Kevin Dietsch

Kevin Dietsch

Seeking Alpha

I first wrote about Smith & Wesson (NASDAQ:SWBI) here on Seeking Alpha back in March 2023, and since then I have written three other articles in which I have rated the stock a Buy. And as you can see in the chart above, Smith & Wesson has far outperformed the S&P 500 (SPY), even though the company is still in a period of increased costs.

And once the unfortunately lengthy relocation costs are out of the way, the very shareholder-friendly management is likely to return a large portion of the free cash flow to shareholders. As a result, I expect to see another double-digit dividend increase and increased buybacks in FY25.

The market was expecting margins to improve in Q4 2024 at the earliest, so the double beat on earnings and revenue, combined with the margin improvement in Q3, sent shares soaring on the news. And Q3 gross margins of 28.7% are still below the long-term target of 32% to 42%, and typically Q4 is the strongest quarter, so we can expect another margin improvement in the next earnings results if all goes normally. As there are more operating days in Q4, 64 instead of 58, and the operations in the new headquarters are also more established, this should have a positive impact on margins.

In addition, election years often have a positive impact on demand in this sector, and the new 1854 lever action rifle has strong potential to be a growth driver. In general, new products are a large part of sales, in this quarter it was 20%, but in other quarters it has been as much as 1/3. This could be a risk, as Smith & Wesson needs to be one of the most innovative companies to continue to grow sales and keep competitors from taking market share. But right now it works very well and the brand power is strong.

On the Q2 earnings call, management stated that they outperformed the NCIS by 7%, and for Q3, Smith & Wesson's long gun segment doubled the market growth rate, while the handgun segment declined less than the market, which was down 4%. Therefore, Smith & Wesson probably took market share from the competition for the second time.

And also the remaining relocation costs have moved in a positive direction, from $25-$30 million in Q2 to just $10 million now. But of course, I would have liked to see the costs disappear completely in Q3. In conclusion, Smith & Wesson and Sturm, Ruger & Company (RGR) remain the dominant players in the market and I strongly believe that the normalized FCF, which I will discuss in a moment, will be very beneficial to Smith & Wesson's shareholders.

The margin decline over the last few months is largely due to the relocation, and that obviously has an impact on FCF, but as the Tennessee operations are now up and running, the efficiencies and margins will improve. While the first goal will be to repay the $65 million of borrowings by the end of the year, the FCF is likely to benefit shareholders thereafter.

Smith & Wesson 10-K 2021

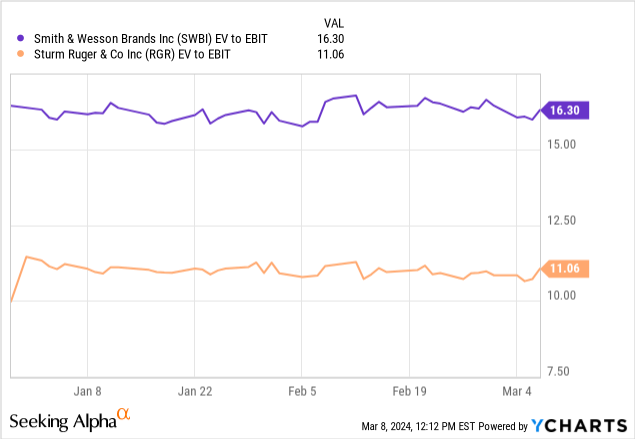

To see the potential of FCF for Smith & Wesson, I think it is good to see what they looked like before the big increase in revenue from COVID and the riots at that time. At the end of FY2020 in April 2020, they had FCF of $67 million on net sales of $529 million.

For the first 9 months of this year, net sales are $376 million and the last quarter is usually the best, so I think net sales for fiscal year 2024 will be around $520 to $535 million. At the old margins, they would have close to $70 million of FCF, and since I expect the top line to be higher next year and the margins to come back to their old strength, I am hoping for $80 million to $100 million of FCF next year.

This would give a huge headroom for dividend increases and buybacks. Currently, the dividend costs $5.5 million per quarter or $22 million per year, so an increase should be easily achievable if Q4 is strongly positive, as it currently looks.

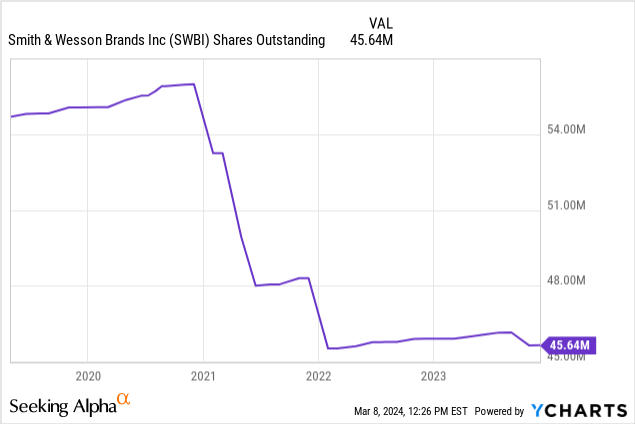

From an EV/EBIT multiple perspective, SWBI currently looks not too cheap, rather fairly valued, but normalized after deducting the one-time relocation costs, the multiple should be much more attractive and more in line with Sturm, Ruger & Company.

EPS of $1.5 at a 16x multiple would support a share price of just under $25 in FY25, which I think is definitely doable. And in the coming years, the high level of share buybacks in particular should have a very positive impact on EPS. I would not be surprised to see Smith & Wesson deliver total returns in excess of 15% per year over the long term.

In recent months, share repurchases have been used more to stop SBC dilution, but once the debt is paid down and FCF returns to its former strength, the share count is likely to decline.

And the combination of rising dividends, share buybacks, and modest earnings growth is one of the most effective ways in the capital markets to generate extraordinary returns from boring companies. If the dividend is increased by another 20% in the next quarter, this should have a very positive impact on the share price.

Craig-Hallum also upgraded the stock to Buy, and as I said, I still think Smith & Wesson has a lot of upside left into 2024/2025 and probably beyond, but I don't think they're going to hit 2020 free cash flow and sales levels this year. The situation was different then, and if they hit $100 million+ in FCF this election cycle, I think that would be a huge accomplishment.

Finally, a brief summary. Smith & Wesson has shareholder-friendly management that is likely to return the high free cash flow to shareholders in the future, the industry has high barriers to entry, and buyers in the market often buy by brand. In addition, Smith & Wesson continues to gain market share, a testament to the quality of its innovations.