Joe Raedle

Joe Raedle

I believe that Stanley Black & Decker (NYSE:SWK) is a hold because the company is proactively tackling its challenges through strategic initiatives aimed at innovation and operational efficiency, especially in developing cutting-edge tool technologies and implementing a comprehensive cost reduction strategy. These measures are designed to enhance its position in the fast-paced tool industry, despite the hurdles posed by economic fluctuations and supply chain disruptions. Considering the company's focused efforts towards these strategic goals and an anticipated low to no growth scenario, the current stock price of $88.94 seems slightly elevated, justifying a hold position in my portfolio. This perspective is based on a cautiously optimistic outlook, acknowledging Stanley Black & Decker's capabilities for future growth and increased profitability, even as it navigates through existing market uncertainties.

On my journey to achieving financial freedom, I often find myself spending extensive amounts of time looking into high-quality, easy-to-understand businesses that have demonstrated the power of compounding, in the hopes of establishing a robust portfolio that grows steadily for decades to come.

The strategy I have gravitated towards is dividend investing as I believe it is an excellent pathway to achieving my investing goals thanks to the mix of passive income, compounding growth and risk mitigation it offers.

One such business that has demonstrated the strong dividend characteristics that I look for historically is Stanley Black & Decker. The company is down more than 50% from its high in 2021 with the current stock price only 11.4% above the stock price from 10 years ago. Stanley Black & Decker recently reported their fourth quarter and full year 2023 earnings on February 1, which was met with a sharp selloff of roughly 7% which caught my attention and makes me believe it is a great time to analyze and discuss the company.

Stanley Black & Decker, established in 1843 and headquartered in Connecticut, is a global leader in industrial tools and equipment, serving diverse sectors with brands like Black & Decker and DEWALT. With over 100 manufacturing facilities worldwide, it's the largest tool company, employing over 60,000 people spanning across 60 countries.

In the past few years, Stanley Black & Decker has faced industry-wide challenges due to economic pressures leading to a slowdown in demand for its outdoor and DIY tools, which has led to a sharp decline in its stock price from a high of $203.86 in 2021 to $88.94 today. These conditions were influenced by rising interest rates and tighter consumer budgets. Despite these market headwinds, the company implemented strategic measures to navigate the economic downturn effectively. By adjusting prices and implementing cost control measures, Stanley Black & Decker has managed to maintain its market position and financial stability.

When analyzing a company like Stanley Black & Decker, I tend to focus particularly on its dividend and the underlying fundamentals, as this is ultimately the driving force behind dividend performance. As I have discussed, I believe dividends are an excellent way for an investor to establish steady income, but they also provide reliable insight into a company's financial health, which is perfect for myself as I am steadfast on achieving financial freedom through long-term stable dividend investing.

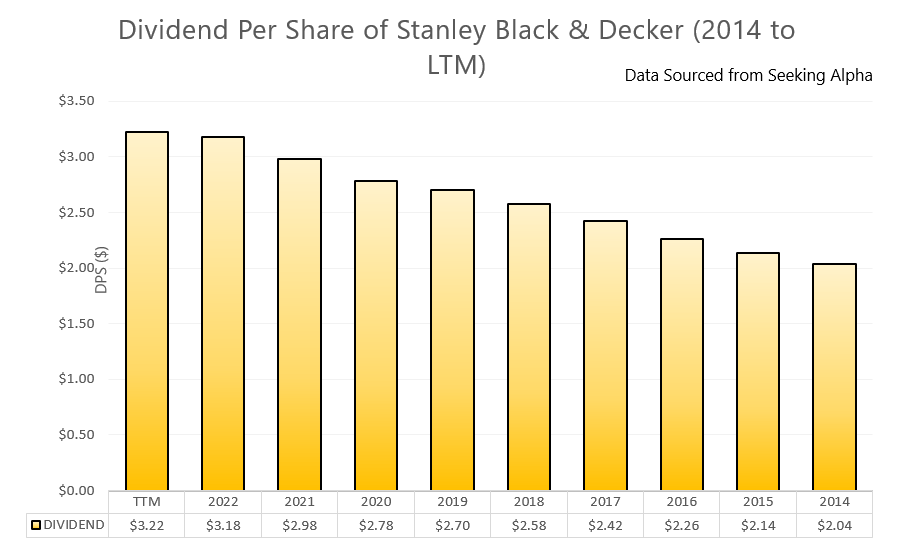

Stanley Black & Decker is a dividend king, the company has one of the most impressive dividend track records I have seen, paying a cash dividend every year for 147 years. In that period, the company has continually raised its dividend, establishing itself as one of the premier dividend providers and has a 10-year dividend compound annual growth rate (CAGR) of approximately 5.2%. Today, the dividend stands at $3.22 which equates to a solid dividend yield of 3.60% based on the current price of $88.94, which is greater than the S&P500 average dividend yield of 1.62%.

