Riska

Riska

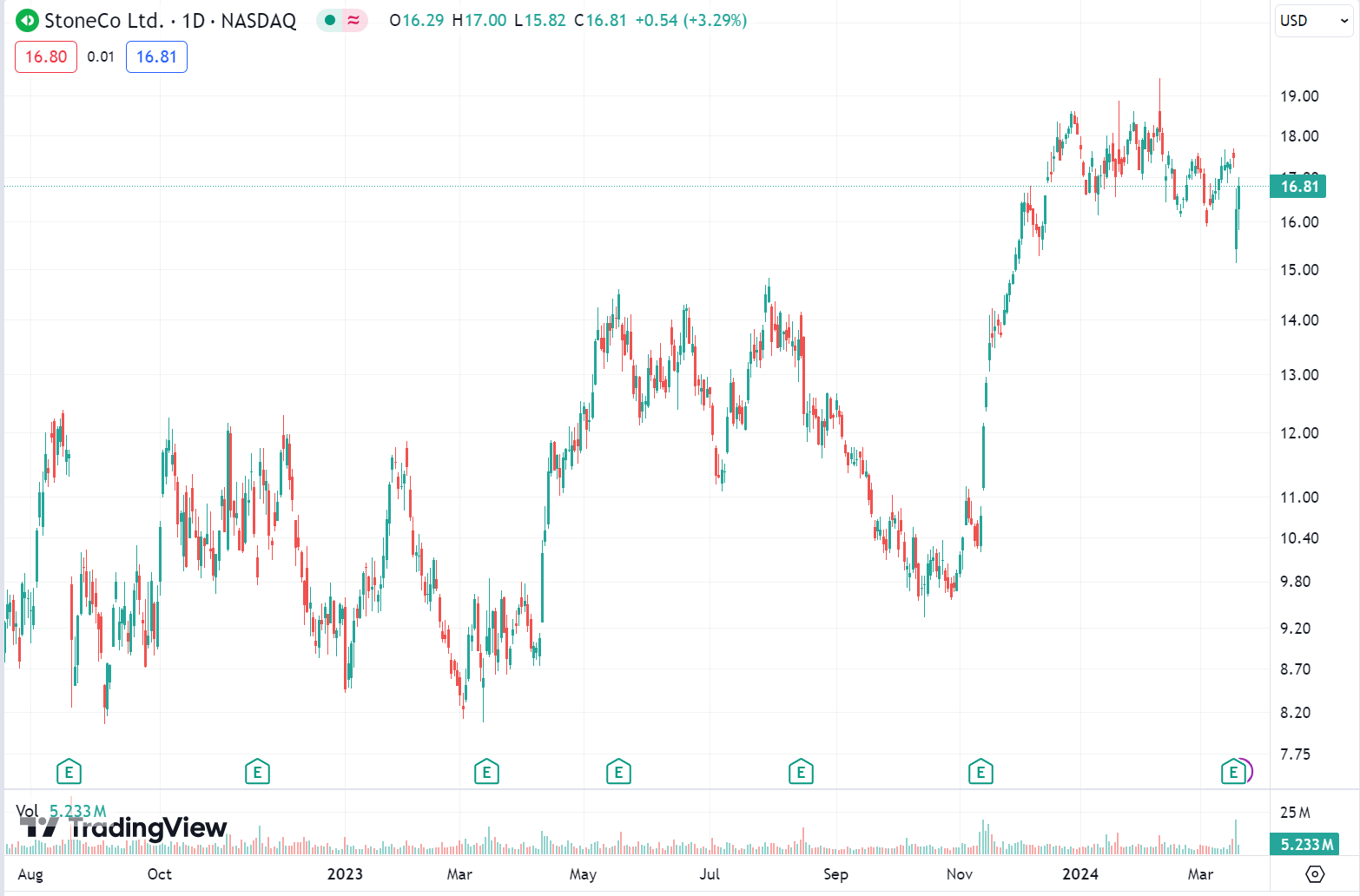

StoneCo (NASDAQ:STNE) just reported its Q4 earnings. In after-hours trading, the stock dropped as much as -15%. Since, the dip has been almost completely been bought, so that the stock is down just around 3%.

