Klaus Vedfelt

Klaus Vedfelt

In my previous analysis of WFE (wafer front end) semiconductor equipment, Applied Materials, Inc. (NASDAQ:AMAT) had lost its market share dominance to ASML Holding N.V. (ASML) in 2023. Now, AMAT has announced its latest earnings. At the time of my December 5, 2023, Seeking Alpha article entitled "Applied Materials: Weak Earnings Means ASML Takes Over The #1 Equipment Spot In 2023," AMAT had only reported earnings through Q3 2023. This article presents semiconductor equipment sales for all companies in this analysis for the entire year, which incidentally does not include service or spare parts.

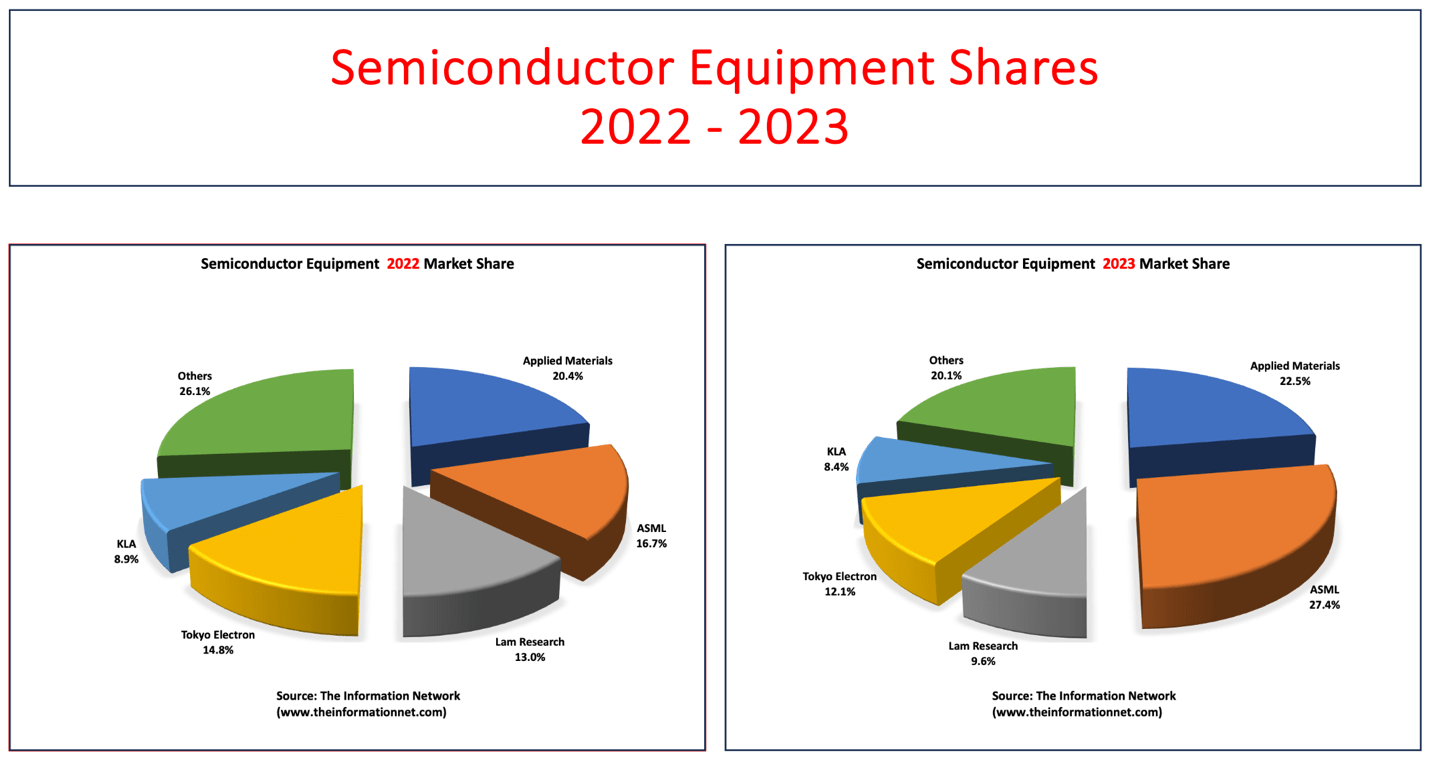

As shown in Chart 1, according to The Information Network’s report entitled “Global Semiconductor Equipment: Markets, Market Shares and Market Forecasts,” AMAT relinquishment of its top position—a status it maintained for two decades, with the exception of 2019 when ASML previously claimed the lead.

I believe that 2024 will be a challenging year for AMAT, tied to ASML's sanctioned high-end DUV lithography systems to China, which would have required AMAT's etch and deposition equipment for multi-patterning, and ASML's High-NA EUV lithography equipment, which doesn't require AMATs equipment.

These financial factors are combined with AMAT's significant legal problems, in which it has been receiving subpoenas from the U.S. Securities and Exchange Commission and from the U.S. Attorney’s Office for the District of Massachusetts in February 2024, and from the U.S. Attorney’s Office for the District of Massachusetts in August 2022 and February 2024, and the U.S. Commerce Department’s Bureau of Industry and Security in November 2023. As a result, I rate this company a Sell and caution investors of the implications for AMAT management.

In the midst of China sanctions throughout 2022 and 2023, ASML ascended to the pinnacle of the Wafer Front End Semiconductor Equipment market in 2023, surpassing Applied Materials to become the leading supplier. ASML’s share rocketed to 27.4% from 16.7% in 2022.

