Monty Rakusen

Monty Rakusen

TransDigm (NYSE:TDG) supplies components used in military and commercial aircrafts. In the latest quarter, TransDigm's results beat analysts' estimates once again, delivering strong growth across all three segments. Today, we'll dive into the company's latest results, assess the business model and strategy, and unpack the company's valuation to assess whether shares are a buy today.

TransDigm is a supplier of critical components used in aircrafts. It does both the design and production of these components, which includes everything from ignition systems, engine technology, specialized pumps, power conditioning devices, and sensor products. The vast majority (55%) of its sales include aftermarket content and proprietary products that are sold to customers in both commercial aircraft and military and defense aircraft.

With just under 50 independent operating companies employing 7000 people, each company has a focus on a particular vertical or strategy. Under the TransDigm umbrella, they all work together to deliver highly engineered products to customers in an efficient and timely manner.

TransDigm is unique in that the company seeks to deliver 'private equity-like returns' to shareholders through disciplined capital allocation. Over the years, a key part of the company's success can be attributed to its ability to acquire small tuck-ins to create value and develop new business lines and cost cutting initiatives to enhance the bottom line on a per share basis.

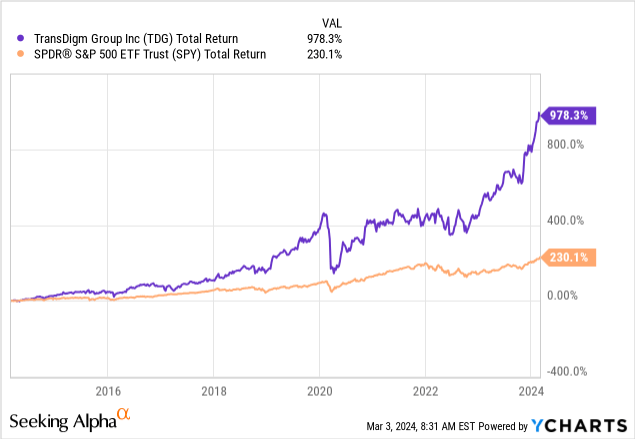

Shares of TransDigm have performed exceptionally over the years. In the last ten years, the company's shares have returned 978.3%, up over 10-fold compared to the S&P500's total return of 230.1%. Had an investor bought and held for the last decade, they would have been sitting on a stock that would have returned them a CAGR of 26.8%.

While multiple expansion can be attributed partially to the company's returns, this share price outperformance is largely backed up by impressive growth in the company's financials. Over the last decade, TransDigm's revenues have compounded at a 13.1% CAGR with EBITDA growing at a CAGR of 14.2%. In the last two decades, the revenue and EBITDA CAGRs are slightly higher, growing at 16.8% and 17.8%, respectively. As the company's EBITDA has grown at a quicker rate than its sales, this demonstrates that TransDigm has been able to expand margins over time. Its current margins are quite impressive at 48.8% for the full year 2023 (source: S&P Capital IQ).