This reminds me of a similar reaction to StoneCo's earnings almost 2 years ago, when the stock first dropped 30%... to double since:

TradingView

And, just as I did back then, I believe the market misunderstands important aspects of StoneCo's earnings report - and its business. So, again just as I did back then, let's discuss "the good, the bad, and the misunderstood" of StoneCo's earnings.

My article 2 years ago (Seeking Alpha)

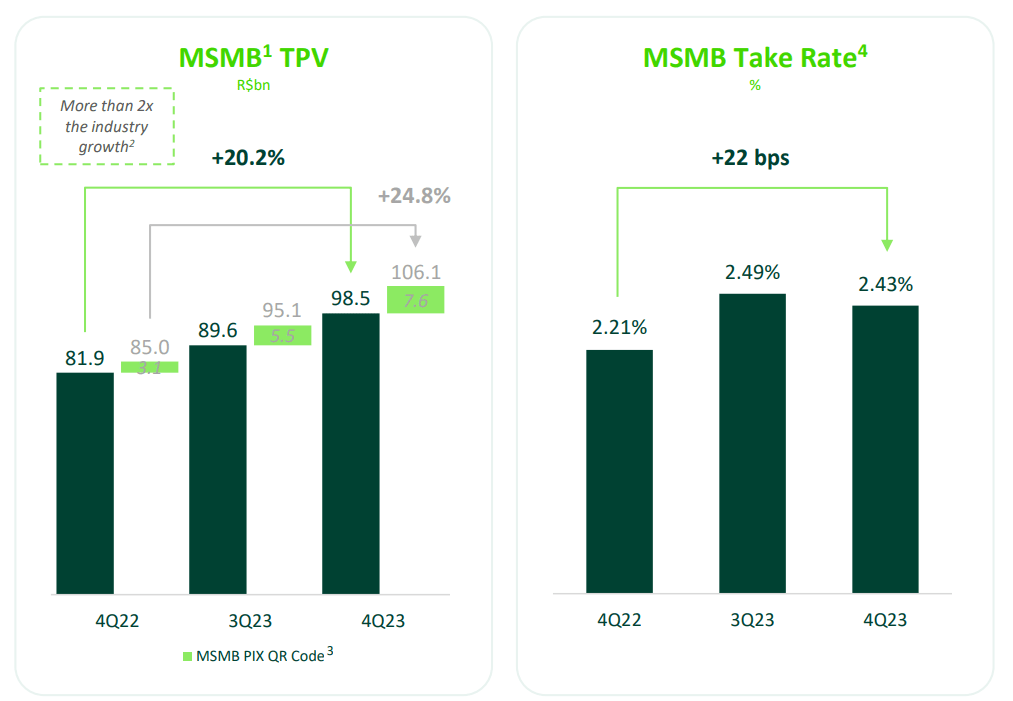

StoneCo was able to further increase its pricing throughout the year to a take rate of 2.43%, while total payment volume increased further.

StoneCo Q4 earnings report

This is because its customer base has shifted toward smaller vendors, who are charged a higher percentage. However, in the fourth quarter, this shift toward smaller vendors did not continue according to management and won't repeat either in 2024... Yet, management expects the take rate to continue to increase, up to 2.49% in 2024. I believe this goes to show StoneCo's pricing power.

Competition (read: traditional Brazilian banks) simply charges a multitude of StoneCo and is unwilling to drop its rates. It is easy to see why, because the take rate is public information. Once a bank lowers its take rate for new customers - to acquire those new customers - it has to lower them for all its current customers... which would be a significant loss of income.

As such, Q4 earnings and management commentary provided further testimony to StoneCo's ability to obtain new customers without having to lower its prices - it can even increase them somewhat in my view.

