MicroStockHub/iStock via Getty Images

MicroStockHub/iStock via Getty Images

Teradata (NYSE:TDC) is a lesser-known bet on artificial intelligence (AI), machine learning (ML), and internet and software services infrastructure. The company has some compelling elements, but its balance sheet at this time makes it a relatively weak investment, in my opinion. I have rated the firm a Hold due to the potential upside to come if management can prove better results than historically at the advent of these new technological capabilities.

Teradata is a provider of database and analytics software, services, and technologies. It is most prominently known for its data warehousing solutions and analytical processing capabilities. It serves businesses by aiding them in consolidating data from a range of sources and analyzing it for actionable insights. This supports decision-making across various industries, and its services are designed to manage high data loads for efficient and complex analytical operations at scale.

GuruFocus

In fiscal 2023, Teradata reported high growth in its public cloud annual recurring revenue (ARR), increasing by 48% to $528 million. It emphasized its role in AI, and it mentioned how it is leveraging its data and analytics strengths during this time in technological evolution. In fiscal 2024, the firm is forecasting public cloud ARR growth between 35% and 41%, aiming to maintain a 75% return of free cash flow. By 2025, the company is on track to achieve $1 billion in Cloud ARR.

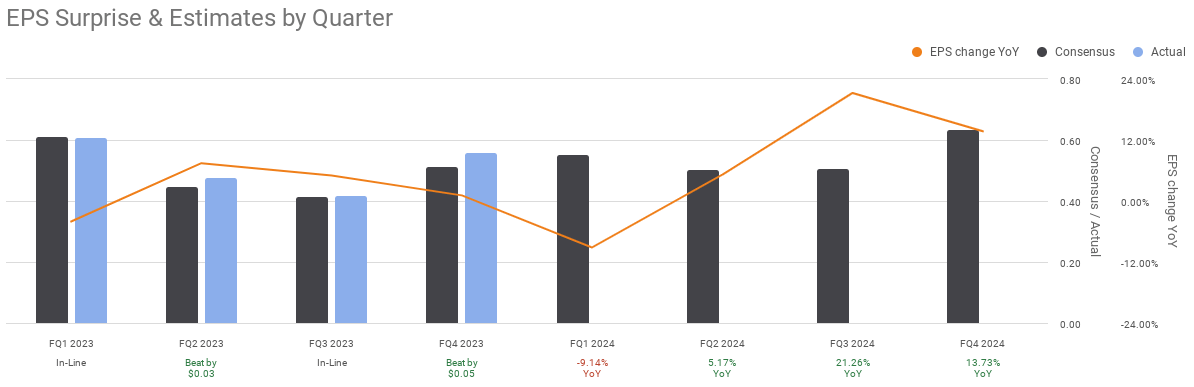

Teradata's latest quarter earnings were on 2/12/2024, and it beat GAAP estimates by $0.01, contributing to a full year of in-line and beaten consensus expectations:

Seeking Alpha

This year, through its ClearScape Analytics platform and ModelOps capabilities, Teradata is focusing on AI and ML. Specifically, it wants to simplify the AI model deployment journey, ensuring trusted AI through "no code" capabilities, advanced governance, and AI "explainability" controls.

Teradata has also introduced AI Unlimited, which is a serverless AI/ML engine in the cloud, now in private view via Microsoft (MSFT) and AWS (AMZN). The service offers higher efficiency in AI innovation by providing data engineers, data scientists, and developers with high-performance compute and in-engine analytics on demand. This makes the scope of AI larger and easier to access, helping to democratize the adoption and customization of the technology across industries.