Author, based on data from S&P Capital IQ

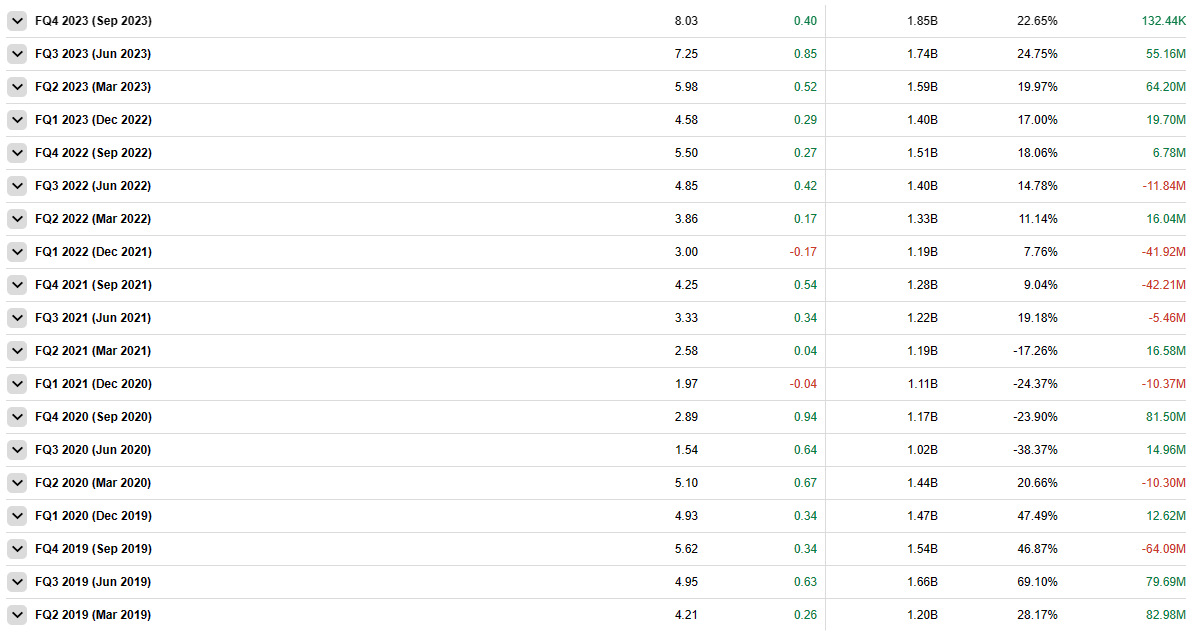

When looking at the latest quarterly results for Q1 2024, TransDigm seemed to have performed well with a beat on both revenue and EPS for the quarter. In the company's quarterly results released on February 8th, TransDigm had revenues clock in at $1.79 billion, which beat consensus estimates by $108.8 million. EPS also beat consensus estimates of $6.40 with adjusted EPS coming in at $7.16 per share.

Quarterly Highlights (Investor Presentation)

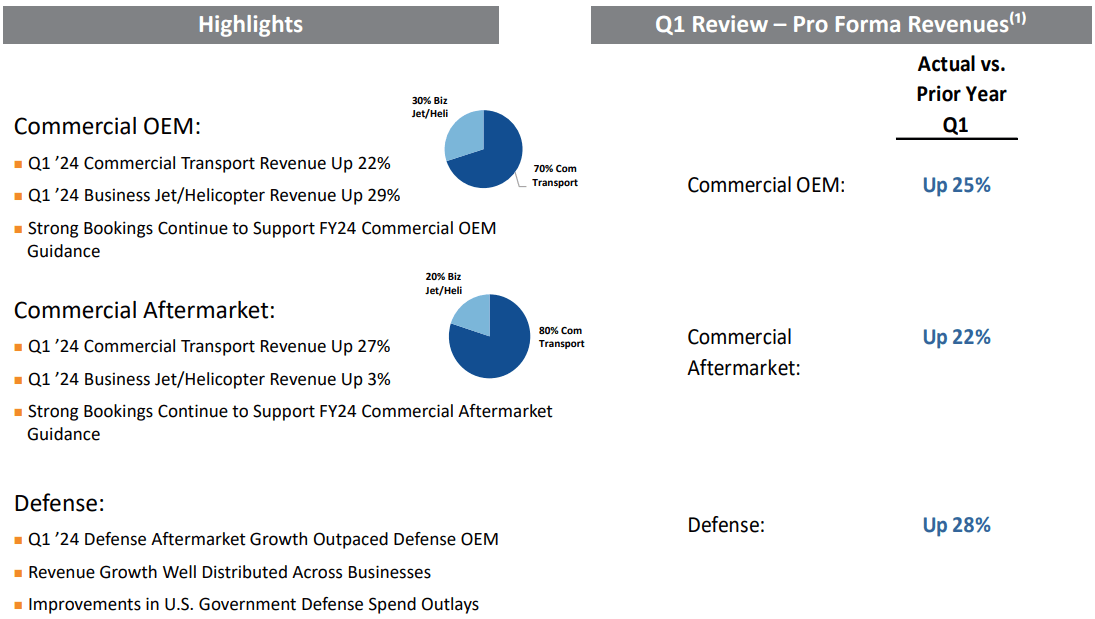

Across all three segments, revenues were up over 20% in each of the company's main businesses. In Commercial OEM, Commercial Aftermarket, and Defense, the segments' strong growth was driven by strong customer demand as well as contributions from the Calspan acquisition, which was a $725 million all cash deal announced in May of last year that added $200 million of annual revenues to TransDigm's top line.

