alvarez

alvarez

Dear readers,

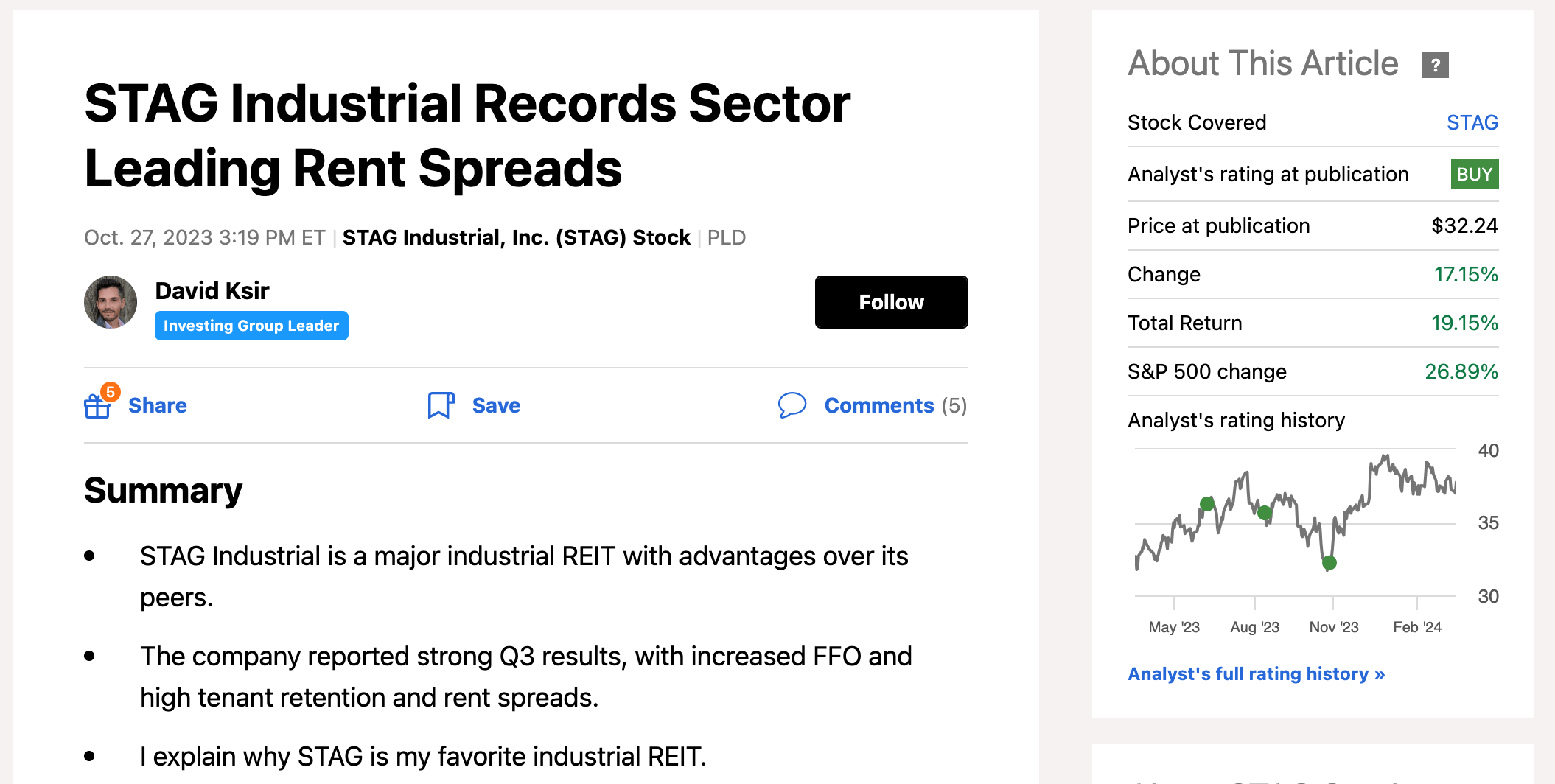

STAG Industrial (NYSE:STAG) has been my favorite industrial REIT for a while, and for good reasons. The last time I covered the stock was in October with a BUY rating at $32 per share. My thesis back then was supported by a number of positives:

The investment has done well with a solid RoR of 19%, though this was below the RoR of the S&P 500 (SPX) of 27% which rallied hard during this time on AI-related hype.

