nazar_ab

nazar_ab

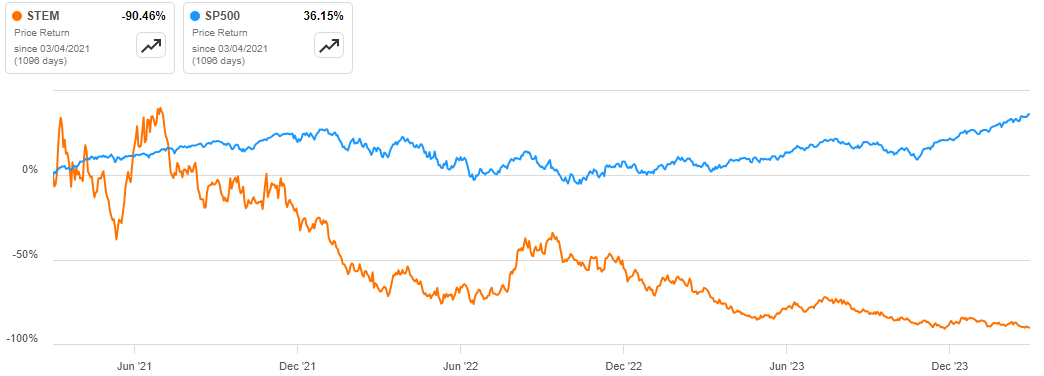

Stem, Inc. (NYSE:STEM) is a company that specializes in AI-driven clean energy solutions and services. Its stock has slumped since reaching its highs of the low 50s. It has lost about 90.46% over the last three years, underperforming the S&P 500 by a margin of about 126.61%.

Seeking Alpha

Following with massive loss, it appears that this stock has bottomed, and it is currently in what appears to me as a consolidation phase where a trend reversal is likely, or a downward breakout could occur. Even though the company’s fundamentals are weak at the moment, I don’t see a downward breakout because the company is currently making remarkable strides forward, which I believe will usher in a bullish trajectory in the long run. Given this background, I recommend patience in the short run as this company aligns for future growth and as we wait for the fundamentals to improve. From a technical standpoint, a good entry point would be when the MACD crosses the signal line or when the stock price moves above the 50-day moving average. Until then, I recommend patience.

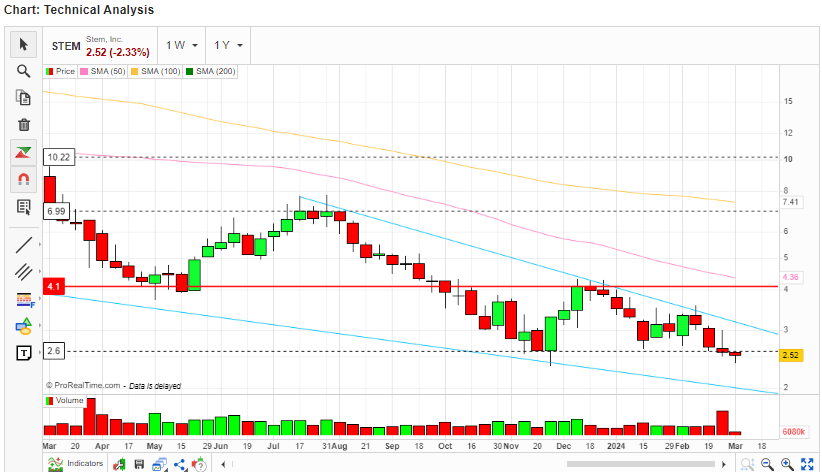

Based on several indicators and chart patterns, I will do a technical analysis of this stock. To begin with, since hitting its all-time high, the share price has formed a descending triangle which is a bearish pattern.

Trading View

Based on this bearish pattern, it appears that the stock has fallen slightly below its IPO price and therefore it may signal it has bottomed or a downward breakout could occur because the price is at its support zone. Let’s dive deeper and assess the possibilities here.

Looking at the recent price movement, it is apparent that since March 2023, the price has been moving within a narrow range, an indication that it has entered a consolidation phase where trend reversal is likely.

