Results: TaskUs, Inc. Exceeded Expectations And The Consensus Has Updated Its Estimates

It's been a good week for TaskUs, Inc. (NASDAQ:TASK) shareholders, because the company has just released its latest yearly results, and the shares gained 7.7% to US$13.21. Revenues were US$924m, approximately in line with expectations, although statutory earnings per share (EPS) performed substantially better. EPS of US$0.48 were also better than expected, beating analyst predictions by 15%. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

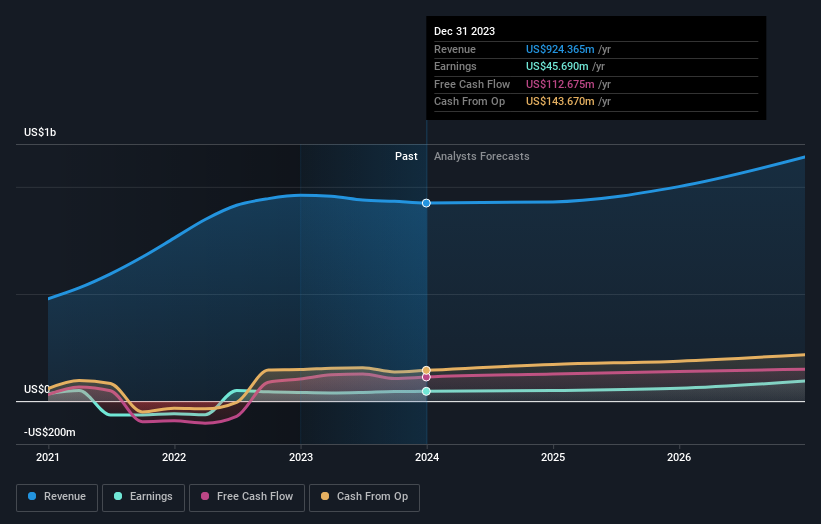

See our latest analysis for TaskUs

Following last week's earnings report, TaskUs' seven analysts are forecasting 2024 revenues to be US$929.5m, approximately in line with the last 12 months. Statutory earnings per share are predicted to rise 6.5% to US$0.55. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$914.5m and earnings per share (EPS) of US$0.57 in 2024. So it looks like there's been a small decline in overall sentiment after the recent results - there's been no major change to revenue estimates, but the analysts did make a minor downgrade to their earnings per share forecasts.

The consensus price target held steady at US$14.71, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic TaskUs analyst has a price target of US$18.00 per share, while the most pessimistic values it at US$12.00. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. It's pretty clear that there is an expectation that TaskUs' revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 0.6% growth on an annualised basis. This is compared to a historical growth rate of 22% over the past five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 6.4% per year. Factoring in the forecast slowdown in growth, it seems obvious that TaskUs is also expected to grow slower than other industry participants.