Wasan Tita/iStock via Getty Images

Wasan Tita/iStock via Getty Images

SS&C Technologies (NASDAQ:SSNC) is a global leader in financial services and healthcare technology solutions. Operating largely behind the scenes, they provide mission-critical software and services to a diverse clientele, including investment firms, banks, and healthcare organizations.

Despite a strong 739% all-time price return since its 2010 IPO, SS&C stock has hit volatility since reaching its all-time-high of $83 in 2021. Its 5-year return stands at merely 6%, with the stock trading sideways over the past year. Since my latest coverage on the stock in 2020, however, SSNC has appreciated by 15%, confirming my bullish call then.

I initiate my coverage with a buy rating. My modeled 1-year target price of $71 presents a projected 11% upside from today’s price of $64.

key metrics (ycharts)

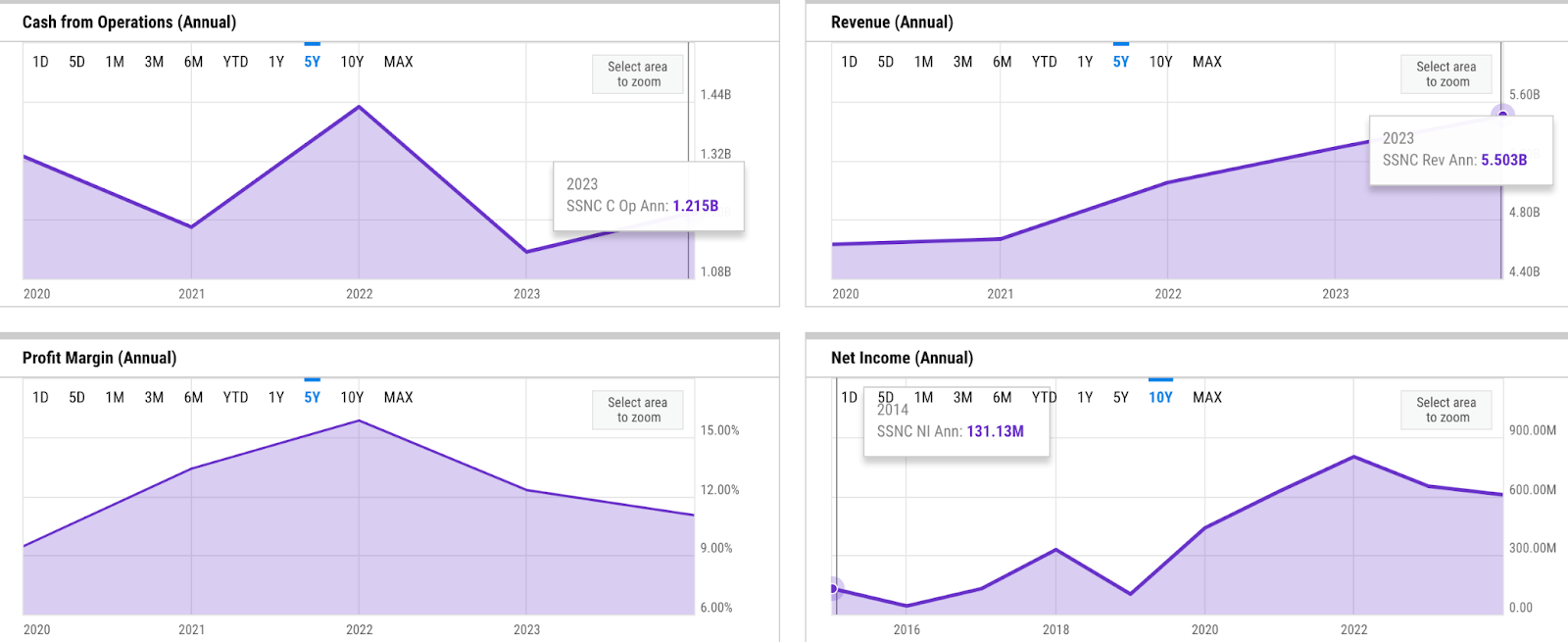

Despite SSNC's overall strong fundamentals, revenue growth has been choppy and slow as of late. For instance, revenue growth was over 100% in 2018 but then started to decline to 35% the following year, and since 2020, SSNC has been a mid-single-digit grower.

