AsianDream/iStock Editorial via Getty Images

AsianDream/iStock Editorial via Getty Images

According to World Population Review, emerging countries are those whose economy is not yet fully developed, but likely will be in the near future.

Emerging countries are also known as emerging economies because the emphasis is on their economic development. There are some emerging countries that you have probably heard of and some that may be less familiar. Nevertheless, pay attention to these countries - you probably buy food that was grown there or wear clothes that were made there. You will probably hear more about these countries soon.

Some of the more commonly known emerging countries include Brazil, Russia, India, and China (the BRIC countries). But there are also many other countries that are rich in oil or other natural resources. Some of those countries include Saudi Arabia, Qatar, and Bahrain.

Countries like Mexico, Vietnam, and Taiwan are replacing China in terms of exporting goods to the US. Other emerging countries in Eastern Europe including Hungary, Romania, and Bulgaria are seeing improved economic growth now that they are no longer under Communist rule from the former Soviet Union.

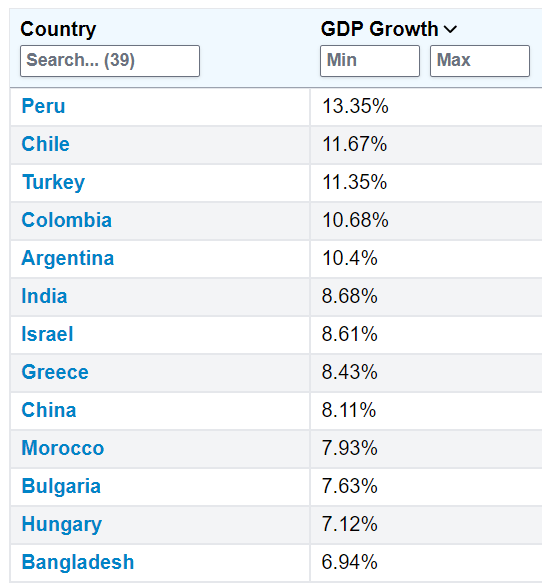

Some African countries are experiencing growth in their emerging economies too, including Nigeria, South Africa, and Morocco. In South America countries like Peru, Chile, Colombia, and Argentina are showing signs of economic growth. Some countries in Southeast Asia are also EM countries including Indonesia, Sri Lanka, and even Bangladesh.

The table below shows GDP growth in 2021 for some of the top EM countries.

World Population Review

In an October 2023 insight from Deloitte, the outlook for emerging markets is seeing supply chains shifting away from China which is leading to improvement in other emerging markets that are picking up the slack and have helped to propel the gains in their economies beyond their developed market peers.

Earlier this year, numerous emerging market economies benefitted from strong demand in the rest of the world and the relatively high commodity prices that accompanied that demand. A handful of countries have also benefitted from changes in global supply chains, as many businesses look to shift some manufacturing away from China.

