da-kuk

da-kuk

TaskUs, Inc. (NASDAQ:TASK) could receive significant business growth thanks to its exposure to markets related to digital experiences, and AI services. I would also expect significant innovation, and know-how generation thanks to partnerships with other actors in the AI industry like Quavo. Besides, I would expect certain financial flexibility, and FCF margin growth coming from recent restructuring efforts, and sales of assets. There are clear risks linked to revenue dependence or contractual risks; however, I think that TASK appears quite undervalued at its current valuation.

TaskUs excels in delivering next-generation customer experiences to the world's most innovative companies. Their focus encompasses representing, protecting and growing his clients' brands.

Source: Company's Website

They offer solutions to meet urgent needs of end customers, manage compliance complexities, moderate online content, and employ artificial intelligence technology for automation.

With over 150 clients across diverse sectors such as e-commerce, FinTech, food delivery and technology, in my view, the company shows versatility and ability to address established and emerging industry segments.

TaskUs bases its business model on three key pillars: digital customer experience, trust and security, and artificial intelligence services. In digital customer experience, it stands out for its focus on digital channels and omnichannel services supported by cloud technology. Trust and security focuses on content moderation and risk management, ensuring safe environments for user interaction.

Regarding artificial intelligence services, which include data annotation to power advanced applications. TaskUs manages detailed agreements, tailored to the needs of corporate clients and startups, including billing conditions, assigned personnel and contractual terms.

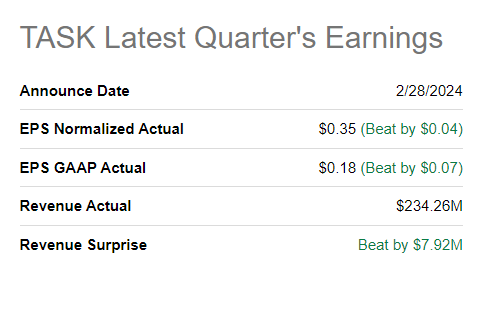

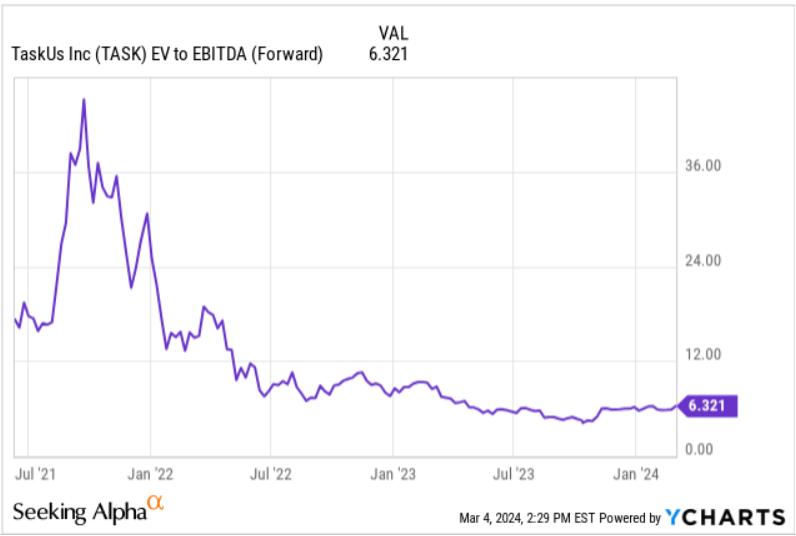

There are two great reasons to revise the company's financials right now. First, TaskUs noted EPS GAAP Actual of $0.18, which was better than expected. In addition, quarterly revenue stood at about $234 million, $7.9 million more than expected. With these figures, the current Ev/EBITDA, and previous trading multiples are another great reason to revise the stock. A few years ago, the company traded at close to 36x EBITDA. Right now, it trades at about 6x EBITDA.

