James Osmond/The Image Bank via Getty Images

James Osmond/The Image Bank via Getty Images

Silvercorp Metals Inc. (NYSE:SVM) (TSX:SVM:CA) is a Canadian mining company with assets in China, primarily in the Ying and GC mining districts. It generates approximately 60% of its revenues from silver, 5% from gold, and the remainder from base metals like lead and zinc.

There is a significant change on the horizon for Silvercorp with the ongoing acquisition of OreCorp. OreCorp is an Australian mining company that owns an 84% stake in the Nyanzaga gold project in Tanzania, which is still in the development stage. Once operational, the Nyanzaga project is expected to produce an average of 240,000 ounces of gold per year over its first decade.

Currently, Silvercorp produces around 125,000 gold-equivalent ounces per year based on last quarter's production results. If the acquisition and construction of Nyanzaga proceed as planned, the revenue mix will shift to approximately 20% silver and 65% gold.

This change in revenue mix can be viewed positively or negatively depending on individual investor perspectives on the two precious metals. Gold has recently outperformed silver and is expected to continue doing so in the near future. This is due to gold's role as a reserve asset on central banks' balance sheets, resulting in strong demand from central banks in recent years.

Nyanzaga is an attractive asset with an after-tax net present value of $618 million and an internal rate of return of 25% at a conservative $1,750 per ounce gold price. The project has a significant scale: it can produce 2.5 million ounces over a 10-year mine life. With a high average head grade (2.1 g / tonne) and recovery rates (88%), Nyanzaga is expected to have low operating costs, with projected all-in sustaining costs (AISC) of around $950 per ounce. These figures are based on OreCorp's Definitive Feasibility Study (DFS) released in August 2022. It is worth noting that the AISC estimate may be conservative given inflationary pressures. Nonetheless, compared to the average AISC in the gold mining sector, which is above $1,200 per ounce, Nyanzaga is expected to be among the top performing projects globally. Additionally, Nyanzaga has secured all necessary permits and is anticipated to begin production in the second half of 2025.

On the downside, the project requires significant initial capital expenditure of $475 million and sustaining capital expenditure of $145 million, according to OreCorp's DFS. This may seem high considering Silvercorp's current market capitalization is $430 million.

However, Silvercorp believes that the initial capex can be substantially reduced through optimization efforts. It is also important to consider that Silvercorp is currently undervalued, as will be discussed later. Furthermore, the company holds a substantial cash position of approximately $200 million.

Completing the acquisition would involve Silvercorp paying around $58 million in cash. The deal would also result in dilution for Silvercorp shareholders, as it includes a share component (0.0967 Silvercorp shares for each OreCorp share). This brings the total market value of the offer to around $200 million, with around 75% in shares and 25% in cash.

Despite the acquisition being dilutive, it is highly accretive given the after-tax NPV of over $600 million. However, to fund the project, Silvercorp may need to access the debt market. On the positive side, Silvercorp currently has no debt and will also utilize internally generated cash flow to finance the construction of Nyanzaga. Even in a challenging year for silver miners, Silvercorp remains highly profitable, with a trailing twelve-month operating cash flow of around $90 million.

The attractiveness of the asset has led to a contested acquisition, resulting in an ongoing bidding war with Perseus Mining (OTCPK:PMNXF). For a detailed history of this war, which dates back to August of last year, interested readers can refer to the previous article on Silvercorp.

The current status of the acquisition is as follows:

Considering the above information, it is still likely that the transaction will be completed in favor of Silvercorp. However, it must be acknowledged that the outcome is not certain.

A potential strategy in this situation is to wait for the completion of the acquisition before initiating a position. This approach is based on the observation that the market has misunderstood the true potential of the acquisition. In fact, Silvercorp's shares experienced a decline following the initial announcement of the acquisition, but rebounded when Perseus contested it.