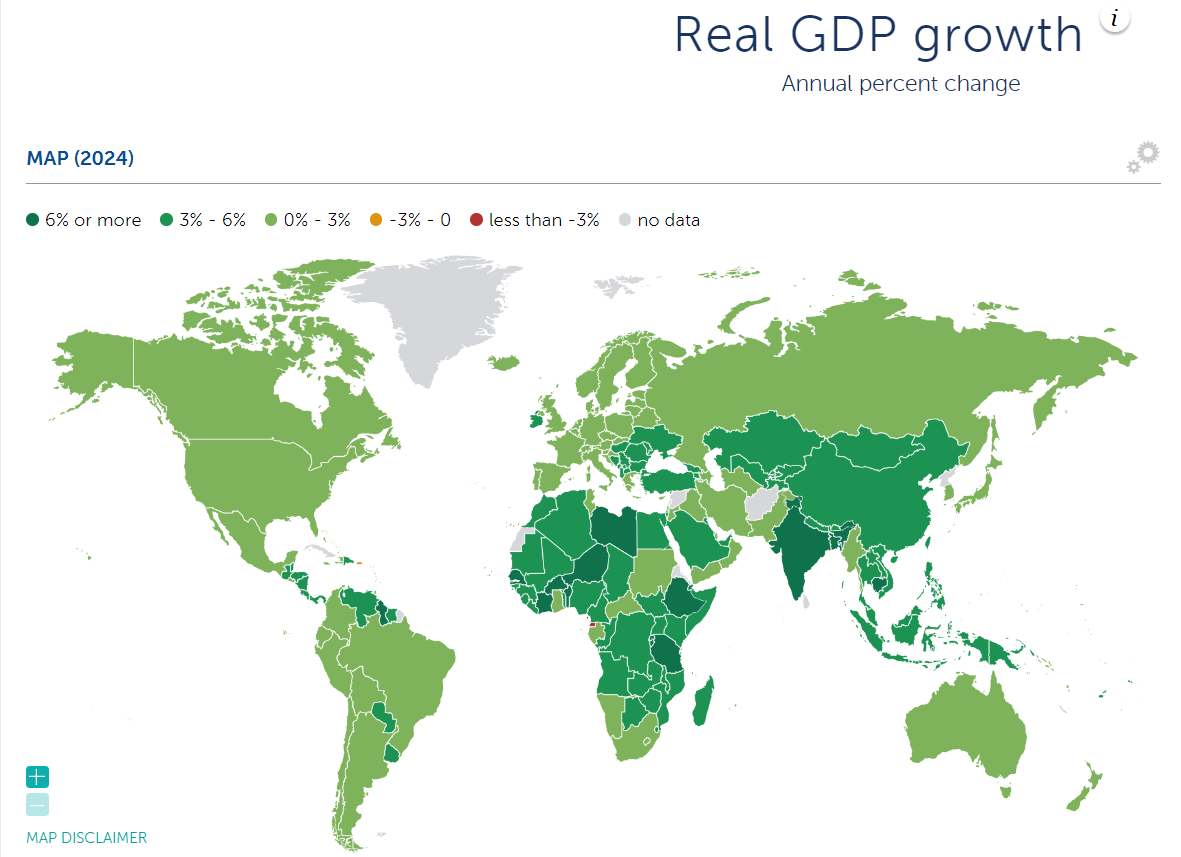

This map from IMF shows real GDP growth graphically as of October 2023 and you can see that Africa, India, eastern Europe, southeast Asia, and parts of South America witnessed strong GDP growth in 2023.

IMF

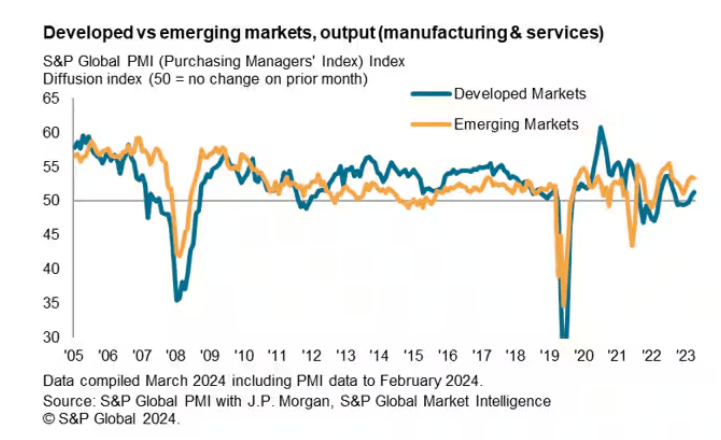

Furthermore, emerging markets continue to outpace developed markets now in the third month of 2024 according to this report from S&P Global.

The emerging market expansion sustained into the second month of 2024, according to PMI data, extending the sequence of growth that commenced in January 2023. Despite slowing slightly from the start of the year, the rate of expansion remained amongst the fastest in the past eight months and also surpassed that of developed markets, the latter seeing growth accelerate to the fastest since June 2023. This has altogether been supportive of global growth midway into the first quarter.

S&P Global

As an income-oriented investor, one way to benefit from this macro trend is to buy shares of a CEF that holds fixed income securities in emerging markets. There are several CEFs available to retail investors that specialize in emerging market bonds and one that I like right now and own shares of in my Income Compounder portfolio is EDF.

The EDF fund seeks to maximize total return and high current income by investing in a managed portfolio of EM fixed income securities with a flexible allocation to local currency sovereign debt, hard currency sovereign debt, and EM corporate debt. According to a recent story from Vanguard, 2024 is an excellent time to consider investing in EM bonds.

In addition to attractive valuations, the EM asset class benefits from a unique combination of wide spreads and long duration, something that neither U.S. IG nor U.S. HY can offer. This leaves EM debt uniquely poised to benefit from a rally in rates as central banks cut, and from supportive risk appetite as growth normalizes. With historically expensive valuations in U.S. corporate bonds and strong investor demand for fixed income assets, EM debt stands to benefit. Increasing demand is likely to overwhelm supply in the coming months, helping drive outperformance in EM debt.

