volodyar

volodyar

Following the Fiscal Year 2023 results release, we are back to analyze Stevanato Group (NYSE:STVN). As a reminder, our team has a buy-rating view supported by Secular Tailwinds In Biologics Demand, 2) a CAPEX plan with an economic moat, and 3) a margin expansion projection. After the Q4 results, we are moving Stevanato Group to a neutral rating. Indeed, the company has already reached our target price set at $31.8 per share, and even if it now trades at a lower level, we believe there are more downside risks than upside potential. In a nutshell, our team is optimistic about long-term demand (Fig 1), but we have an equal weight view on the company, mainly based on late-cycle destocking and a high valuation.

Stevanato Positive Outlook

Fig 1

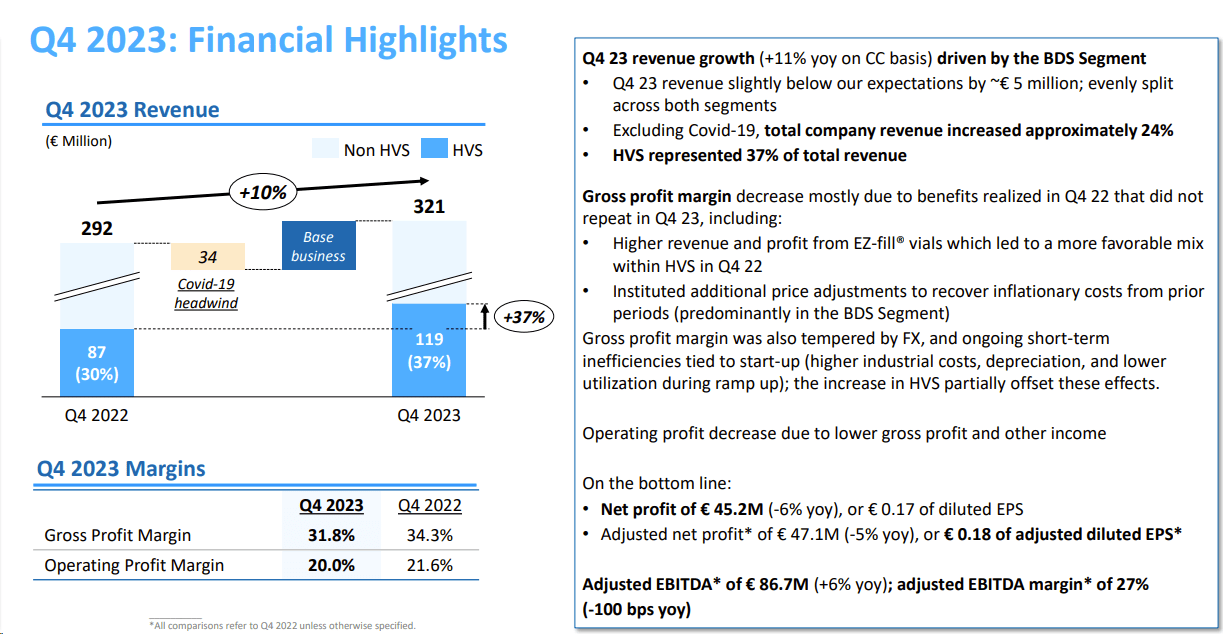

Before moving forward with our view, reporting the latest company update is essential. Stevanato closed 2023 with double-digit growth in turnover, achieving a revenue line of €1.1 billion, with a plus 10% compared to the 2022 results. Going down to the P&L, EBITDA, and net profit decreased due to start-up costs of two new plants in Latina (Italy) and Fishers (USA). Cross-checking Wall Street expectations, Q4 sales were above estimates with sales of €321 million, while the gross margin reached 31.8%, below consensus that, on average, was forecasting a margin of 33.0%. Stevanato delivered an adjusted EBITDA of €87 million (Fig 2). In particular, the company reports an unfavorable exchange rate effect in the last quarter. In addition, Stevanato suffered slightly from a tough comparison and lower profits from ready-to-use EZ-fill bottles. Sales related to COVID-19 decreased again and now represent less than 1% of total turnover. Finally, net profit fell to €45.2 million in Q4 and to €143 million for the full year, with a decline of 6.4% and 1.9%, respectively.

