VioletaStoimenova/E+ via Getty Images

VioletaStoimenova/E+ via Getty Images

The stock market has been quite nervous over the past week, with only a few assets achieving positive performance. The rapid rise in yields on long-term maturities is generating uncertainty in the markets, and banking is one of the sectors that is having the worst of it: in just 4 days, S&T Bancorp (NASDAQ:STBA) has plummeted about 8%. Moreover, Q3 2023 results have only made matters worse:

In short, it was not one of the best quarters for S&T Bancorp. Anyway, I think even if the results had been positive, they could not have entirely offset the bearish movement of the major U.S. indexes.

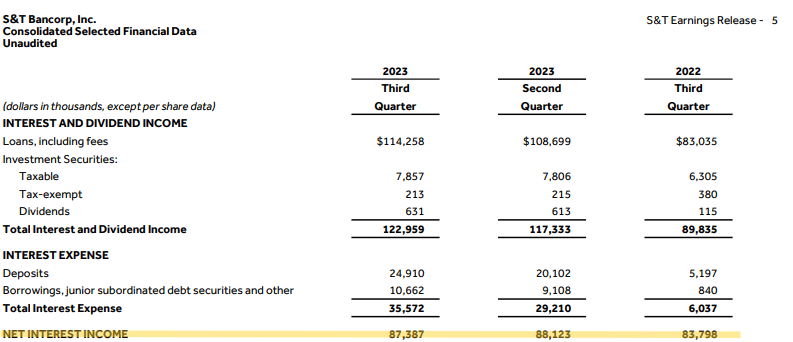

S&T Bancorp Q3 2023

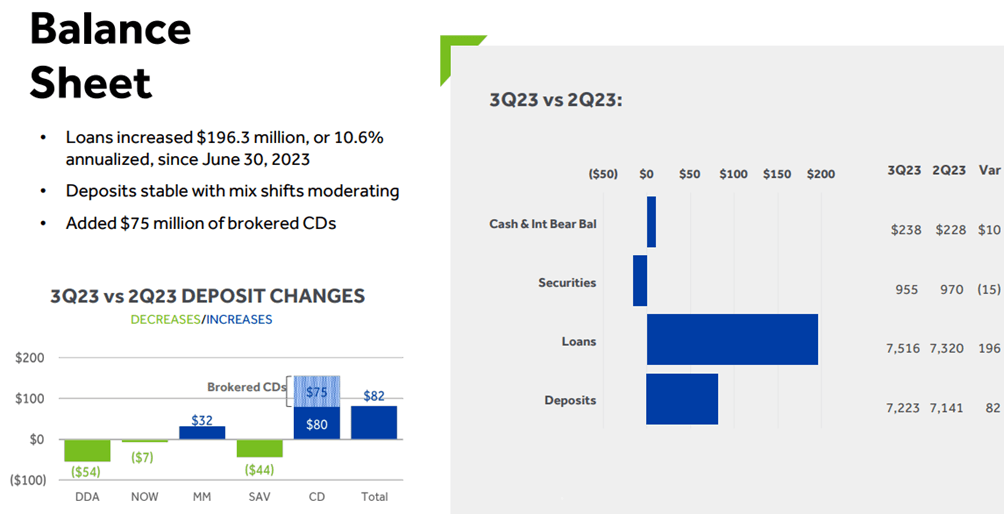

Net interest income was $87.38 million, down $0.74 million from the previous quarter. Compared to Q3 2022, there was an increase of $3.59 million.

It is no coincidence that S&T Bancorp experienced a stall in growth after Q3 2022, in fact during that period Fed aggressively raised interest rates. The cost of deposits has increased significantly from just a year ago, we are talking about a $19.72 million increase, not little for a bank that generally has a profit of just over $30 million. However, S&T Bancorp has not suffered as much as its peers in this respect.

