Icon Sportswire/Icon Sportswire via Getty Images

Icon Sportswire/Icon Sportswire via Getty Images![]()

While it's not the largest player in the alcoholic beverage space, Molson Coors Beverage Company (NYSE:TAP) is a true giant in that market. The firm has a market capitalization of $13.39 billion as of this writing, and it owns a wide variety of leading brands such as Coors Light, Miller Lite, Molson Canadian, Miller High Life, Vizzy Hard Seltzer, and more. Even with such a star-studded portfolio of brands under its belt, the firm faces stiff competition from other players in the space. That is why it is imperative for investors to continue to monitor financial results when they become available. How the company performs from quarter-to-quarter paints the picture, as time goes, of how well it is stacking up against expectations.

When looking at the most recent quarter, which is the final quarter of the 2023 fiscal year that management just reported on February 13th, the company achieved mixed performance. Revenue came in higher than expectations. Adjusted earnings did as well. But GAAP earnings fell short of forecasts.

Ignoring analysts' expectations for a moment, the overall trend for the business seems to be positive. Revenue is growing, and cash flows are mostly following suit. In addition to this, shares of the enterprise are trading discounted relative to similar big players. All of these factors, combined, make me believe that this is a solid 'buy' candidate at this time.

Before we get into the fundamental results announced on February 13th, it might be helpful to dig a bit into the overall operations of Molson Coors Beverage Company. As I mentioned already, the company operates largely as an alcoholic beverage business. Its earliest predecessor, Molson, dates back to 1786, making it one of the oldest companies in the Western world still in existence.

From its humble origins, the business grew to be an international player in the beverage market. But it should not be surprising for investors to know that the largest chunk of its business comes from North America. In fact, according to management, the company is the oldest beer company and the second-largest brewer by volume on the continent. In total, it claims to have a roughly 20% share of the market in this region.

The enterprise also has operations elsewhere. These international operations are conducted through its EMEA & APAC segment, which includes its primary brands, as well as licensed brands, in a wide variety of countries throughout Europe, the Middle East, Africa, and the Asia Pacific region. The company also claims to be the second-largest brewer by volume in the European countries in which it operates, with an aggregate 18% market share there.

Of course, Molson Coors Beverage Company sells more than just alcoholic beverages. Some of its non-alcoholic beverages include cannabis-infused ones that are sold in Canada through a joint venture that it has with HEXO Corp. The company also boasts agreements that allow it to brew, package, and ship products on behalf of other smaller players such as The Yuengling Company, Pabst Brewing Company, and Labatt USA Operating Co.