However, I don't think that it's a structural issue. Part of the reason why revenue growth has been slow as of late is the overall size of SSNC. SSNC generated $5.5 billion of revenue in FY 2023, which is $220 million more than last year. Though it seems like a meaningful increment, it is merely over 4% YoY growth. The uneven revenue growth outlook, in the meantime, has been due to the size of inorganic revenues that have periodically flown into SSNC, driven by occasional M&A activities, which have been key to SSNC's growth strategy for decades.

SSNC has strong profitability and cash flow generation. On average, it generates over $1 billion of operating cash flow / OCF every year. In 2021, SSNC delivered a net income of over $800 million, a 5-year high. However, since then, annual earnings have declined to $607 million in 2023. In the same period, net margin also contracted from 15% to 11%. In my view, the margin contraction could explain the lackluster share performance since 2022.

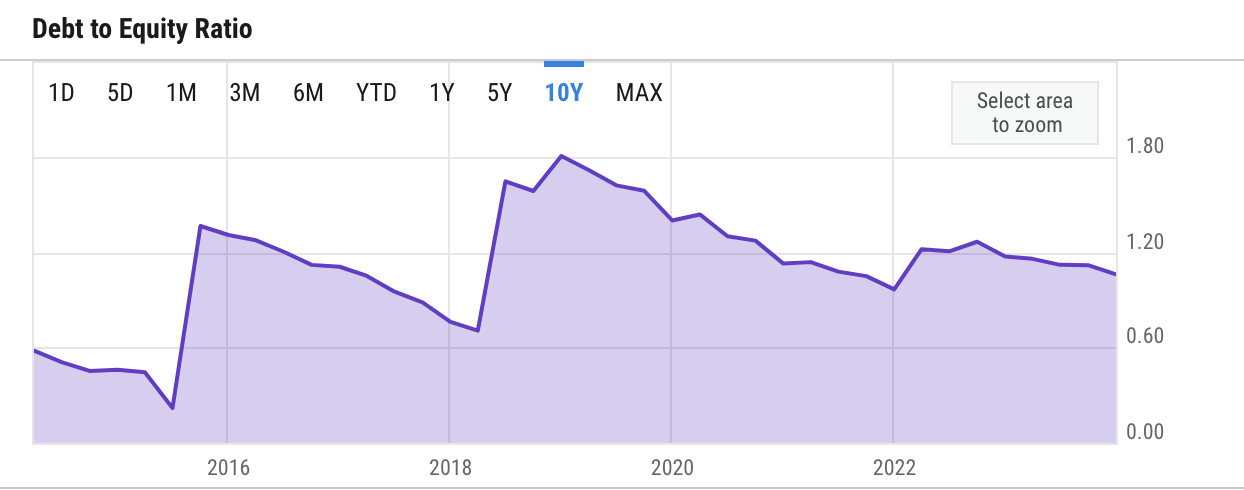

DE ratio (ycharts)

Given its decades of experience in levered M&A deals, SSNC has also been very disciplined in managing its debt level. Debt-to-equity / DE ratio rarely steps outside a certain range.

key metrics (ycharts)

Overall, Liquidity has been solid. Cash and short-term investments stood at over $400 million as of Q4 2023. It also remains elevated today compared to a few years ago, when it was hovering between $100 million - $200 million. Aside from M&A activities, another significant use of cash would be for dividend payments. SSNC has consistently been growing its dividend per share / DPS. In the last fiscal year, FY 2023, DPS was $0.88, doubled from 3 years ago.

I believe there are some catalysts that should help SSNC improve its revenue growth and expand its margins in 2024 and beyond.

In my opinion, SSNC is strategically positioned to benefit from a confluence of trends driving operational cost optimization across fund administration, primarily driven by margin pressure due to increased inflation, broader weak portfolio performance, and higher regulatory scrutiny.

