FOTOKITA/iStock via Getty Images

FOTOKITA/iStock via Getty Images

This article was coproduced with Leo Nelissen.

Does anyone remember the Scottish pop rock band Pilot?

I do.

Of course, I was in third grade when their famous song, Magic, debuted and reached number five during the summer of 1975 in the U.S. on the Billboard Hot 100.

I'm sure you know the lyrics, "Oh, ho, ho, it's magic, you know."

I have the song in my iTunes folder, and every time I hear the music I'm reminded of my favorite real estate investment trust, or REIT, known for its one-letter ticker: O.

O, O, O It's Magic You Know

What's so magical about this net lease REIT?

After a strong ending of 2023, real estate is in a tough spot again, with the Vanguard Real Estate Index Fund ETF Shares (VNQ) dropping 4.2% year-to-date, underperforming the S&P 500 (SP500) by almost 9 points!

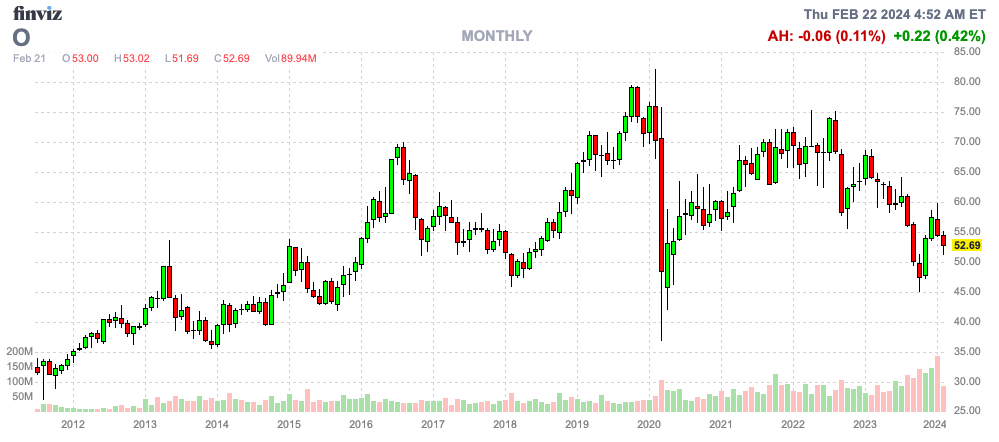

One of the victims is Realty Income Corporation (NYSE:O), the King of net lease real estate.

Down 8% year-to-date, the giant is trading more than 20% below its 52-week high and 33% under its all-time high in 2019.