Stanley Black & Decker's dividend growth visualized (Division One Dividend)

Furthermore, Stanley Black & Decker has a concerning payout ratio of 155.4% which is an unsustainable payout ratio in my opinion and would generally lead me to believe that the company may not maintain their current dividend and are unlikely to raise and may reduce the dividend in the near future, however given the history of Stanley Black & Decker's dividend I would argue it is less likely. Nonetheless, the present payout ratio for the company is alarming and will require a return to sustainable profit growth soon if the company wants to continue to maintain its impressive dividend history. When compared to some of its biggest competitors such as Illinois Tool Works (ITW) and Deere & Co (DE), SWK's dividend presently appears to be weaker, particularly when considering the growth of each dividend over the past few years. However, despite the seemingly worse dividend in recent years, Stanley Black & Decker currently has a greater dividend yield compared to its competitors, which may make SWK an intriguing option for investors when considering these 3 machinery giants.

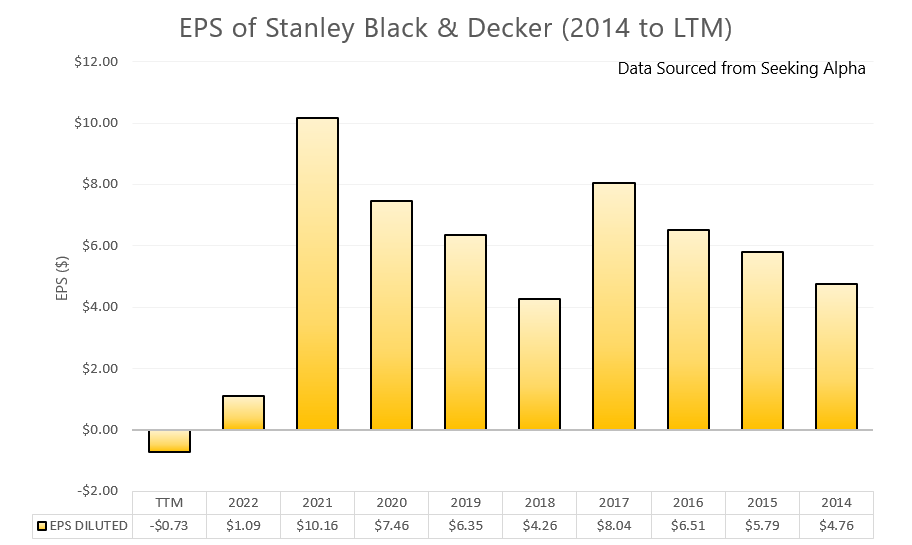

Stanley Black & Decker's overall financial performance over the past decade has been mediocre, and it has underperformed its biggest competition. This underperformance is underlined by moderate revenue growth, which has resulted in a CAGR of 3.9% over the past decade. This moderate growth in total revenue for SWK has not translated to key profitability metrics, which have worsened during over the decade. One of the profitability metrics I place importance on is earnings per share (EPS) has significantly worsened. During the period between 2014 and 2023 EPS declined from $4.76 to $-1.88. This decline of EPS will be worrisome for investors as it is massively down from the high in 2022 of $9.33 and the first time in decades that the company has seen negative EPS.

Stanley Black & Decker's EPS decline visualized (Division One Dividend)

Turning to the balance sheet, for me, the company's balance sheet appears to be respectable, underscored by a current ratio, which stands at approximately 1.3, and a solid debt to equity ratio of 1.58. I think when looking at the balance sheet, investors should monitor the debt levels, which have been increasing at a faster rate than cash and assets. At the same time, shareholder's equity has been trending down further, highlighting the increased rate at which liabilities are increasing relative to assets and emphasizing the necessity that Stanley Black & Decker return to growth sooner rather than later.

When analyzing the latest quarterly earnings of Stanley Black & Decker, being the Q4 and full-year 2023 earnings, the company has continued to see declines in revenue, with a decline of 6.88% compared to the previous year, which was mirrored by EPS which declined at a sharper rate. On a more positive note, the company managed to improve gross margins 10.7 points to 29.6% in the fourth quarter, something that I hope will precede a broader improvement to operating margins. During the call, management reiterated this mission to relentlessly focus on the successful execution of the strategic business transformation objectives in order to support a strong foundation for improved profitability in 2024. Management attributed the overall decline in sales and profits of the business to a tough market backdrop, which has been characterized by lower demand across the board. Looking at the quarterly dividend, it grew at 1.25% to $3.22 compared to the prior year.