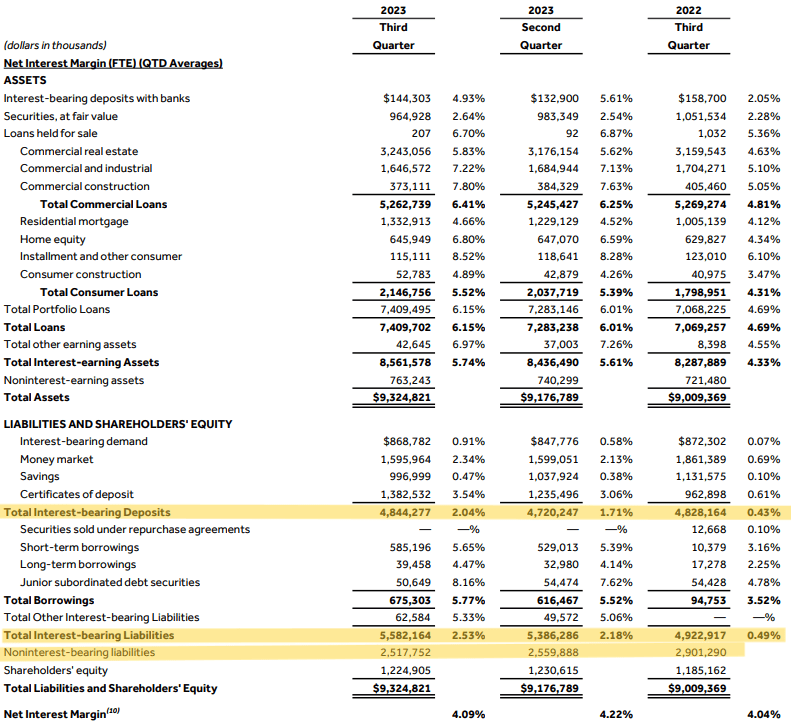

S&T Bancorp Q3 2023

Looking at the cost of interest-bearing deposits, all in all, we are just above 2 percent: the most distressed banks even reached 4 percent. In addition, non-interest-bearing deposits have remained fairly stable; in fact, they have decreased by only $384 million from last year. This may seem like a bad result at first glance, but it is not since peers suffered far worse decreases.

When SVB failed, almost all regional banks suffered significant deposit decreases in the following weeks due to a lack of confidence in the financial system. This effect, combined with money market rates reaching 5 percent, was overall not so bad for S&T Bancorp.

To date, customers' search for higher rates continues, but it appears that the decrease in non-interest-bearing deposits is stabilizing. This quarter the decrease was $54 million, the lowest amount since the Fed's restrictive monetary policy began. In Q2 2023 the decline was more than double, $138 million. Since these funds have been replaced by others to which the bank pays interest, the net interest margin has been struggling to improve for months.

S&T Bancorp Q3 2023

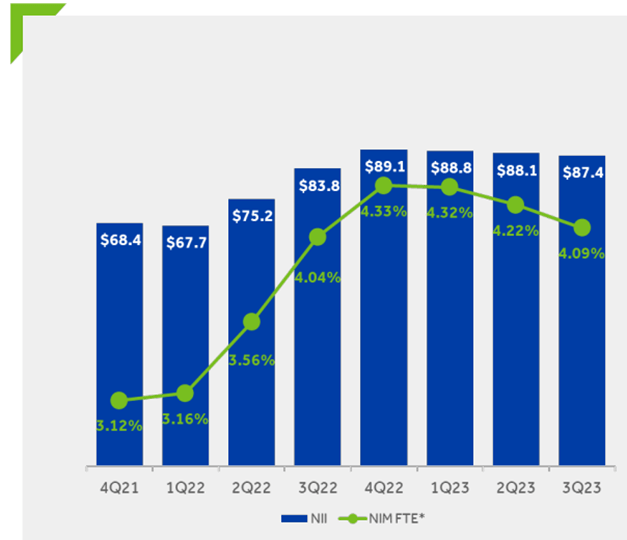

It has always been declining this year and reached 4.09%. Although 24 basis points lower than Q4 2022, it is still quite a positive result overall. The industry average is currently 3.27%, but this result may change in the coming days with the release of new quarterly reports. Achieving such a high net interest margin was also made possible by an increase in the Loan-to-Deposit ratio. In this quarterly, this ratio is 96 percent; a year ago it was 5 percent lower. In short, the bank has tried to make as much use of its funds as possible in a high interest rate environment. On the one hand, this is agreeable, but on the other hand, it puts the bank in a tight financial situation. Indeed, a high LTD ratio coincides with fewer reserves available to cover any sudden shocks.

But for how long will the net interest margin continue to fall? According to CFO Mark Kochvar's estimates, it is likely that the period of distress could extend into mid-2024.

Assuming no change in the Fed Funds Rate, the pressure on borrowing costs will continue for at least the next two quarters and will result in a reduction in the net interest margin between 10-12 basis points for each. Basically, the bottom is expected in mid-2024 and will be between 3.75%-3.80%. Of course, should the Fed reverse monetary policy, these estimates would be completely offset.