Finviz

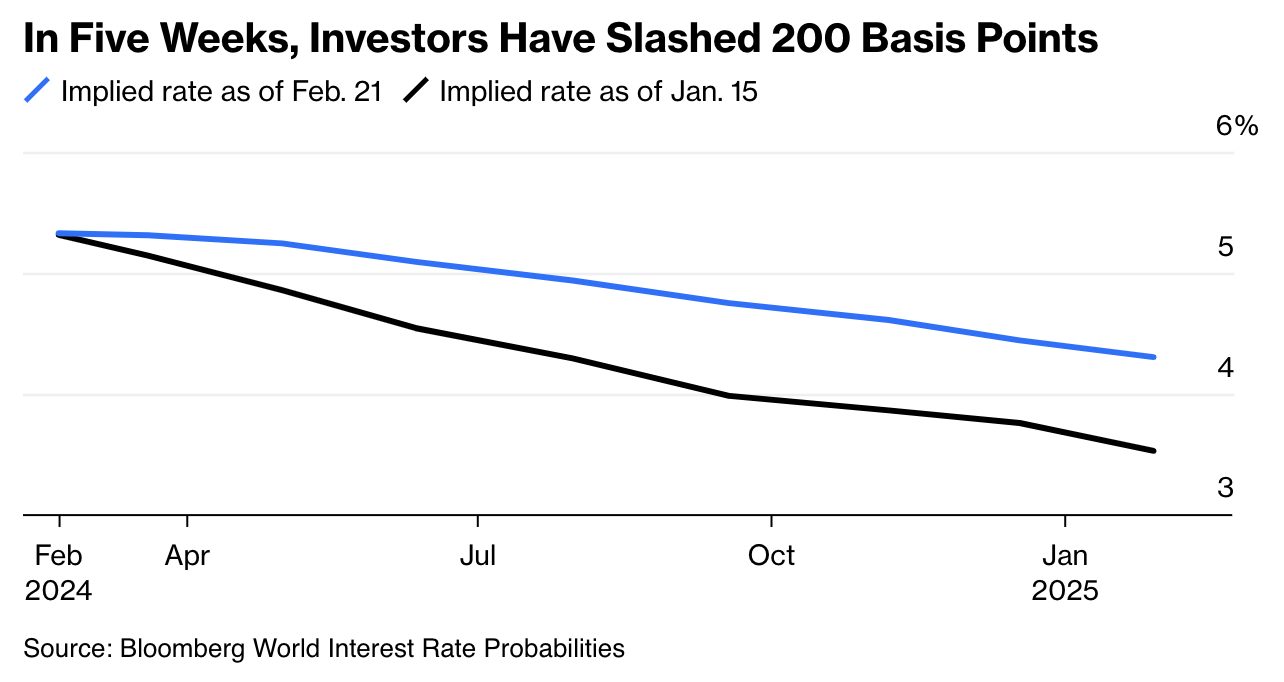

Recent weakness is caused by developments we have discussed since mid-2023: the fact that inflation is sticky and rates should be expected to remain higher for longer.

Last year’s Santa rally was caused by the market becoming very dovish. However, as John Authers writes for Bloomberg, the Federal Reserve's anticipated rate cuts in 2024 have been revised downwards amidst evolving economic data.

Originally projected to decrease rates seven times by 2025, recent adjustments indicate a more moderate expectation of around four cuts, reflecting the Fed's cautious approach amid inflation concerns.

Bloomberg

REITs, who prefer low rates and low inflation, dislike this development.

Essentially, market sentiment suggests a falling likelihood of a rate cut in March, with May being the earliest possibility - albeit with only a 30% probability.

While these developments may be unfavorable for investors looking to make a quick buck in real estate or other areas that are sensitive to interest rates, it is fantastic news for conservative long-term investors looking to buy the market’s best stocks at great prices – and isn't that what long-term investing is all about?

Contrarian investing may not always feel right, but it sure is the best way to make money.

This brings us to Realty Income, the star of this article.

The company, which enjoys frequent coverage on our Investing Group, just released its Q4 quarterly earnings, which allows us to take a very close look at the company.

As the title of this article may suggest, we really liked what we saw. Not only is the stock price offering us a chance to buy Realty Income at a discount, but it also comes with a super resilient business model, merger tailwinds, secular industry growth opportunities, and much more.

So, let’s dive into the details!

Despite economic headwinds like elevated rates and sticky inflation, Realty Income achieved significant milestones.

