Richard Drury

Richard Drury

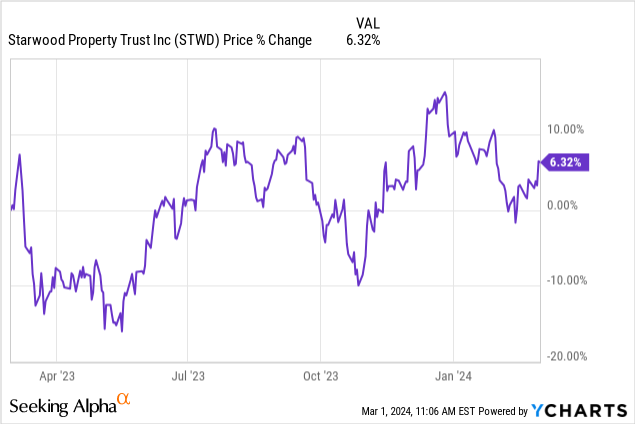

Starwood Property Trust (NYSE:STWD), on February 22, 2024 reported better than expected distributable earnings that continues to fundamentally support my buy recommendation from October 2023. The REIT is seeing solid performance in its core commercial and residential (C&R) lending segment and Starwood Property easily supported its $0.48 per-share quarterly dividend with distributable earnings in the fourth-quarter. Shares are likely fair valued based off of GAAP book value, but the risk profile remains skewed to the upside. Starwood Property pays a 9.4% dividend on autopilot, which should appeal to income investors especially!

In October 2023, I rated the commercial mortgage lender a buy due to the REIT’s juicy income and yield: A Solid 10% Yield Waits For Dividend Investors. Starwood Property continued to submit solid results for its Q4'23 with distributable earnings surpassing the consensus estimate by $0.10 per-share. The REIT has a well-structured, diversified portfolio and easily supported its dividend with distributable earnings in Q4'23.

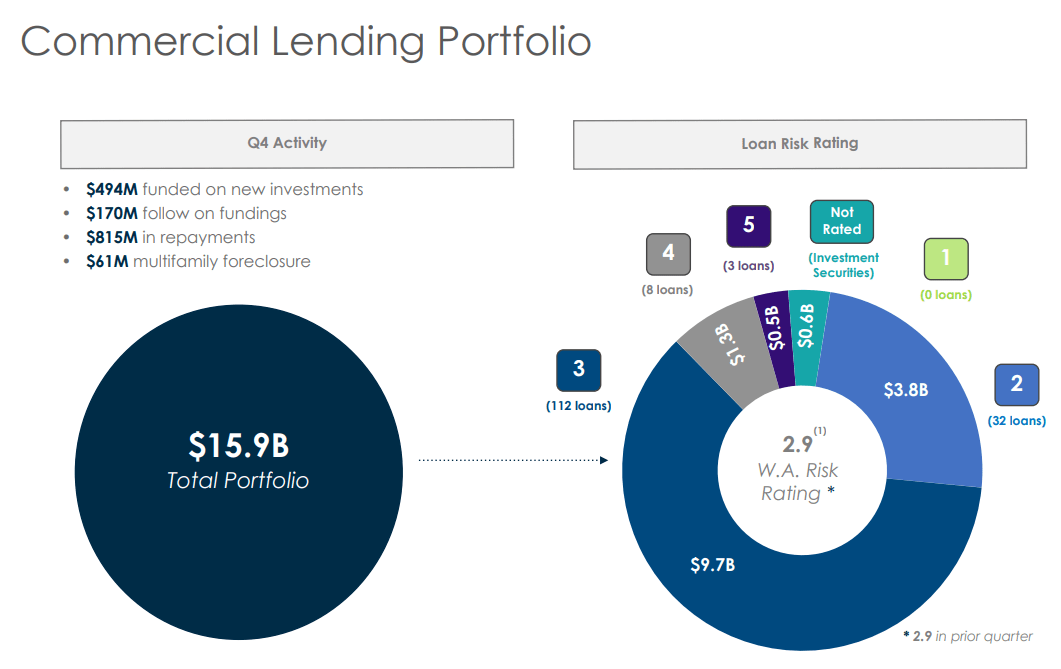

Starwood Property is a traditional mortgage lender that invests chiefly in commercial real estate loans. The REIT does have other investments as well, including property investments (medical offices) and a servicing business, but Starwood Property makes its money mainly from lending capital to CRE investors. In Q4’23, Starwood Property owned a CRE loan portfolio worth $15.9B, which represented about 58% of the company’s total investments of $27.3B. The portfolio chiefly consisted of First Mortgages (94%), followed by commercial mortgage-backed securities and subordinated mortgages.

