Sterling Check Corp. (NASDAQ:STER) Analysts Are Pretty Bullish On The Stock After Recent Results

Shareholders will be ecstatic, with their stake up 28% over the past week following Sterling Check Corp.'s (NASDAQ:STER) latest annual results. Results were overall in line with expectations, with the company breaking even at the statutory earnings per share (EPS) level on US$720m in revenue. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Sterling Check after the latest results.

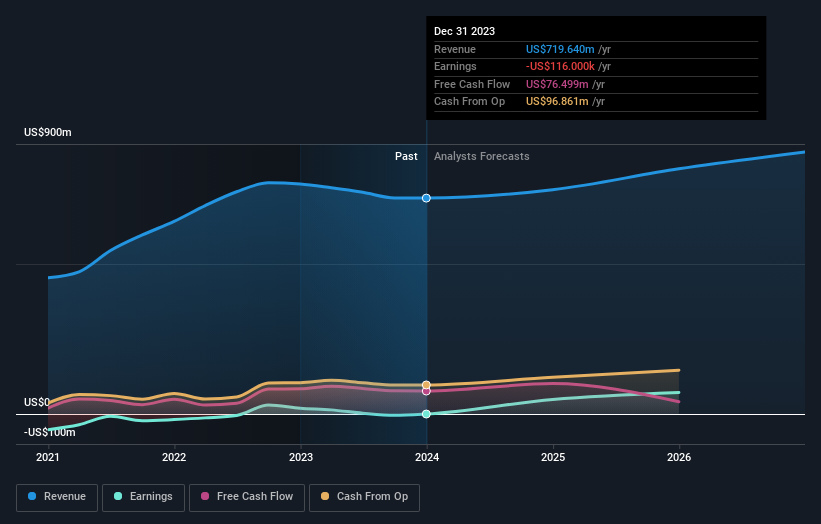

See our latest analysis for Sterling Check

Taking into account the latest results, the current consensus from Sterling Check's ten analysts is for revenues of US$747.6m in 2024. This would reflect a reasonable 3.9% increase on its revenue over the past 12 months. Sterling Check is also expected to turn profitable, with statutory earnings of US$0.51 per share. In the lead-up to this report, the analysts had been modelling revenues of US$750.8m and earnings per share (EPS) of US$0.51 in 2024. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

With the analysts reconfirming their revenue and earnings forecasts, it's surprising to see that the price target rose 7.5% to US$15.20. It looks as though they previously had some doubts over whether the business would live up to their expectations. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values Sterling Check at US$17.00 per share, while the most bearish prices it at US$13.00. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting Sterling Check is an easy business to forecast or the the analysts are all using similar assumptions.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Sterling Check's past performance and to peers in the same industry. We would highlight that Sterling Check's revenue growth is expected to slow, with the forecast 3.9% annualised growth rate until the end of 2024 being well below the historical 15% p.a. growth over the last three years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 6.4% annually. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Sterling Check.