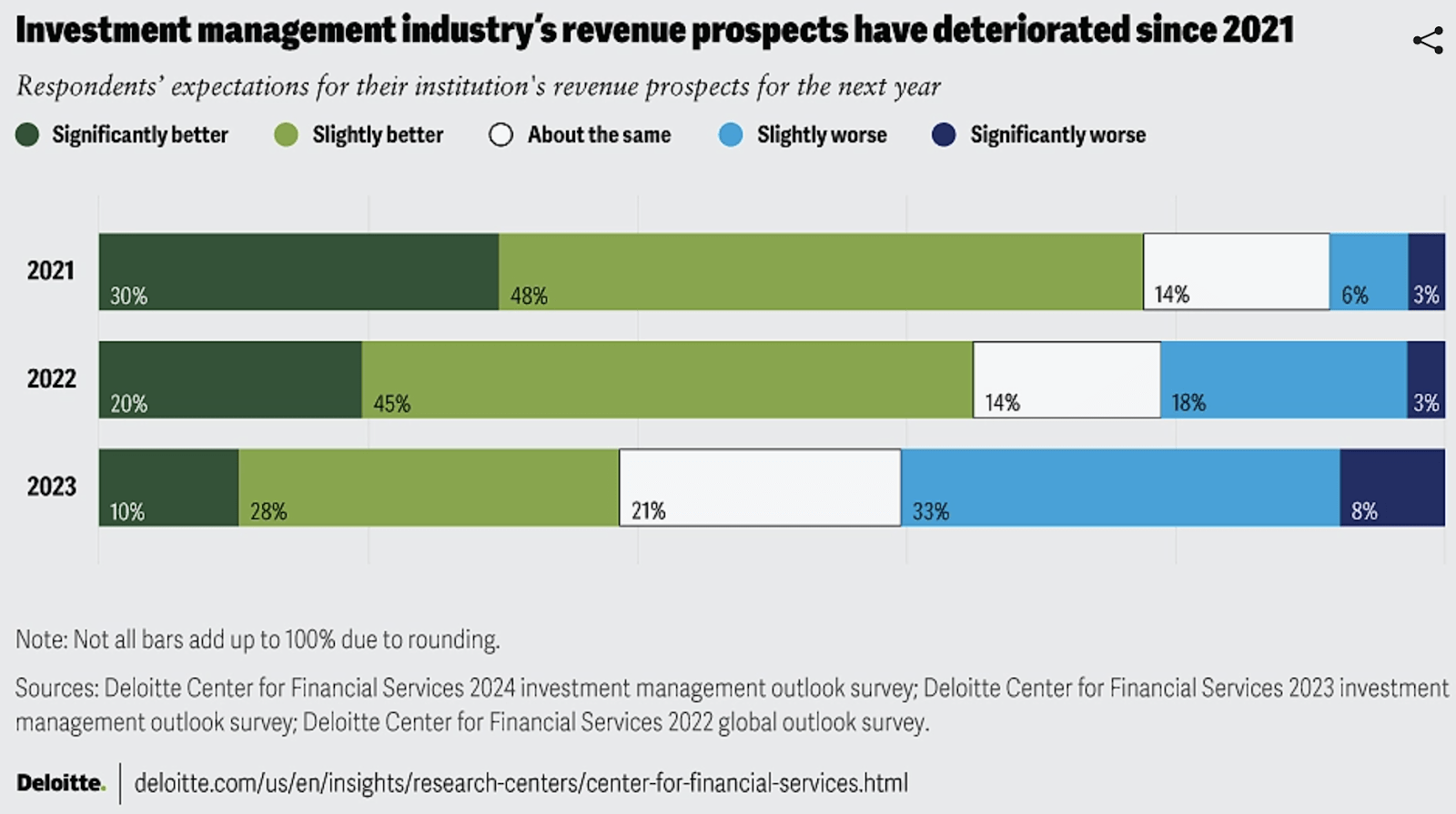

lower revenue expectation in 2024 (deloitte)

