MTW). For those not familiar with the enterprise, it's engaged in the production and sale of equipment like hydraulic cranes, lattice boom crawler cranes, boom trucks, tower cranes, and more. Back in February of 2023, I ended up writing a bullish article about the company. At that time, both the top and bottom lines for the business were performing well. The stock looked attractively priced and I expected shares to outperform the broader market for the foreseeable future. For a time, things were going quite well. But then, on February 15th of this year, exactly one year after the publication of the aforementioned article, shares tanked, closing down 18.6%. This followed a rather painful fourth quarter earnings release. And as a result, shares are now down 2.6% from when I last wrote about the firm compared to the 20.8% rise seen by the S&P 500. Despite this pain and the expectation that 2024 will not be a year of recovery, the stock does still look attractively priced and I believe that the 'buy' rating I assigned it just requires additional time and patience to play out.

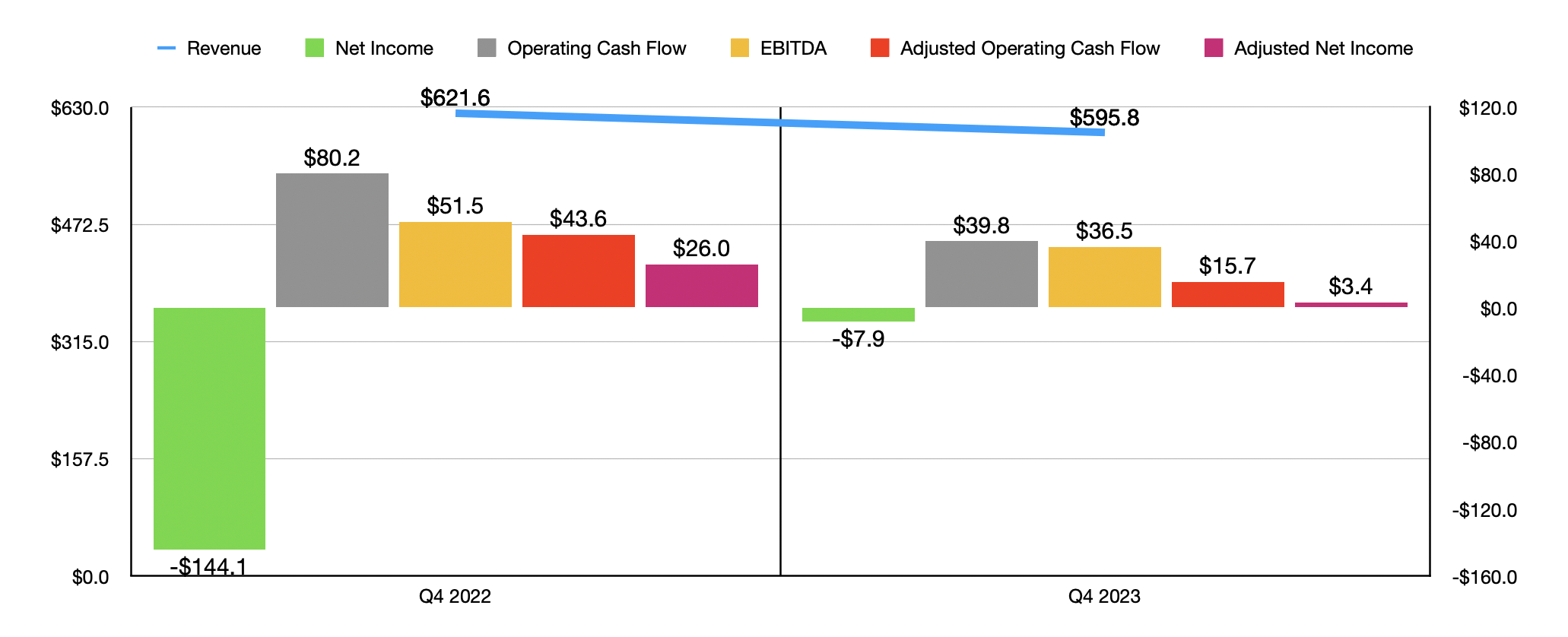

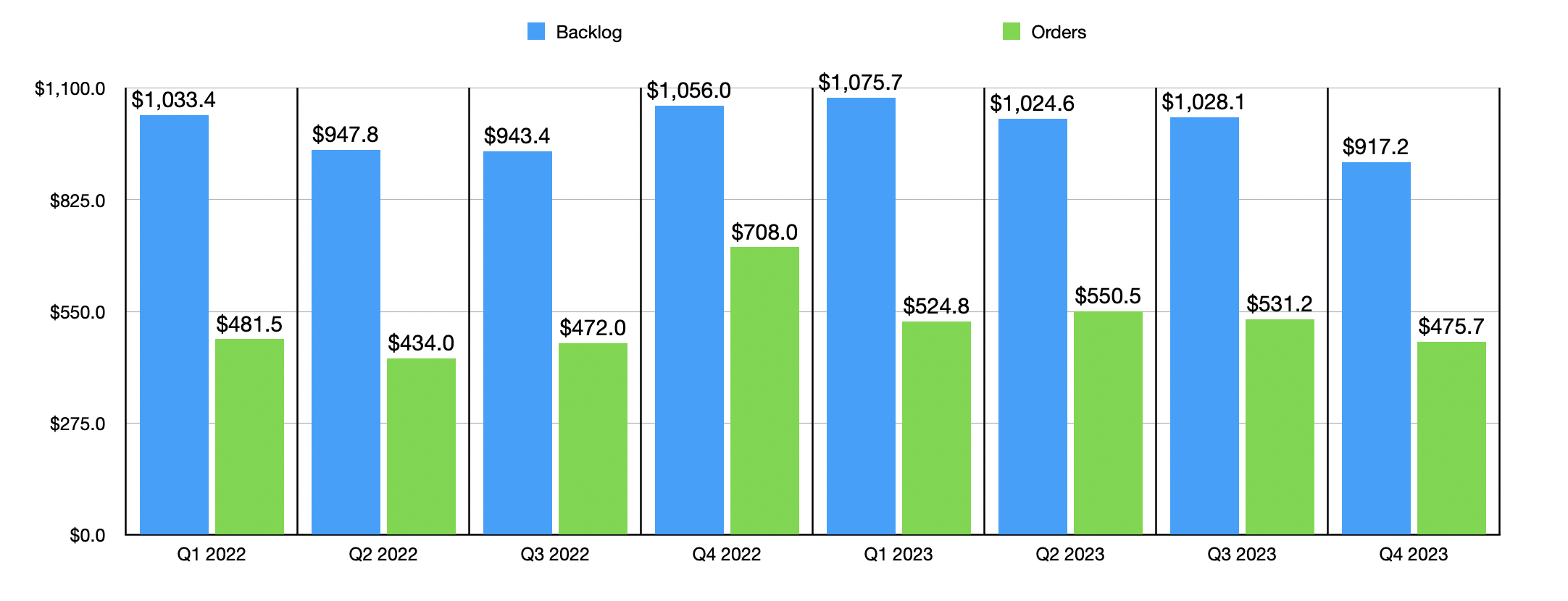

Earlier this month, the management team at Manitowoc announced financial results covering the final quarter of the company's 2023 fiscal year. For that quarter alone, revenue came in at $595.8 million. That's down 4.2% from the $621.6 million generated the same time one year earlier. Interestingly, the situation would have been worse had it not been for a $9 million benefit the company received from foreign currency fluctuations. This decline was expected. In fact, sales ended up exceeding forecasts set by analysts by $12.5 million. But it is important to point out that, although it was an expected decline, it's an unpleasant one. Looking at orders received, this was the first time where, on a year over year basis, the picture was weaker in 2023 than it was the year prior. Overall orders dropped 32.8% in the final quarter of last year relative to the final quarter one year earlier. But compared to the first nine months of 2023 compared to the first nine months of 2022, orders were actually up 15.8% year over year.

Author - SEC EDGAR Data

On the bottom line, the picture has been a bit more volatile. Although the company reported a net loss of $7.9 million for the final quarter of the year, that was far better than the $144.1 million loss reported for one year earlier. On the other hand, operating cash flow dropped from $80.2 million to $39.8 million. On an adjusted basis, it declined from $43.6 million to $15.7 million. Even EBITDA took a hit, declining from $51.5 million to $36.5 million.