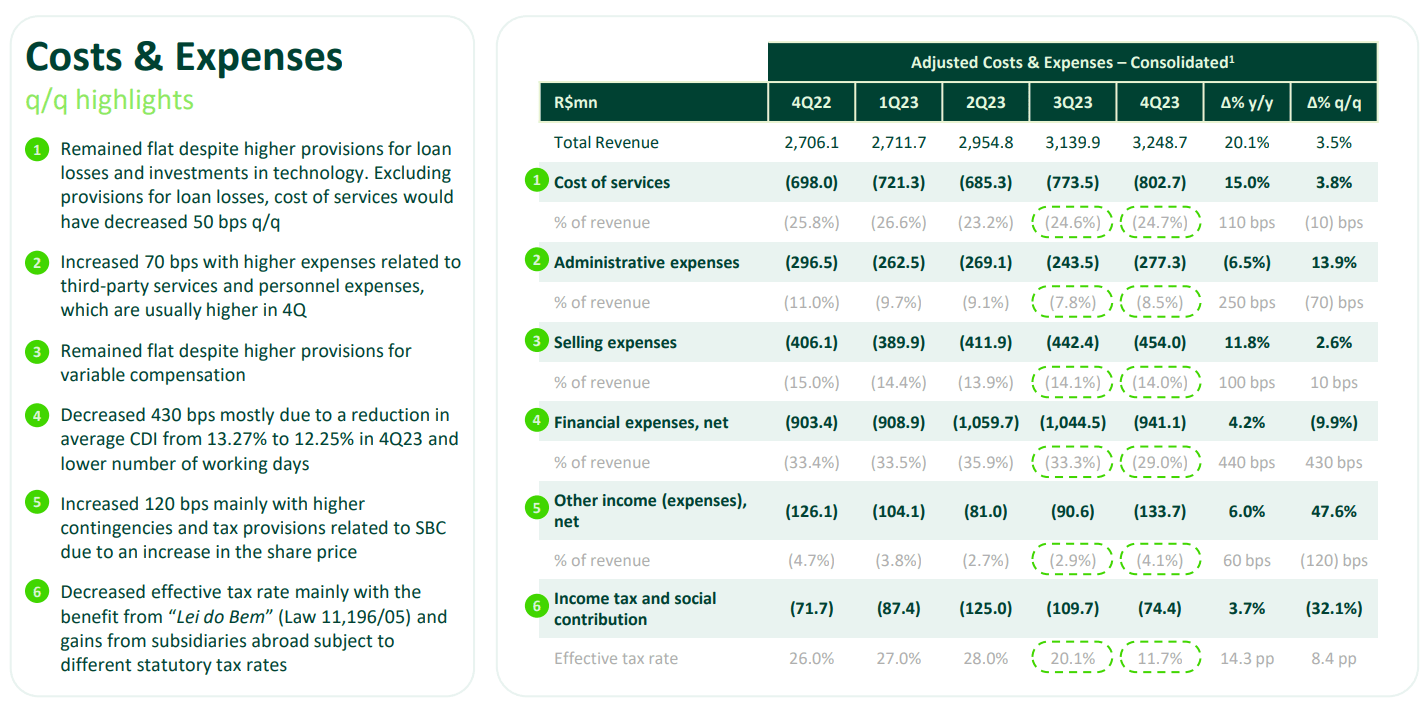

StoneCo's most important cost is its financial expenses. As such, it is great to see that these dropped almost 10%... while StoneCo actually increased its extended credit (more on that below).

