bjdlzx

bjdlzx

As I approach my retirement years now that I have turned 65 and officially retired from my full-time 40-year career as an information systems manager, I have sort of switched careers and am now managing my investments. My personal portfolio is held mostly in an IRA (currently in two different accounts, with Schwab and Fidelity) and I tend to reinvest most of my distributions to grow my portfolio and future income stream. I refer to my portfolio as my Income Compounder and I provided an update that includes a spreadsheet that lists all 50 holdings in an article published a couple of weeks ago that you can read here.

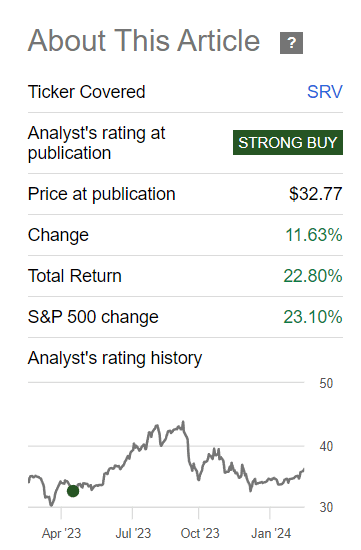

One of the asset classes that I hold in my IC portfolio is midstream energy. In this article, I would like to share my thoughts on investing in that asset class in 2024 and beyond, and why it makes sense for income investors to consider adding some midstream energy assets to their own portfolios. In fact, one of my core holdings in my IC portfolio is the NXG Cushing Midstream Energy fund (NYSE:SRV), which I first reviewed in April 2023 when I rated it a Strong Buy. Now, almost a year later, that fund has delivered a total return of nearly 23%, and I still rate the fund a Buy (downgraded from Strong Buy only because the discount has closed) for income investors who seek a high yield income investment with some potential for capital appreciation.

Seeking Alpha

The SRV closed end fund is just one fund that holds midstream assets and there are others to consider as well that I will also briefly review and compare including KYN, TTP, and EMO. But before I get into the funds, let’s review the current and future outlook for the midstream energy sector.

The energy sector went through some volatility in 2023 and struggled to keep pace with the broader market after delivering the best performance of any equity sector in 2022. However, the midstream energy sub-sector driven by MLPs and pipeline companies provided a bright spot for the industry as explained in this article from ETF Trends in December.

Midstream or energy infrastructure encompasses a subset of the energy sector that handles the transportation, processing, and storage of energy products. Services are largely provided under long-term, fee-based contracts. These fee-based business models result in more stable cash flows regardless of the commodity price environment. This results in more defensive energy exposure. Midstream also offers more generous yields than broader energy, which contributes to differences in total return.

With weaker oil and natural gas prices this year, midstream has handily outperformed broader energy thus far in 2023. The Alerian Midstream Energy Index (AMNA), the broad North American benchmark for energy infrastructure companies, has gained 13.0%. The S&P Energy Select Sector Index (IXE) was down 0.2% on a total-return basis as of December 18.

In previous years, the midstream sector was very capital intensive and relied on high leverage and capital spending that far exceeded the cash flow generation of the assets. In more recent years, there has been a transformation to more disciplined capital expenditures that are mostly internally financed and have led to more robust cash flow generation. Those cash flows are largely uncorrelated to larger market forces such as commodity prices, macroeconomic issues (i.e. interest rates, inflation), or higher valuations.