Source: Seeking Alpha Source: YCharts

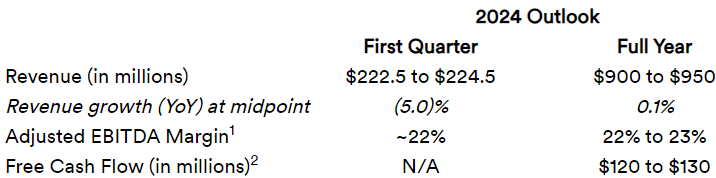

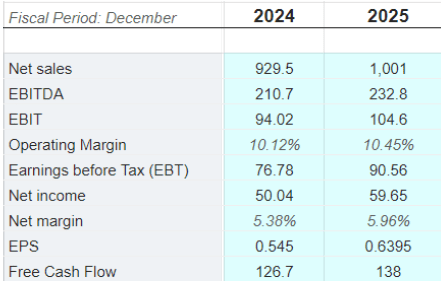

The outlook for 2024 included both net sales growth, Adjusted EBITDA margin of about 22%-23% and FCF close to $120-$130 million. Currently trading with an enterprise value that is not far from $1.3 billion, TaskUs' Ev/FCF is not far from 10x 2024 FCF. If we look at the figures of competitors, the current valuation appears to be cheap.

Source: Quarterly Report

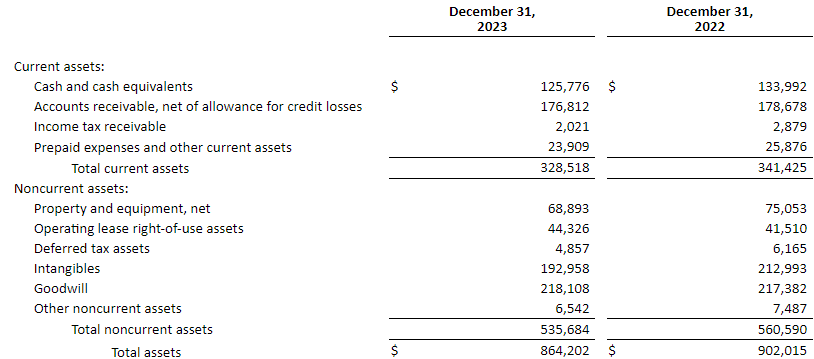

TaskUs' balance sheet appears quite solid with a significant amount of cash, and some accounts receivable. The company finances its operations with some debt, money due to providers, employees, which seems quite ideal. It means that many people out there believe in the company's business model.

The largest assets reported are the following. As of December 31, 2023, the company noted cash and cash equivalents of about $125 million, with accounts receivable worth $176 million, and total current assets $328 million. The current ratio is larger than 3x, so I am not concerned about the liquidity issues. Besides, intangibles close to $192 million, and goodwill of about $218 million, are also a large part of the total amount of assets.

Source: Quarterly Report

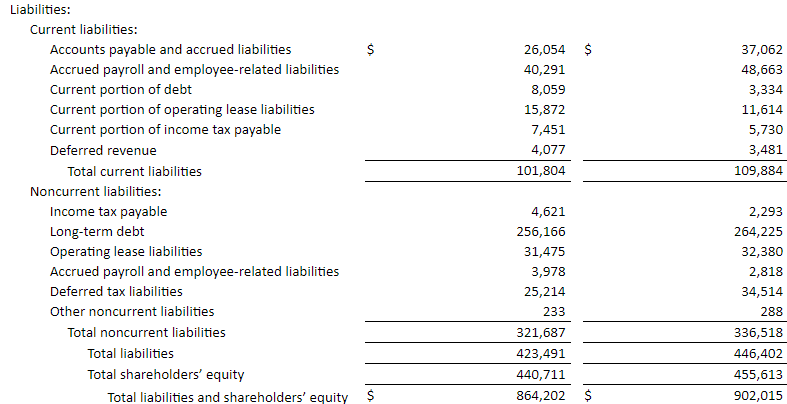

I am not concerned about the total amount of debt because the debt/EBITDA appears to be under 2x. It is also worth noting that the total amount of debt creased in 2023. The most remarkable liabilities are accounts payable and accrued liabilities worth $26 million, accrued payroll and employee-related liabilities of close to $40 million, long-term debt of close to $256 million, and operating lease liabilities worth $31 million. With total liabilities of about $423 million, the implied asset/liability ratio is larger than 2x.