StoneCo Q4 earnings report

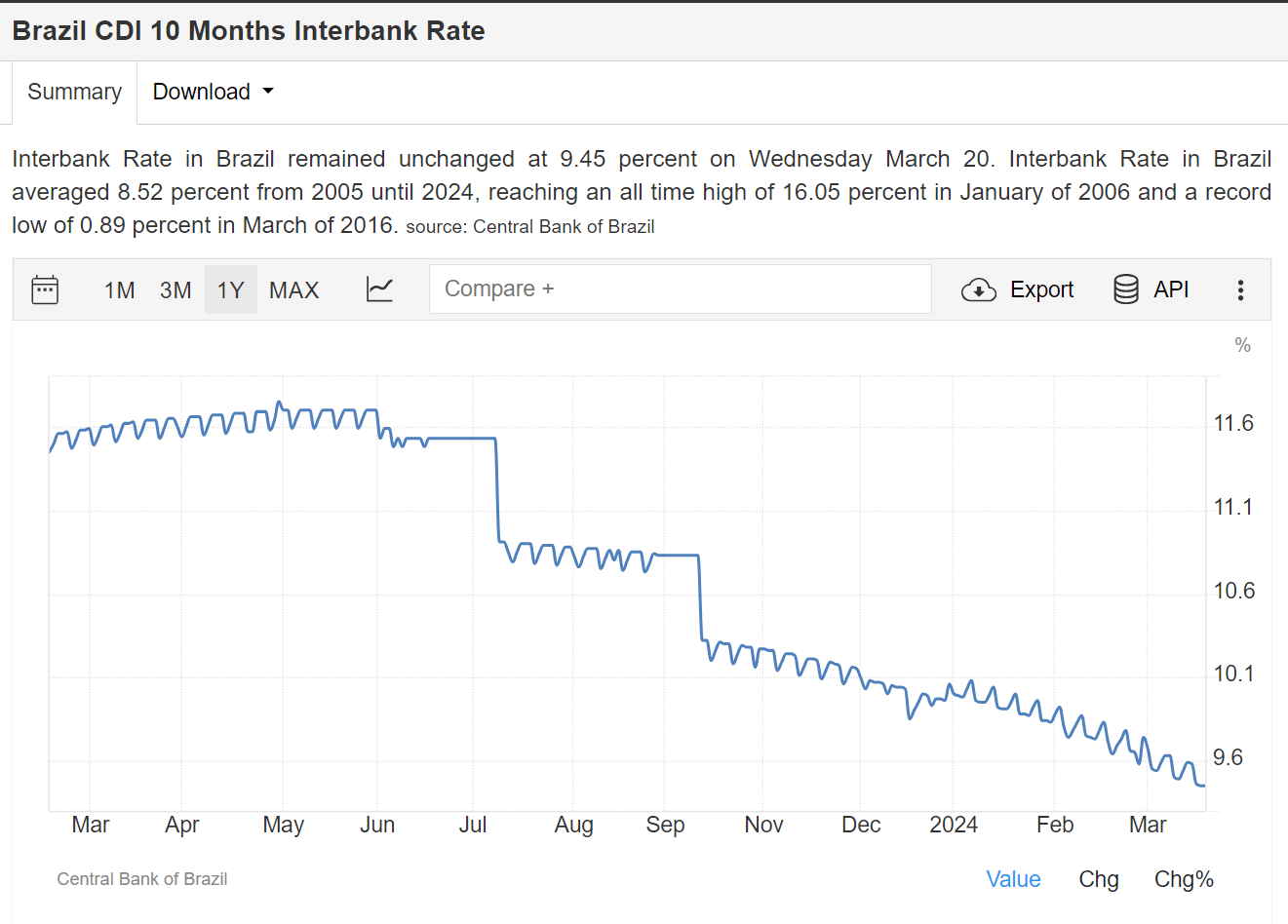

The decrease is mainly the result of the drop in Brazil's interbank rate. In that sense, it is great to see that this rate has continued to decrease throughout Q1 24:

Trading Economics

As such, we can expect a further drop in StoneCo's most important cost line... which is likely to even further drop, as the Brazilian Central Bank lags its peers in cutting interest rates.