Starwood Property

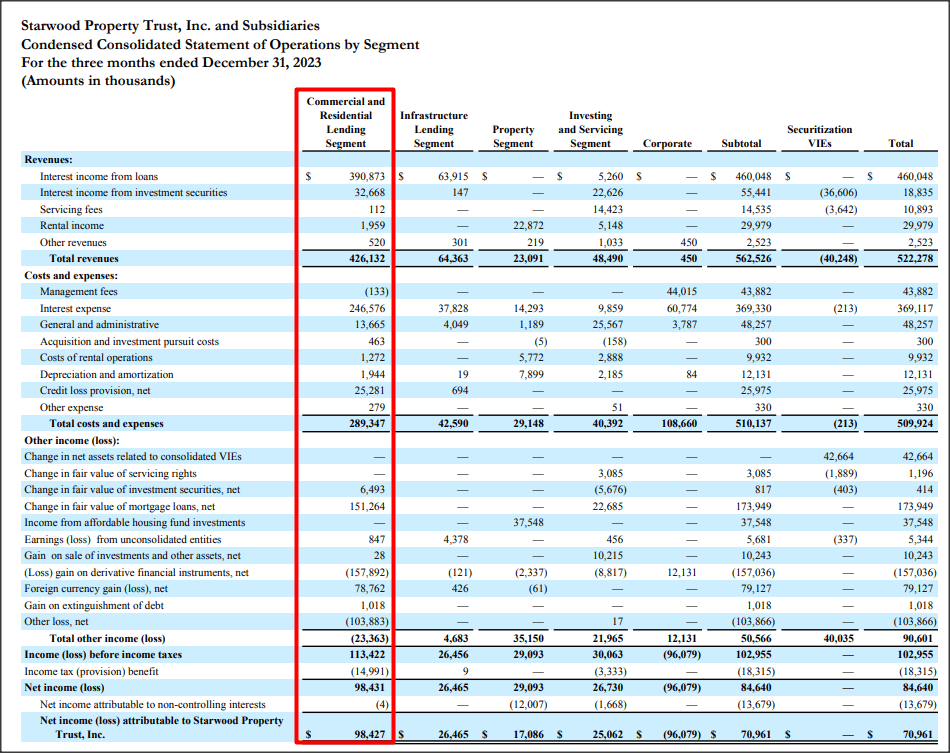

C&R lending expectedly was the biggest income source for Starwood Property in the fourth-quarter. With $98.4M in net income, C&R lending remained the most material business division for the REIT in Q4'23. The REIT recognized $25.3M in credit loss provisions in the C&R lending segment in the fourth-quarter, however, which resulted in a full-year provision of $225.7M (1.4% of the CRE portfolio). The percentage is very small and does not indicate any major, dividend-threatening risks, in my opinion.

Starwood Property

Not surprisingly, the C&R lending business generated the largest amount of distributable earnings for the commercial mortgage lender in the fourth-quarter as well. On average, C&R lending generated $0.61 per-share quarterly in distributable earnings throughout FY 2023 compared to an average of only $0.06-0.07 per-share in earnings from other segments.

C&R lending is therefore far and away the most material segment for Starwood Property Trust and about 8.7X larger than either the property investment business or REIS (which includes Starwood Property's servicing business).

The chart below breaks down Starwood Property’s distributable earnings by operating segment. The dividend coverage ratio in FY 2023 was 107%, however, due to solid financial performance in Q4'23, the dividend coverage profile was considerably better, at 121%, then in the quarter before that. The dividend safety margin, in my opinion, is reasonably solid, largely because the REIT’s distributable earnings variability, especially in the C&R lending segment, is quite limited. In FY 2024, I expect a robust performance from the C&R segment, which is concentrated in Class A properties (86.5% on a consolidated basis).