Author - SEC EDGAR Data

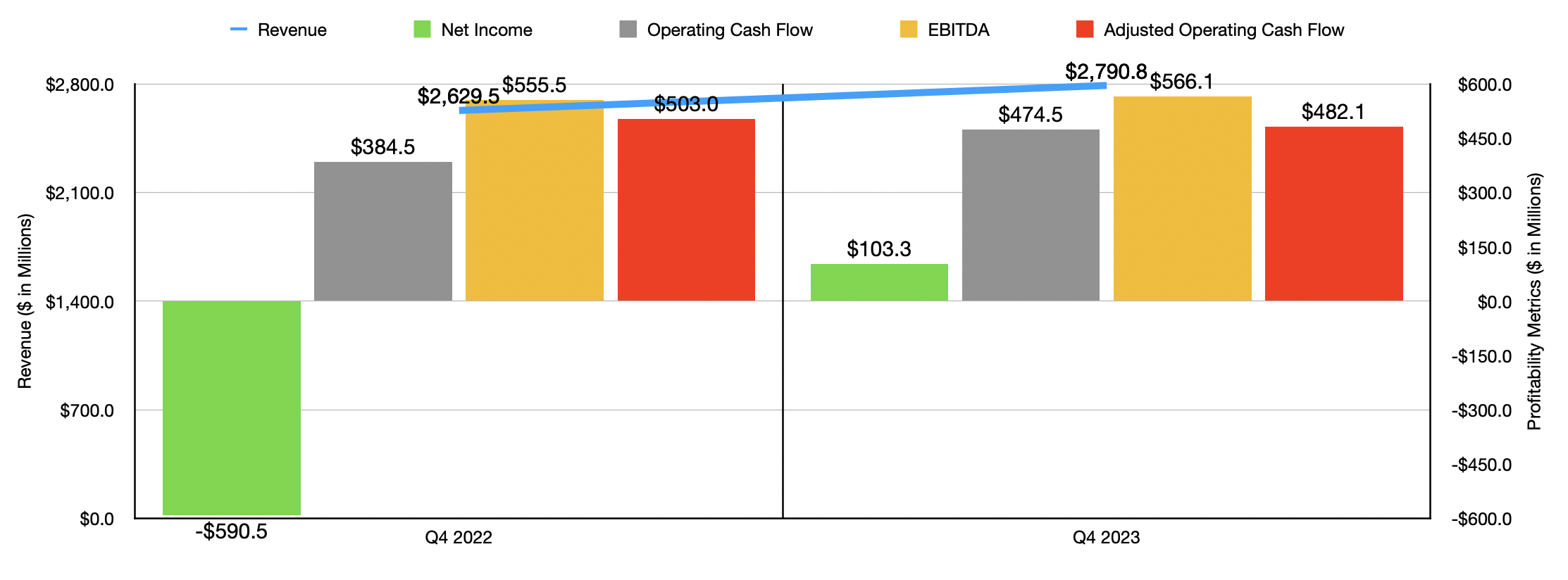

Fundamentally, the picture of the business has been looking up as of late. As an example, we need only look at data covering the final quarter of the 2023 fiscal year. Revenue for that time came in at $2.79 billion. In addition to coming in 6.1% above the $2.63 billion the business generated the same time one year earlier, it also was $10 million above what analysts forecasted for the quarter.