Stevanato Q4 results in a Snap

Fig 2

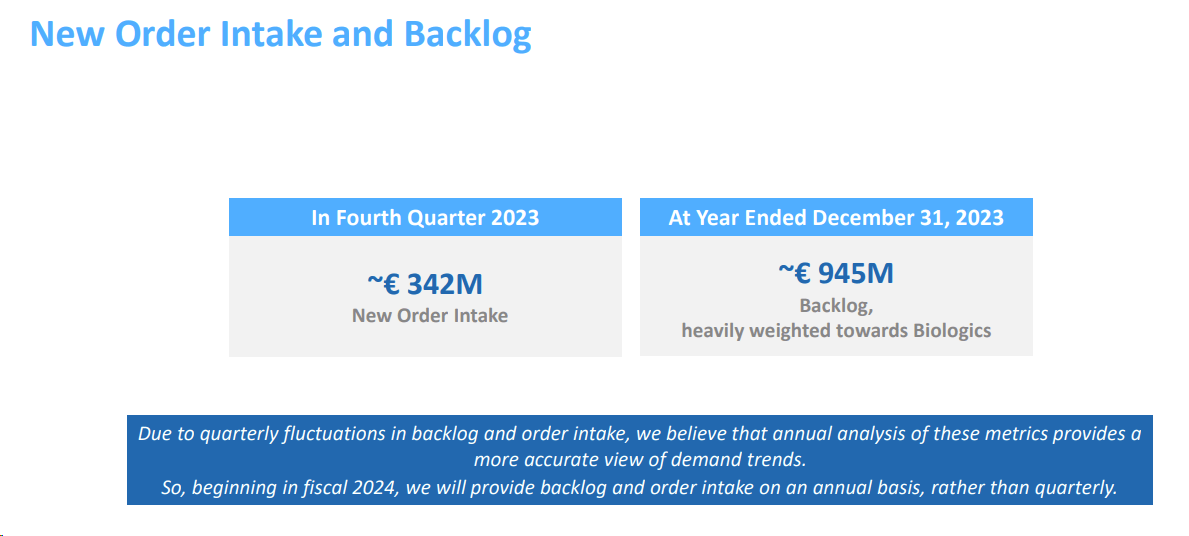

On a positive note, Stevanato anticipated further revenue growth in 2024. Furthermore, as of December end, the company's order backlog reached approximately €945 million, with €342 million in new orders in the last quarter (Fig 3).

Stevanato Order Backlog

Fig 3

Starting with the CEO's words, he reported how "Despite the near-term headwinds from destocking, revenue grew 10% compared with fiscal 2022, and we increased our mix of high-value solutions. We remain optimistic about our 2027 mid-term targets." The company should be aware of the competition outlook. Despite being cautiously optimistic, we believe Stevanato's valuation looks full. Even applying the company's forward 2024 guidance with a multiple of 25x (we valued the company with an EV/EBITDA of 24x), there is a mismatch in the valuation. Looking at the comps, on average, Schott Pharma AG, Gerresheimer AG, and West Pharmaceutical Services Inc trades at a 24x multiple with a P/E of 33x. Stevanato's P/E is above 40x with a 25.75x EV/EBITDA. For the above reason, we continued to value the company (aligned with peers' valuation) and confirmed our previous target price at $31.8 per share with an equal weight rating.

Downside risks to our target price include 1) higher competition, 2) asset replacement risks, 3) lower sector multiple valuations, 4) lower-than-anticipated demand, and 5) clients' destocking activities.

Stevanato's Q4 print was below consensus, but in our forward-thinking view, we see different outlooks from comps like Schott and Gerresheimer. Destocking activities should be muted across the space. Even if management confirmed the 2027 financial target (and we see favorable tailwinds in the future), we are now more prudent. For this reason, we confirm our valuation of $31.8 per share with a neutral rating status. We expect Wall Street calls on destocking impact, margin progression, and new capacity online. This might result in stock price volatility.