Trading View-Author

To get a clear direction, I will look at the technical indicators. First, the stock is trading below its 50-day, 100-day, and 200-day moving averages which are descending, indicating that generally, it is in a bearish momentum at the moment.

MarketScreener-Author

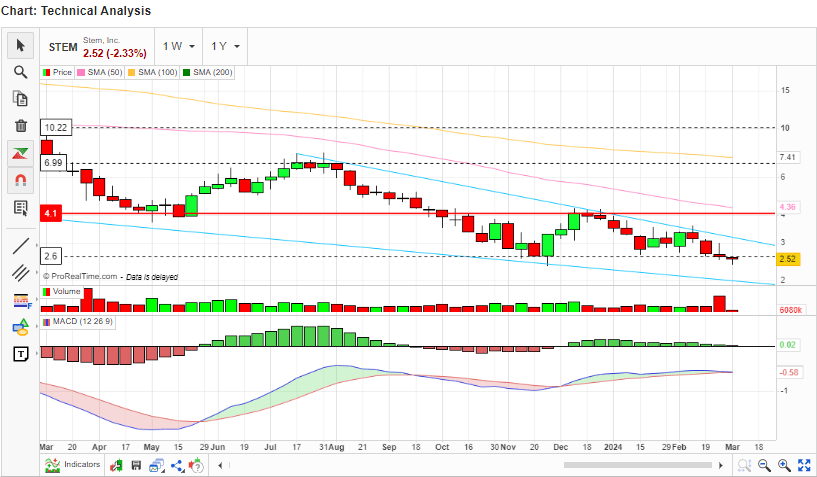

However, looking at the MACD we get a clearer signal that even though the stock is in a downward momentum, the trend is weakening, and a reversal is likely. This is because the MACD is almost at the same level as the signal line and an indication of a neutral outlook. Further, its histogram, although bearish, is growing smaller with each new bar, indicating that the bears could be losing control.

MarketScreener-Author

In conclusion, this stock is undisputedly in a downward trajectory, but it appears that it is currently consolidating and that a reversal is likely. The price might move slightly lower as it keeps consolidating. Given this background, I recommend patience as we wait for confirmation of a bullish reversal, perhaps when the price moves above the 50-day moving average and when the MACD crosses the signal line and exhibits a clear bullish divergence.

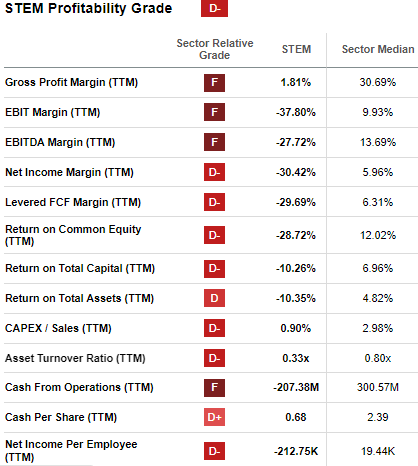

Owing to its awful share price performance, it is expected that the company’s fundamentals are not attractive. To validate this, the company has a weak profitability both in absolute and comparative terms. It has a trailing gross margin of 1.81% which is low when viewed in isolation and significantly low when compared to the sector median of 30.69%. More disturbingly, its negative net margin of 30.42% is way below the sector median of 5.96%. In my view, its poor profitability reflects its inability to control cost as a percentage of revenue. To say the least, in profitability, it’s disheartening to note that it lags the sector in all profitability metrics, making this an underdog in the profitability race.

Seeking Alpha

To add to its profitability woes, Stem has a high debt burden. Its total debt stands at $603.88 million, translating to a debt-to-equity ratio of 1.42. This is a very high leverage and it is a cause of concern to me because it increases the risk of default and limits the company’s ability to invest in growth opportunities. It troubles me more to note the company’s negative operating cash flows and negative EBITDA in trailing terms, meaning that the company likely isn’t generating enough cash flows to repay its debt and likely isn't generating enough earnings to cover its interest expenses.

Additionally, Stem has a very low price-sales ratio of 0.87 which is 42.30% less than the sector median. This implies that the company is significantly undervalued by the market, which I believe is a reflection of the company’s low demand and lack of confidence in its products and services.

Even though the company doesn’t look attractive at the moment, I believe it’s the future possibilities that matter most. With this background, let’s evaluate what lies ahead for this company.