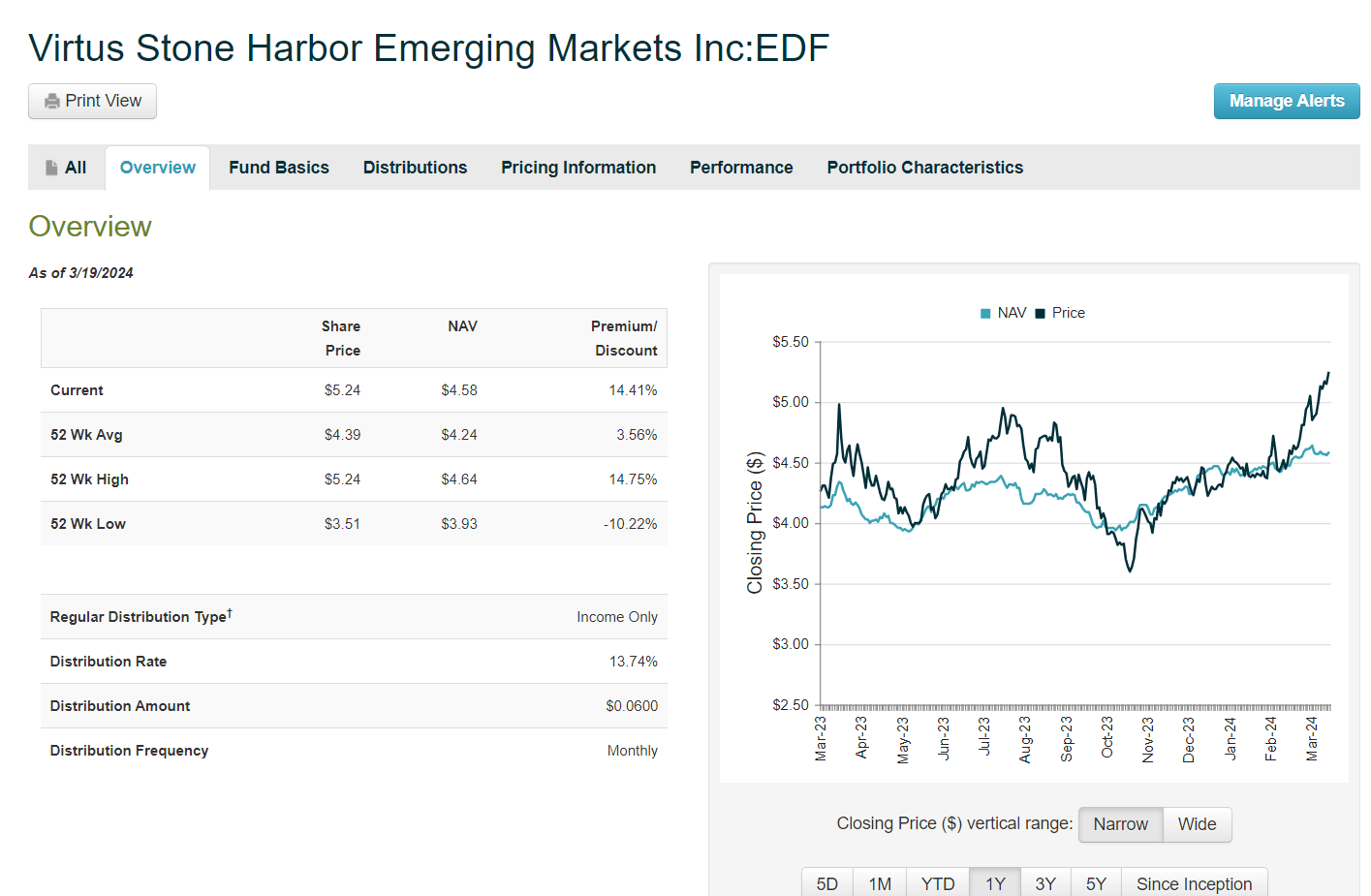

I hold a small position in EDF as a proactive allocation to EM bonds in my IC portfolio, but recently trimmed my position as the premium to NAV has risen substantially in the past few months. Part of the reason for the change in premium was likely due to the completion of the reorganization with the former EDI fund (Virtus Stone Harbor Emerging Markets Total Income Fund) that was merged into EDF last year. The reorganization was completed in December and EDF has soared since then.

As can be seen in the chart from CEF Connect below, the fund traded at a discount back in October 2023 and then moved to a small premium in December before shooting higher to what is now close to the highest premium in the past year at over 14% above NAV. As a result, I rate the fund a Hold at the current price of $5.31 as of market close on March 20, 2024.