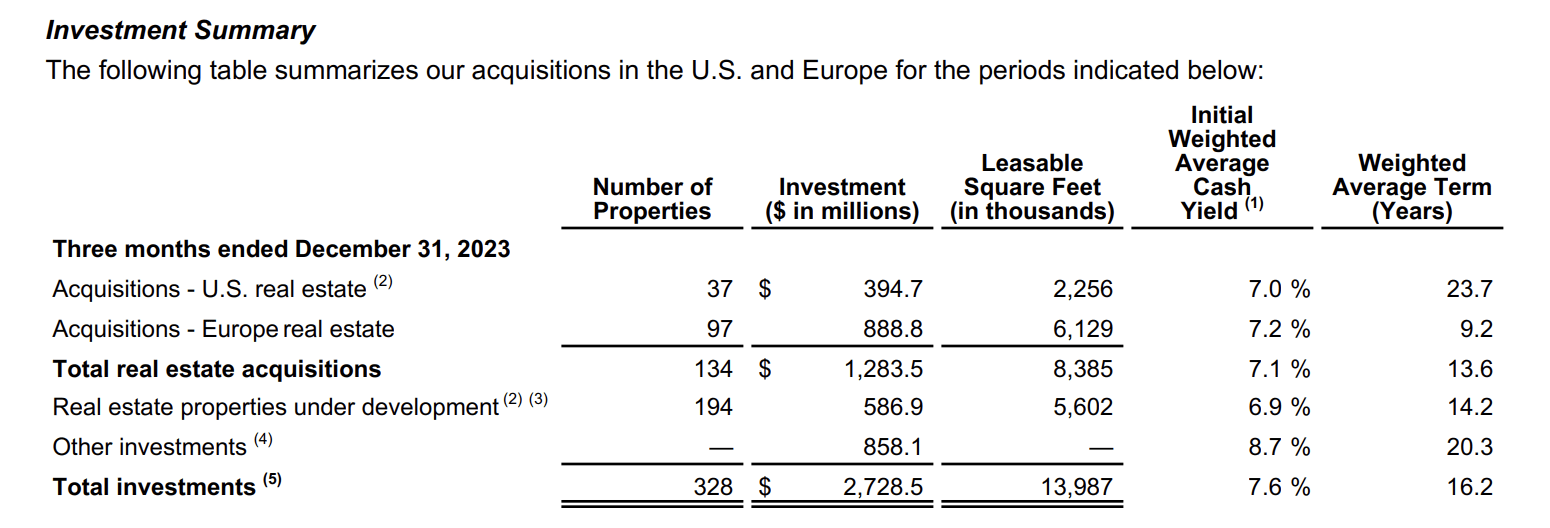

The company closed over $9.5 billion in property-level investments across eight different countries through 271 transactions, marking a record-high annual investment volume.

Notably, the fourth quarter witnessed $2.7 billion in investments, which shows that the company isn’t shying away from potential risks tied to an environment of elevated funding costs.

On top of that, as we can see below, the weighted average lease term of these deals was 16.2 years, which creates long-term visibility and lowers occupancy risks.

Realty Income

Furthermore, these investments were made at an attractive weighted average cash yield of 7.6%, indicating the company's ability to secure good deals when others are struggling.

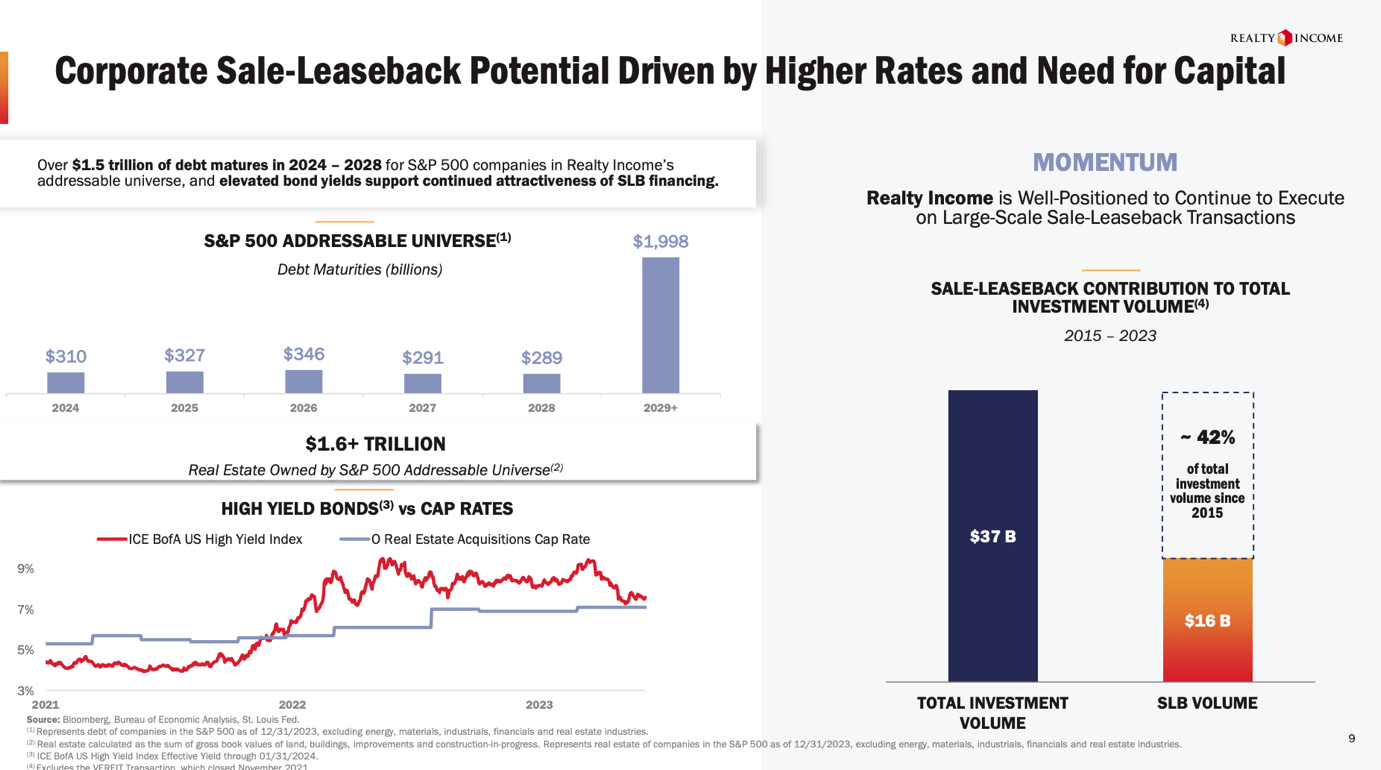

Key transactions included a multimillion-dollar sale-leaseback (“SLB”) agreement with Decathlon, a prominent sporting goods retailer in Europe.