As illustrated by the company's track record, this acquisition is consistent with its strategy of adding complementary businesses to its operations and allowing them to operate independently. Since many of these companies are often times the only providers of such parts or specialized components for aircrafts, TransDigm enjoys tremendous pricing power and acquisitions have proven themselves as a good way for deploying capital consistent with this vision.

In Commercial OEM, sales were up 25% compared to last year's Q1, driven by demand from both commercial transport as well as business aircraft. Up 22% in commercial transport and 29% in business aircraft, a major trend that should continue to drive this is growth in bookings. With higher production rates of OEM aircraft, this bodes well for TransDigm who's products can be found on virtually every modern aircraft today. While Boeing did announce that they will slow production for the 737 MAX, the rest of the market has been looking pretty strong with higher booking rates.

In Commercial Aftermarket, revenues were 22% higher against the same quarter last year, with similar trends highlighted by Commercial OEM. Demand tends to be fairly stable and consistent long-term but lumpy in the short term. In the passenger submarket, bookings remain elevated, which shows indications that the air travel market is recovering. As many who follow the industry will know, it's taken a long time for air travel to reach its pre-pandemic levels, and so the fact that it's just 2.5% below 2019 levels suggest that a recovery is well underway. The International Air Transport Association (IATA) is forecasting demand to reach 104% of 2019 levels in 2024 and 111% of 2019 levels in 2025. With more domestic and international journeys via air, TransDigm should benefit as aftermarket demand for components trends upwards driven by these tailwinds.

Finally, in defense, the company's largest segment during the quarter at 38% of sales, revenues were up 28% year over year. While defense bookings were up considerably against the previous year, we should keep in mind that this is generally not a fast growing segment for TransDigm. U.S. government spending has been strong and is expected to continue, but TransDigm does foresee some deceleration as per guidance forecasting growth between low-single digits to high-single digits in 2024.