According to ASML’s Q4 2023 earnings call, CFO Roger Dassen reported:

“Looking at the full year, net sales grew 30% to €27.6 billion, with a gross margin of 51.3%. EUV system sales grew 30% to €9.1 billion, realized from 53 systems while a total, we shipped 42 EUV systems in 2023. DUV system sales grew 60% to €12.3 billion.”

The Information Network

Chart 1

AMAT's semiconductor revenues grew by just $26 million QoQ in the latest quarter despite strong revenue from China, which I discuss below. For 2023, revenue dropped $253 million YoY. This compares to ASML, which grew $345 million QoQ and $7.9 billion YoY for the calendar year.

Tokyo Electron Limited (TOELF, TOELY), hailing from Japan, found itself in third place following a significant following a market share drop from 14.8% in 2022 to 12.1%. Tokyo Electron and other Japanese firms such as Hitachi High-Tech, Screen, and Kokusai, were adversely affected by the strong U.S. dollar in the second half of 2023, which led to a 2% reduction in their revenues (when measured in U.S. dollars) in the fourth quarter of 2023.

This downturn mirrored the challenges faced by Lam Research (LRCX), which also saw a considerable market share decrease from 13.0% to 9.6%.

KLA Corporation (KLAC) rounded out the Top 5 companies as its share dropped slightly from 8.9% to 8.4%.

There were several factors impacting market share changes in 2023.

On the negative side, a strong U.S. dollar against the Japanese Yen affected sales by -2% for Tokyo Electron and other Japanese companies.

The memory market was mired by a downturn through all of 2023, as I discussed in my July 24, 2023, Seeking Alpha article "Lam Research Earnings: All Eyes On Memory Chip Recovery." This sector's vulnerability, exacerbated by diminished demands for end products such as PCs and smartphones, directly impacted companies with a high exposure to the memory market, including Lam and Tokyo Electron.

On a positive note, strong sales to China lifted the WFE market, primarily for mid-critical and mature nodes in China. Imports of equipment needed to produce semiconductors rose by 14% in 2023 to $40 billion.