Realty Income

This sale-leaseback deal is a fantastic example of Realty Income using its competitive edge to generate value in a tough market.

Essentially, an SLB deal is a transaction where a company in need of funding sells its building to Realty Income. A lot of retailers use this strategy, as it frees up cash for expansion and other purposes.

It is somewhat comparable to a loan, as selling the building frees up a lot of cash in exchange for regular rent payments.

Especially in an environment where credit conditions are tight for most companies, SLB offers opportunities that Realty Income can exploit.

Realty Income

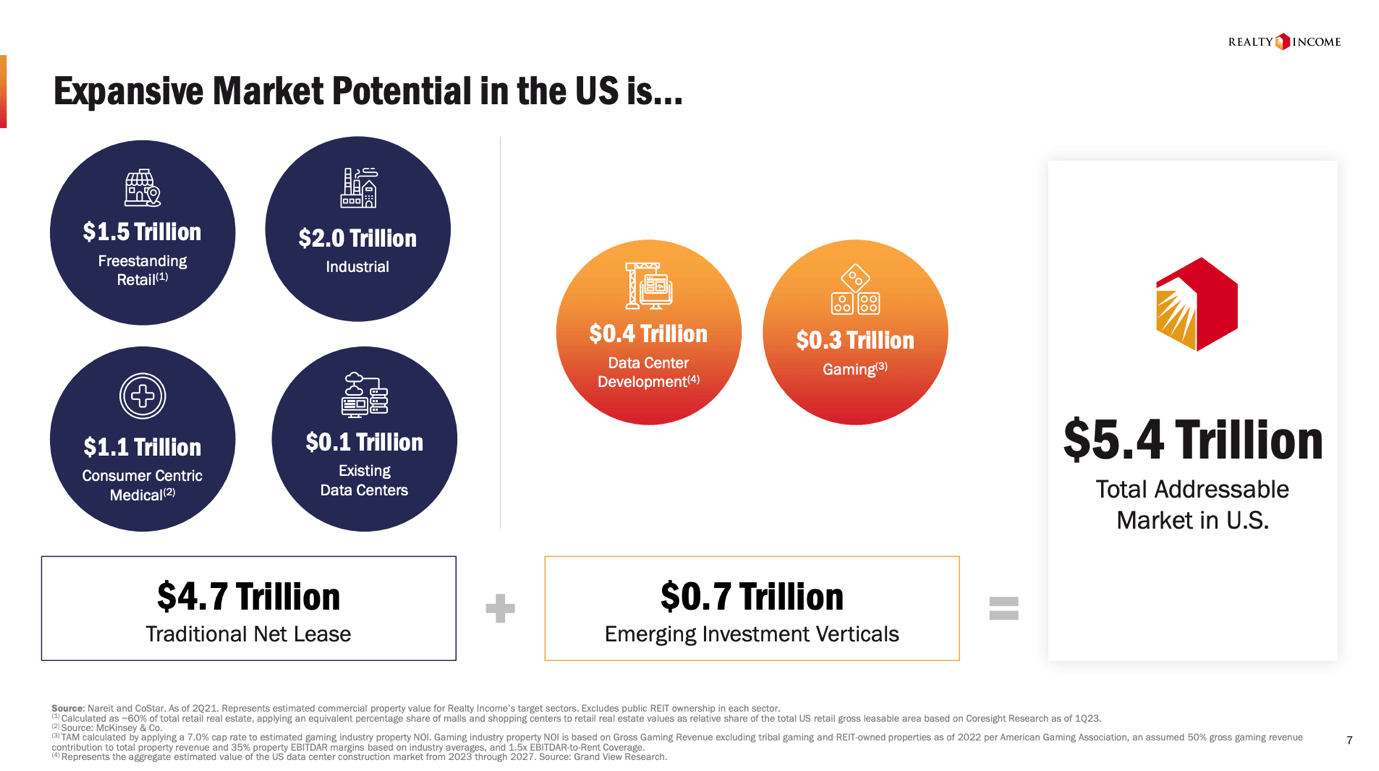

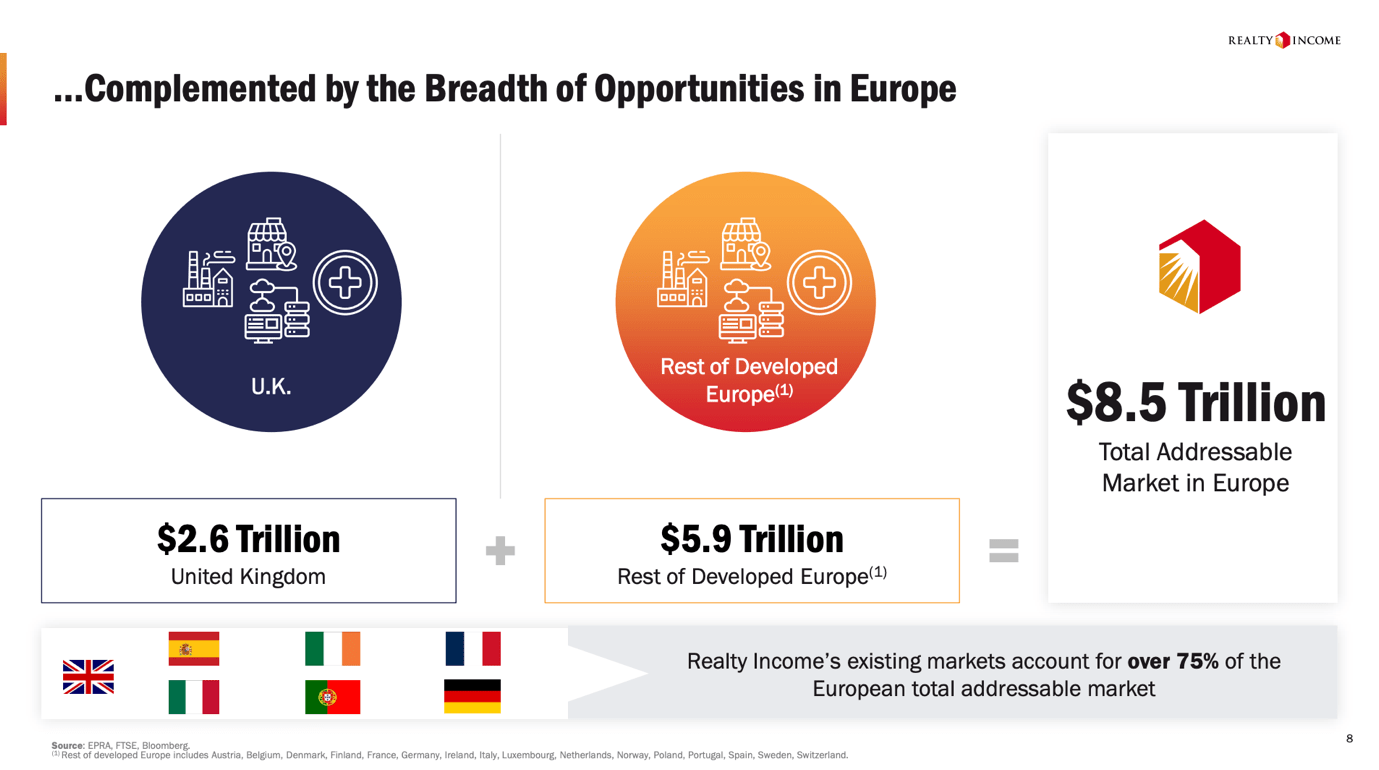

Even better, during its Q4 earnings call, the company explained that it recognizes the vast potential in consolidating the fragmented net lease real estate market, estimating a total addressable market of $14 trillion across the U.S. and Europe!

This includes $5.4 trillion worth of opportunities in the U.S…

Realty Income

… and $8.5 trillion of opportunities in Europe.

Realty Income

Given these favorable opportunities, the company's strategic initiatives, including partnerships with industry giants like Blackstone (BX) and investments in emerging sectors such as data centers, reflect its proactive approach to capitalizing on market trends.

Furthermore, the recent merger with Spirit Realty Capital (SRC) enhances the company's access to capital markets, enabling efficient funding through increased trading volume and the ATM equity program.