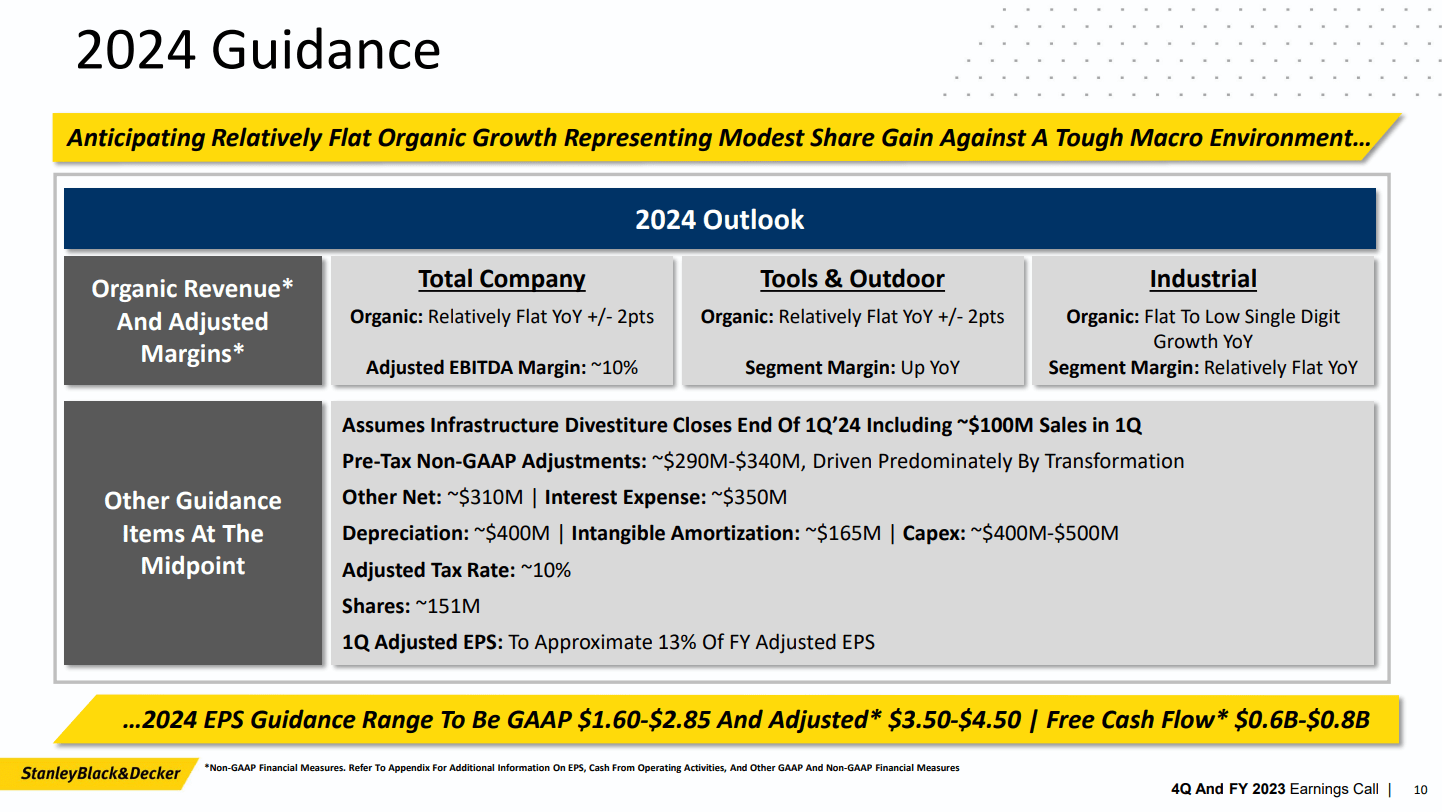

Looking forward to 2024, management expects revenue to be relatively flat, with little to no growth across its two major segments. Promisingly, however, management anticipates that EPS for the full year will be in the range of $1.60 to $2.85 which is far above the negative EPS experienced in 2023. This is a favorable sign as it gives me more confidence that the company will sustain its dividend and continue its impressive history of dividend raises which has stretched back decades. I believe that SWK will return to growth over the coming quarters and meet the guidance they provided thanks to their new initiatives and their cost reduction strategies, which I will discuss in more detail in the section below.