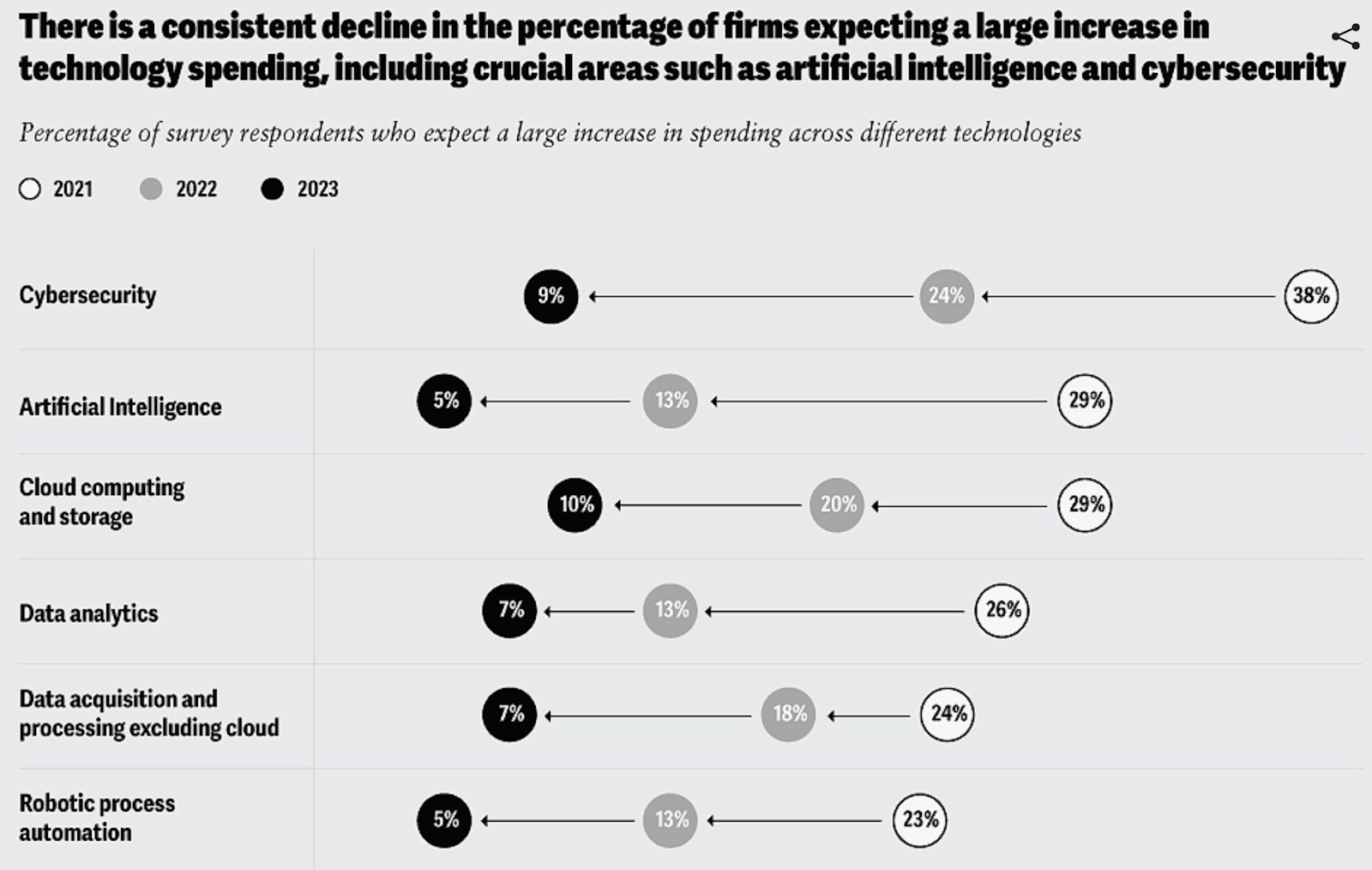

Based on a survey from Deloitte, we may continue to see declining revenue prospects in the financial services industry in 2024, implying that margin pressure may persist. This should drive demand for SSNC’s comprehensive solution, which could help drive costs down by potentially consolidating a few solutions across the front, middle, and back offices, into a single platform. In Q4 earnings call, the management’s comment also aligns with our findings:

We're seeing a lot of opportunities across the financial services industry as large firms look for ways to drive down costs within their back office operations while improving their front end technology. These market dynamics can be beneficial for our GIDS, Retirement and Alternative Fund Services businesses. Across the company, we have focused on offering comprehensive solutions to our customers comprised of multiple products and services in an integrated and holistic way.