Source: Quarterly Report

TaskUs' business strategy focuses on continued growth through various opportunities. First, I believe that they could grow thanks to existing customers, capitalizing on the growth and complexity of their needs through investments in strategic account management. In addition, I believe that new products like TaskGPT, which was recently launched, may also serve as net revenue catalysts.

In addition, TaskUs appears to be connecting with many other companies like Quavo, and many other competitors. I think that synergies from these partnerships, and know-how acquired from joined projects could also represent net sales catalysts. For more information about the agreement with Quavo, which was signed in March, 2024, there is substantial information in the press release noted below. I cannot say whether the market did have a look at all the details about their automated dispute management solutions.

TaskUs, Inc. announced a formal partnership today with Quavo, the industry-leading provider of automated dispute management solutions for issuing financial institutions. Source: Press Release

TaskUs is investing in Large Language Models, and Generative AI technologies. According to market experts, the global large language model market could grow at close to 35.9% from 2024 to 2030. Under my best-case scenario, TaskUs would enjoy net sales growth driven by growth in these markets.

TaskUs could also receive significant business growth thanks to applications of artificial intelligence in the trust, risk and security management market. According to Allied Market Research, this market could enjoy business growth close to 16.2%. Under my best-case scenario, I included net sales growth close to the growth of these markets.

AI trust, Risk and Security Management Market to reach $7.4 Billion, Globally, by 2032 at 16.2% CAGR. Source: Allied Market Research

Given the recent growth in companies outside the United States, and India, I believe that internationalization could bring significant net sales growth. Considering that these technologies appear to be successful in some jurisdictions like the United States, or the Philippines, I would expect the same results in Europe, South America, or the rest of Asia. As a result, we may see net sales growth driven by economies of scale.

As of December 31, 2023, TaskUs had a worldwide headcount of approximately 48,200 people across 28 locations in 12 countries. Source: Quarterly Report

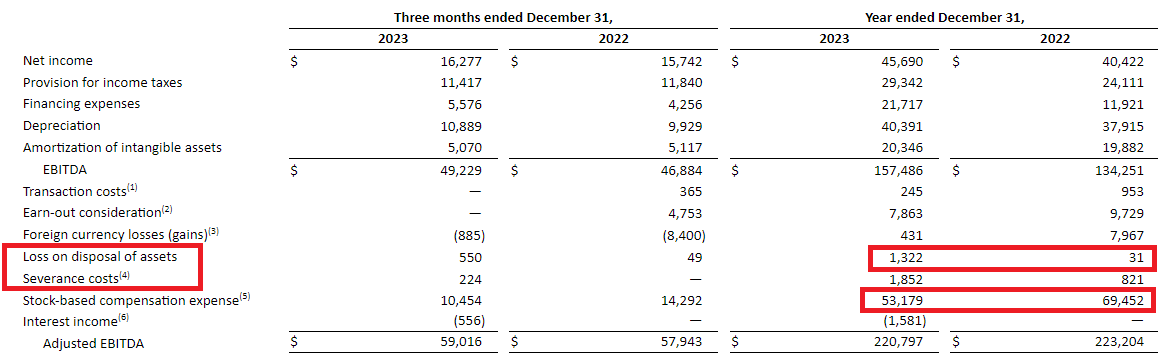

In the last quarter, TaskUs noted significant disposal of assets, and severance costs, which I believe could bring not only cash in hand. In my view, we may see significant financial flexibility coming from severance efforts. As a result, we may see EBITDA margin, and FCF margin increases in the coming years.