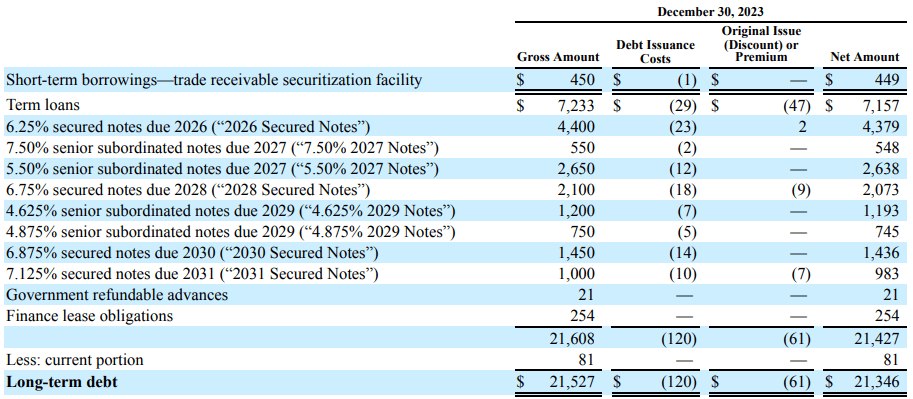

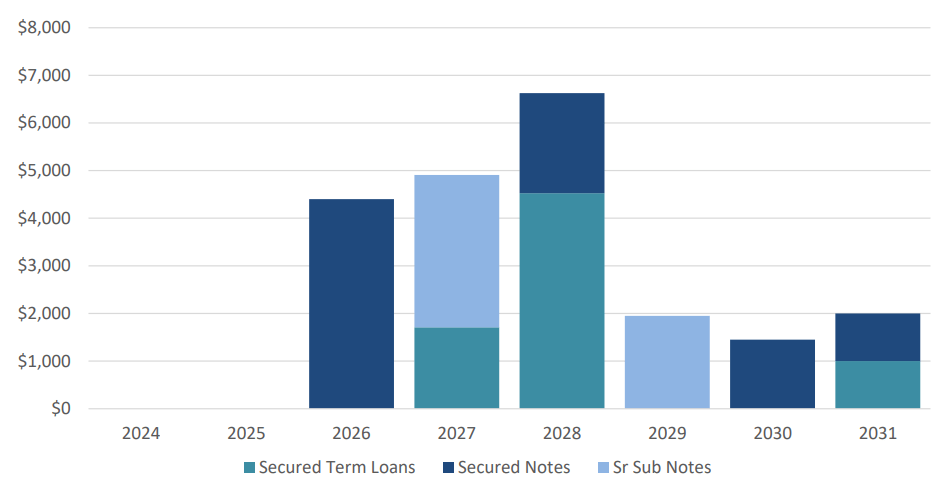

At the end of the quarter, TransDigm had $4.2 billion of cash on its balance sheet with long-term debt of $21.1 billion. With a Net Debt to EBITDA ratio of 5.0x, TransDigm has a pretty heavy debt load, but this ratio isn't unusual compared to what it's historically carried on its books. The vast majority of its debt is secured at fixed interest rates with long-dated maturities, so there isn't an immediate refinancing risk. The weighted average interest rate is 6.3%.

Company Filings Debt Maturity Profile (Investor Presentation)

As for my outlook, I would expect revenue growth of 15%+ in the near term. This is consistent with the last five years of growth and is consistent with management's guidance for 20% growth in commercial OEM, mid-teens growth in the commercial aftermarket, and high-single digit growth in defense for 2024. Importantly, this guidance doesn't include any additional impact from new acquisitions yet to be announced. For an acquisitive company like TransDigm, it's likely that the company will exceed its own guidance. Historically, TransDigm has had a reputation for under-promising and overdelivering. Looking at the quarterly EPS figures over the last five years (20 quarters), there have been only two quarters when EPS came in below consensus estimates. While past performance is not an indicator of future results, great companies led by disciplined capital allocators tend to surprise to the upside long-term.

EPS History (Seeking Alpha )

Regarding the company's profitability, management is guiding for $29.97 to $31.73 of EPS for the full year 2024. To me, I think it's very likely that the company could exceed this. While the company did have to revise guidance lower as a result of higher interest expense expected as a result of the issuance of $2 billion of debt in November 2023, margins have been pretty high at 51% EBITDA margins. That 51% figure is higher than what we've historically seen, and so if that can continue even at 50%, there's reason to believe that EPS range could be surpassed.

Longer term, TransDigm is likely to benefit from strong tailwinds in the global aerospace aftermarket market, which is expected to reach a market size of $38.3 billion by 2030. Growing at a 4% CAGR, I believe TransDigm's growth rate can exceed the industry growth rate due to its pricing power and tuck-in acquisitions that can meaningfully move the needle over the long run.

Based on the 18 sellside analysts who cover TransDigm's stock, there are 14 'buy' ratings and 4 'hold' ratings with an average price target is $1,246.71, with a high estimate of $1,380.00 and a low estimate of $1,050.00 (source: TD Securities). From the current price to the average price target one year out, this implies potential upside of 5.4% so it seems that analysts are moderately bullish on the company's near-term outlook.

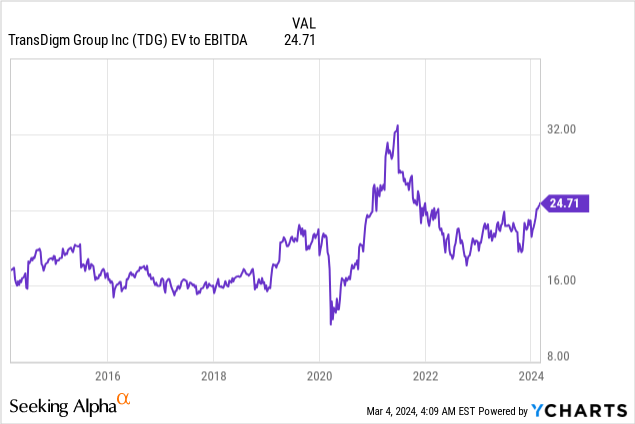

With TransDigm's own estimate for $2 billion of free cash flow in 2024, it's not exactly a cheap stock, with an enterprise value of $83.5 billion (41x free cash flow). The EV/EBITDA multiple has also climbed in recent years to 24.7x; at the higher end of the historical range. While the market has certainly picked up on the fact that TransDigm is a high quality growth company with a strong moat, the valuation seems a bit stretched for now. Keep in mind that at 24.7x EBITDA, the interest expense here is a real expense, as TransDigm pays out a little over $1.3 billion annually to service its debt.

