cagkansayin

cagkansayin

Shockwave Medical, Inc. (NASDAQ:SWAV) specializes in developing and commercializing medical devices pioneering intravascular lithotripsy [IVL] technology for cracking calcified plaque presented in vascular and heart valve diseases. These methods provide a minimally intrusive alternative to traditional surgery. The company has made acquisitions to expand its portfolio and enter new markets with promising revenues. SWAV has also achieved milestones like DGR codes that facilitate reimbursement of payments for coronary IVL procedures and the obtention of EU MDR certification that should strengthen its market position. In my valuation analysis, I conclude that SWAV trades at a well-deserved premium relative to its peers and argue that it remains a great investment due to its promising long-term business prospects in the sector.

Shockwave Medical is a medical device company founded in 2009 and headquartered in Santa Clara, California. SWAV develops intravascular IVL technology that can majorly aid in treating calcified plaque in peripheral and coronary vascular and heart valve diseases. IVL is also applied to transfemoral access for Transcatheter Aortic Valve Replacement [TAVR] and coronary artery bypass grafting [CABG]. IVL technology provides a minimally invasive option to treat calcified plaques, avoiding surgical interventions, which positions SWAV's business moat in its sector.

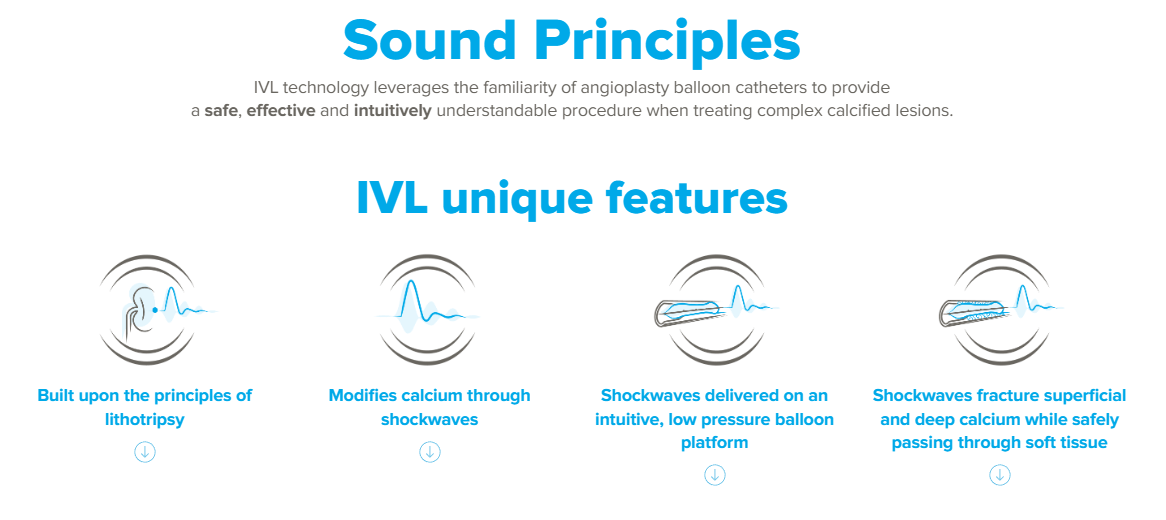

Peripheral Vascular Disease [PAD] is a disorder characterized by the narrowing or blockage of arteries due to calcified plaque buildup. This condition leads to reduced blood flow to limbs, especially the legs. IVL has a mechanism of action using sonic pressure to break medial and intimal calcium without producing trauma to the vessel wall. The expansion of the vessels allows the placement of a stent, if necessary, to enhance blood flow. This can be potentially life-saving in certain instances, which makes SWAV's value proposition compelling in the marketplace.

Moreover, Coronary artery disease [CAD] implicates hardening and narrowing of coronary arteries, making it difficult for blood to reach the heart muscles. The sonic energy breaks the calcified lesions and facilitates a stent insertion to restore blood flow. This method is used when angioplasty balloons can be implanted due to calcium accumulation. So, SWAV's treatment value is enhanced by this added feature.

Source: Investor Presentation February 2024.

Note that heart valve disease is the calcification of heart valves, such as the aortic valve, that provokes aortic stenosis, which needs to be repaired using a transcatheter valve. IVL prepares the heart for this procedure. Moreover, transfemoral access, including TAVR and CABG, cleans calcified deposits in the femoral artery with minimally intrusive methods. This makes SWAV's IP portfolio exceedingly valuable in certain patient profiles.

Another SWAV technology that is sold in the EU is Reducer, which treats symptoms of refractory angina by narrowing the coronary sinus permanently to back pressure to redistribute the blood flow, improving the ischemic myocardium and alleviating angina's symptoms like chest pain, tiredness, shortness of breath, and weakness. The implantation of this device is not intrusive compared to surgery and is performed under local anesthesia. The Lithrotripsy platforms are three and include 1) a balloon-based for lesions that can be accessed and treated with this type of catheter, 2) a catheter-based for difficult-to-cross lesions, and 3) a high-power platform for delivering energy or shock waves from a distance without contact with the calcification.