Seeking Alpha

Apart from the stock price climbing higher, since my last coverage, STAG posted their Q4 2023 results on February 13th and interest rate expectations have changed significantly. Today, I publish an update to my thesis based on up-to-date numbers and present four reasons why, in my mind, STAG continues to stand out as the #1 industrial REIT.

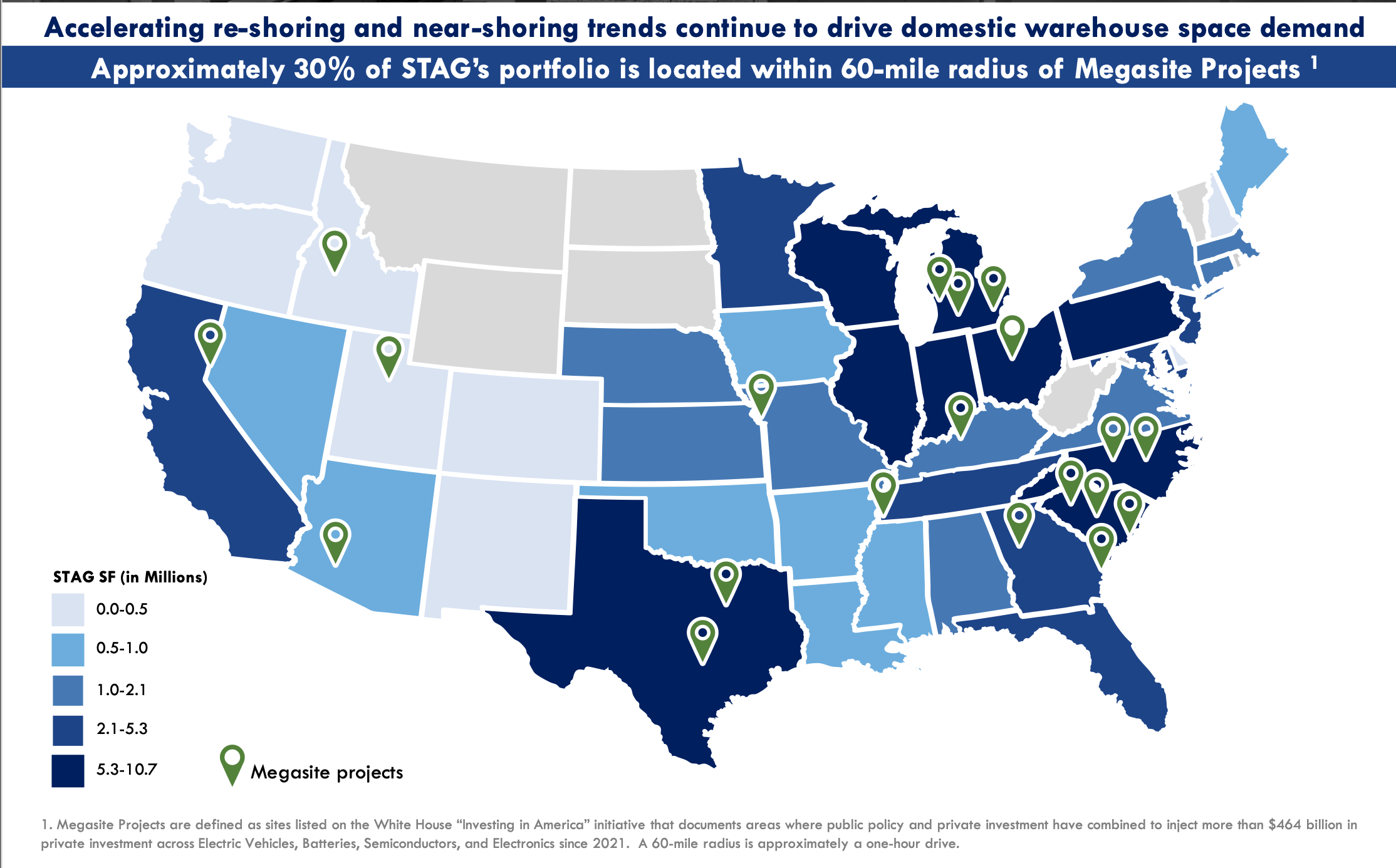

The industrial REIT market is dominated by Prologis which has 20x the market cap of STAG. But STAG has a major advantage, as its properties may be better located to capture future demand for logistics space.