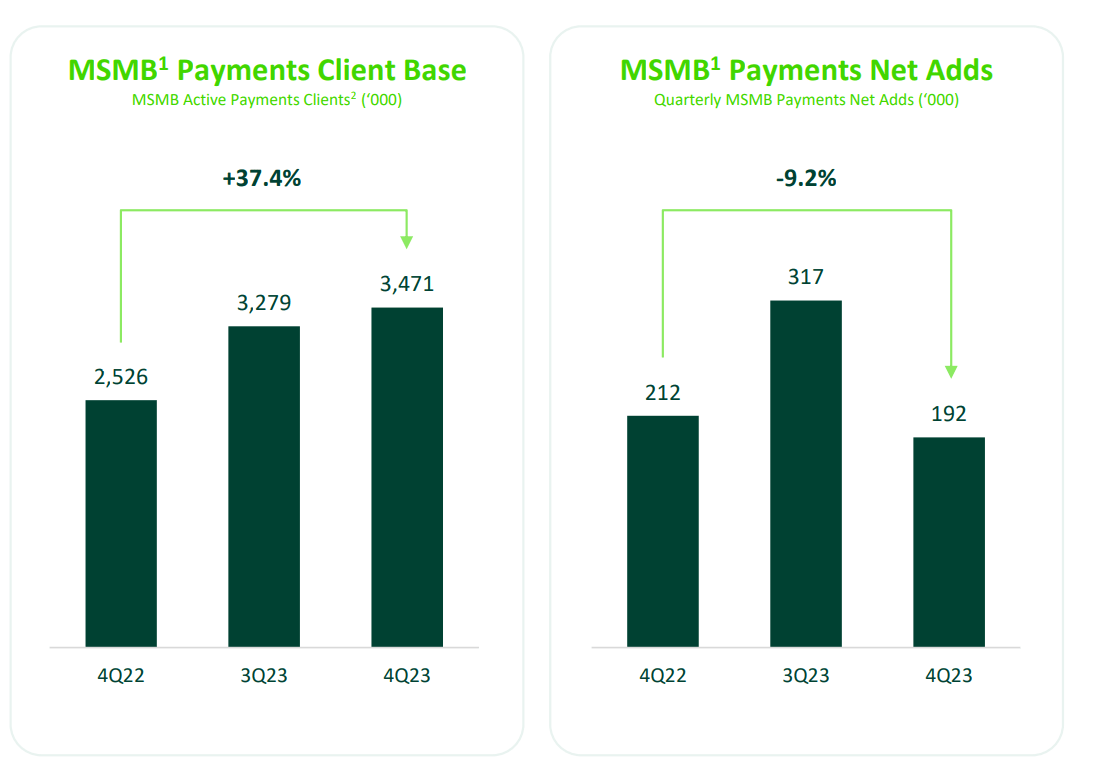

While the number of customers increased sharply (+37% year-over-year), Q4 was a rather weak quarter. In fact, StoneCo signed up fewer new customers than it did in Q4 2023.

StoneCo Q4 earnings report

Note that the "slowdown" is the result of very strong growth in the prior quarters, rather than "low growth" in this quarter... the number of customers still increased by 6% quarter-over-quarter. If StoneCo were to add 200k net new users for every quarter during 2024, its number of customers would increase by no less than 23%. I think that is still a very nice growth rate.