Source: Q4 earnings call.

revenue breakdown (SSNC presentation)

In my view, the trend would also help drive revenue growth in a meaningful way, due to its positive impact on SSNC's key businesses. SSNC derives most of its revenues from Alternatives, Advent, and GIDS businesses, which provide fund management and transfer agent solutions for fund-of-funds, private equity, and other investment management firms across front-to-back offices. With over $2.8 billion of revenue, these segments alone make up over half of SSNC’s business.

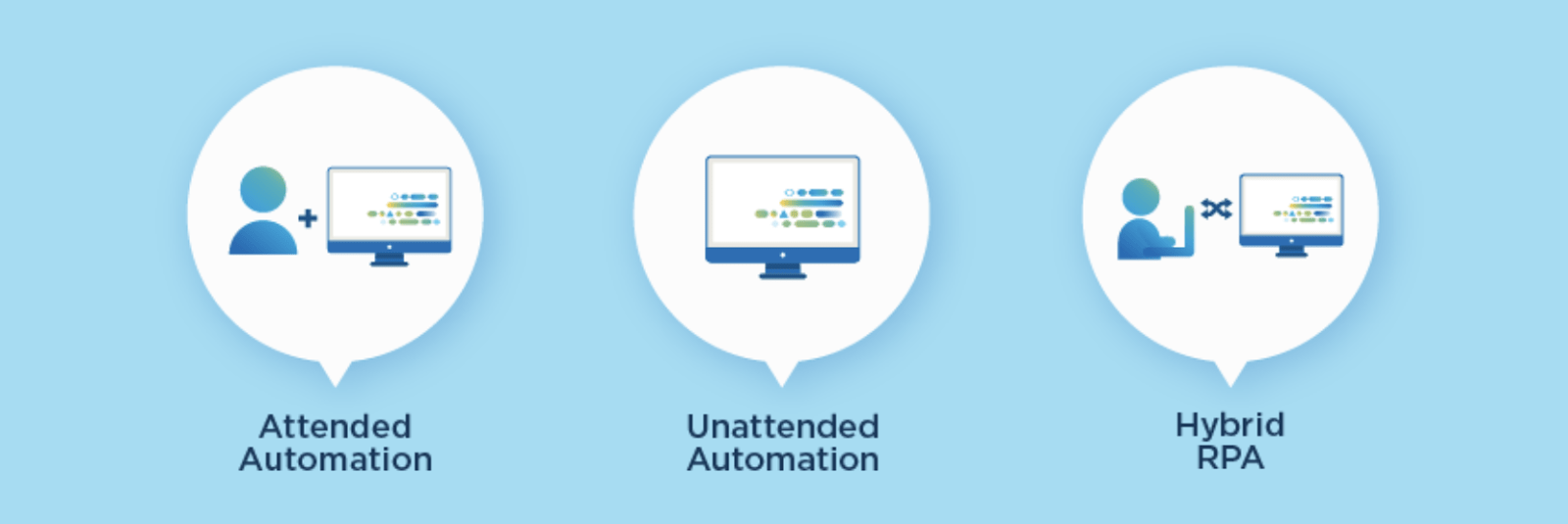

Furthermore, the increased demand for cost optimization would also benefit Blue Prism, one of the latest SSNC acquisitions. Blue Prism has been the second-fastest growing business for SSNC, and at just over $200 million of revenue, I believe there is plenty of room to grow.

So far, SSNC has also helped Blue Prism to realize potential margin expansion. Their digital workforce initiative, spearheaded by Blue Prism's robotic process automation (RPA), is expected to yield $100 million in annual savings through better cost efficiencies:

For the year, we obtained approximately 2,000 full-time equivalents in digital worker productivity, which we expect to yield $100 million savings annually. We are optimistic about our ability to continue to drive additional benefit from digital workers and other automation strategies.

Source: Q4 earnings call.