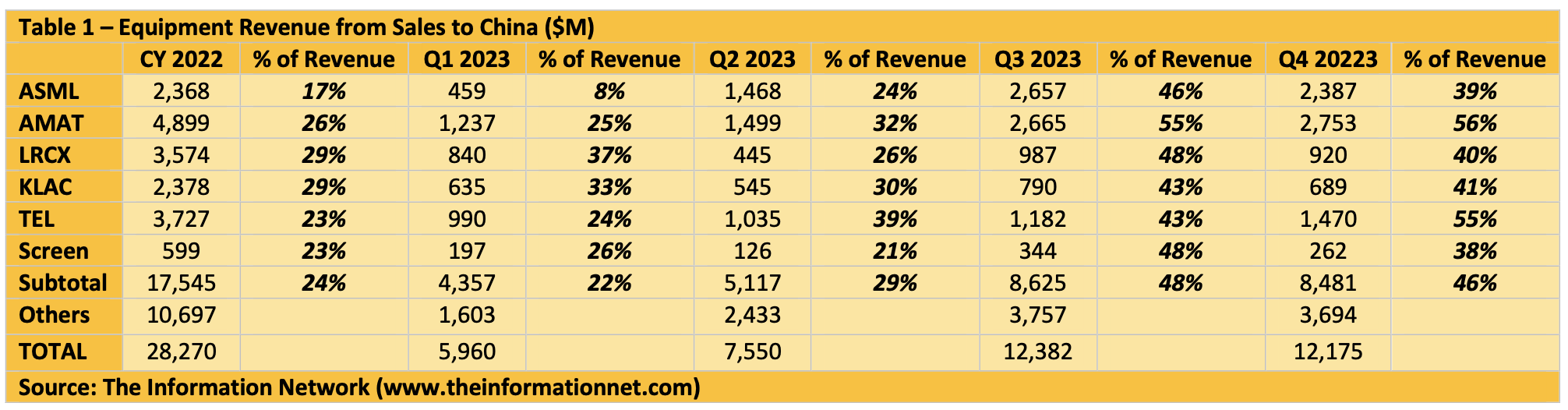

In Table 2, I show the Top 6 Semiconductor equipment companies and their China revenues and percentage of revenues generated from China for CY 2022 and Q1-Q4 2023. In Q3, the % of revenue was nearly the same for each company but elevated, indicating that Chinese semiconductor companies are importing equipment irrespective of process equipment type.

In CY2022, shown to the left of the table, revenues from China were 22%. This is similar to the 22% and 29% in Q1 2023 and Q2 2023, respectively.

But in Q3 and Q4 2023 we see an explosive growth in revenues, from pull-ins of equipment slated for 2024 as well as a hoarding of equipment by Chinese companies prior to anticipation of further, more deeply impacting sanctions.

Also noted in Table 1 is the large percentage of revenues from China by AMAT. This 55% and 56%, higher than competitors, helped AMAT gain 2% of market share in 2023.

The Information Network

Looking back at Table 1, in Q4 2024 ASML generated 39% of revenues from China. While still significantly larger than the 17% in 2022, it slowed in Q4 2023. An important consideration for the other companies in 2024 is that DUV lithography sales, even though in 2023, semiconductor equipment was imported for the processing of mature and mid-critical nodes to China, as vendors complied with export control regulations.

Why? Because DUV lithography on its own only works up to the 39nm technology node. Lower than that, multi-patterning processes need to be used, and these processes use deposition and etch equipment from AMAT. Limiting DUV sales to China for mature and mid-critical nodes will significantly impact AMAT's sales of etch and deposition equipment, which I discuss below.

As for the impact on U.S. sanctions on China, in October 2023, the U.S. government published updated export control regulations, according to ASML. The regulations consist of both an update from the October communication of the previous year and the implementation of U.S. regulations within the trilateral agreement involving the Dutch, Japanese, and U.S. governments.