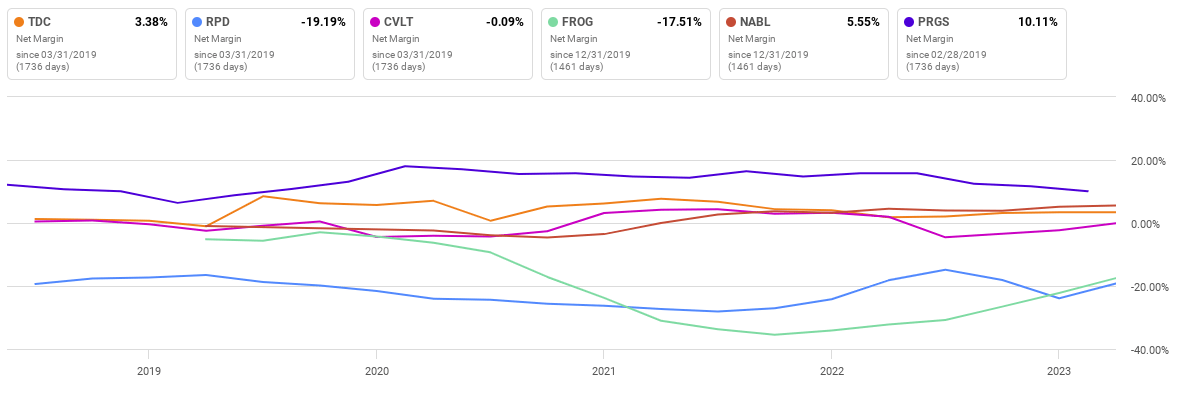

Teradata's strongest suit is its profitability, including a gross profit margin of 60.88%, a 24.4% difference from the sector median of 48.94%. Additionally, its net income margin of 3.38% is a 34.04% difference from the sector median of 2.52%.

Seeking Alpha

Its growth is also strong, but slightly less so than its profitability, with forward EPS GAAP growth of 73.41%, a 1,001.42% difference from the sector median of 6.67%, but forward revenue growth of just 2.58%, which is a -61.77% difference from the sector median of 6.74%.

As my focus is primarily on the technology sector as an analyst, I am well aware of the growing long-term CAGR expectations surrounding the AI and machine/deep learning markets at this time. For example, Bloomberg Intelligence estimated a 42% generative AI market CAGR over the next 10 years in June 2023. It put an estimate of $1.3 trillion for the market by 2032.

Teradata seems well-equipped to capitalize on this growth, but I would argue that it likely isn't one of the strongest companies to invest in for exposure to AI and ML, primarily as a result of a notably weak balance sheet.

