Sysco (SYY) Rides on Recipe for Growth & Prudent Buyouts

Sysco Corporation SYY has been experiencing favorable outcomes from its Recipe for Growth strategy, which is strengthening its supply chain and capacity across sales. Management undertakes acquisitions to grow its distribution network and customer base and boost growth. That being said, the company is not immune to the rising cost environment.

Let’s delve deeper.

Factors Working in Sysco’s Favor

Sysco is focused on its Recipe for Growth, which includes enhancing customers’ experience via digital tools. The company is also bent on improving its supply chain to cater to customers efficiently and consistently, on the back of better delivery and omnichannel inventory management. Management is on track to improve its supply-chain performance.

Next, Sysco aims at providing customer-oriented merchandising and marketing solutions to augment sales. The company also targets team-based selling, with an emphasis on important cuisines. SYY is focused on cultivating new capacities, channels and segments, along with sponsoring investments via cost-saving initiatives.

Image Source: Zacks Investment Research

Sysco is on track with prudent buyouts to fuel growth. In the first quarter of fiscal 2024, the company closed the buyout of BIX Produce, which aids its specialty produce business (FreshPoint) to strengthen its geographical presence in unexplored areas and enhance its specialty produce offerings. In October 2023, SYY revealed that it has inked a deal to acquire Edward Don & Company, which will enhance the former’s distribution network and offerings.

Is All Rosy for Sysco?

Sysco has been encountering product cost inflation for a while now. In the second quarter of fiscal 2024, the company witnessed product cost inflation of 1.1%, measured by the estimated change in product costs, mainly in the meat and frozen categories. During the quarter, operating expenses rose 3.9% due to cost inflation and increased volumes. Apart from this, SYY’s international presence keeps it exposed to the risks of unfavorable currency translations. The persistence of these trends is a concern.

Final Thoughts

All said, Sysco has been focused on enhancing efficiency through supply-chain productivity and structural cost-containment efforts. The extensive range of product offerings, together with the proficiency of Sysco’s sales team, positions it well to achieve impressive outcomes. For fiscal 2024, management envisions sales to increase in the mid-single digits to nearly $80 billion. Adjusted earnings per share are expected to rise 5-10% to the range of $4.20-$4.40 during the same time frame.

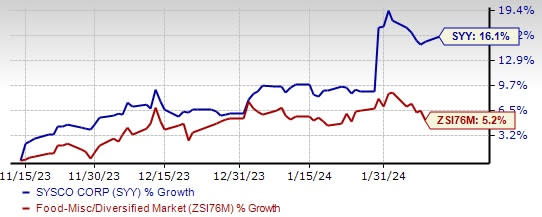

Shares of this currently Zacks Rank #3 (Hold) company have risen 16.1% in the past three months compared with the industry’s 5.2% growth.