Author - SEC EDGAR Data

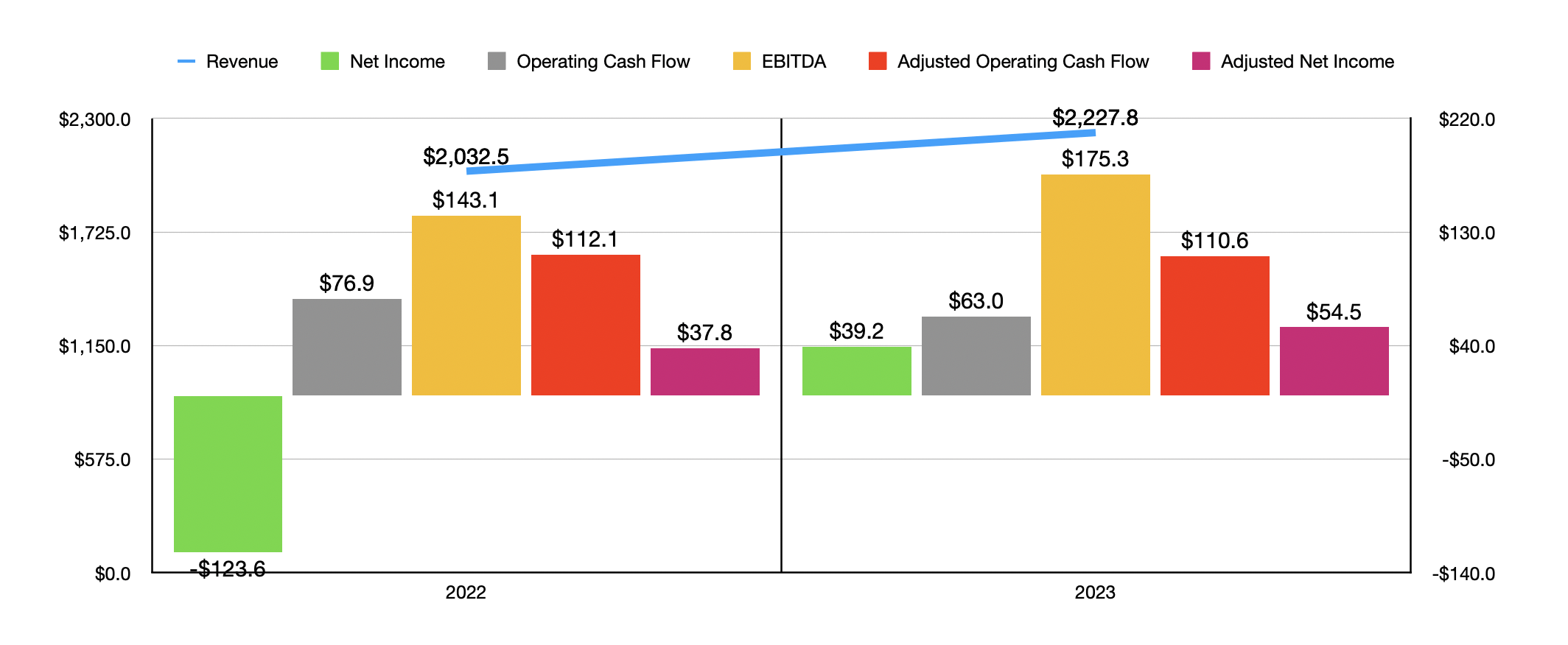

Now, if we were to look at the 2023 fiscal year in its entirety relative to 2022. The picture does look a bit more interesting. In this case, revenue actually was higher year over year as the chart above illustrates. Net profits were better as well. Adjusted operating cash flow was down, but only modestly. And EBITDA for the business managed to climb nicely from $143.1 million to $175.3 million. Only official operating cash flow was materially worse on the bottom line in 2023 relative to the 2022 fiscal year. But even then, the company demonstrated itself to be cash flow positive. Unfortunately, this does not seem to be enough to offset not only the weak orders and the decline in revenue, but also the fact that backlog shrink for the first time since the second quarter of last year. Overall backlog is currently $917.2 million. That represents a decline of $110.9 million reported for the third quarter of the 2023 fiscal year. These are leading indicators that suggest that the future might not be so bright.

Author - SEC EDGAR Data

Despite these weak leading indicators, management is not so sure that the picture will be bad for the year. Even though management expects the European tower crane market to remain 'challenging' throughout 2024, management did say that global demand for mobile cranes should remain strong. Because of this, the company is now forecasting revenue of between $2.275 billion and $2.375 billion. That would be about 4.4% above what the company generated last year if we use the midpoint of guidance. Despite the anticipated strength on the top line, the bottom line is a bit more complicated. Management has a very large range for adjusted earnings guidance. They anticipate adjusted profits per share of between $0.95 and $1.55. If we do take the midpoint of that guidance, it would give us net income of $43.9 million. That would be down from the $54.5 million in adjusted profits generated in 2023. Based on the data provided, it's also likely that adjusted operating cash flow will be around $105 million. That would be down from what it was in 2023. In addition to this, EBITDA should come in at between $150 million and $180 million. Unless it hits the high end of that range, that would represent a drop from the $175.3 million generated in 2023.