Realty Income

In the fourth quarter, Realty Income allocated roughly $2.7 billion to high-quality investments, with a significant portion derived internationally.

Key investments included a loan to Asda in the U.K. and a preferred equity investment in the Bellagio joint venture with Blackstone.

The company also initiated a data center development joint venture with Digital Realty (DLR), signaling its interest in emerging sectors with promising growth potential.

Furthermore, and with regard to economic headwinds, despite a slight decline in occupancy to 98.6% at year-end, Realty Income achieved same-store rent growth of 2.6% in the fourth quarter and 1.9% for the year.

In light of these developments, Realty Income's recent merger with Spirit Realty Capital and subsequent capital-raising activities position the company for robust growth in 2024.

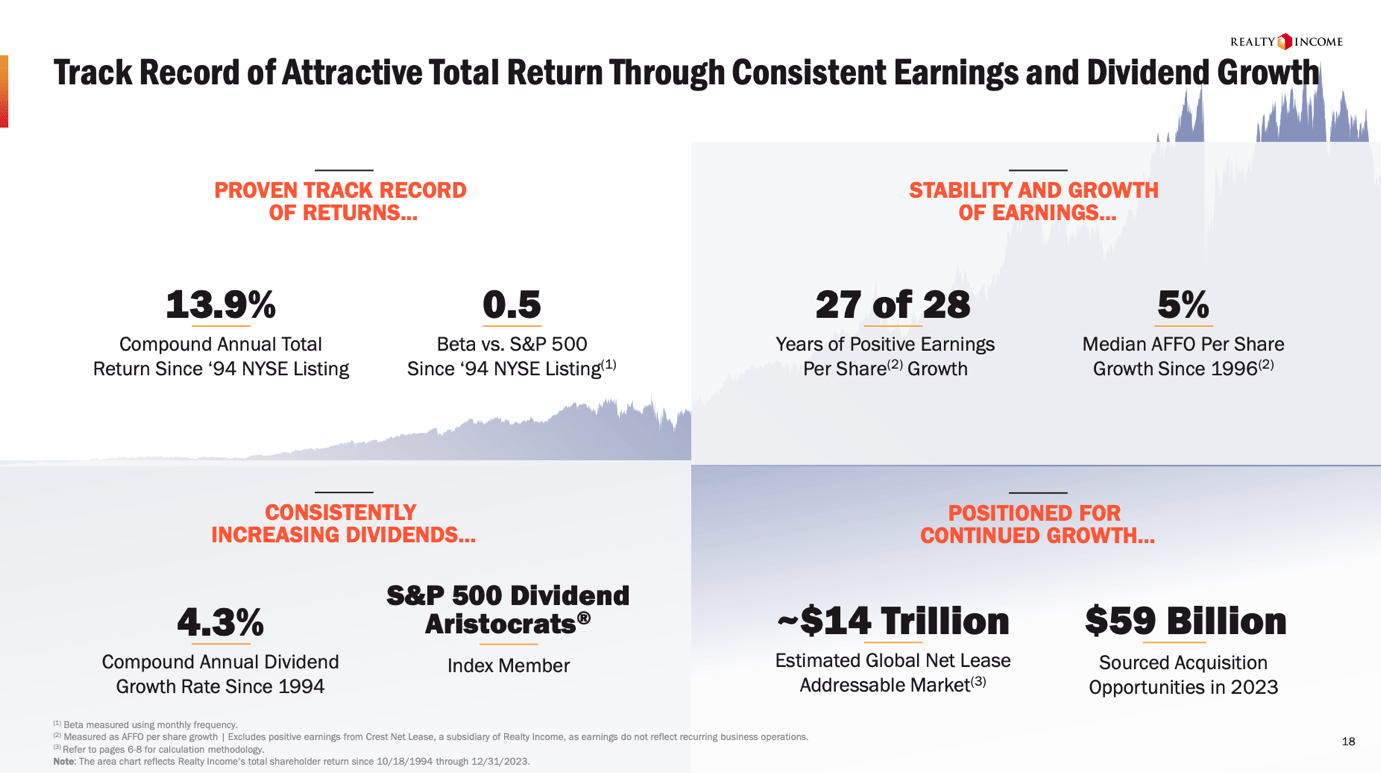

Management has provided forward-looking guidance, forecasting an AFFO (adjusted funds from operations) per share growth rate of 4.3% in 2024 without the need for additional public equity!