Source: Investor Presentation February 2024.

Furthermore, SWAV's products comprise Shockwave S4, M5, and C2, with CE certification to be sold within the EU; Shockwave L6 is approved for use only in the US; Shockwave Javelin is still under examination and is not yet approved for sale; Shockwave C2 AERO, Carotid IVL, Crescendo, VTL, Mitral VTL, Shockwave E8 are devices under development, not available for commercial sale; Reducer is CE marked but under clinical testing in Canada and considered for investigational use in the US.

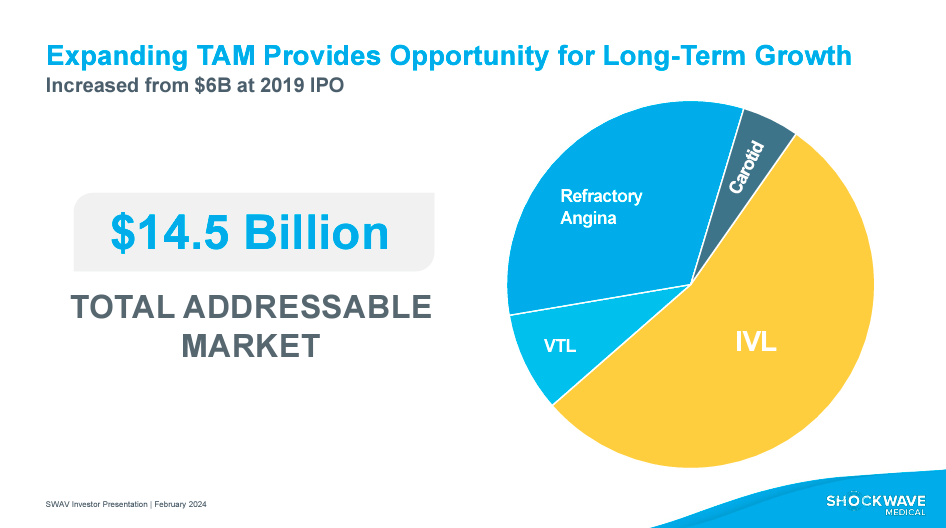

According to the investor presentation of February 2024, SWAV's total addressable market [TAM] is $14.5 billion, distributed in four segments: the application of the IVL technology is the largest segment; the Carotid segment applies to treatments related to the arteries in the neck; VTL is for treatments in the aortic valve; and finally, there is the segment associated with Refractory Angina. This TAM shows a significant opportunity for SWAV's expansion within the industry, reflected in its relatively promising revenue growth. For context, I estimate SWAV's Revenue CAGR to be 174.7% since 2017, which is exceedingly impressive.

Additionally, in the last Earnings Call, SWAV's executives announced the launch of the C2 product in Japan, expanded sales in several countries, and introduced new products such as L6 for peripheral vessels and C2+ for coronaries. This announcement indicates the capability to grow in diverse markets. Also, they reported on the acquisition and integration of Neovasc and Reducer products to treat refractory angina. These devices diversify the portfolio and open new markets promising significant revenue streams, securing long-term additional growth revenue verticals.

Source: Investor Presentation February 2024.

Furthermore, SWAV has made progress in regulatory aspects, obtaining DRG codes to facilitate the reimbursement for coronary IVL therapies. Using these codes in hospitals could increase the adoption of SWAV technologies and devices. The company also received the European Union's Medical Device Regulation [MDR] certification for multiple products to ensure their safety and efficacy and to obtain permission to sell in an important market such as the EU.

Overall, SWAV presents an optimistic view of future performance due to market expansion, strategic acquisitions, and the achievement of regulatory milestones. The combination of these elements forecasts continued growth with a revenue projection between $910 million and $930 million for 2024. These revenue forecasts are impressive, but they are quite realistic.

After reading their most recent earnings call, I see a company that has been quite savvy in its product development and launches. For instance, the C2+ product launch improved over its predecessor with over 50% more pulses and received good reviews early in its rollout. Moreover, management implied that prior authorization CMS issues are subsiding as the approval process is more streamlined. This shows that SWAV is actively pursuing new strategic launches and working closely with health insurance administrative processes to improve sales efficiency.

Source: ShockWave Medical's Website.