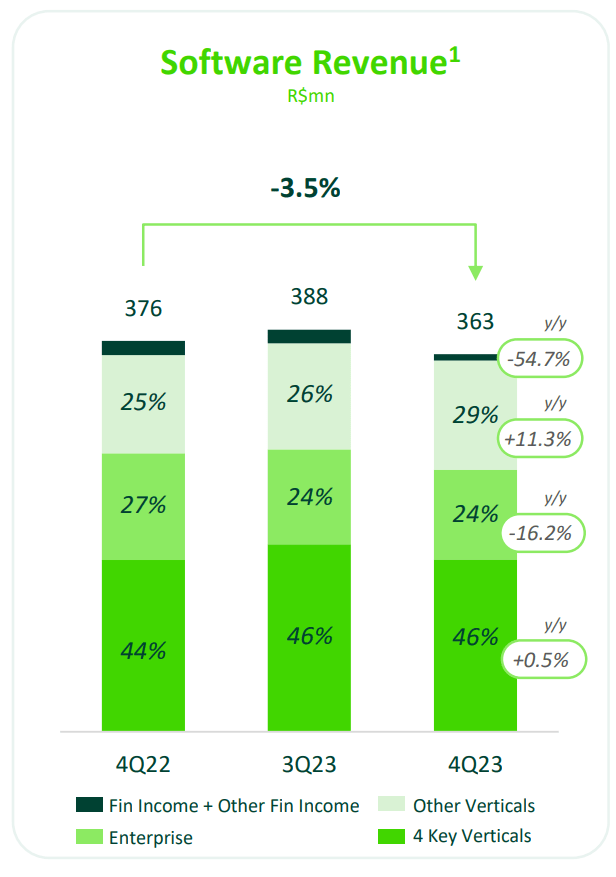

Software put in another soft quarter, in which sales actually decreased year-over-year, and EBITDA dipped quite drastically due to a one-off depreciation. However, the software division has gotten so unimportant (EBITDA this Q was 59 million BRL, less than 4% of the firm's EBITDA), that this underperformance does not bother me all that much.

StoneCo Q4 earnings report

StoneCo's EPS expectations' beat, was partially because of the very low effective tax rate (11%). This occurred as some daughter companies of StoneCo that focus on R&D made use of some Brazilian tax code that allows for fiscal benefits if investing in R&D. Sadly, next year, StoneCo expects to benefit far less from this treatment, and its effective tax rate will likely again increase to more than 20%. While this has nothing to do with the firm's operations, it will still be a drag of 10% on EPS.

Deposits of customers increased year-over-year by 52% and 36% since last quarter. Note, StoneCo does not pay any interest rate on these deposits. The growth is simply because more businesses link StoneCo's payment service directly to a bank account they hold at StoneCo, as advertised by StoneCo.

Several commentaries, including on Seeking Alpha, criticize this evolution. I just cannot understand the rationale behind this criticism. If someone is willing to park money with me for free, while the interest rate is more than 11%... I simply cannot understand why that would be a bad thing.

Yes, it means that StoneCo is transitioning towards a banking model and away from its payments provider. However, it does not take away from the payment business! The banking business is in addition to the payments business. In my book, having additional profits is better than not having those profits. Especially when there are at least some synergies between both businesses, which there are.