Since 2013, the company has generated annual AFFO per share growth in the low-5% range.

Realty Income

Furthermore:

Additionally, the company anticipates approximately $2 billion in acquisitions for 2024, to be funded through internally generated cash flow, ATM proceeds, and available credit facilities, which is fantastic news for its already strong balance sheet and per-share value of the business.

This is what Mizuho Securities wrote after the earnings release (emphasis added):

“Importantly, the 4.3% growth forecast takes into consideration only $2B of incremental acquisitions, more than 70% lower than O's FY23 acquisition volume, and requires NO incremental capital raising, which is especially noteworthy at a time when interest rates are volatile and capital is scarce/expensive.”

We also believe these projections perfectly underscore Realty Income's ability to capitalize on future opportunities while maintaining a disciplined approach to capital deployment.

In addition to raising $1.6 billion worth of equity in 4Q23, the company used the debt market for funding and to adjust its balance sheet.

In a strategic move to manage its debt capital, the company executed bond issuance activities totaling approximately $2.2 billion.

These activities were aimed at de-risking the company's 2024 maturity schedule.

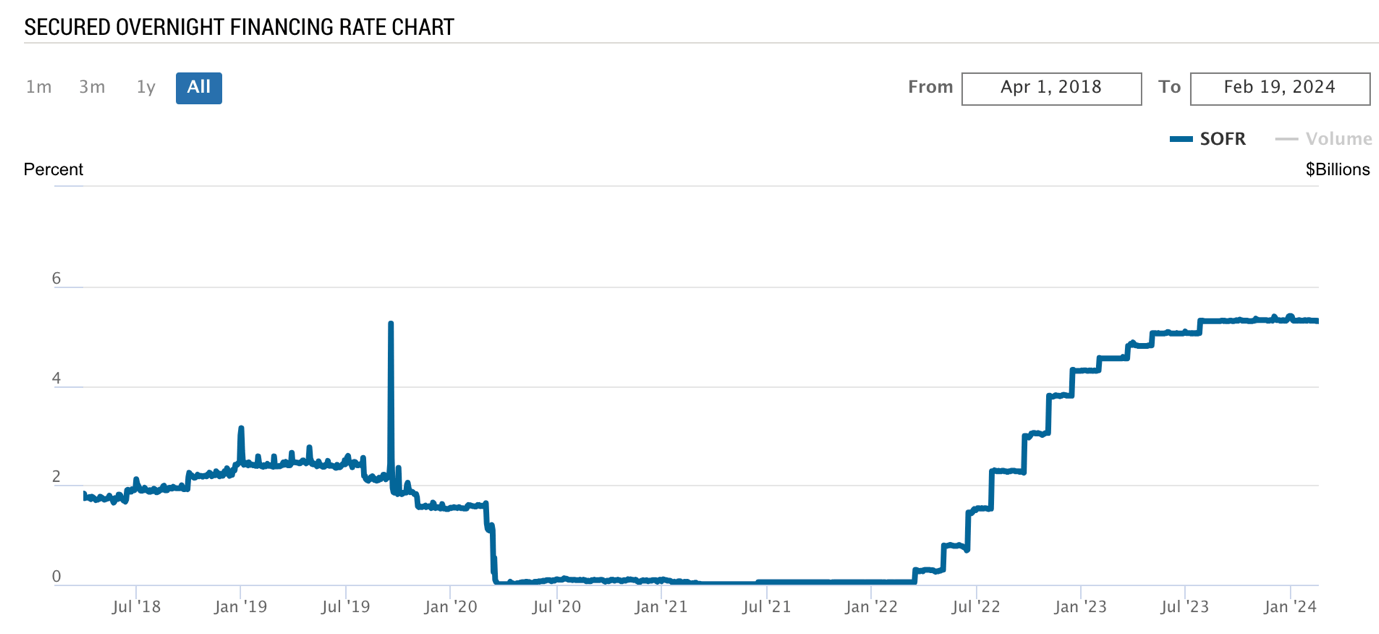

The bond issuances resulted in offerings with attractive terms, including a weighted average duration of approximately 10.2 years and a weighted average yield to maturity of roughly 5.5%, which is extremely attractive in an environment where SOFR rates are currently at 5.3% - up from roughly 0% before 2022.

Federal Reserve Bank of New York

This approach allows the company to fund its business operations without the necessity of tapping into the debt capital markets throughout the year.