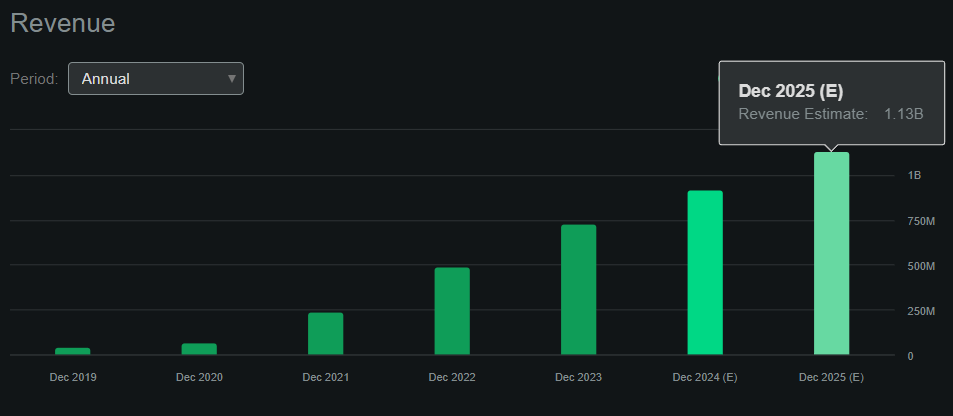

As a result, SWAV reported record revenues in Q4 2023 and promising upticks in gross profits while sustaining its margins. Quarterly revenues reached $203 million, with full-year 2023 revenues reaching $730.2 million, implying a 49% increase over 2022 results. Moreover, the international part of the IVL business and improvements in insurance administrative processes resulted in an impressive quarterly gross profit of $177.7 million, with stable gross margins at roughly 88.0%. For context, SWAV did $67.8 million in revenues in 2020, and 2023's gross profits are already 2.6 times greater than that figure! This showcases impressive revenue growth but, more importantly, profitable growth. This is despite the significant YoY increase in quarterly R&D expenses from $23.7 million to $42.3 million.

Source: Seeking Alpha's Dashboard on $SWAV.

From a valuation perspective, I'd argue that SWAV needs to be evaluated as a growth company. It has historically experienced explosive revenue growth but is trading at a relatively high valuation multiple. At the current market cap of $9.85 billion and projected revenues of $1.13 billion by 2025, the implied forward P/S ratio is 8.72. For context, the sector's median forward P/S is much lower at about 4.1. Yet, its valuation makes sense when contextualized by SWAV's revenue growth.

For context, SWAV's historical revenue CAGR since 2017 was 174.7%, and by 2025, revenue forecasts imply a 24.4% CAGR as well. If you compare this to SWAV's sector median forecasted revenue CAGR of 8.9%, it's reasonable to expect SWAV to trade at a premium. After all, its revenue growth is expected to be 2.7 times greater than its industry peers. By comparison, the forward P/S multiple is just 2.1 times greater than peers. So, in fact, I think SWAV trades at a compelling valuation.

SWAV is currently making a run toward its previous ATHs. (Source: TradingView.)

Furthermore, SWAV is already a cash-generating machine. If we exclude acquisition, SWAV generated roughly $165.5 million in cash flow in 2023. I estimated this figure by adding its CFOs and CAPEX. The company's balance sheet also seems safe, as it holds a net cash position as of December 2023. SWAV has $990.6 million in cash and equivalents against $770.6 million in total debt. In fact, SWAV's cash position has increased significantly since 2017, from $53.7 million. This signals that the company's cash flow and balance sheet are more than enough to sustain long-term growth but also positions SWAV for more M&A transactions in the future if needed. This gives ample opportunity to unlock shareholder value down the road, which, coupled with its promising business fundamentals, leads me to rate SWAV a "Strong Buy" within its sector.

Nevertheless, SWAV is not without its risks. Particularly, this is a growth company and is indeed priced as such. Thus, if revenue growth disappoints, the forward P/S multiple will contract accordingly. This would likely result in substantial shareholder losses. Moreover, SWAV's niche in IVL technology has been a significant value driver. Yet, this field is in constant flux, as heart disease is one of the leading causes of death in the world. Thus, there are significant incentives to disrupt this research field continually, so SWAV technology can become outdated relatively quickly if a breakthrough occurs.

Additionally, looking back at their recent earnings call, much of their future success hinges on prior authorization processes remaining streamlined for securing reimbursements. If insurance companies like Aetna were to change their internal policies in a way detrimental to SWAV's sales, it could significantly impact the company's future results. So, there's always a risk that insurers could adopt even more restrictive policies, yet management has been actively managing this potential risk for now. Naturally, SWAV also counts on C2+ and its L6 and E8 peripheral catheters to do well in the long run. So far, C2+ is getting early positive results, but L6 and E8 catheters remain to be seen. Still, I think SWAV's track record has been outstanding overall, so they'll most likely continue delivering quality products like their IVL solutions.

Source: ShockWave Medical's website.

Aside from these risks, I believe the investment profile favors long-term investors at these levels. It's reasonable to expect that the company will continue accumulating shareholder value over time, and its strong liquidity positions it well to engage in opportunistic M&A if needed to maintain its IP portfolio relevant in its field.

I believe that SWAV is well positioned to sustain its impressive revenue growth into 2024 and 2025. The company's IVL technology and recent acquisitions will lead to sustainable long-term revenue verticals. Moreover, its strong balance sheet and ample cash position give it the flexibility to adapt if needed, positioning it well for opportunistic M&A transactions in the future. Currently, SWAV trades at a premium relative to its peers, but I believe such a premium is more than justified given its revenue growth prospects. Hence, I think SWAV is a great investment for long-term investors in this sector, and I'm optimistic about the company's success over time.