You see, traditionally industrial REITs have focused on areas near major port cities such as Los Angeles and San Francisco which cater heavily to imports from China. This approach worked very well in the past, but there are two recent trends which present a threat. First, the government's on-shoring activities have created a number of large factories (Megasites) across the country and away from traditional warehouse hot spots and second, there has been a clear shift in imports from China to Mexico. In fact, after more than two decades, Mexico became the number one importer last year.

STAG's portfolio of properties is positioned well to benefit from these two trends with a high portion of properties near the Mexican border (especially in Texas) and 30% of properties near newly opened or planned Megasite projects (especially in North Carolina where half of the properties are within 30 miles from these newly on-shored projects).

In real estate, location is everything. And it seems to me that STAG's properties are located in all the right places to capture future demand.

STAG IR

STAG has not been known for high dividend growth.

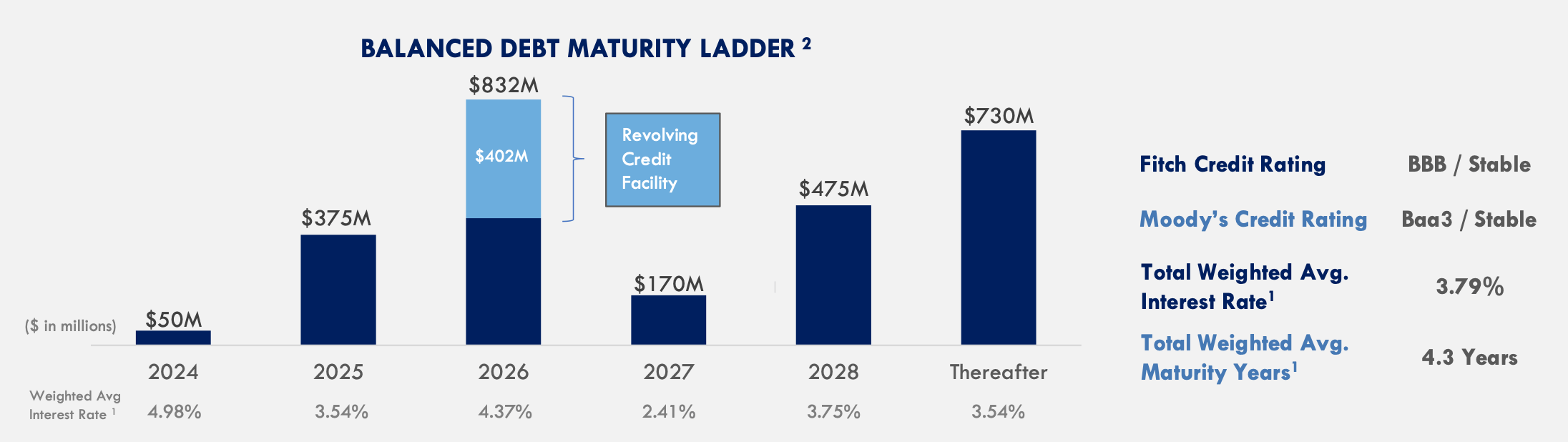

In fact, growth over the last 5 years has been non-existent, with a CAGR of just 0.69%. This is because the company has been working hard to deleverage its balance sheet and lower its payout ratio, which stood around 80% before Covid.

Seeking Alpha

Both of those goals have been achieved. The balance sheet now has a BBB rating and a very reasonable net debt/EBITDA of 4.9x, down from 5.2x last year and 5.5x the year prior. And the dividend payout ratio stands at 65% of FFO (and 75% of AFFO), which is at the bottom end of management's target range.