Source: Quarterly Report

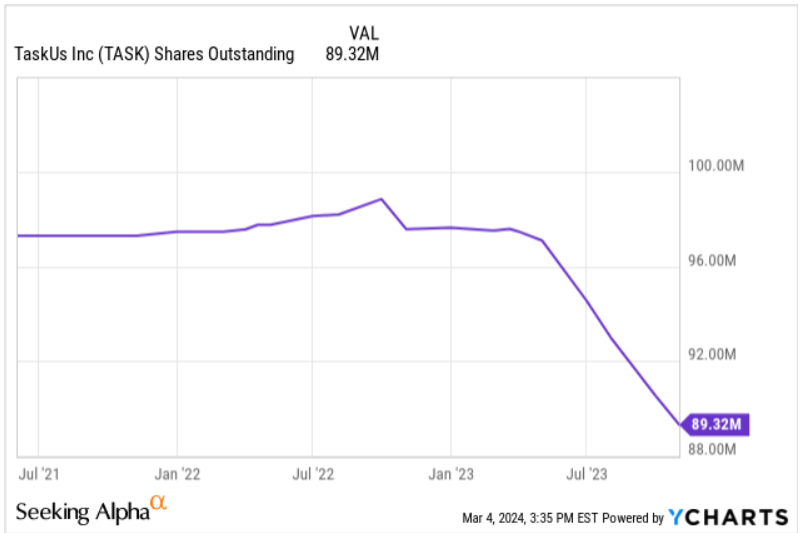

In 2023, TaskUs repurchased a significant amount of shares, which I believe may bring demand for the stock. In my view, as soon as other investors have a look at the amount of shares acquired, they may buy too.

Repurchased 2.0 million shares in the fourth quarter and 10.1 million for the full year ending December 31, 2023. Source: Quarterly Report

It is also worth noting that the share count will decline quite a bit in 2023. As a result, I believe that the implied fair price may increase leading to increases in the market price.

Source: YCharts

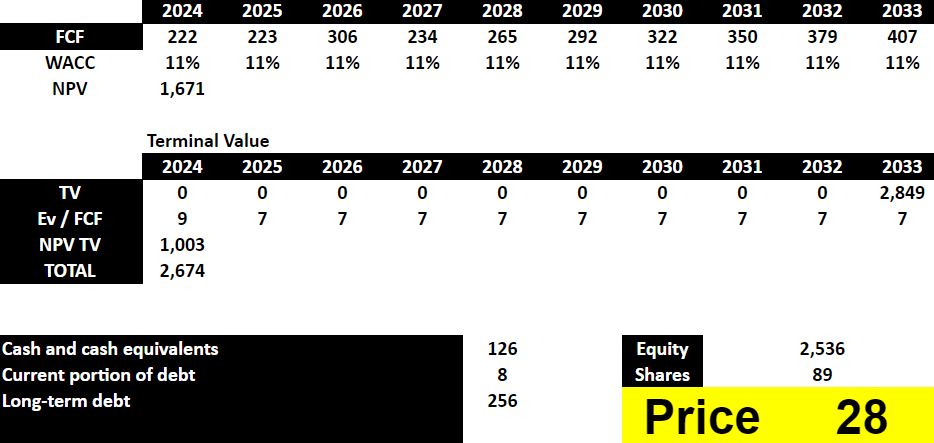

Under my base case scenario, I included 2033 net sales of close to $1350 million, with 2033 net income of close to $151 million. Given the growth expected for the target markets, and revisions of other analysts, I believe that my numbers are conservative. The following are figures from other investors.