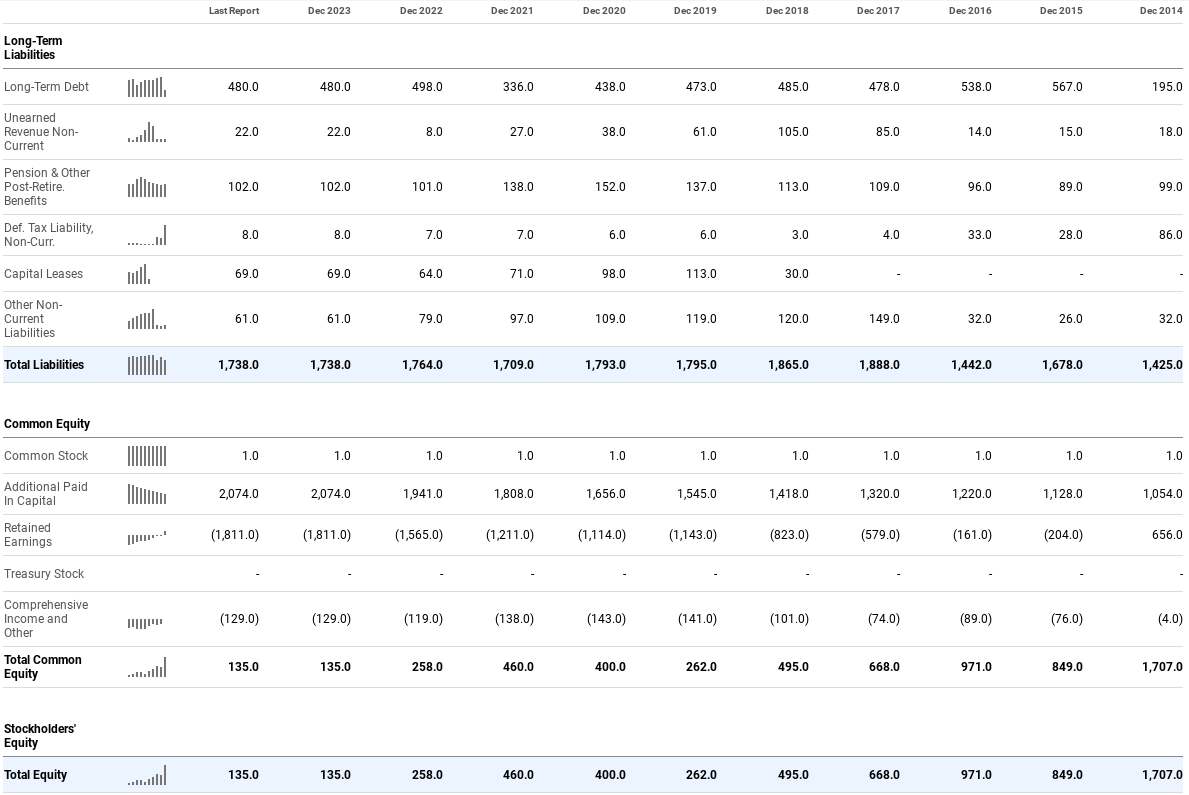

Teradata has a weak balance sheet at this time, with an equity-to-asset ratio of 0.07 and a debt-to-equity ratio of 4.74. Compare this to JFrog (FROG), which has an equity-to-asset ratio of 0.7 and a debt-to-equity ratio of just 0.03. Additionally, compare it to N-able (NABL), which has an equity-to-asset ratio of 0.61 and a debt-to-equity ratio of 0.53.

Seeking Alpha

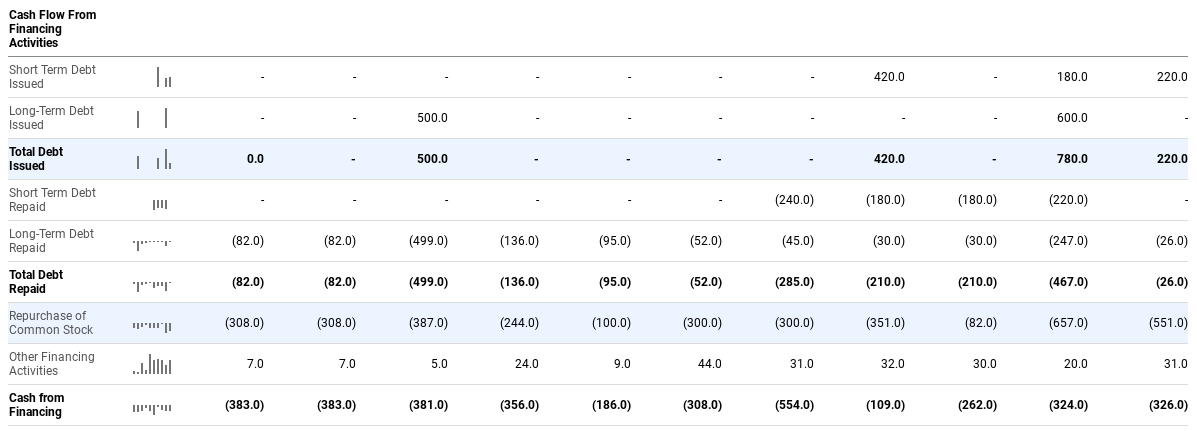

However, Teradata has not issued debt frequently over the past decade, although when it has, it has done so at a high volume. Additionally, it has not issued any common stock and has positively repurchased common stock every year since 2014, bolstering shareholder value over the long term. I would argue that it may be wiser at this stage for the firm to begin to repay its debt rigorously, and to hold off on repurchases of common stock at this time to aid in doing so.