CEF Connect

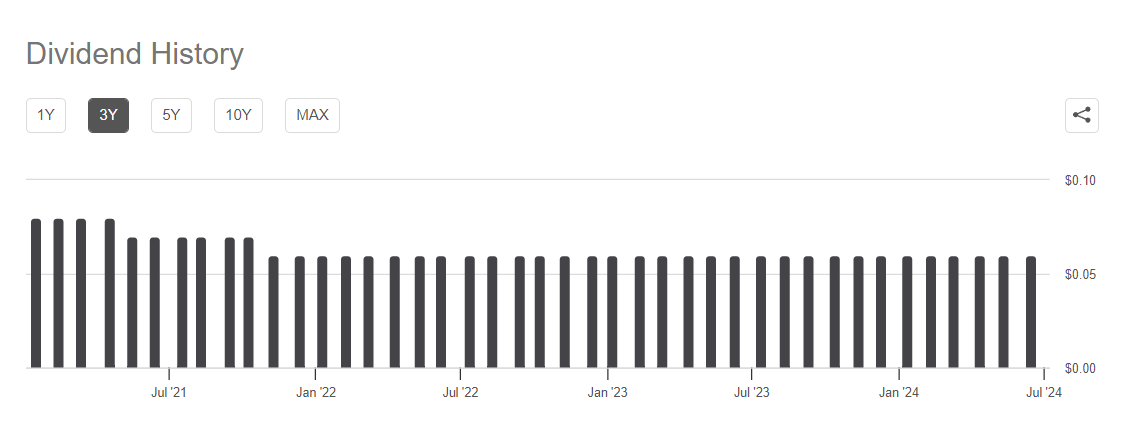

Yet even though the price of the fund has risen dramatically since the start of the year, the NAV is also increasing and EDF offers investors a monthly distribution of $0.06 resulting in a yield on cost of about 13.7%. The distributions have been set at a steady, level distribution and have remained the same since November 2021 when it was reduced from $0.07.

Seeking Alpha

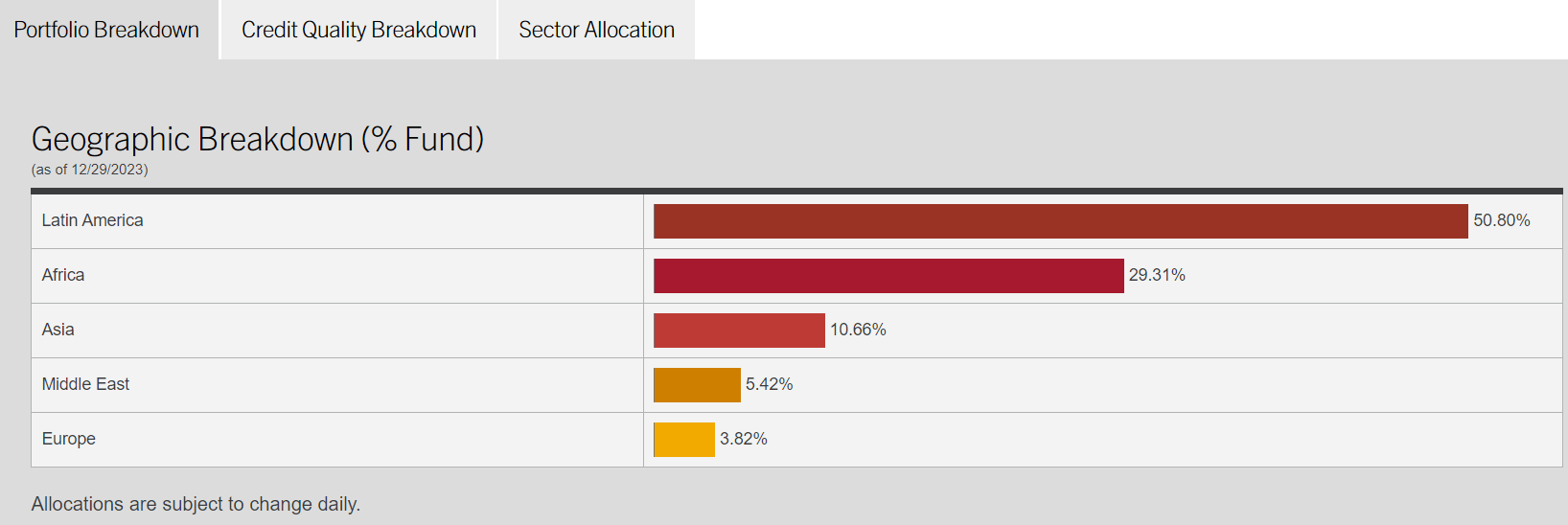

According to the website, EDF currently holds 130 positions with total net assets of $132 million. It uses an effective leverage of 26.5% based on reverse repurchase agreements resulting in total managed assets of $179.7 million. Those assets are graphically dispersed with over 50% in Latin America as shown in this graphic dated 12/29/23.