Stanley Black and Decker 2024 Guidance (Stanley Black and Decker)

Stanley Black & Decker's strategy, emphasizing innovation and operational efficiency, notably in developing cordless and electric tools, showcases a proactive approach in the competitive tool industry. The integration of robotics and AI, leading to a 20% productivity increase at their Decatur, Georgia plant for example, indicates a strong commitment to technological advancement. I believe that this showcases the company's ability to leverage technology in a meaningful way in order to improve financial performance, ultimately translating to increased value for shareholders. This commitment to innovation in order to stand out has not gone unnoticed, however, given that the company received numerous awards in the last few years, for products such as the DEWALT IMPACT CONNECT PVC/PEX Cutter Attachment, including at the Pro Tool Innovation awards. In my opinion, this signifies the company's leadership in tool innovation and highlights Stanley Black & Decker's ability to not only keep pace with but also anticipate and shape technological advancements within the industry.

The innovative side of the business is combined with a strong focus on cost management and operational efficiency, which has been exemplified by the Global Cost Reduction Program, which has achieved $835 million in pre-tax run-rate savings and a $1.1 billion inventory reduction by the end of 2023. These initiatives are critical for improving gross margins and enabling strategic investments in growth amid challenging market conditions, especially given that the company has struggled with profitability in recent years. Although I think these initiatives are a step in the right direction, the effectiveness of these programs in the longer term depends on the company's agility in responding to economic fluctuations and adapting strategies accordingly, something they have struggled with in my opinion.

Stanley Black & Decker's dual focus on leveraging cutting-edge technology and enhancing operational efficiencies presents a solid framework for sustained growth and financial stability. This strategic orientation positions the company well to meet evolving consumer and professional needs, potentially offering attractive returns for investors. Nonetheless, I think the success of these strategies hinges on the company's ability to execute them effectively, maintain cost discipline, and continuously innovate in response to the changing landscape of the tool industry.

Regarding valuation, as I mentioned before, I believe that Stanley Black & Decker has demonstrated solid dividend growth over the decade and shows potential for a promising future. This makes it a company I would consider owning if the price is right, given the dividend it pays out. Taking a look, at SWK's valuation, it currently carries a B- grade indicating that it might be slightly undervalued, although Wall Street has assigned a hold rating to Stanley Black & Decker which contradicts this assessment. Currently priced at $88.94, Stanley Black & Decker's price to earnings (P/E) ratio is negative. Hence, assessing its value based on this ratio becomes challenging.

To determine whether SWK is undervalued or not, I have employed a Discounted Dividend Model (DDM). This model estimates the stock's price by discounting predicted dividends to their present value. For my calculations in this model, I have used a weighted average cost of capital (WACC) of 8.1%, which is in line with what others have estimated. I've chosen a growth rate of 4.1% which is below the historical average and slightly below what analysts predict. This reflects my conservative perspective on Stanley Black & Decker. According to the DDM, I've calculated an intrinsic value of $82.76 which is slightly lower than the current price of $88.94. Considering this value, it seems there could be room for the company's stock to decline. However, given their dividend history and overall track record, I believe that holding onto SWK shares would be a reasonable decision.

DDM of Stanley Black and Decker (Division One Dividend)

In my opinion, while Stanley Black & Decker's focus on innovation and market leadership is commendable, there are risks that should be taken into consideration. Firstly, although their emphasis on cutting edge cordless and electric tools is innovative, there is a risk of technological obsolescence. To stay on top, continuous and significant investment in research and development becomes necessary. However, this could strain budgets and divert resources from important operational areas. It's crucial to strike a balance between innovation and resource allocation to ensure business efficiency and sustainability.

The global supply chain that the company relies on also faces risks from disruptions, as we have seen during the COVID-19 pandemic. Such vulnerabilities can cause manufacturing and distribution inefficiencies, which could cause potential losses. The complex interconnectedness of the supply network exposes the company to delays, shortages and increased costs. Therefore, it is essential to have contingency plans in place along with diversification strategies to maintain resilience.

Furthermore, recent economic downturns in sectors like construction and manufacturing have put pressure on Stanley Black & Decker by reducing demand for their products and impacting profitability. Rising costs and lower consumer demand, exacerbated by global uncertainties, have presented challenges. These economic conditions necessitate strategic adjustments to navigate fluctuating market demands while maintaining financial health.

Stanley Black & Decker is actively working on addressing its challenges by focusing on innovation and efficiency improvements. They are particularly focused on developing tool technologies and implementing a cost reduction plan. These actions are aimed at strengthening their position in the dynamic tool industry in the face of economic and supply chain uncertainties. Considering the company's efforts and the expected low to no growth, I believe that the current stock price of $88.94 is slightly higher than its value. Therefore, I would consider it a hold, for now. This perspective is based on optimism, acknowledging Stanley Black & Decker's potential to regain profitability and continue expanding its historically impressive dividend despite ongoing market challenges.