landbysea/iStock via Getty Images

landbysea/iStock via Getty Images

Note:

Tidewater Inc. (NYSE:TDW) has been covered by me previously, so investors should view this article as an update to my earlier publications on the company.

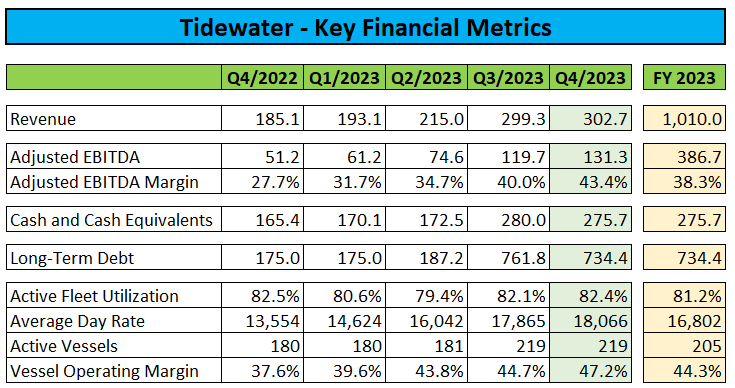

Last month, leading offshore support vessel and services provider Tidewater Inc. or "Tidewater" reported improved fourth quarter and full year 2023 results:

Company Press Releases / Regulatory Filings

The company's vessel operating margin (equivalent to gross margin) of 47.2% and average day rate of $18,066 represented new multi-year highs thus resulting in vastly increased profitability with Adjusted EBITDA reaching $131.3 million.

While these numbers were largely in line with the management's guidance and consensus estimates, market participants' expectations had been somewhat muted following two consecutive bottom line misses.

But unlike previous quarters, Tidewater's results were not materially impacted by elevated repair, mobilization and fleet integration costs in conjunction with the recent acquisition of 37 platform supply vessels ("PSVs") from Solstad Offshore.

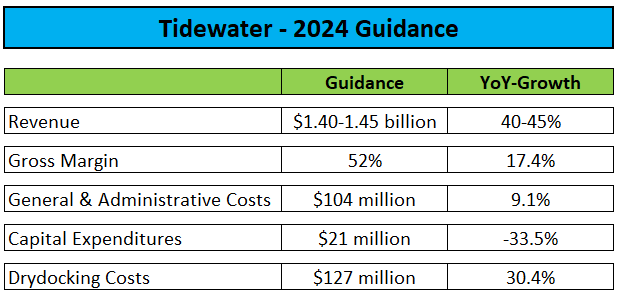

On the conference call, management also provided detailed guidance for 2024:

Conference Call Transcript

Based on these numbers, I would expect Adjusted EBITDA to increase by almost 65% to approximately $635 million this year.

The company's current backlog stands at $1.1 billion with 75% of available days for 2024 already fixed.

While seasonality will result in Q1 revenues increasing only modestly over Q4, management expects strong improvements in both Q2 and Q3 followed by a less-pronounced increase in Q4.

Q1 gross margin is expected at 45% with margins projected to increase to 56% in Q4.

In addition, the company authorized a new $48.6 million share repurchase program which represents the maximum permissible amount under Tidewater's existing debt agreements.

According to statements made by management on the conference call, the company continues to prioritize accretive growth:

More broadly, as we think about capital allocation throughout 2024, the share repurchase program will be an important feature of how we allocate our capital. Acquisitions remain a capital allocation priority as we do believe there are viable candidates that can be acquired on an accretive basis that will allow us to leverage our shore-based infrastructure and to take advantage of the economies of scale that the Tidewater platform provides.

Nevertheless, Tidewater expects to return to a net cash position in the second half of 2025:

We will continue to weigh the relative merits of any given acquisition against the value of the share repurchases and pursue the most accretive alternative. We remain mindful of our balance sheet and we want to maintain a clear line of sight to a net cash position within six quarters. Ultimately, our goal is to establish a long-term debt capital structure more appropriate for a cyclical business, and we will act opportunistically to do so as we progress through the year.