EDF website

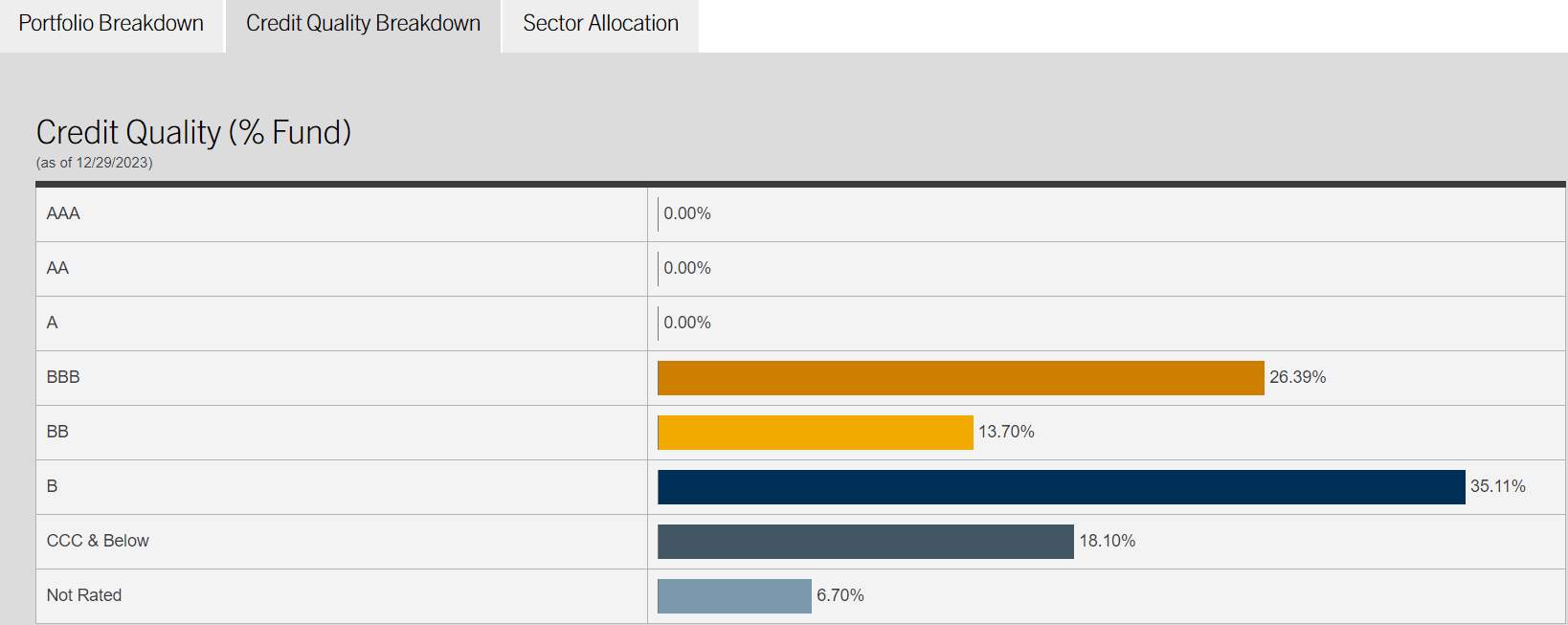

As you might expect, the credit quality in EDF holdings is mostly below investment grade (which results in higher yields from those investments, but also represents higher risk). The investment grade rating of BBB suggests that about a quarter of the holdings are above investment grade with the rest "junk" (below IG) rated at BB and below.

EDF website

As of the end of 2023, roughly 55% of the securities were held in sovereign hard currency, 25% in corporate bonds, and roughly 20% in sovereign local currency.

The management team includes Stone Harbor Investment Partners, a global credit specialist with expertise in emerging markets and over 30 years of experience.