Source: Market Screener

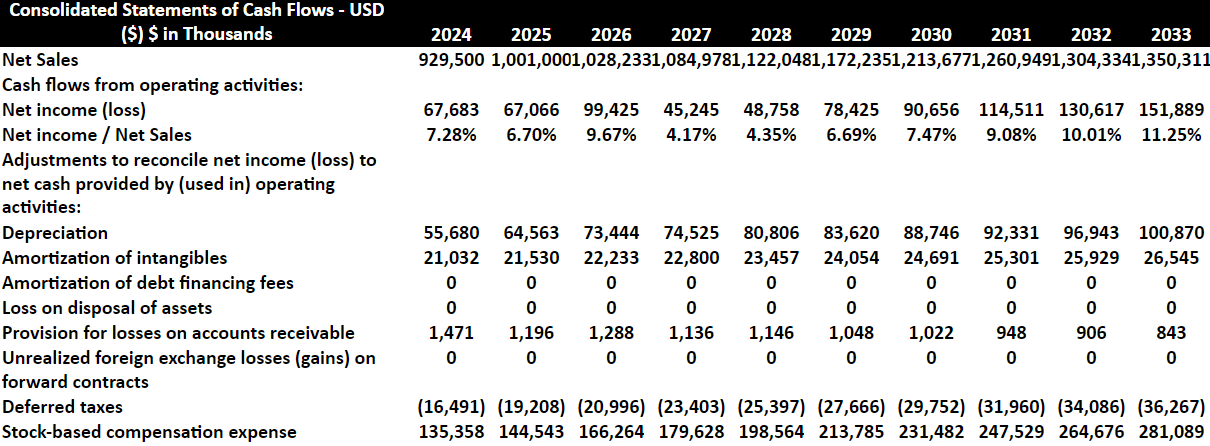

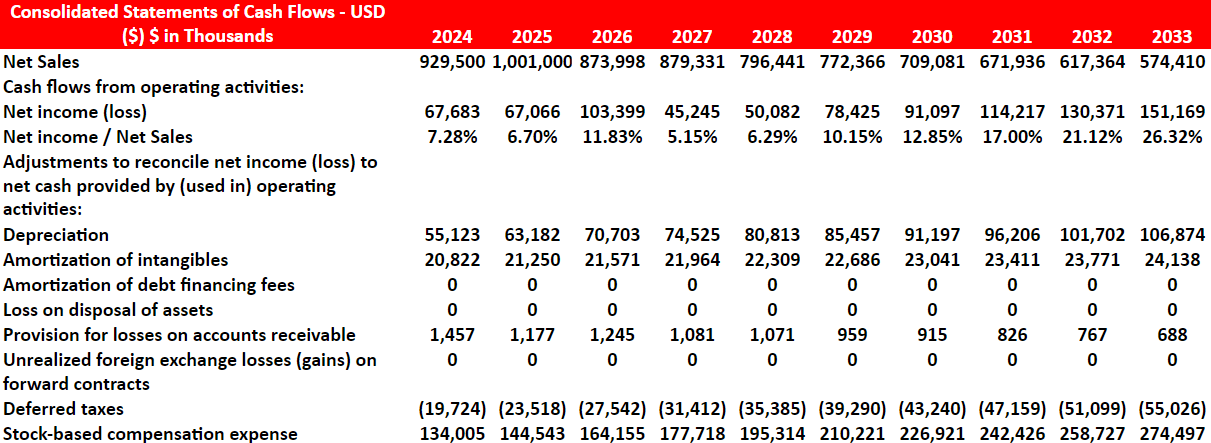

I also included the following adjustments to reconcile net income. First, I assumed 2033 depreciation of about $100 million, with amortization of intangibles close to $26 million, deferred taxes worth -$37 million, and stock-based compensation expense worth $281 million.

Source: My Expectations

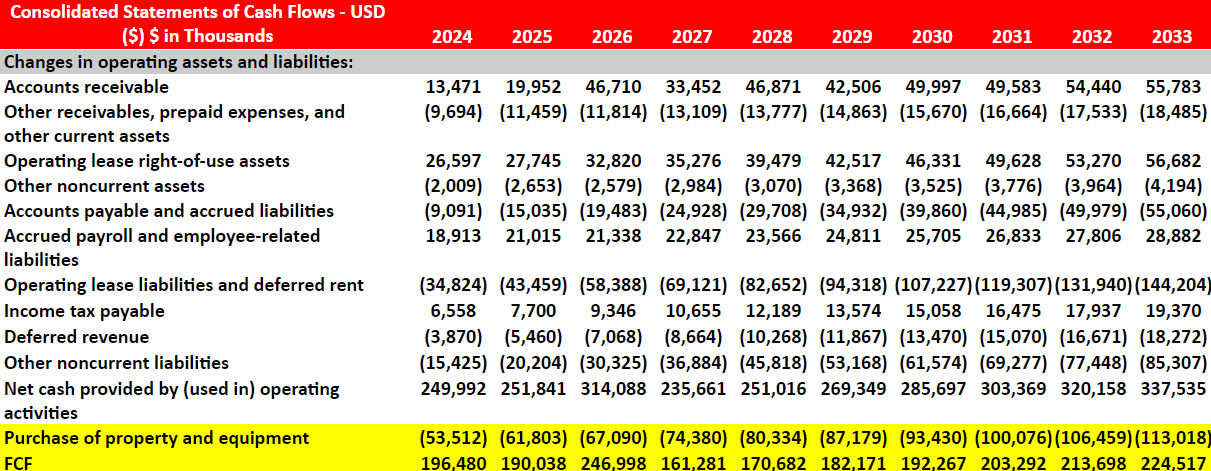

In addition, I assumed the following changes in operating assets and liabilities. First, I included 2033 changes in accounts receivable of $54 million, with other receivables, prepaid expenses, and other current assets of about -$20 million, and operating lease right-of-use assets worth $65 million.