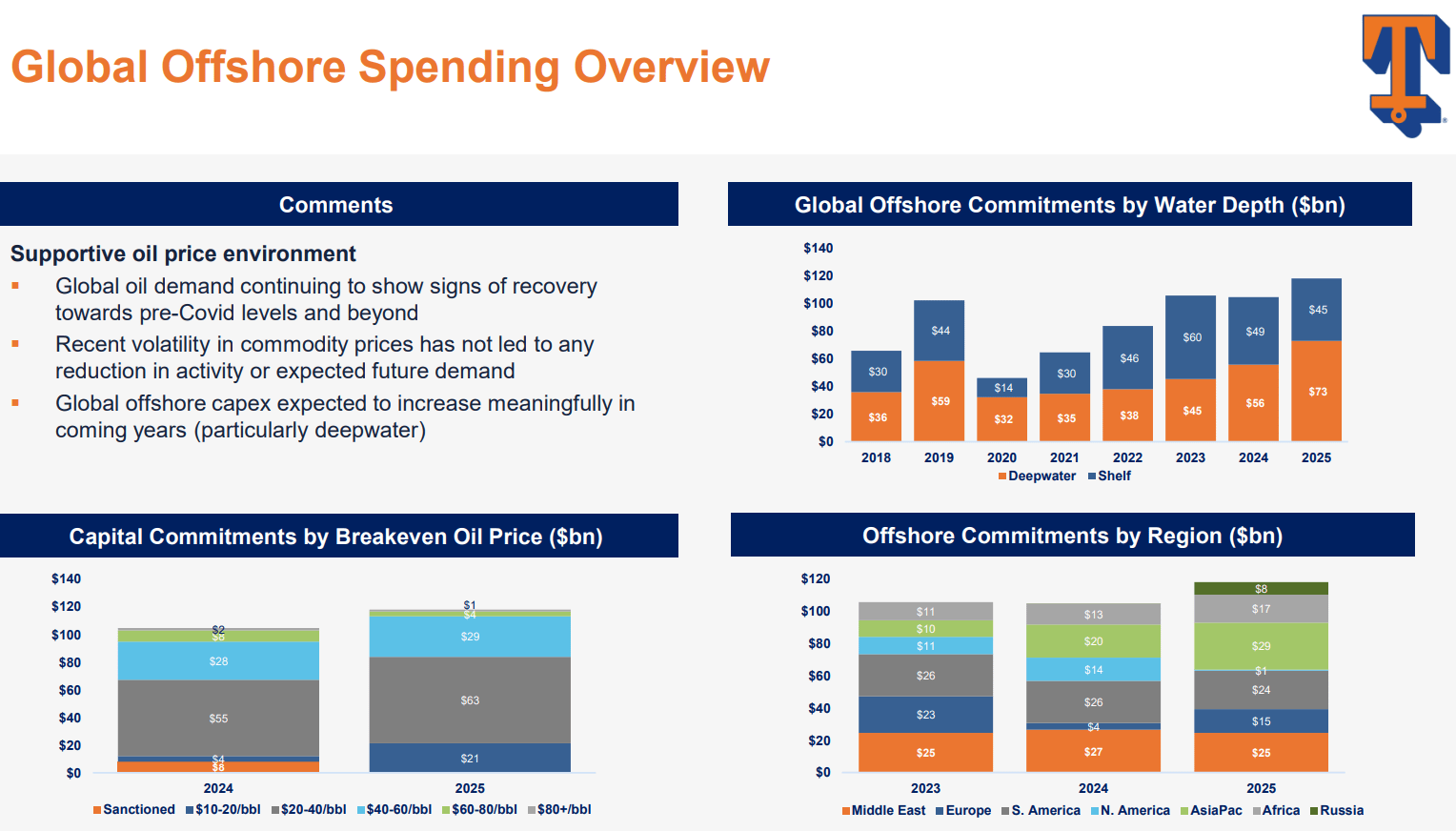

Considering increased deepwater spending commitments, the outlook for offshore support vessel providers remains strong:

Company Presentation

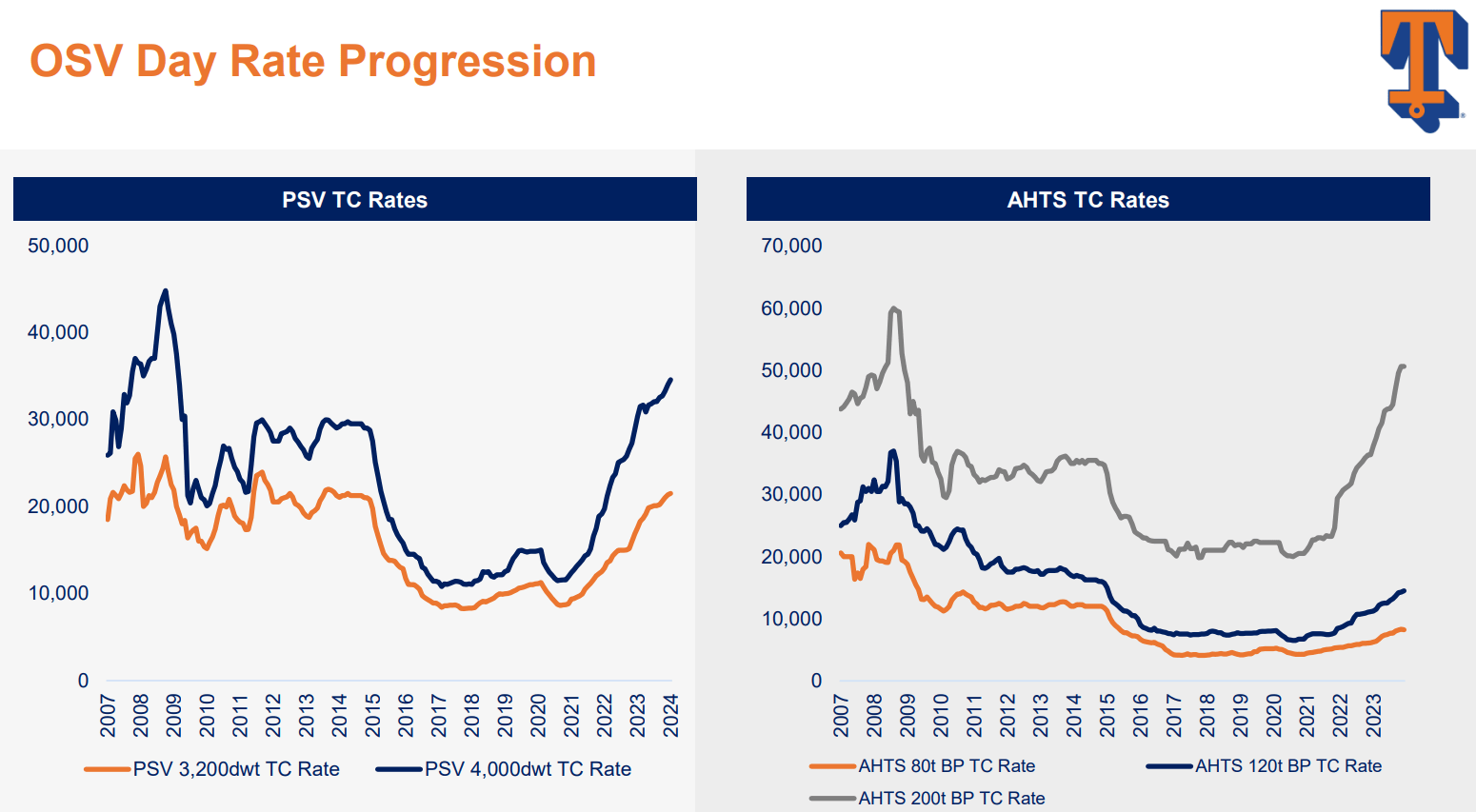

Particularly larger PSVs have seen strong demand in recent quarters with leading dayrates at 15-year highs:

Company Presentation

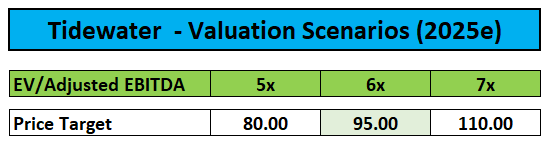

While I remain constructive on offshore oil and gas service providers, the most recent rally has resulted in Tidewater's shares trading within 5% of my increased $95.00 price target.

Author's Estimates

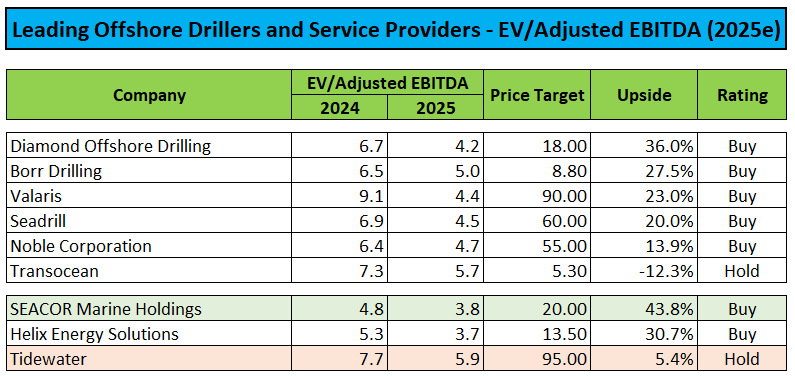

Considering the fact that a number of offshore drillers and particularly smaller competitor SEACOR Marine Holdings (SMHI) or "SEACOR Marine" offer substantially higher upside, I am downgrading Tidewater's shares from "Buy" to "Hold".

Author's Estimates and Calculations

Please note that this downgrade is solely based on valuation and does not reflect any sort of fundamental concerns but with the company's closest U.S. exchange-listed competitor offering more than 40% upside from current share price levels, I would prefer SEACOR Marine over industry leader Tidewater.

However, investors should be aware of the fact that SEACOR Marine's expected earnings trajectory is not yet fully visible in the company's numbers and liquidity in the stock isn't great. Similar to Tidewater, shares are trading near multi-year highs.

Following two consecutive misses, Tidewater's fourth quarter results managed to live up to expectations thus resulting in a 15% post-earnings move in the shares. In combination with strong tailwinds from a multi-week oil price rally, the stock is approaching my upwardly revised $95 price target.

With a number of offshore drillers and particularly closest U.S. exchange-listed competitor SEACOR Marine Holdings offering substantially higher upside, I am downgrading Tidewater's shares from "Buy" to "Hold".

However, I remain constructive on the outlook for offshore oil and gas service providers as a whole.