FY 2023 | |||||

Distributable Earnings | Q1'23 | Q2'23 | Q3'23 | Q4'23 | Average |

C&R Lending | $0.60 | $0.56 | $0.64 | $0.63 | $0.61 |

Infrastructure | $0.06 | $0.06 | $0.03 | $0.07 | $0.06 |

Property | $0.06 | $0.07 | $0.07 | $0.07 | $0.07 |

REIS | $0.04 | $0.07 | $0.05 | $0.10 | $0.07 |

Corporate | ($0.27) | ($0.27) | ($0.30) | ($0.29) | ($0.28) |

Total | $0.49 | $0.49 | $0.49 | $0.58 | $0.51 |

Dividend | $0.48 | $0.48 | $0.48 | $0.48 | $0.48 |

Coverage | 102% | 102% | 102% | 121% | 107% |

(Source: Author)

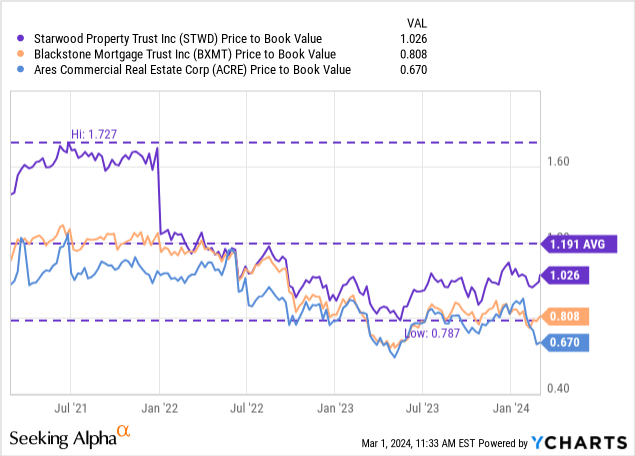

Starwood Property remains a top-quality CRE play, in my opinion. The dividend is well-supported by distributable earnings and the REIT only had 13% exposure to offices (10% in the U.S.). Starwood Property's shares are currently trading at 1.03X GAAP book value, which is much higher than what rivals' shares cost.

Blackstone Mortgage Trust (BXMT) trades at a 21% discount to book value because of its CECL reserve trend, which caused me to down-grade BXMT. Ares Commercial Real Estate (ACRE) recently chopped its dividend by 24%, which is set to lead to an improving dividend coverage profile.

This created additional uncertainty, resulting in what I believe is an exaggerated 33% discount to book value and a much more appealing risk profile. I warned about a growing likelihood for Ares Commercial to cut its dividend back in October 2023. I just up-graded Ares Commercial to buy as I believe the dividend going forward will be much better supported than in the past.

Starwood Property's P/B valuation ratio averaged 1.19X in the last three years. However, I don't expect much capital growth or multiplier expansion in the near term, as concerns about the commercial real estate market could suppress valuations in FY 2024. Considering that shares are trading above book value ($19.95 per-share), I consider shares to be about fairly valued right now. However, the dividend is the main reason for investors to consider buying Starwood Property's shares.

As was the case with Blackstone Mortgage, the provision trend is worth monitoring. A rising amount of credit loss provisions/write-offs is likely to detrimentally affect Starwood Property’s dividend coverage profile. So far, the commercial mortgage lender has decent coverage, ~107% in FY 2023, but the dividend safety margin may erode if Starwood Property has to put more money aside for loans that are expected to go bad.

Starwood Property is putting dividend collection on autopilot. The REIT is paying a well-supported 9.4% yield. The commercial mortgage lender has significant earnings power, especially in the C&R lending segment, which contributes the majority, ~58%, of the REIT's earnings available for distribution. The portfolio as such was well-performing and the amount of money set aside for provisions is not especially high (1.4%). Given that the 9.4% yield is well-protected by earnings available for distribution, I continue to rate shares a buy for dividend investors!