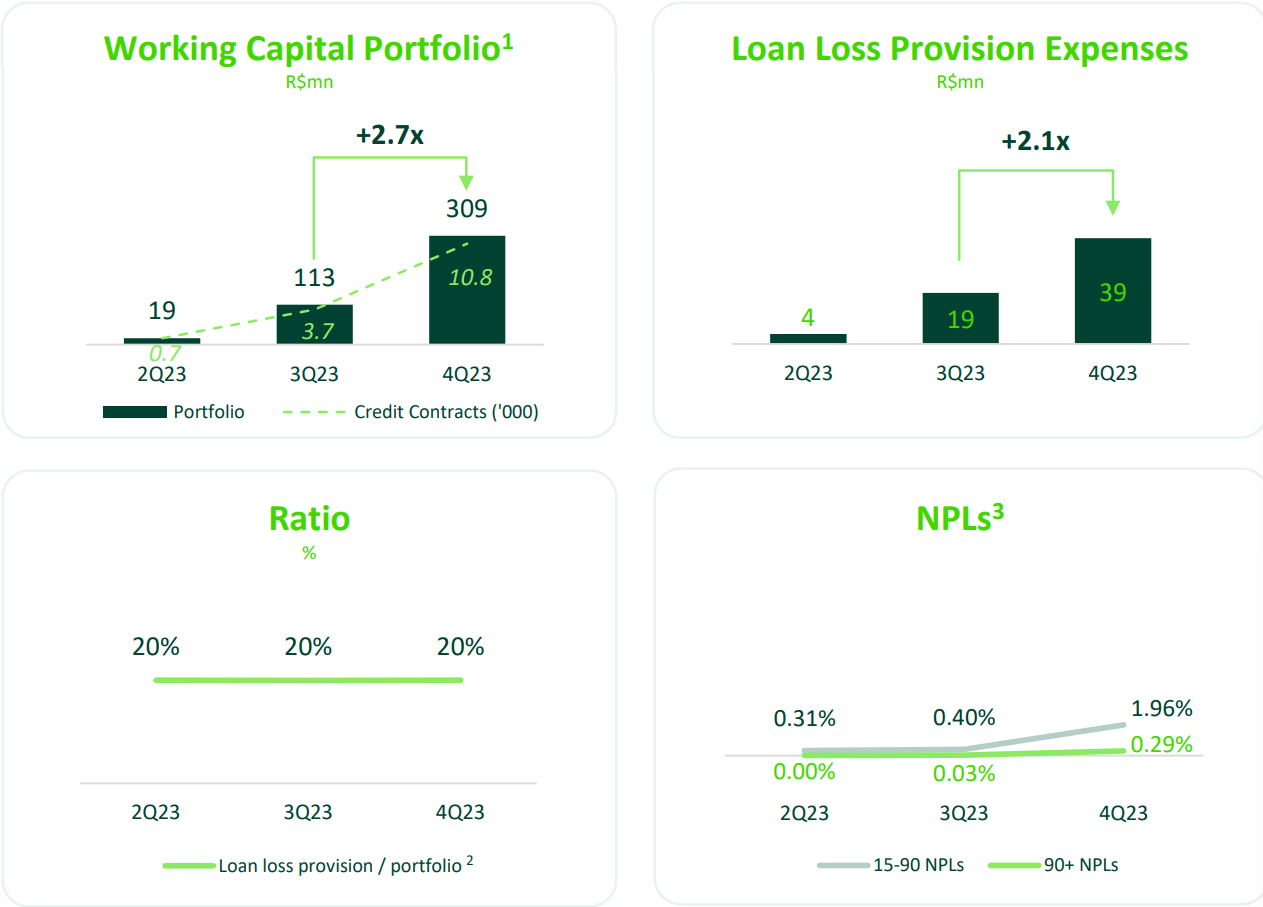

What seemingly shocked investors most, based on the many questions analysts continued to ask in the earnings call, was the very high provision for loan loss expenses. StoneCo booked 39M BRL additional provisions for such expenses, bringing the total to 62M BRL.

The shock is understandable, given that the crash in StoneCo's stock during 2021 was caused, to an important extent, by having a large amount of non-performing loans in its credit business. It is, therefore, understandable that some shareholders are quite sensitive to any whiff of problems at the credit division.

However, there are no actual problems. The actual rate of non-performing loans is 0.29%, and 2.25% if you include loan payments just 15 days overdue. Management is just extremely conservative, and has been accounting a 20% provision ever since it has re-started its credit business (see graph left under):

StoneCo Q4 earnings report

Obviously, this number will certainly increase in the coming quarters, as many of the currently outstanding loans originate in this quarter (which makes it quite impossible for them to be already non-performing). Still, management stated that it believes that non-performing loans will gradually increase towards 10% in the coming years. Note that while 10% may seem high, a proportion of the amount due of these non-performing loans will, eventually, be recovered.

As such, I believe loan loss provisions are merely increasing because StoneCo is scaling up its working capital product, NOT because the working capital loans are failing. There seems to be a lot of confusion about this point, which I believe has been a drag on the stock price. This may change, as management has stated that it might start reducing its loan loss provision ratio throughout 2024, as it gets a better idea of the real underlying NPL-ratio.

StoneCo is a strong buy for me. It is doing all the right things: growing its number of payment customers (at a slower clip than historically, but still well over 20%/year), signing them up for its banking service (for which they don't pay any interests!), and increasingly providing them lucrative working capital (which they account for very conservatively). Based on management's guidance, StoneCo trades at around 13x next year's net profit. I believe that is cheap, too cheap, hence why StoneCo is a strong buy.