Silvercorp is significantly undervalued, and a simple calculation can help illustrate why. As of today, the company is valued at $430 million. Silvercorp has no debt and holds $198.2 million in cash and cash equivalents, as per the recently released financial results for Q3 FY2024. Even in the current challenging environment, Silvercorp remains profitable due to the cost-effectiveness of its operations.

It's worth mentioning that the cash position mentioned above does not include the investments in associates. Notably, Silvercorp owns a 27% stake in New Pacific Metals, a silver explorer in Bolivia. The investment portfolio was valued at $140 million at the end of December.

Based on these figures, it can be deduced that Silvercorp has an enterprise value of approximately $80 million. In Q3 FY2024, the cash flow from operating activities was $23.6 million. Therefore, considering the current silver prices, Silvercorp generates sufficient cash from its operations to cover its entire enterprise value in less than one year.

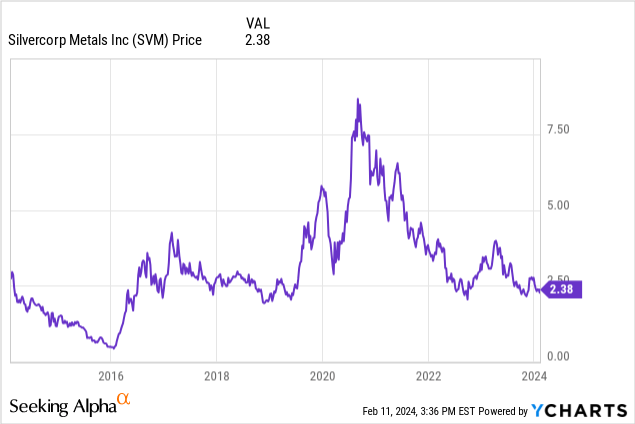

The chart below depicts the price movement of Silvercorp shares over the past decade. It shows a visually appealing pattern. Currently, Silvercorp's shares are trading at a significant support level, indicating that they have potentially reached the lowest point and are at a turning point.

The price of gold and silver will remain the primary factor influencing Silvercorp in the short term. I anticipate that the monetary pressures on precious metals will ease in the next 12 months. This process may not follow a linear path, as occasional increases in inflation could compel central banks to adopt a more cautious approach to maintain their credibility. However, considering the substantial debt levels in most developed countries, I believe the long-term trajectory for precious metals remains upward.

Referring to the chart above, we can also assess the potential upside for Silvercorp. In a bull market for precious metals, there is no reason why Silvercorp couldn't reach the highs it achieved in 2020. This would imply a potential upside of nearly 300%.

Silvercorp's discounted valuation can be attributed to a few factors. Firstly, the sentiment towards silver miners is currently unfavorable due to stagnant silver prices and rising expenses, resulting in squeezed profit margins.

Another reason for the discounted valuation is the perceived risk associated with its presence in China. Geopolitical tensions fueled by the conflict in Ukraine, economic weakness, deflation, and political uncertainty have led international investors to withdraw their investments from China at an unprecedented rate.

However, it is crucial to clarify that Silvercorp is not a Chinese company. It is a Canadian company with interests in several Chinese subsidiaries that, in turn, hold the mining permits. I believe that Silvercorp does not have a governance issue. While there is a remote possibility that mining permits may not be renewed, in case of an all-out economic war with the US, there is currently no evidence of this. In fact, Silvercorp has recently renewed some permits and even obtained new ones. Additionally, the acquisition of OreCorp provides an opportunity for geographical diversification and could potentially lead to a revaluation.

In conclusion, I consider Silvercorp to be an undervalued opportunity in the precious metals sector. While interest in the sector has declined, along with valuations, this is a natural consequence of the miners' compressing margins. However, with inflation slowing down and metal prices remaining resilient, we may be approaching a bottom. The end of this interest rate tightening cycle could act as a catalyst for a new bull run in precious metals and their equities. In such a scenario, undervalued and best-in-class companies like Silvercorp are likely to fly.