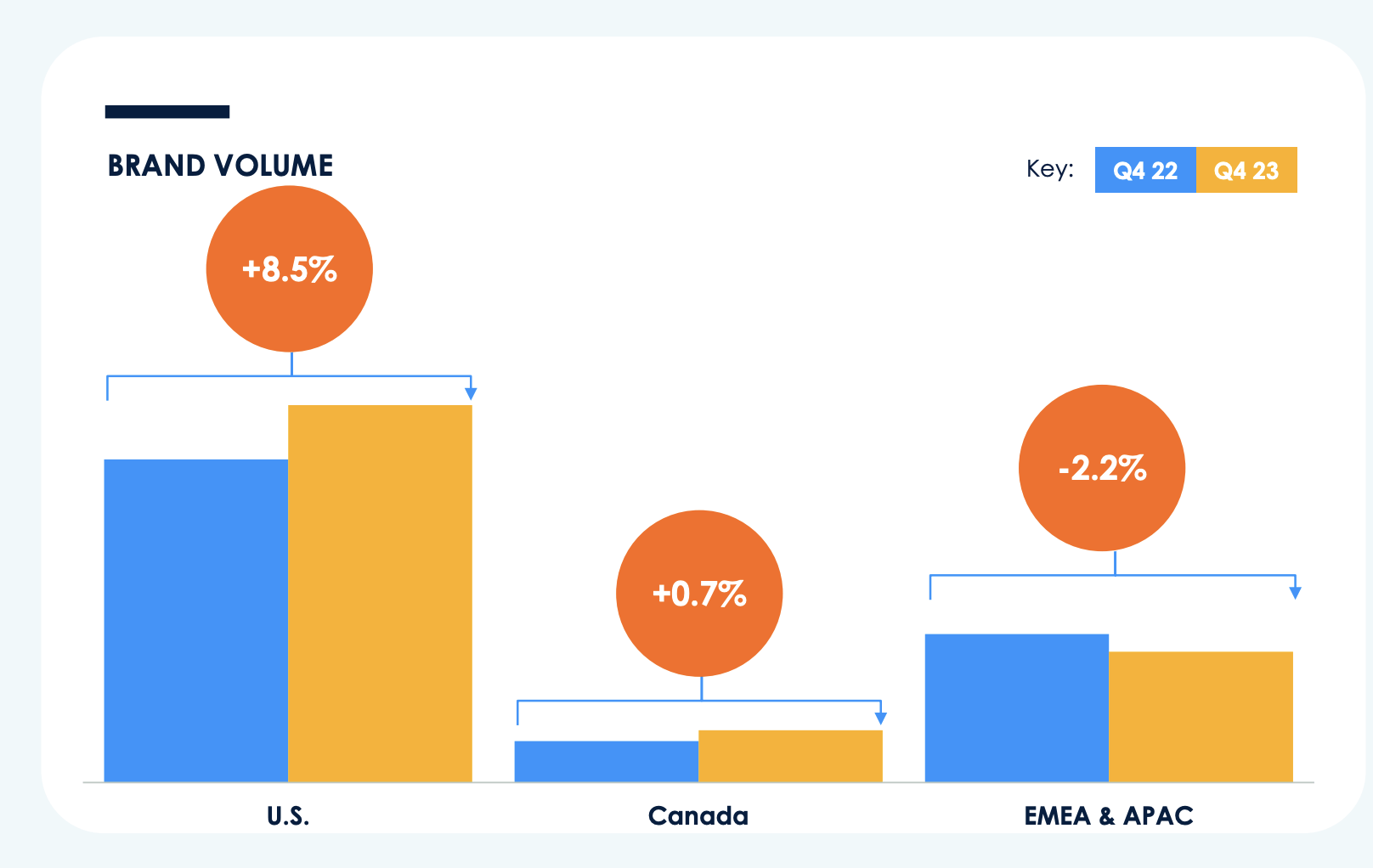

Some of the sales increase was driven by foreign currency fluctuations. Without those, revenue would have risen by about 5%. The firm's ability to raise prices and changes in product mix helped to push revenue up by 4.2% year-over-year. However, the company also benefited from slightly higher volumes shipped during the quarter. Financial brand volumes in the Americas, for instance, jumped by 4.3% year-over-year, with the Americas leading the way with a 6.7% rise. The company's core brands were responsible for pushing brand volume up by 8.5% in the U.S. market.

Molson Coors Beverage Company

Unfortunately, North America was not representative of the globe more broadly. The EMEA&APAC segment actually saw a 2.2% drop in brand volume on a year-over-year basis because of the negative impact caused by inflation in places like central and Eastern Europe. Softness in the space in the UK was also problematic. But even in North America, there was some weakness. In Latin America specifically, weak demand and overall economic conditions pushed volumes down by 5%. And even in Canada, volume was up by only 0.7%. And according to management, that was only due to strength in the premium offerings the company has.

The increase in revenue resulted in improved bottom line performance. The company went from generating a net loss of $590.5 million to generating a profit of $103.3 million. That took the earnings per share of the enterprise from negative $2.73 to positive $0.48. As great as that move was to see, earnings fell short of the $1.13 per share that analysts had forecast. But on an adjusted basis, the $1.19 per share that the company reported exceeded forecasts by $0.07 per share.

Other profitability metrics largely followed suit. Operating cash flow went from $384.5 million to $474.5 million. It is worth noting, unfortunately, that after adjusting for changes in working capital, cash flow did dip modestly from $503 million to $482.1 million. But EBITDA helped to make up for this, inching up from $555.5 million to $566.1 million.

