A-Ko-N/iStock via Getty Images

A-Ko-N/iStock via Getty Images

Welcome to another installment of our BDC Market Weekly Review, where we discuss market activity in the Business Development Company ("BDC") sector from both the bottom-up - highlighting individual news and events - as well as the top-down - providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the second week of March.

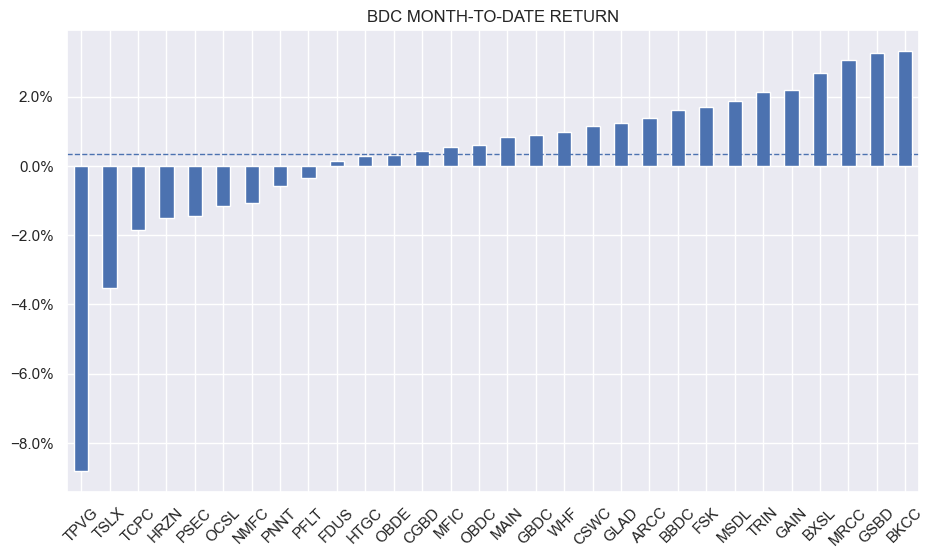

BDC returns were marginally positive as most companies finished in the green. A handful of BDCs, including the dire return from TPVG managed to pull the average weekly return quite a bit lower. Month-to-date the sector is fairly flat.

Systematic Income

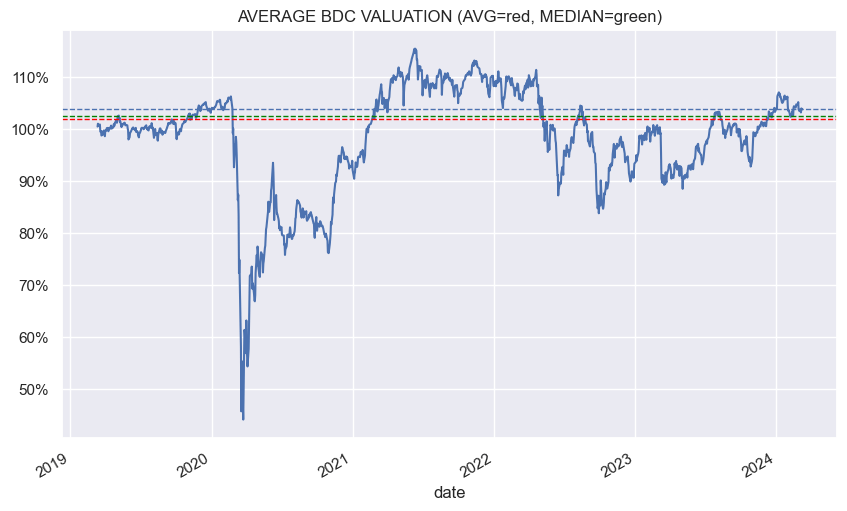

Aggregate valuations remain at the upper end of their range over the last year.