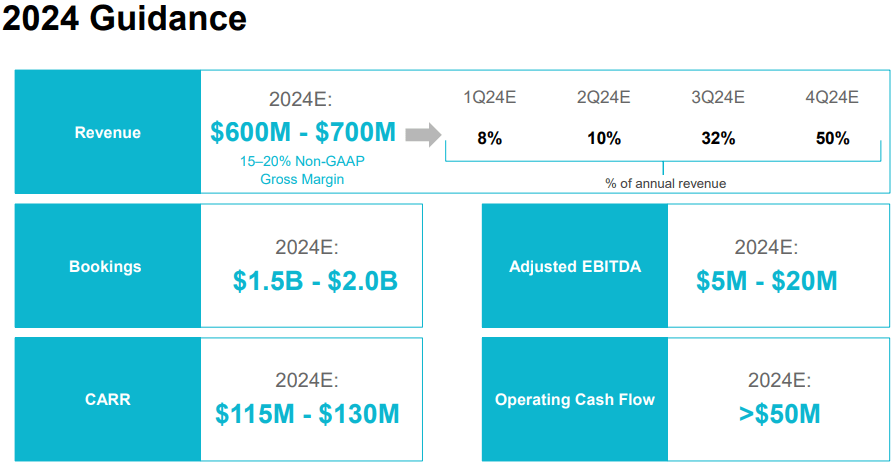

While the past is very discouraging, Stem has an optimistic outlook. To begin with a small recap, even though its profitability is not attractive, characterized by negative trailing EBITDA, it is promising to note the significant forward strides the company is making in its profitability journey. It inspires some hope to note that the company achieved an EBITDA breakeven in the second half of 2023, an indication of its improving operational and financial discipline. The most attractive thing is that the company’s guidance for FY2024 estimates are an EBITDA of $5-20 million, a testament to its commitment to profitability and operational efficiency. In general, the 2024 outlook is very optimistic, as shown below.

Q4 2023 Presentation

Further, Seeking Alpha holds a forward revenue growth rate of 34.07% for this company which is way above the sector median of 6.24%. Looking at these projections, it is apparent that the future is bright and there is optimism about this company’s prospects.

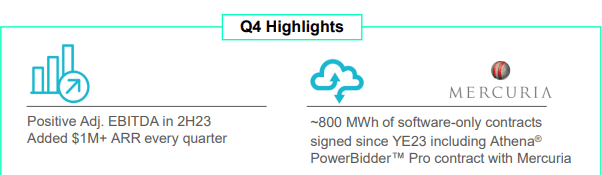

In the spirit of, “the means justify the end,” let me highlight some of the company’s means that will justify the foreseen bright end. First off, its revenue potential and visibility have been significantly enhanced through the 800 MWh of software-only contracts signed since the end of 2023.

Q4 2023 Presentation

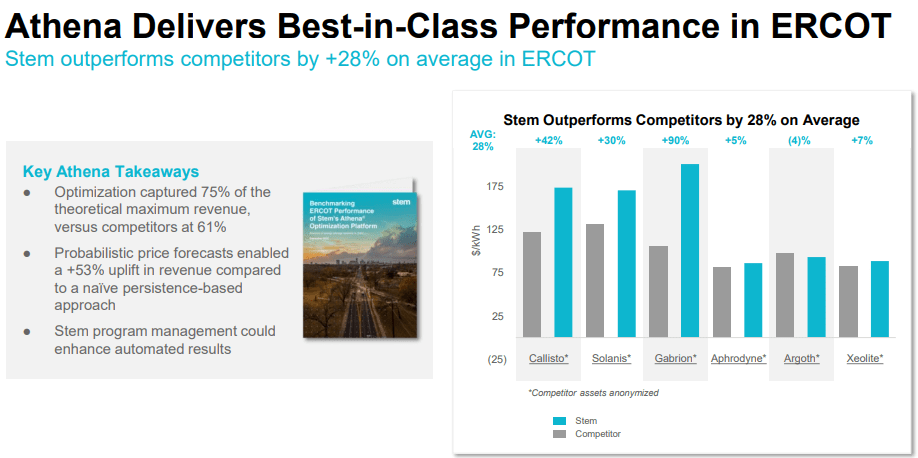

Further, the company enjoys a backlog of about $2 billion which provides more visibility in its earnings possibilities in the future. In addition, Stem has a strong demand for its Athena PowerBidder Pro which I believe will keep driving future growth because it is helping the company beat competition. Athena helped the company outperform its competitors by more than 28% in ERCOT.