STAG IR

Therefore, I think it's likely that as the REIT continues to grow its FFO per share - driven by high rent increases (discussed below) - dividend growth could pick up to 4-5% per year. Apart from the obvious benefit of higher dividend payments, this could help the stock re-rate to a higher multiple as the bad reputation of a stagnant dividend is lifted.

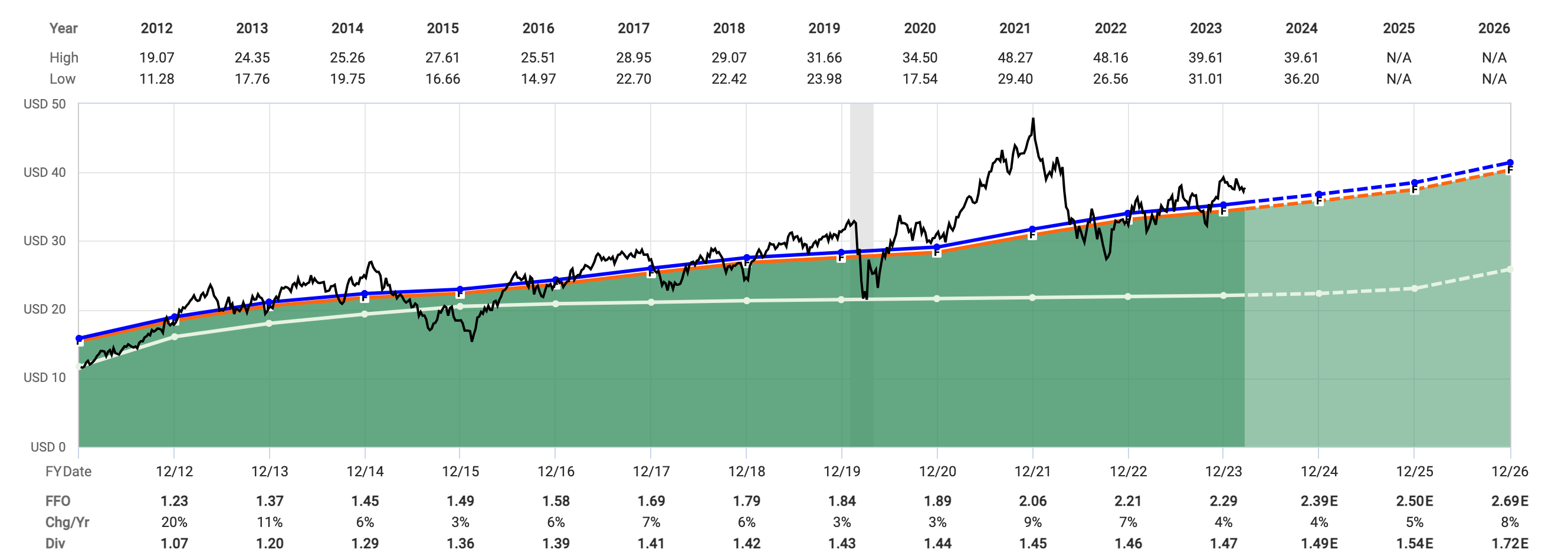

STAG has seen solid FFO per share growth over the past years with 9% growth in 2021, 7% in 2022 and 4% in 2023. Going forward, the general consensus is for 5% annual growth.

FAST Graphs

That's not crazy high, but I want to point out that the growth is highly visible. One could even say that it's locked in. The REIT averages 2.5% rent escalators on all of its leases, and its rents are currently deeply below market rents. As a result, each year when a portion of leases expire, STAG can re-lease the space at a significantly higher rent. Last year, the REIT averaged 31% cash rent spreads on executed leases.

STAG IR

And since CBRE expects that the market rent will grow by mid-single digits in 2024, it's very likely that STAG will continue to see high rent spreads on new leases, driving its FFO per share higher.