RPA segments (SSNC)

Given the early days of implementation, I would expect further fine-tuning around Blue Prism’s solution to unlock a stronger productivity outlook. The successful internal implementation could also provide SSNC with a convincing ROI-driven case study to attract customers for Blue Prism. For instance, the positive implementation track record may manifest in higher inbound demand or shorter sales cycles.

Risk remains minimal, in my opinion, though there are several points worth noting regarding Blue Prism’s prospects. Despite the early promise, overreliance on automation may lead to technical challenges that limit the effectiveness of complex tasks. As such, I am of the view that there is a ceiling for RPA implementations in any organization.

Furthermore, integrating and scaling RPA can be complex and require significant upfront investment and change management. Overall, this increases the risk of facing unexpected challenges that could delay cost savings and impact client satisfaction.

decline in % of firms to spend on tech in 2024 (deloitte)

Moreover, there is a possibility for lower demand for less mission-critical solutions within the financial services sector today. The persisting margin pressure in investment management businesses in 2024 could make more firms more selective when adopting new technology solutions, including RPA. Despite the promise of increased productivity, RPA remains unproven and less mission-critical next to the end-to-end fund administration solutions offered by SSNC.

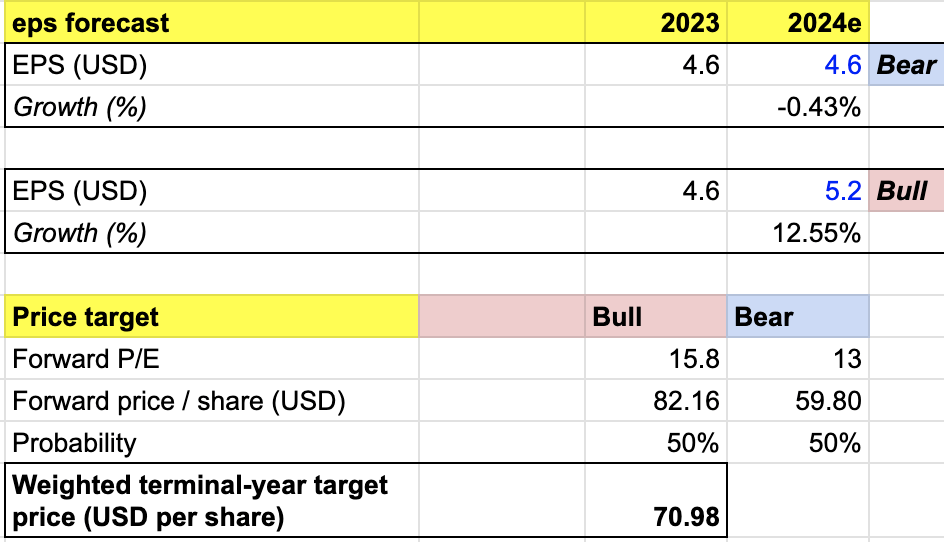

My target price for TRVG is driven by the following assumptions for the bull vs bear scenarios of the FY 2024 projection:

Bull scenario (50% probability) assumptions - SSNC to achieve FY 2024 EPS of $5.2, a 12.55% growth, near the highest end of SSNC’s estimate. This would suggest a significant improvement in EPS, which has been stagnant in recent times. With this outlook, I would expect SSNC to trade at a forward P/E of 15.8, taking the stock to $82, near its 5-year high.

Bear scenario (50% probability) assumptions - SSNC to deliver FY 2024 EPS of $4.6, significantly lower than SSNC’s low-end estimate. I assign SSNC a 13x forward P/E, implying a potential correction as SSNC continues to see a decline or flat FY EPS growth.

price target (own analysis)

Consolidating all the information above into my model, I arrived at an FY 2024 weighted target price of $71 per share, suggesting an 11% upside from the current price level. I rate the stock a buy.

Despite market turbulence, SSNC presents compelling long-term potential. Tailwinds like cost pressures in fund administration due to inflation, performance, and regulation fuel demand for their services. While early successes with Blue Prism are promising, potential implementation hurdles and limited effectiveness for complex tasks suggest a ceiling for its impact. My $71 1-year target price and buy rating reflect optimism for SSNC's ability to navigate risks and capitalize on growth opportunities.