On October 17, 2023, the US Department of Commerce's Bureau of Industry and Security ("BIS") declared that lithography machines with a maximum "dedicated chuck overlay (DCO)" value between 1.5nm and 2.4nm are prohibited from being shipped from the U.S. to China. The DCO value serves as an indicator of imaging performance, with smaller values indicating higher accuracy.

Under these new rules, the BIS has imposed a ban on shipments of ASML's NXT:1980Di and NXT:1970Ci machines, which have maximum DCO values of 1.6nm and 2nm, respectively, from the U.S. to China. As of now, there is no indication that the Dutch government will follow suit.

ASML expects that these sanctions will impact its sales to China by -10 to -15%. And that would mean lower sales from AMAT, LRCX, and TEL.

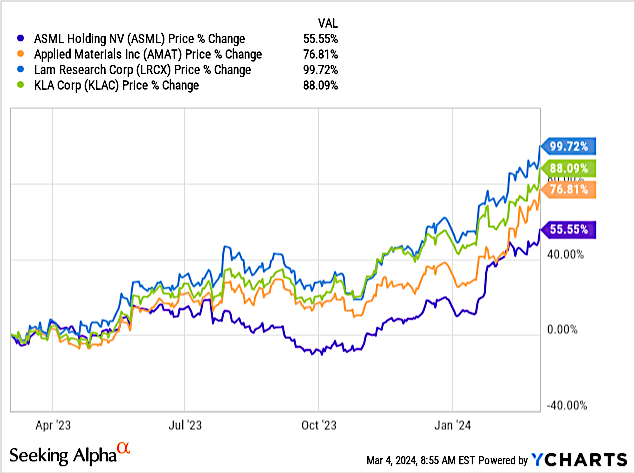

Chart 2 shows share price for ASML, AMAT, LRCX, and KLAC over a 1-year period. ASML’s performance is worse than competitors despite the strong top-end revenue growth in 2023. LRCX, which fared worse, shows the strongest growth.

YCharts

Chart 2

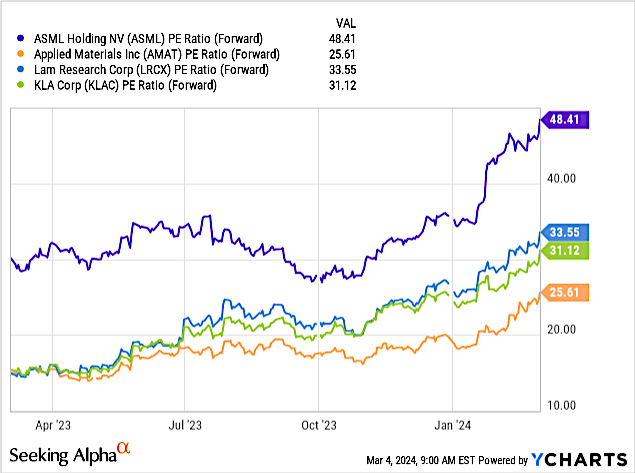

Chart 3 shows the Forward P/E ratio of the four companies indicating ASML is overbought at 48.41x and AMAT at the lowest at 25.61x. Note that AMAT has an attractive forward P/E ratio despite revenues that dropped $253 million YoY in 2023.

I also suggest that AMAT's gain of 2 percentage points in market share is a result of a significant drop of 6 percentage points by the "other" equipment companies indicated in Chart 1 above. As Chinese companies began hoarding Western Equipment in 2H 2023, as shown in Table 1, they were primarily buying from the top equipment manufacturers analyzed in this article. Thus, smaller companies outside the Top 5 in this article, were passed over for equipment purchases.

YCharts

Chart 3

For 2024, I see a recovery of WFE revenues, which dropped double digits in 2023, but because of pull-ins from 2024, primarily by Chinese semiconductor companies, this recover won’t happen until 2H 2024.

Restrictions on ASML shipping advanced DUV systems (and of course EUV systems) will have limited impact on ASML, but a much larger impact on companies selling deposition and etch systems for multi-patterning.