Seeking Alpha

Teradata has a forward P/E GAAP ratio of 32.50, which is a 14.42% difference from the sector median of 28.41. Considering that Teradata is relatively small compared to premium tech companies, a discounted cash flow analysis may work quite well in determining the intrinsic value of the firm.

To do this, I predicted a conservative 12.5% EPS without NRI growth rate for the next 10 years as an annual average, which prices in some of the unpredictability in profitability thus far but also considers long-term AI market growth outlined by firms like Bloomberg Intelligence.

I also used a 4% terminal stage EPS without NRI growth rate as an annual average for 10 years following my growth stage and an 11% discount rate. My fair value estimate came to $37.25, which indicates a -1.5% margin of safety on the $37.81 stock price at the time of this writing.

Considering potentially no margin of safety in Teradata shares at this time, I believe investors would also be wise to consider inhibitions in the AI market and machine learning growth, which could negatively impact my future 12.5% annual EPS growth rate prediction. The technology industry is going through a large shift, and regulatory restraints are likely to increase as the capabilities of AI scale.

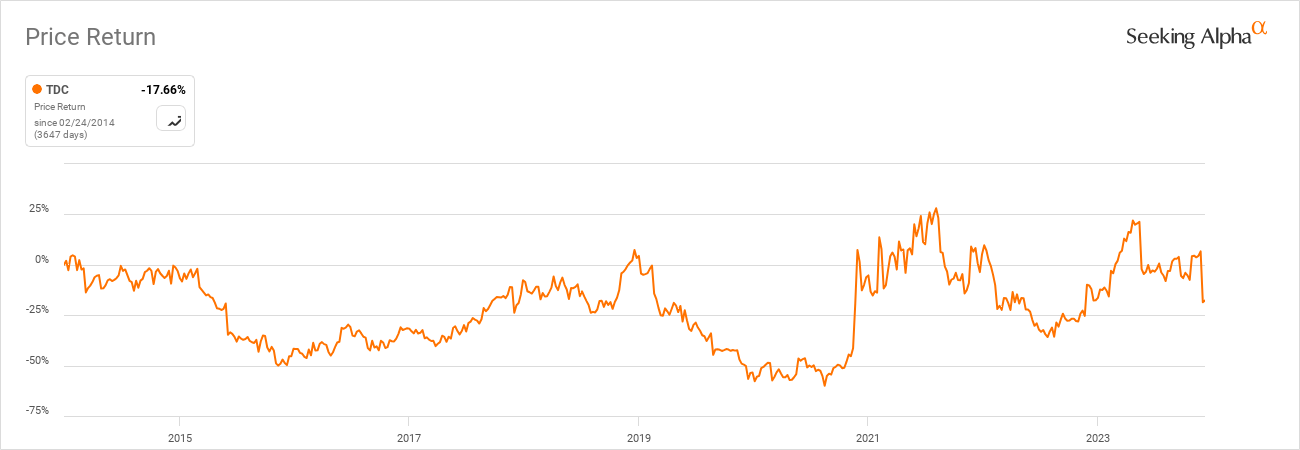

Additionally, while past returns are no guarantee of future results, they do indicate track records and traits of the company. At this time, Teradata has had a negative 17.66% price return over the past 10 years. That indicates that the firm has been unsuccessful over the long term at this time at generating stable shareholder value.

Seeking Alpha

I think Teradata could be a good investment, but the long-term risks remain high, primarily due to its balance sheet. Its exposure to AI, ML, and other advanced technology infrastructures may be compelling, but I have not seen enough evidence that the financial health of the company has been managed prudently enough historically or at this time for above-alpha returns over the next few decades. Therefore, my analyst rating for Teradata stock is a Hold.