Author - SEC EDGAR Data

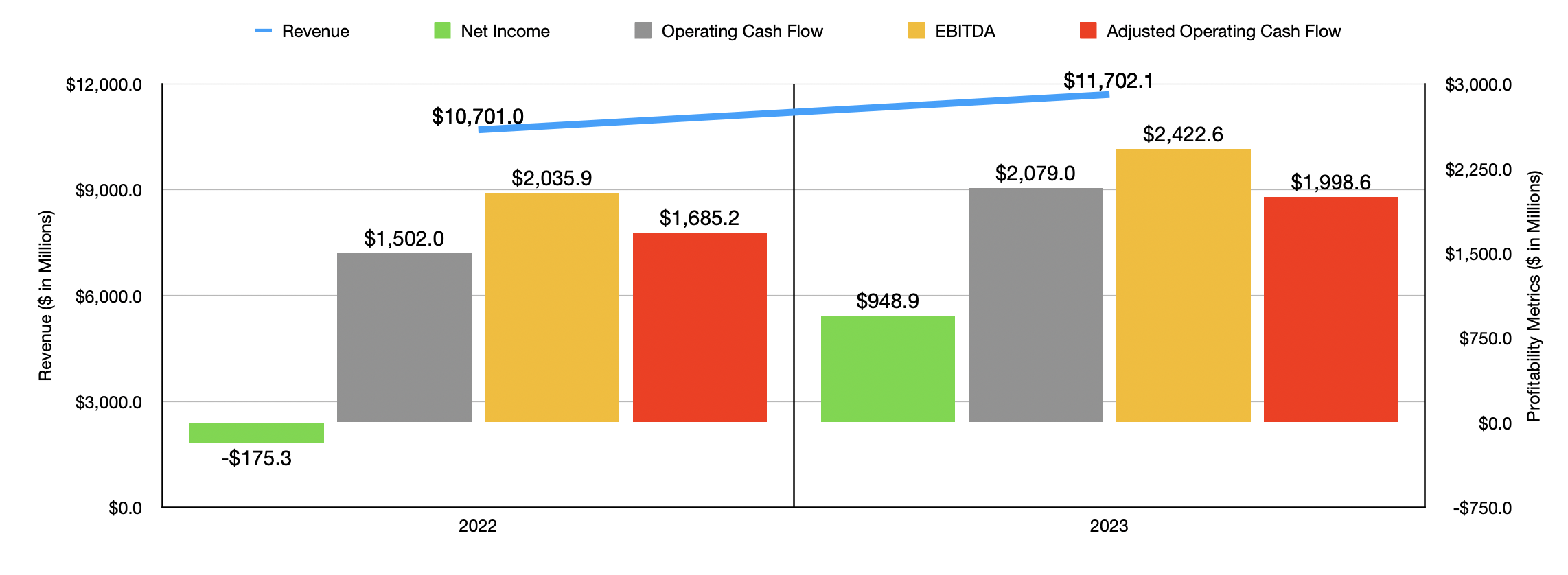

As you can see in the chart above, results for the 2023 fiscal year in their entirety were better than what they were for 2022. This was without exception. Management was clearly pleased, and they appeared bullish about the future because they made sure to reward shareholders directly. The annual dividend paid out by the company during 2023 was 8% higher than it was in 2022. The company also made sure to repurchase $205.8 million worth of shares for the year. That stacked up nicely compared to the $51.5 million worth of shares repurchased in 2022.

More likely than not, share repurchases will continue. I say this because, in October of 2023, the company announced a new, larger, repurchase program that could see the company buy up to $2 billion worth of its units over a five-year window. $150 million of the share repurchases that the company engaged in last year came from that program, with all of those purchases spread out between November and December. So if anything, the business is just getting started.

Of course, the company is not forgetting about its own financial health. Management decided to reduce net debt by $607.3 million last year. That brings total net debt down to $5.36 billion.

Molson Coors Beverage Company

When it comes to the 2024 fiscal year, management believes that revenue, on a constant currency basis, will rise at the low single-digit rate. While that's not impressive, it's better than a sales decline. Underlying earnings per share growth is being guided toward the mid-single digit range. If we assume that this would translate to a 5% year-over-year growth rate and if we ignore the prospect of share buybacks, we would be looking at net profits for the year of $996.3 million.

Taking the company's other guidance, I was able to get rough approximations for what operating cash flow and EBITDA should end up being. Based on my estimates, they should be $1.95 billion and $2.22 billion, respectively.

Author - SEC EDGAR Data

Using those results, I could then value the business as shown in the chart above. The stock actually looks fairly attractive, especially from a cash flow perspective. To follow up with this, I then created the table below. In it, you can see how shares stack up against four similar firms. What I found interesting was that units were cheaper than all four of the companies in all three different scenarios. So, in addition to being attractively priced on an absolute basis, units are attractively priced relative to other players.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Molson Coors Beverage Company | 14.1 | 6.7 | 7.8 |

| The Boston Beer Company, Inc. (SAM) | 52.6 | 21.1 | 18.5 |

| Heineken N.V. (OTCQX:HEINY) | 21.6 | 16.3 | 12.5 |

| Anheuser-Busch InBev SA/NV (BUD) | 20.4 | N/A | 15.1 |

| Constellation Brands, Inc. (STZ) | 28.8 | 16.4 | 19.8 |

At this time, all I can say is that I believe Molson Coors Beverage Company is doing a fine job. While it is disappointing to see the Q4 earnings fall short of expectations, and it would have been nice to see adjusted operating cash flow rise year-over-year, the overall picture for the company is positive. If my estimates are correct, cash flows will be slightly lower this year than they were in 2023. But given how cheap the stock is, both on an absolute basis and relative to similar enterprises, a solid "buy" rating for Molson Coors Beverage Company seems digestible.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.