EDF website

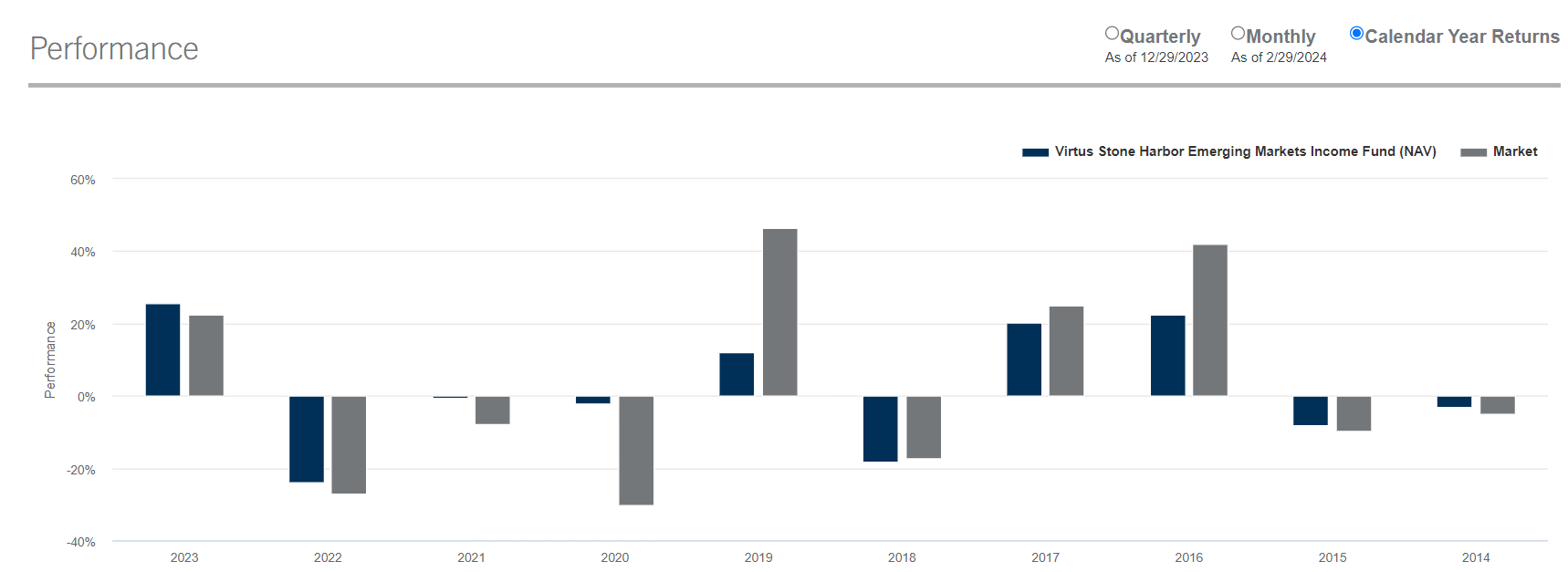

The EDF fund was originally incepted in 2010 by Stone Harbor and in 2022, Virtus acquired the assets of Stone Harbor and renamed the fund. As you can see in the chart of past performance, the fund struggled in previous years with 2022 being an especially bad year for the fund, while in 2023 things began to turn around.

EDF website

While some analysts dislike EDF because of its past performance, there were many contributors to that poor performance that are no longer in play today. One recent example is the impact that the COVID-19 pandemic had on EM economies, which were hit harder and have been slower to recover than developed economies.

Now in early 2024, credit conditions have improved, inflation is coming down, and EM economies are poised to outperform their developed peers in the coming months. This research article from S&P Global in February summarizes the improving conditions for EM economies.

Credit conditions in Emerging Markets (EMs) have improved. In Q4 2023, the pace of defaults in EMs was lower than in the U.S. and Europe, following better economic and financing conditions, continued disinflation, positive growth surprises, and a clearer path for Fed policy interest rate cuts. Issuances outside Greater China rose by more than 20% in January compared with December.

With the focus on countries in Latin America especially, EDF is well positioned to benefit from the improving conditions in EM countries. As the growth outlook from Deloitte explains, those countries are some that are best positioned to benefit from improved consumer spending and reduced inflation.

Countries in Latin America and Eastern Europe are likely best positioned to usher in the strongest growth in consumer spending. Part of this is because their economies had been mired in recession earlier and are now poised for a recovery.

… Emerging market economies that have tamed inflation will be in the best position to keep economic activity moving in the right direction while the rest of the world struggles to avoid recession.

While EDF has demonstrated an ability to grow the fund with its EDI merger and use of leverage, it is not without risks. One risk is that the fund trades at a relatively high premium to its current NAV.