Systematic Income

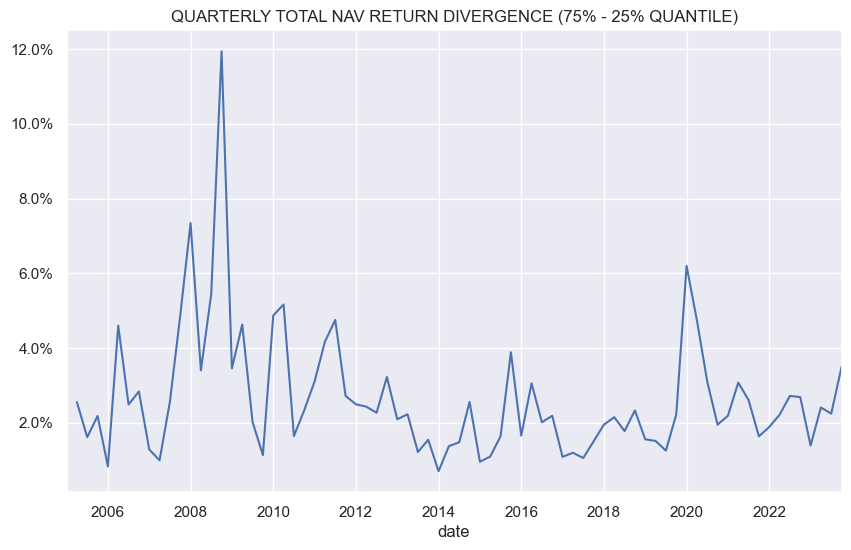

Now with the Q4 reporting period behind us, one clear theme is the divergence in total NAV performance. The chart below plots the divergence in the quarterly BDC total NAV returns. From a technical standpoint, this is measured by the difference in performance quantiles, specifically the 75th and 25th quantiles. Rather than looking at the difference between the highest and lowest quarterly returns which can be affected by unusual outliers, it looks at the difference in total NAV returns between BDCs three-quarters towards the top and a quarter from the bottom.

Systematic Income

What we see is that sector performance tends to diverge during difficult market periods such as the GFC in 2008, the Energy crash in 2015, the COVID crash in 2020, and most recently. What's interesting about this latest increase in performance divergence is that, unlike the previous instances, it is happening in a bull market.

However, what's very clear is that while the market is very much risk-on, BDC performance divergence tells us that there is quite a bit of stress underneath. That level is not yet at previous peaks (though it's not far off the Energy crash level), but it has increased.

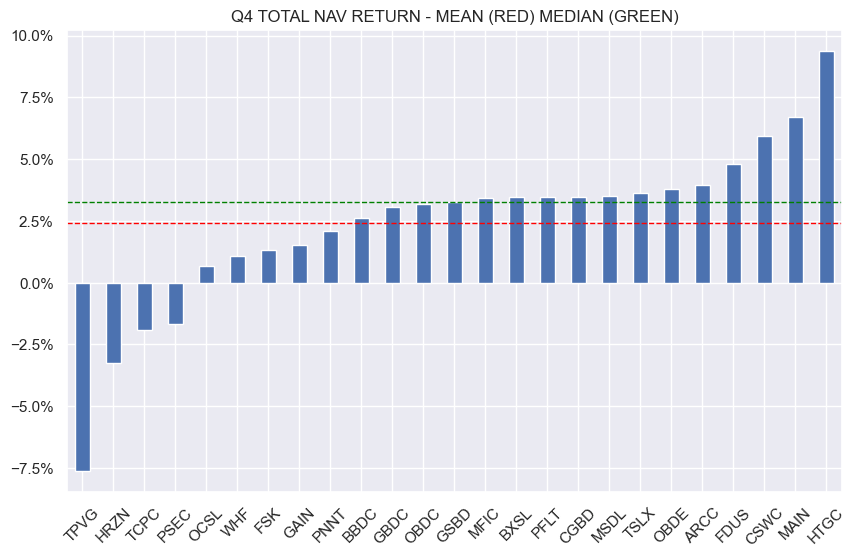

A look at the chart of Q4 total NAV returns shows that 4 BDCs in our coverage have registered a drop (8 have registered a drop in the NAV itself, adjusted for unusual special dividends). Three BDCs have seen a drop in the NAV itself of more than 5%.