Based on forward P/E ratios in Chart 3, AMAT has the lowest forward P/E ratio and makes the company attractive. However, I have great concern about the company’s business strategy.

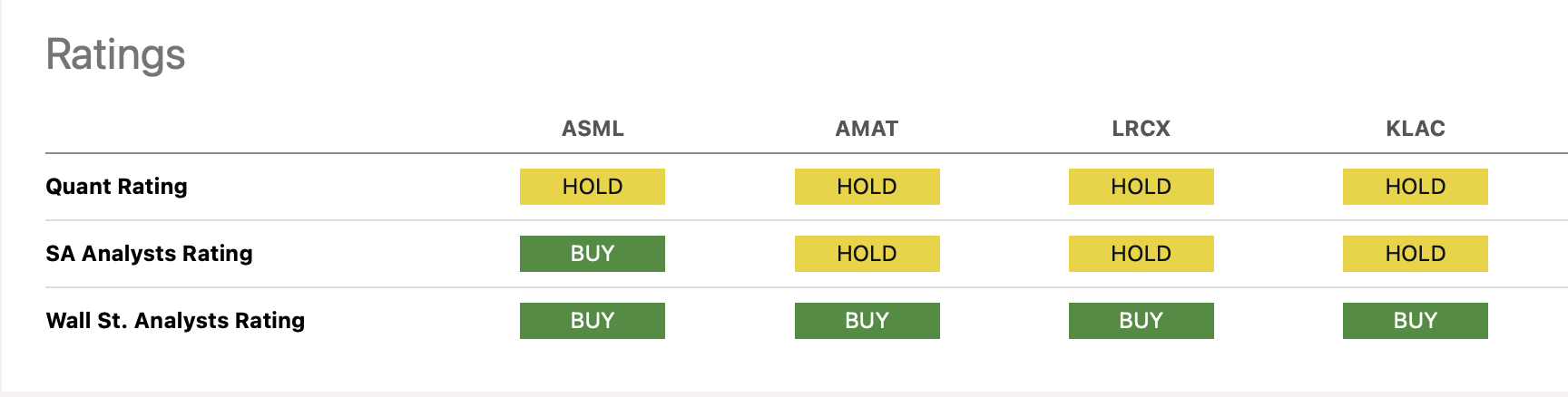

Chart 4 shows Ratings of the four companies. Seeking Alpha’s Quant Rating is a Hold for all four companies, although all have a Buy rating from Wall St. Analysts.

Seeking Alpha

Chart 4

I already reported that AMAT managed to move $331 million in revenues in three tranches from 2018 revenues into 2019 to improve market share. It didn’t work, as ASML took over the #1 spot from AMAT for the first time in 20 years. Curiously, not one analyst reported these antics.

Now we learn of another head fake from AMAT – allegations that the company has shipped sanctioned equipment to China in violation of U.S. sanction laws. According to Seeking Alpha news, AMAT received multiple subpoenas from U.S. government authorities seeking information pertaining to its China shipments:

The semiconductor firm received subpoenas from the U.S. Securities and Exchange Commission in February 2024. It also received a subpoena from the U.S. Attorney’s Office for the District of Massachusetts in the same month requesting information related to certain federal award applications.

The recent subpoenas are in addition to ones received from the U.S. Attorney’s Office for the District of Massachusetts in August 2022 and February 2024, as well as from the U.S. Commerce Department’s Bureau of Industry and Security in November 2023.

Sales of its deposition and etch systems, which normally compliment lithography DUV systems from ASML will be impacted by China sanctions and by advanced High-NA EUV. While sales for AMAT were strong in China in 2023 without U.S. sanctions, this growth will not be mirrored in 2024.

I also caution investors that several different government departments have issued subpoenas against AMAT. This is serious, and could ultimately lead to implications for AMAT's management, raising the question "where does the buck stop."

In conclusion, I rate this company a Sell.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.