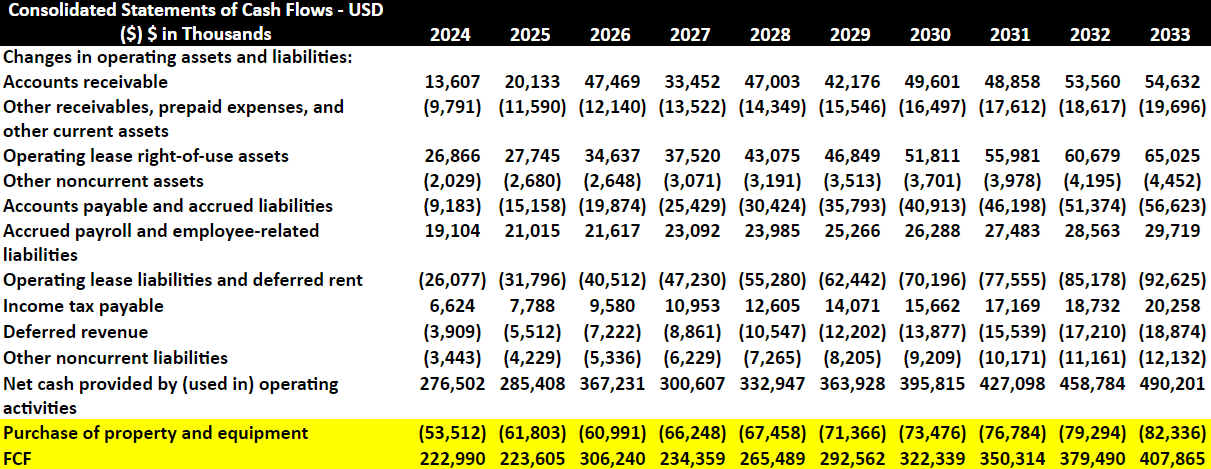

In addition, with changes in accounts payable and accrued liabilities of close to -$57 million, accrued payroll and employee-related liabilities worth $29 million, and operating lease liabilities and deferred rent worth -$93 million, I assumed changes in income tax payable of about $20 million.

Finally, taking into account 2033 deferred revenue of about -$19 million, 2033 net cash provided by operating activities would be $490 million. Finally, taking into account purchase of property and equipment of -$83 million, 2033 FCF would be $407 million.

Source: My Expectations

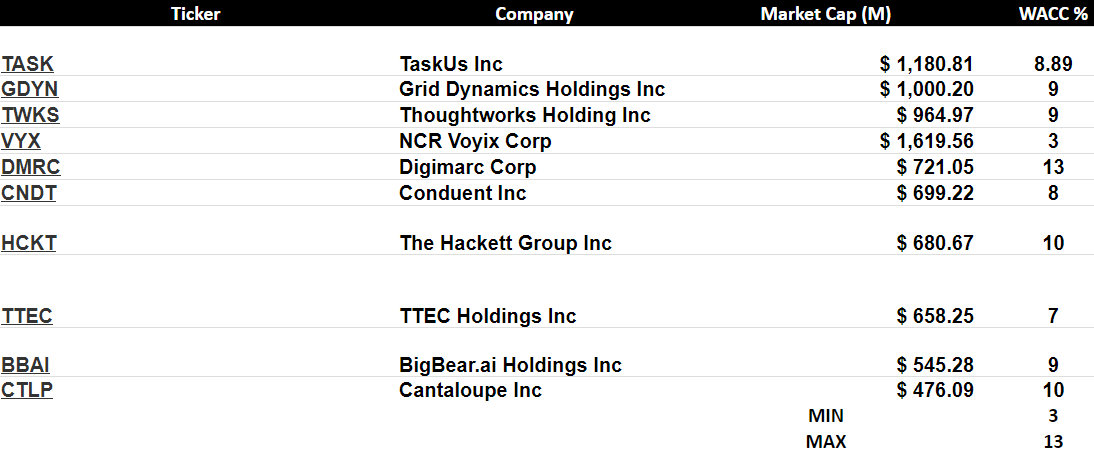

With other financial advisors reporting a WACC between 13% and 3%, I assumed a WACC close to 11%, which I believe is conservative. I also believe that in the worst-case scenario, a cost of capital close to 15% would make sense.