Systematic Income

What is clearly happening is that high short-term rates are creating stress for borrowers, however, this stress is felt differently across the BDC sector. Some portfolios are handling it well while others are clearly not. Since the market does not expect the Fed to slash rates swiftly, stress across the borrower space will remain and perhaps worsen, particularly if the economy continues to slow. And because BDC portfolios tend to exhibit serial correlations (underperformers tend to underperform and vice-versa), the stress is likely to be more prevalent across BDCs that are already struggling.

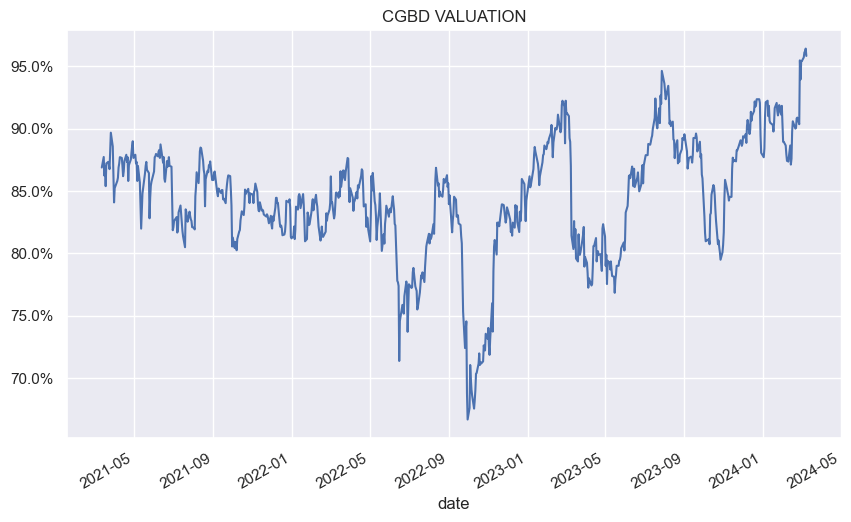

Carlyle Secured Lending (CGBD) had a good quarter. The base dividend was hiked by over 8% and the supplemental was increased by a penny. The 3.5% total NAV return for the quarter was slightly above the average. Non-accruals remained stable and above the sector average.

The valuation is close to its highest level in both absolute and relative terms, at 6% below the median level. Over the last year, the stock slightly underperformed the sector in total NAV terms (but outperformed over the last 3 years). Perhaps more importantly. it outperformed the sector in price terms which was due to the expected valuation compression. Further valuation compression will probably be hard going. CGBD remains in the High Income Portfolio.

Systematic Income

Shareholders of TCP Capital Corp (TCPC) and BlackRock Capital Investment Corp. (BKCC) have approved the merger and BKCC will become a wholly owned subsidiary of TCPC. Recall that there has been a trend of merging poor BDCs - a kind of rebranding a la ValuJet / AirTran (when ValuJet adopted the name of its smaller subsidiary AirTran after a ValuJet crash in the Everglades). FCRD - another train wreck of a BDC - was similarly acquired by CCAP earlier. From a practical standpoint, this opens up some space in our BDC Tool. So far we have added two new BDCs - Blue Owl Capital Corp. III (OBDE) and Morgan Stanley Direct Lending Fund (MSDL) were added. We will be doing more analysis on these new entrants soon.

The divergence in NAV performance that we saw in Q4 is likely to continue over the next couple of quarters even if the Fed starts to cut rates. In our BDC allocation, we have been tilting to higher-quality names with a history of strong portfolio performance and this has worked well. In our High Income Portfolio which has the largest BDC allocation, only 1 out of our 7 BDC holdings has registered an NAV drop over Q4 while, in terms of actual holdings, only 1% out of the 15% BDC sleeve had an NAV drop. A higher-quality tilt with an eye to valuations should continue to be a winning strategy in the sector over the medium term.