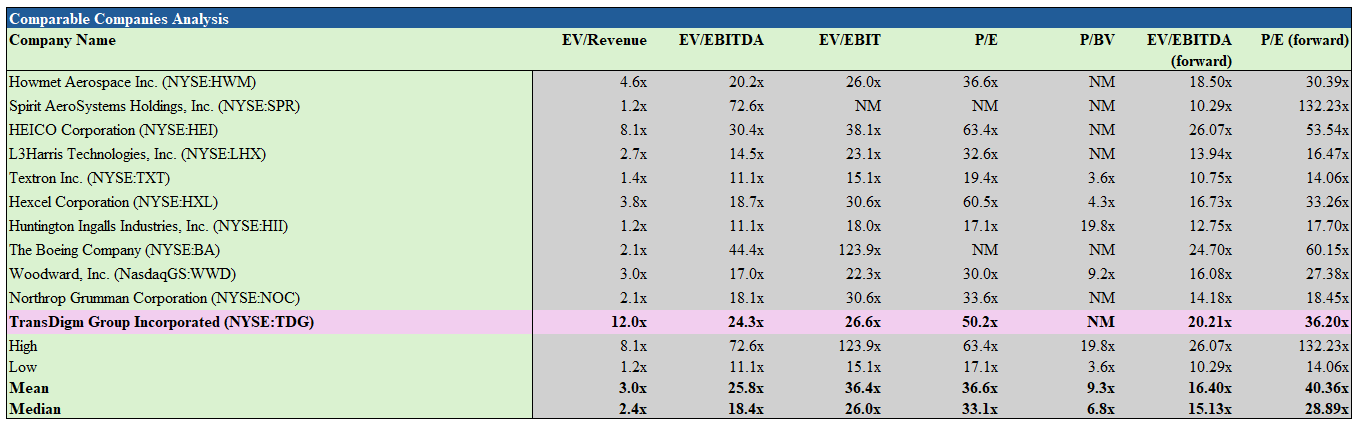

Comparing TransDigm to other peers in the aerospace and defense sector, the company certainly trades well above the peer group. That said, a premium multiple seems warranted due to higher growth prospects and a more impenetrable moat due to its pricing power. While I believe a premium multiple should be applied, the current multiple seems quite high to me. Closer to the mid-point of the historical valuation range at 18.4x EBITDA, I think shares of TransDigm would represent better value. This would also provide investors with more of a margin of safety against a decelerating growth rate as the company de-levers the balance sheet over the next few years.

Author, based on data from S&P Capital IQ

There are a few risks to investing in TransDigm that investors should be aware of. We've discussed the company's debt and balance sheet, but if the company is unable to take on additional debt or is unable to find suitable targets at attractive prices, then this would be a risk to the company's growth-by-acquisition strategy. Secondly, TransDigm has been under scrutiny by regulators due to its aggressive pricing strategy. In many instances, lawmakers have questioned why the government (eg. Pentagon) has put up with regular price increases at such high margins for products that TransDigm makes. As one of the only suppliers for various parts, the company has a wide moat and can set prices, but that could change if regulators decide that enough is enough with what they see as 'aggressive price-gouging'.

No question about it. TransDigm is a high-quality business is the aerospace and defense space that has pricing power in selling critical aircraft components to commercial and defense customers. With a great track record of delivering exceptional returns to shareholders, the company has been a great allocator of capital in making strategic, tuck-in acquisitions.

Through this strategy, the company has had put up impressive numbers in both revenues and earnings, and the latest Q1 results were no different. Looking ahead, TransDigm's growth prospects remain robust, fueled by strong demand in commercial OEM, aftermarket, and defense sectors, as well as its continued focus on acquisitions and operational efficiency. However, in my view, investors should be mindful of the potential risks associated with the company's debt levels, acquisition strategy, and regulatory scrutiny.

I'm a big fan of TransDigm and what they've been able to build. But with a sky-high valuation today, I'm not comfortable buying shares at 41x free cash flow. Closer to the midpoint of the historical valuation range, at around $900 to $950 a share, I'd be much more comfortable initiating a position, as I still like the long-term prospects of the company. So while I rate the shares as a 'hold' today, I'll be eagerly waiting for a pullback to purchase shares of this high-quality company.