Source: Gurufocus

Also assuming an exit Ev/FCF of 7x, the implied enterprise value would be close to $2.6 billion. Adding cash and subtracting debt, I obtained an implied fair price of close to $28 per share.

Source: My DCF Model

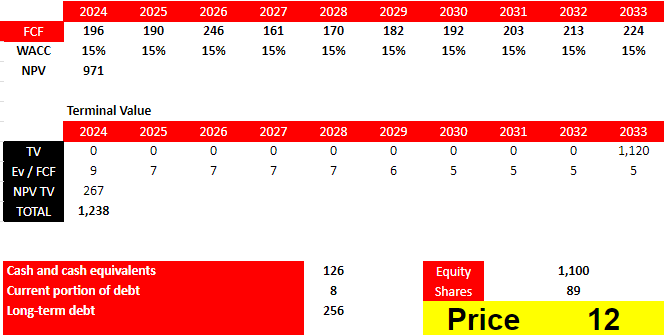

Under my bear case scenario, I assumed 2033 net sales of about $574 million, and 2033 net income close to $151 million. Note that I took into account a decline in net sales, and a certain increase in the profit margin. I believe that the financial figures obtained in this case scenario are quite unlikely.

I also included the following adjustments to reconcile net income to CFO. With 2033 depreciation of about $106 million, amortization of intangibles worth $24 million, I used 2033 stock-based compensation expense close to $274 million.

Source: My Expectations

In addition, the following changes in operating assets and liabilities were assumed. I included 2033 accounts receivable of about $55 million, with other receivables, prepaid expenses, and other current assets of about -$19 million, and operating lease right-of-use assets of close to $56 million.

Besides, accounts payable and accrued liabilities worth -$56 million, and operating lease liabilities and deferred rent -$145 million, imply net cash provided by operating activities of about $337 million. Finally, with purchase of property and equipment worth -$114 million, 2033 FCF would be of about $224 million.

Source: My Expectations

With a WACC of 15%, and Ev/FCF of 5x the implied equity valuation would be of about $1.1 billion. Besides, the implied fair price would not be far from $12 per share.

Source: My DCF Model

According to the last 10-k, TaskUs faces significant risks as it is heavily dependent on a few key customers. Loss of business with key customers could adversely impact financial results. There is a risk of substantial claims for defects, errors or breaches of contract, and contractual limitations may not fully protect against liability.

In addition, failure to meet time commitments, service levels and performance requirements could damage reputation and result in lost revenue. In general, lack of contractual compliance or the perception of noncompliance poses significant threats to TaskUs.

In my opinion, the company faces a large and challenging market, TaskUs faces competition from various business service providers. Its main competitors include established and emerging companies in the outsourcing sector, each seeking to stand out in business culture, innovation, and quality of services.

In my view, the company needs to continue differentiating itself through its omnichannel approach, scalability, and solid experience with leading companies in various industries. I believe that the continued emphasis on adaptability and quality allows it to stand out in a dynamic and competitive market.

TaskUs' focus on digital experiences, trust and AI services will most likely drive revenue stream thanks to business growth in these markets. In my view, the geographic expansion strategy and constant innovation thanks to partnerships like that with Quavo could bring net sales growth. Besides, recent restructuring efforts, and sales of assets could also bring cash in hand, financial flexibility, and FCF margin growth. In addition, also taking into account the stock repurchases, and the decline in the share count, TaskUs looks like a buy. There are clear challenges linked to revenue dependence and contractual risks, and adaptability in a competitive environment. With that, I believe that TaskUs appears undervalued at the current market price.