Author - SEC EDGAR Data

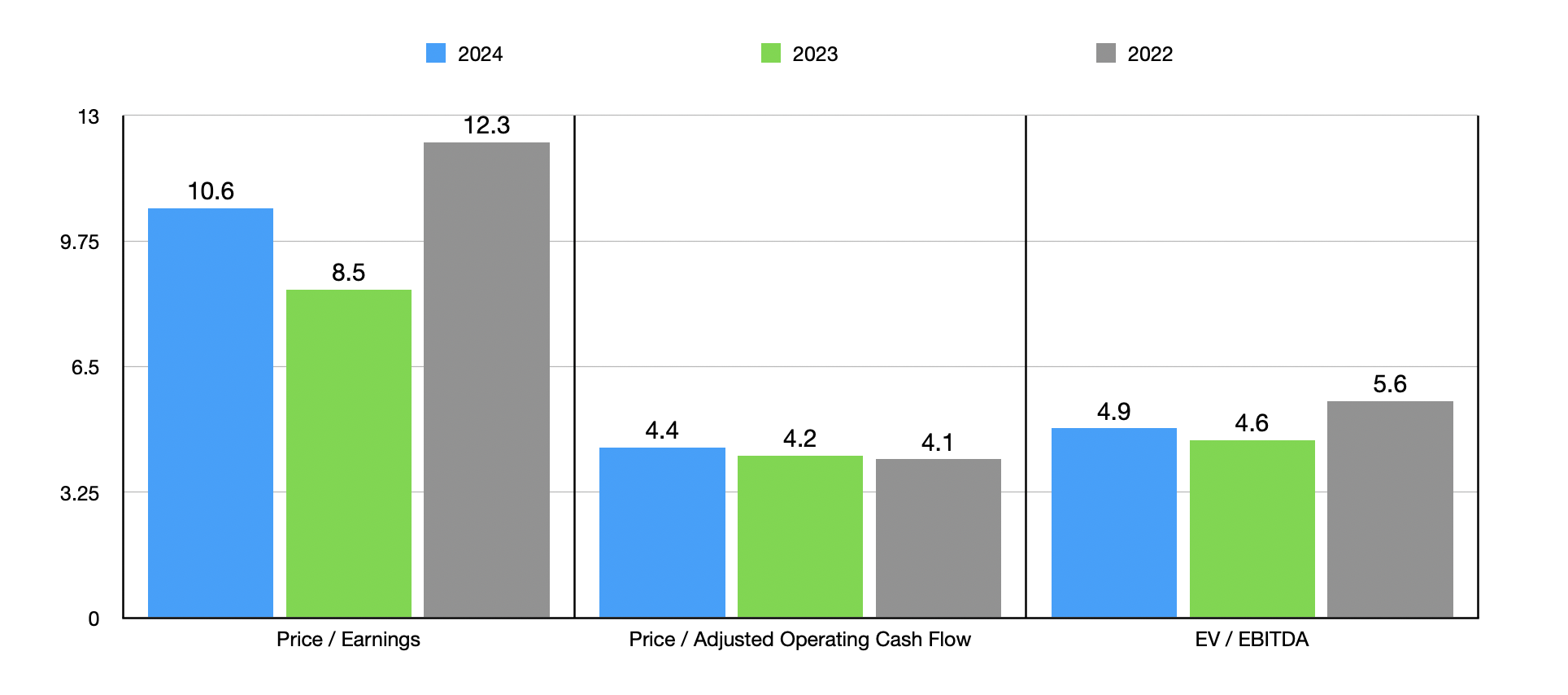

If we assume that management is right in these figures, we can see how shares look on a forward basis in the chart above. The chart also shows how shares are priced using historical data from 2022 and 2023. Even on a forward basis, with multiples expected to be higher than what we would get for last year, the stock does look attractively priced to me. I then, in the table below, decided to compare the firm to five similar enterprises. On a price to earnings basis, two of the five companies ended up being cheaper than our target. But when it comes to the price to operating cash flow approach or the EV to EBITDA approach, only one of the five businesses was cheaper than it.

| Company | Price/Earnings | Price/Operating Cash Flow | EV/EBITDA |

| The Manitowoc Company | 8.5 | 4.2 | 4.6 |

| Terex Corporation (TEX) | 7.3 | 8.2 | 5.7 |

| Wabash National (WNC) | 5.4 | 4.0 | 3.9 |

| Allison Transmission Holdings (ALSN) | 9.5 | 8.1 | 7.9 |

| Trinity Industries (TRN) | 29.8 | 8.4 | 12.1 |

| Westinghouse Air Brake Technologies (WAB) | 29.7 | 20.1 | 15.3 |

It's clear to me that the fundamental performance of Manitowoc is not ideal at this time. But it's during times like this when the best opportunities arise. Although there is no guarantee about the future, the fact that shares look cheap even after factoring in weakness is a major positive. Add on top of this how attractively priced units are compared to similar firms, and I remain confident that the 'buy' rating I assigned the stock previously is still logical.