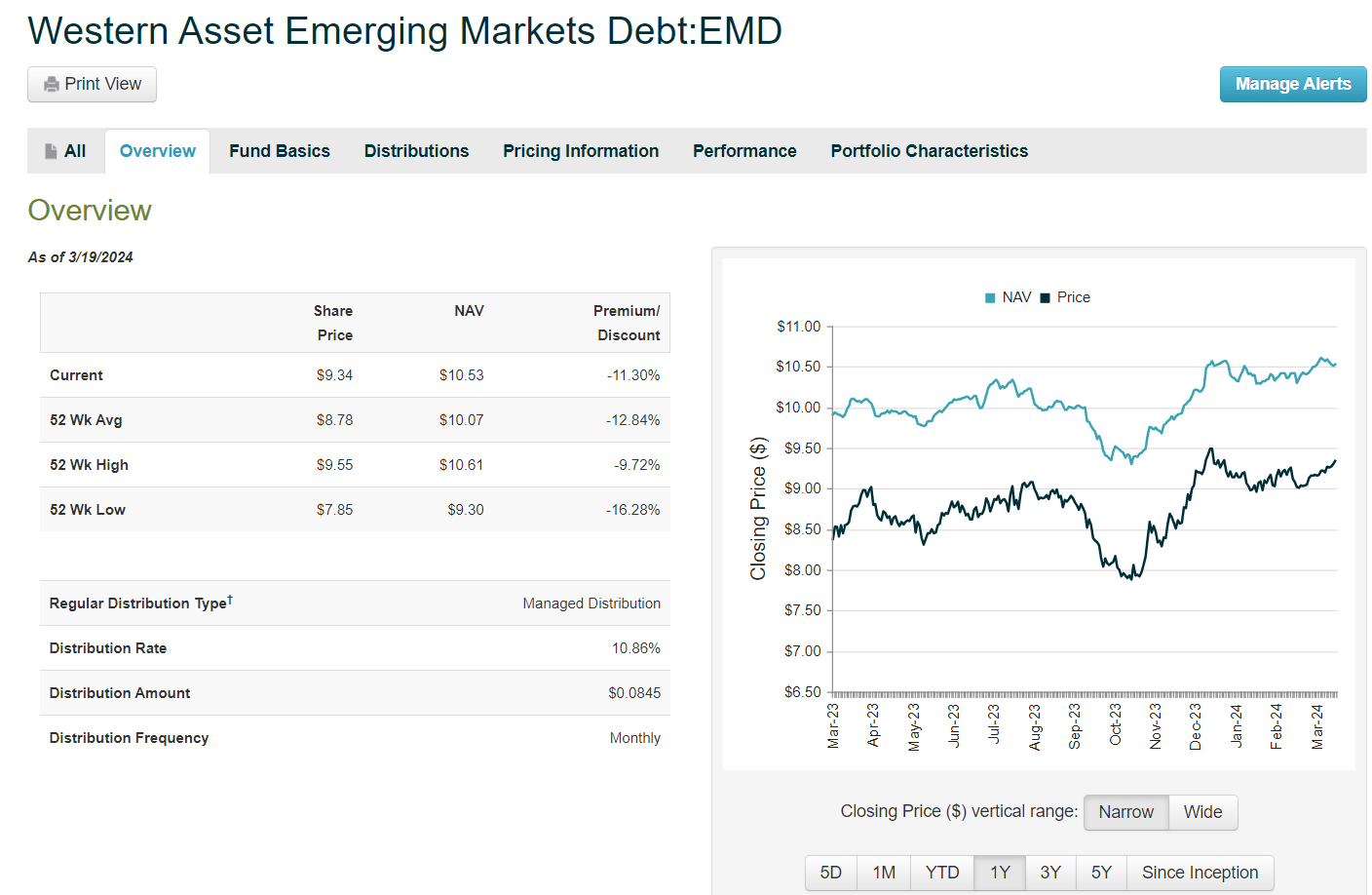

While EDF is one fund to consider in the EM fixed income space, another CEF that also offers a high-yield distribution that is based on EM bonds and other fixed income securities is the Western Asset Emerging Markets Debt Fund Inc (EMD). While EDF trades at a premium of about 14% and yields about 14%, EMD trades at a discount to NAV of about -11.3% and offers a yield of about 10.8%. If you are interested in a fund that will likely benefit from the improving conditions in EM countries and you are looking to start a new position in a fund that offers a potential strong total return, EMD may be the better option right now.

The EMD discount is beginning to close as the NAV is rising. Last year the distribution was increased with the October payout rising from $0.07 per share monthly to $0.0845.

CEF Connect

Like EDF, the past performance since the end of 2021 was not great, but EMD is now turning around and offers a potential strong total return in 2024. I recently used some of my EDF shares that I sold for a profit to start a new position in EMD. I intend to hold both funds and add to them whenever there are any substantial price drops that the market offers while collecting the monthly high-yield distributions from both.