S&T Bancorp Q3 2023

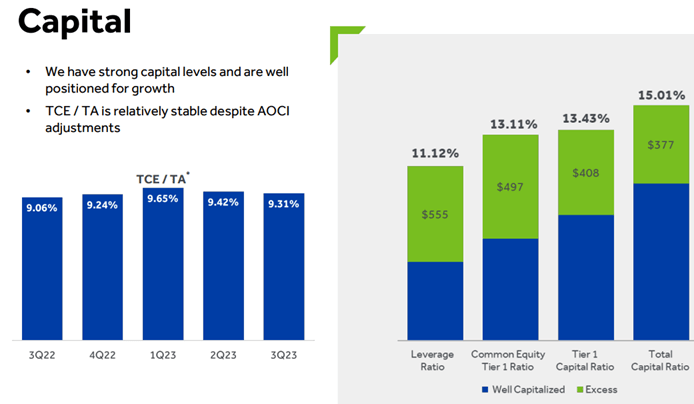

Based on the minimum capital requirements, S&T Bancorp appears to be quite solid, having a significant excess. Moreover, although unrealized losses have increased in the last period, the TCE/TA ratio still remains stable. The reason is driven by the fact that the securities portfolio has a rather shallow weight, so devaluations are not playing a major role. AOCI accounts for just under 10 percent of equity.

S&T Bancorp Q3 2023

As of Q3 2023, securities in the portfolio totaled $955 million, about 10% of total assets. This portfolio produces cash flows between $25-$35 million per quarter, between interest and maturity, and management's intention is to keep the weight of this portfolio at 10%. Thus, we can expect maturing securities to be replaced in the coming months by others with higher yields. Personally, I find this interesting, as it would allow the bank to buy risk-free securities with a yield not seen in two decades. Not all banks can apply this strategy, especially those with high AOCI.

Seeking Alpha

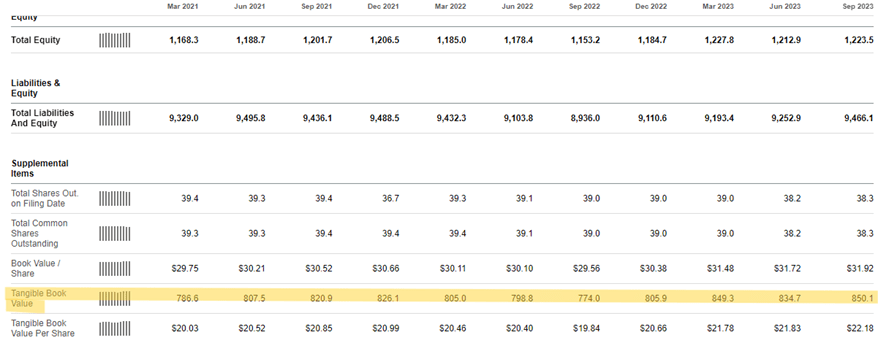

In any case, despite the good premise, Tangible Book value is still under pressure. Although the best result since Q1 2021 was achieved in Q3 2023, all in all, it remains rather flat growth. As seen, the reasons concern the increase in the cost of deposits as well as the increase in AOCI. In addition, dividends do not help either: each quarter $12.40 million is distributed to shareholders.

Finally, I recall that S&T Bancorp still has just under $10 million available to purchase its own shares. In this quarter, management preferred not to take advantage of the buyback and keep cash on the balance sheet. It is possible that this will continue in Q4 2023 as well. In my opinion, management is waiting for Tangible Book value to grow further before buying back its own shares, so it is not the right time yet. As you know, buyback reduces equity and could probably be too risky a move given the current financial environment.

S&T Bancorp's Q3 2023 disappointed expectations and negative market sentiment accentuated the decline in price per share.

Overall, the net interest margin remained quite high, but it is probably still a long way to the bottom. For today, it is estimated that until mid-2024 there will be no improvement. Tangible book value has improved, but long-term growth remains low. In addition, it is unlikely that there will be new buybacks until there is more stability in financing costs.

Seeking Alpha

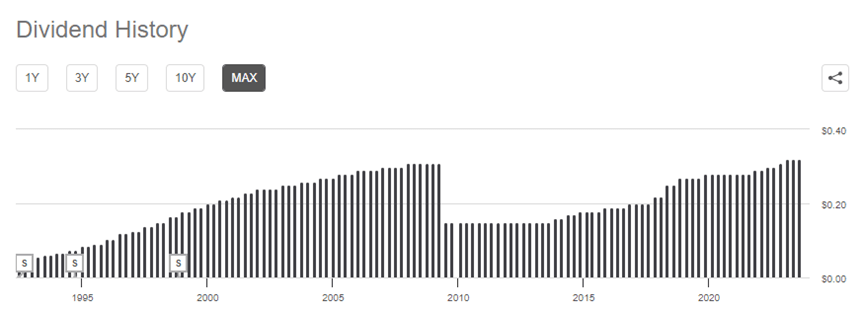

Finally, the dividend continues to be a constant, but as we can see from this image, it is not always guaranteed to improve. In the past, during the most complicated times, it has often been cut or not increased. As of today, the dividend yield is 4.94 percent, but this should not be taken for granted. The yield curve is rapidly returning to a positive slope and typically this has meant a recession in the following months.