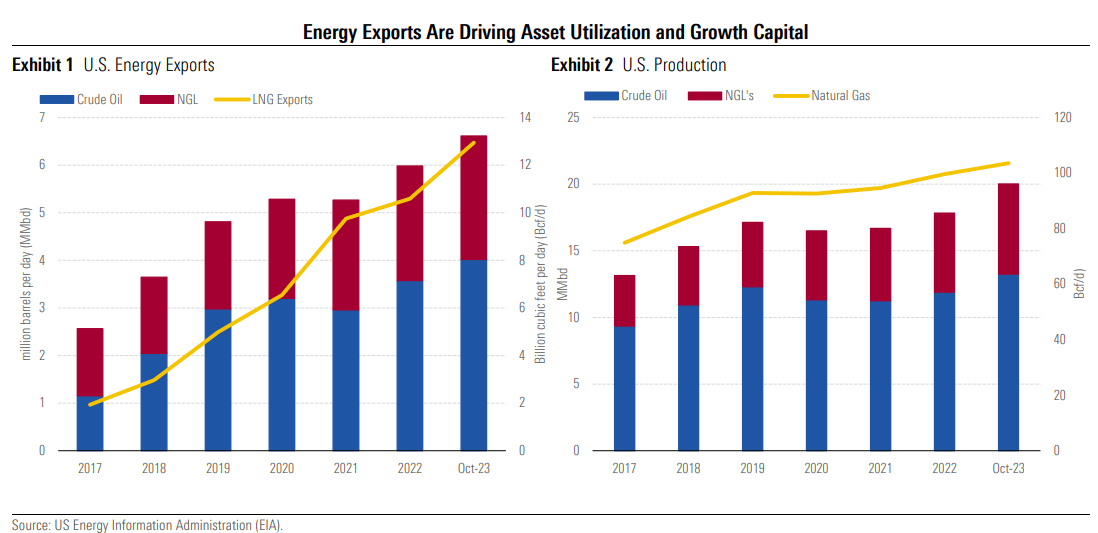

In 2024, energy exports are driving much of the asset utilization and growth capital in North America, as explained in this recent article from Morningstar DBRS.

Morningstar DBRS

Asset utilization levels in North America were quite robust in 2023 as oil and gas production reached record highs in 2023, primarily driven by an increase in energy exports. The United States has emerged as a key energy supplier to Europe post Russia's invasion of Ukraine. While production is starting to moderate on the back of softening global demand, we expect asset utilization in the Sector in 2024 to remain high. Crude oil production in North America has benefitted from wells drilled in 2022 when prices were higher and could moderate in 2024.

The period of persistent underinvestment in the oil and gas industry in the past few years is likely to lead to a prolonged period of higher commodity prices and higher capital returns for the energy sector over the next few years. For 2024 some of the tailwinds that are driving higher asset utilization in North America especially, are likely to continue to lead to strong growth and financial stability in the midstream sector as further explained by Morningstar DBRS:

Consequently, we expect asset utilization in the Sector to remain strong as rising energy exports drive up oil and gas production in North America. Additional tailwinds include consolidation among oil and gas producers, which should improve counterparty risk profiles, stabilizing interest rates and moderating inflation.

A recent example of the consolidation among oil and gas producers included this week’s news that Enterprise Products Partners (EPD) is buying the Texas assets of Western Midstream Partners (WES).

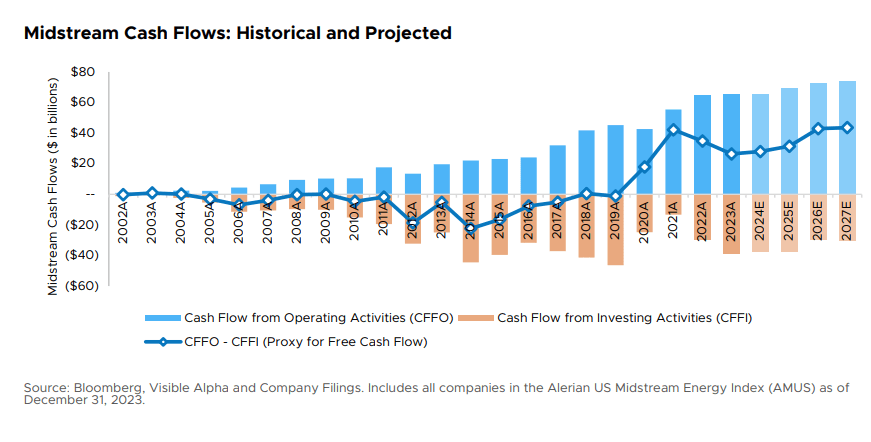

After I published my article on SRV last year, I spoke to NXG Cushing Portfolio Manager John Musgrave who recently shared with me an update on the midstream energy sector in 2024. In the document that he shared with me, there is a discussion on the benefits of free cash flow based on a case study that examined the ten largest US midstream companies by market cap. The discussion explains how a shift has occurred in the past few years in terms of free cash flows with the past three years in particular producing positive FCF generation, a trend that is likely to continue in the years ahead.

NXG Cushing

Historically, the CFFO (cash flows from operations) was insufficient to cover capital expenditures and dividends paid by midstream and MLP companies. Funding from multiple external funding sources such as debt offerings and equity issuances, in addition to CFFO, were required to cover the expenses. But now, with at least three years of positive FCF generation, that spending regime has shifted to more internal funding. That shift has dramatically changed the funding mechanisms, nearly eliminating completely the need for debt and equity offerings. Now, midstream management teams are more strategically directing excess cash flows toward reducing debt and implementing buyback programs, in addition to paying generous dividends or distributions.