So far, we've seen that STAG's properties are better positioned than most and future growth is very visible thanks to below-market rents on existing leases. Moreover, the REIT may see a positive catalyst if management finally decides to increase the magnitude of dividend increases. None of this would matter, if the stock didn't trade at a reasonable valuation. But luckily, it does.

STAG currently trades at 16.3x FFO, which is slightly above the historical average looking all the way back to 2011. If we look at a more recent historical average, which better captures how important e-commerce has become, the stock trades right in line with the P/FFO average from 2017 to today.

FAST Graphs

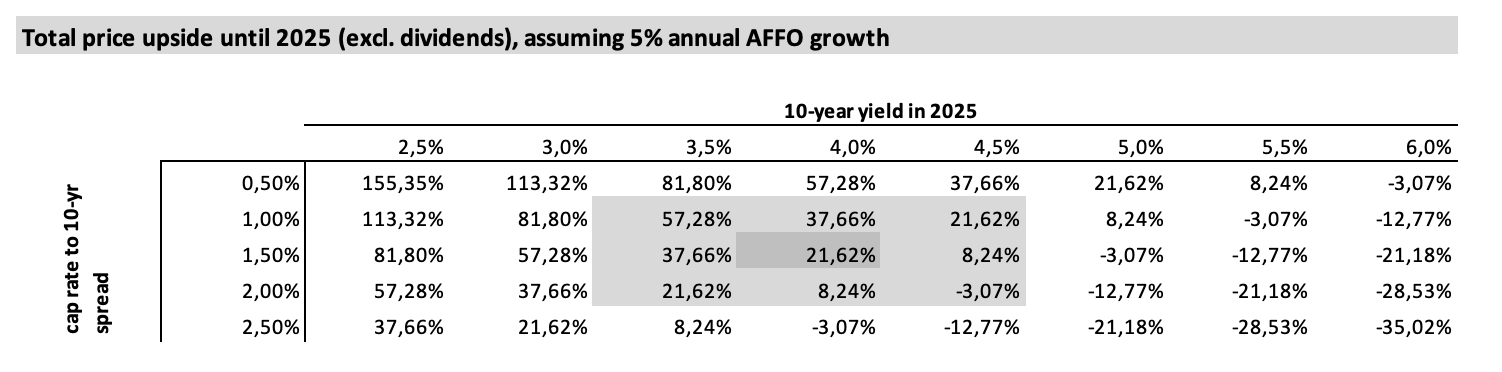

In terms of an implied cap rate, we're looking at 5.8% which is roughly 150 bps above the 10-year treasury yield today, a spread which seems fair given STAG's rating and outlook. My base case is that yields will decline to 3.5-4% over the next two years, which, given the interest sensitive nature of REITs, should drive the stock price materially higher. In particular, at a 10-year yield of 4%, we're looking at 21% in upside, on top of dividends. And a more pronounced drop in yields to 3.5% should drive the price up by over 35%.

Author's calculations

Of course, this interest sensitive nature of the stock works both ways and represents the single biggest risk for STAG as an investment. If rates fail to head lower, or even worse, head higher, the stock price is likely to fall.

Moreover, the thesis hinges on strong ongoing demand for industrial space, driven by growing e-commerce penetration. I think it's almost certain that e-commerce will continue to strengthen, but in the short to medium-term, demand for logistics space could slow if the economy falls into a recession, leading to lower consumer spending. This would undoubtably negatively impact demand for STAG's space, as companies would limit their inventory and potentially downsize their warehouses as leases expire.

Finally, what makes STAG attractive is the location of their properties in relation to where imports are coming from. Therefore, potential geopolitical tensions and/or government policies that limit imports from Mexico represent another potential risk for STAG.

As with all REITs, the decision to invest comes down to your interest rate expectations. If you expect rates and yields to head higher, then STAG is obviously not the right investment because the stock price will go down if yields rise. But if you're in the camp that rates have peaked and, perhaps, even expect yields to decline over the medium term, then STAG can provide a 4% dividend yield while you wait for that decline in yields and upside of roughly 20% if yields decline to 4.0% by 2025. Should yields decline as low as 3.5%, we're looking at an upside of 37%. I think that deserves a BUY rating.