Q4 2023 Presentation

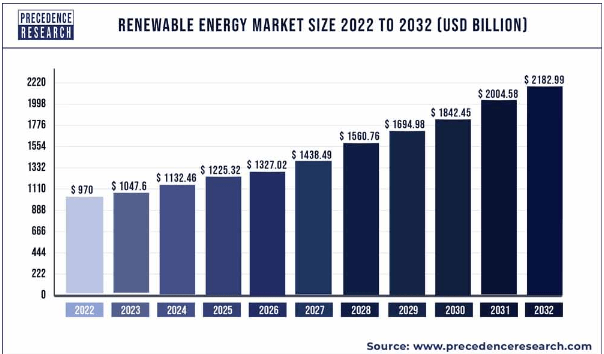

Above all, I expect the company to benefit from the strong demand for renewables. According to Precedence Research, the global renewable market size is projected to grow by a CAGR of 8.50% between 2023 and 2032.

Precedence Research

While the company’s improving contracts backed with a solid backlog are very promising as far as the top line is concerned, not forgetting the strong demand for its products and the projected market growth, I am delighted to map the profitability direction. I am confident that the company’s bottom lines will improve in the future given its improving operational efficiencies and financial discipline.

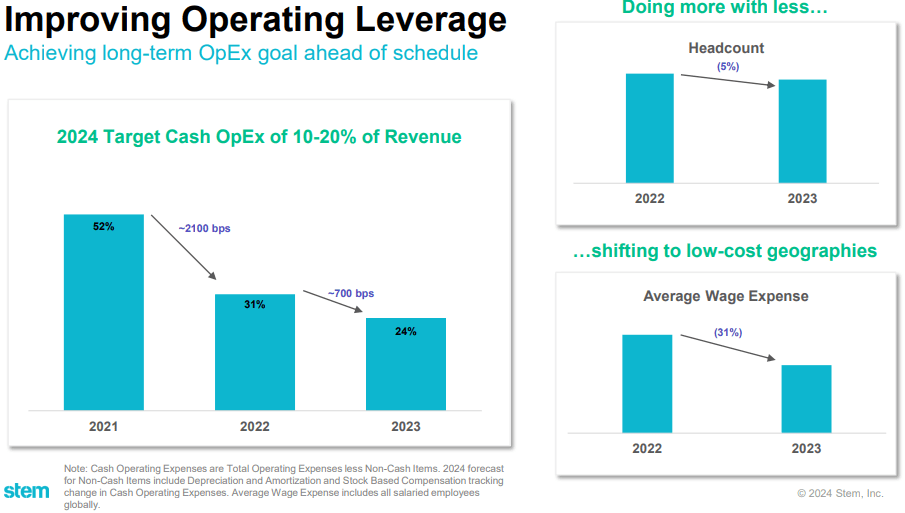

Stem has been consistently reducing its operational leverage since 2021. It has managed to reduce its operating leverage from 52% in 2021 to $24 in 2023, and they are targeting to bring it down to about 10-20% in 2024. This remarkable stride in efficiency will undoubtedly be reflected in its profit margins going forward, and hence the possibility of its projected improvements in profitability.

Q4 2023 Presentation

To achieve this efficiency, the company has adopted several measures including reducing headcount by 5% in 2023 and shifting to low-cost geographies, which helped them reduce average wage expense by 31% in 2023. In conclusion, the profitability journey is very promising and all indicators point to improved margins in the future.

Given this background, I strongly believe that the means justify the end, but investors should exercise patience until this company turns profitable and the bullish trajectory kicks in as guided earlier.

In conclusion, Stem is currently weak both technically and fundamentally. However, the future is promising and there are indicators that this company could perform well in the future. However, until profitability is achieved, and the bullish indicators become clear, I declare my reservations and recommend patience.