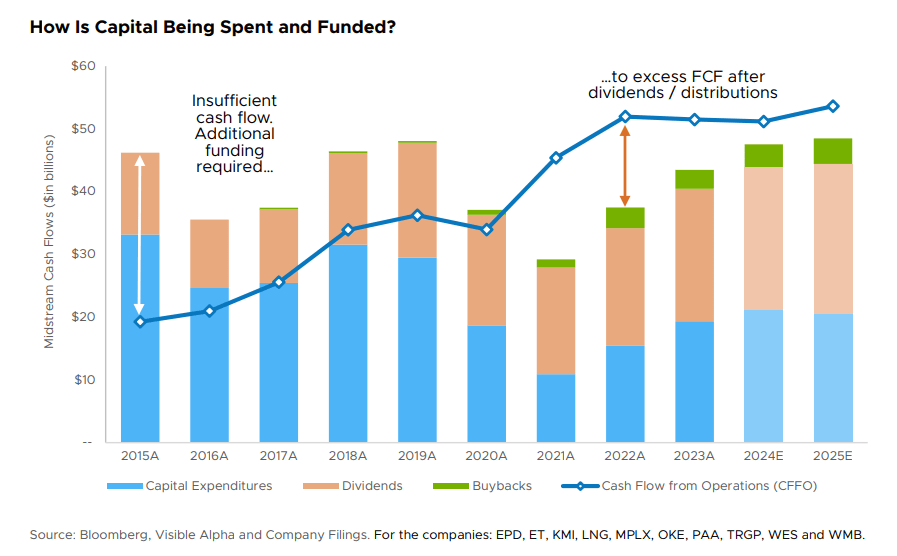

The chart included in the document that he sent me graphically illustrates this change in how capital from free cash flows is being allocated.

NXG Cushing

The current strength of company balance sheets in the midstream sector combined with this trend of increasing positive FCF should enable those companies to increase shareholder returns though dividend/distribution growth and share buybacks along with potential protection against downside volatility resulting from market fluctuations.

When I first covered the SRV fund back in April 2023 it was paying a generous distribution of $0.45 per share monthly, which amounted to an annual yield of about 16% at the time. At that time, the discount to NAV was about -12%. As of today, February 22, 2024, the fund still pays the same monthly distribution, but the discount has closed to -3.5%. The fund has declared those monthly distributions through at least May of this year, resulting in a forward annual yield of about 15% at the current market price.

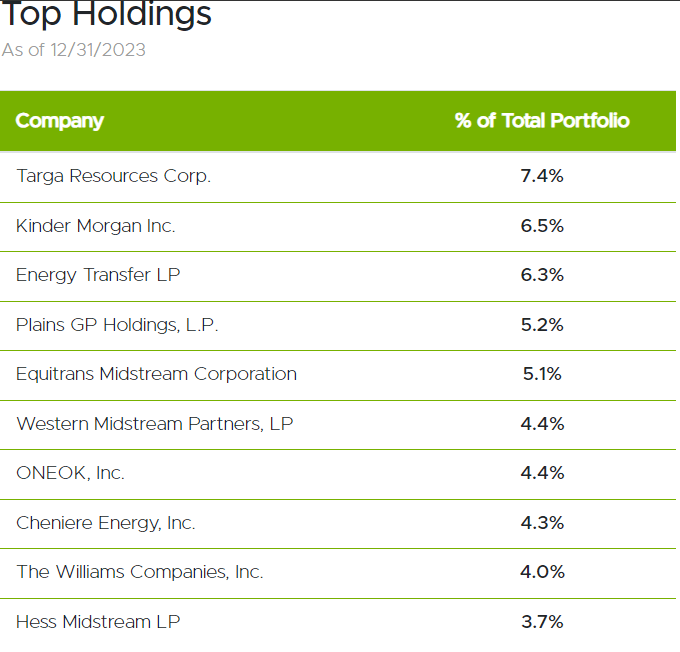

The fund’s top holdings are all top performers in the midstream sector and the top 10 make up about 60% of the total portfolio holdings, which include about $110M in AUM as of 12/31/23.