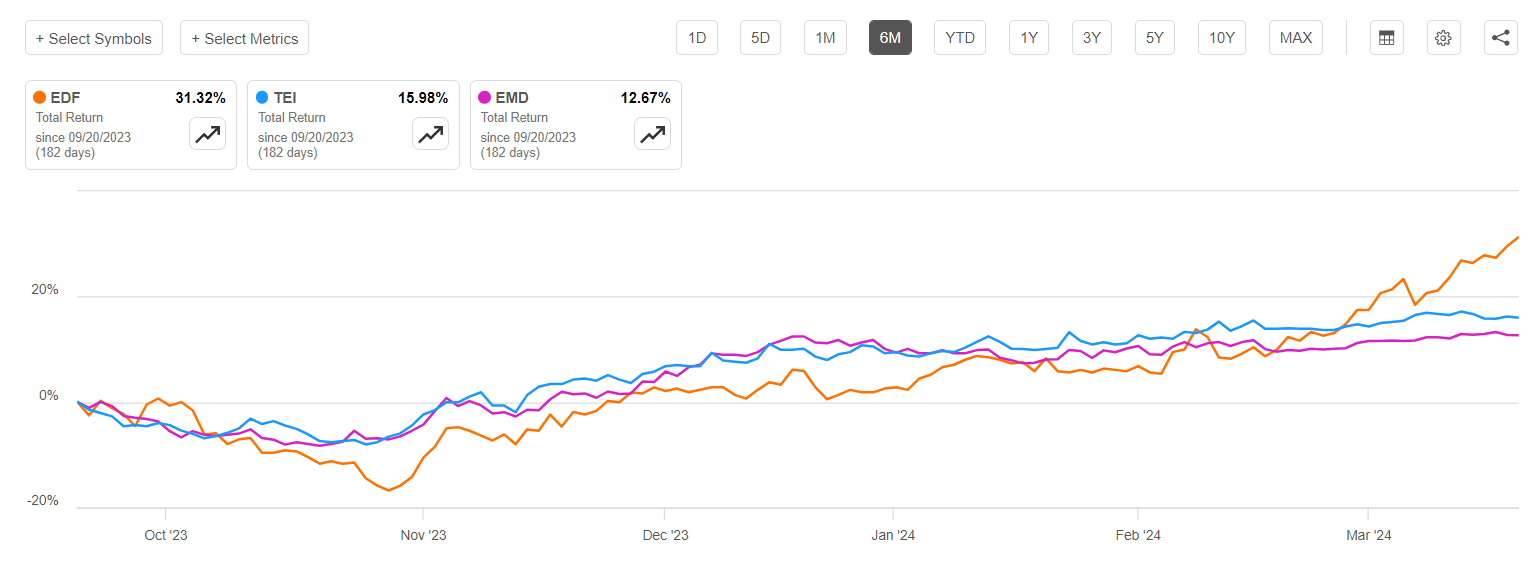

Another EM bond fund to consider is TEI. Like EMD, the TEI fund offers a distribution of about 10.8% (based on a $0.0475 monthly distribution) and trades at a discount of about -12% to NAV. TEI is smaller than EMD and uses less leverage but has seen similar performance over the past year. Overall, EDF has seen by far the best performance of the three due to the recent run-up in price over the past couple of months.

Seeking Alpha

If you are looking for a diversified source of income in your retirement portfolio, or just want to add some exposure to non-US fixed income securities, you may want to consider adding an EM fixed income fund to your portfolio. According to Vanguard, there are several good reasons to add EM bonds in 2024:

Vanguard's active fixed income team believes emerging markets (EM) bonds could outperform much of the rest of the fixed income market in 2024 because of the likelihood of declining global interest rates, the current yield premium over U.S. investment-grade bonds, and a longer duration profile than U.S. high yield.

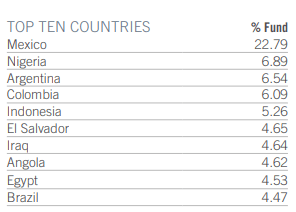

The approach taken by the EDF closed-end fund has resulted in a strong total return over the past year with a rising premium enhancing the total return of the fund to more than 52% (with dividends reinvested). The top 10 holdings are focused on Mexico and other Latin American countries as shown on the fund fact sheet (as of 12/31/23).

EDF website

While EDF currently trades at a relatively high premium, that premium may be justified by the high yield distribution that appears to be well covered after the merger with the EDI fund. If you are interested in an EM fixed income fund that does not trade at such a high premium but instead trades at a discount, you may wish to consider EMD. I like both funds and hold shares of both in my Income Compounder portfolio.