SRV top holdings (NXG Cushing)

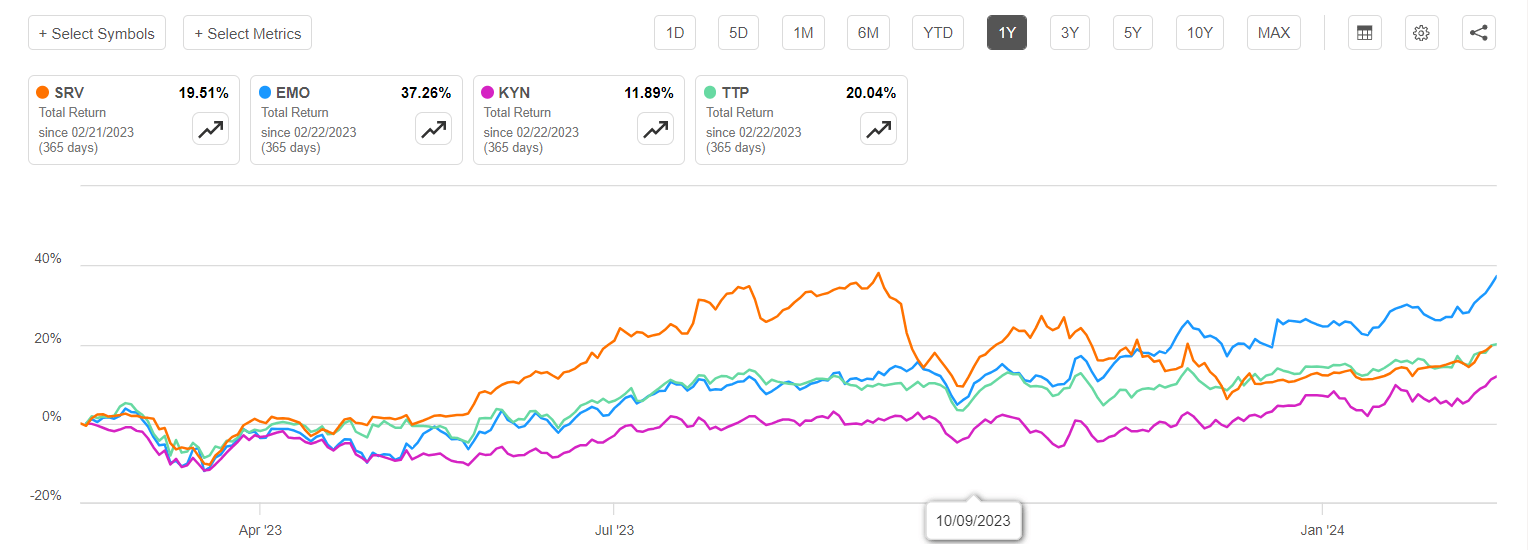

Investors in MLP and midstream companies may be more familiar with other CEFs that invest in the midstream sector, and in my previous article I included a comparison with three peer funds: KYN, TTP, and EMO. In the past year, which is roughly the time since I last covered SRV, the total return of all 4 funds has been comparable with EMO now in the lead for highest total return, however, SRV offers the highest distribution yield (by far).

Seeking Alpha

As an income investor, I am more interested in the income generated from my assets with capital appreciation being a secondary concern, so that is why I chose SRV for my midstream funds. But the other funds are good choices too, depending on your investment goals and objectives. All the midstream funds are likely to benefit from the increasing FCF generation that I discussed above, so if you do not already own a midstream fund (or stock) in your income portfolio, you may want to consider adding SRV.

As I was composing this article, I received an email from NXG Cushing announcing that the Annual Report for the fund is now available. In the Shareholder Letter section of the report, which is dated November 30, 2023, a summary of reasons why midstream is a good investment now is provided:

While the potential of a recession and high interest rates present concerns, we anticipate that the sustained discipline of producers alongside supportive OPEC+ actions should provide support for oil prices. As a result, we anticipate an extended phase of elevated commodity prices as the underinvestment in oil and gas becomes increasingly evident. The mix of reduced capital spending and rising commodity prices should result in significant FCF generation, enhancing investment returns in the energy sector.

With market-leading FCF yields and a strong focus on shareholder returns, we assert that the midstream sector is consistently undervalued and mispriced. High dividend yields, consistent dividend growth, stock buybacks, and debt reduction should serve as catalysts boosting market sentiment and nudging investors to acknowledge the inherent value within the midstream energy sector.

I rate SRV a Buy at the current price of $36.58, which is a slight discount to the NAV, which is $37.44 as of 2/21/24. The discount is closing, and the fund may soon begin to trade at a premium as more investors realize the potential to capture a high yield distribution from this well managed CEF that has potential protection from downside volatility due to its uncorrelated market returns.