Furthermore, the strategy aims to maintain investor diversification across multicurrency debt and mitigate future debt repayment risks.

In addition to bond issuance activities, the company took steps to manage its existing debt.

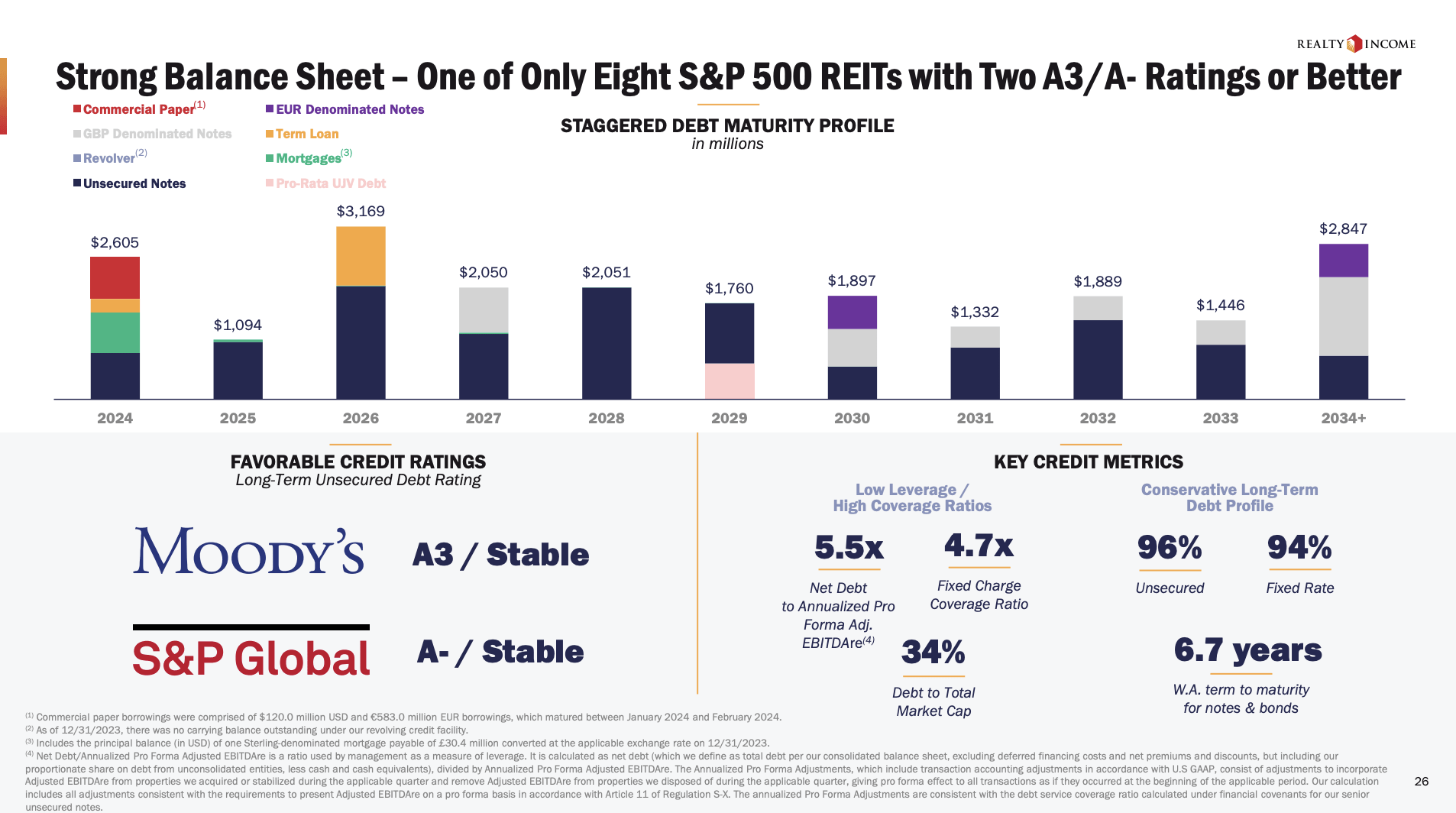

All things considered, the company ended the year with a net debt ratio of 5.5x (EBITDAre) and a weighted average term to maturity of 6.7 years.

On top of that, 94% of its debt has a fixed rate, and 96% of its debt is unsecured.

It also maintains an A- credit rating, one of the best ratings across all industries, not just real estate.

Realty Income

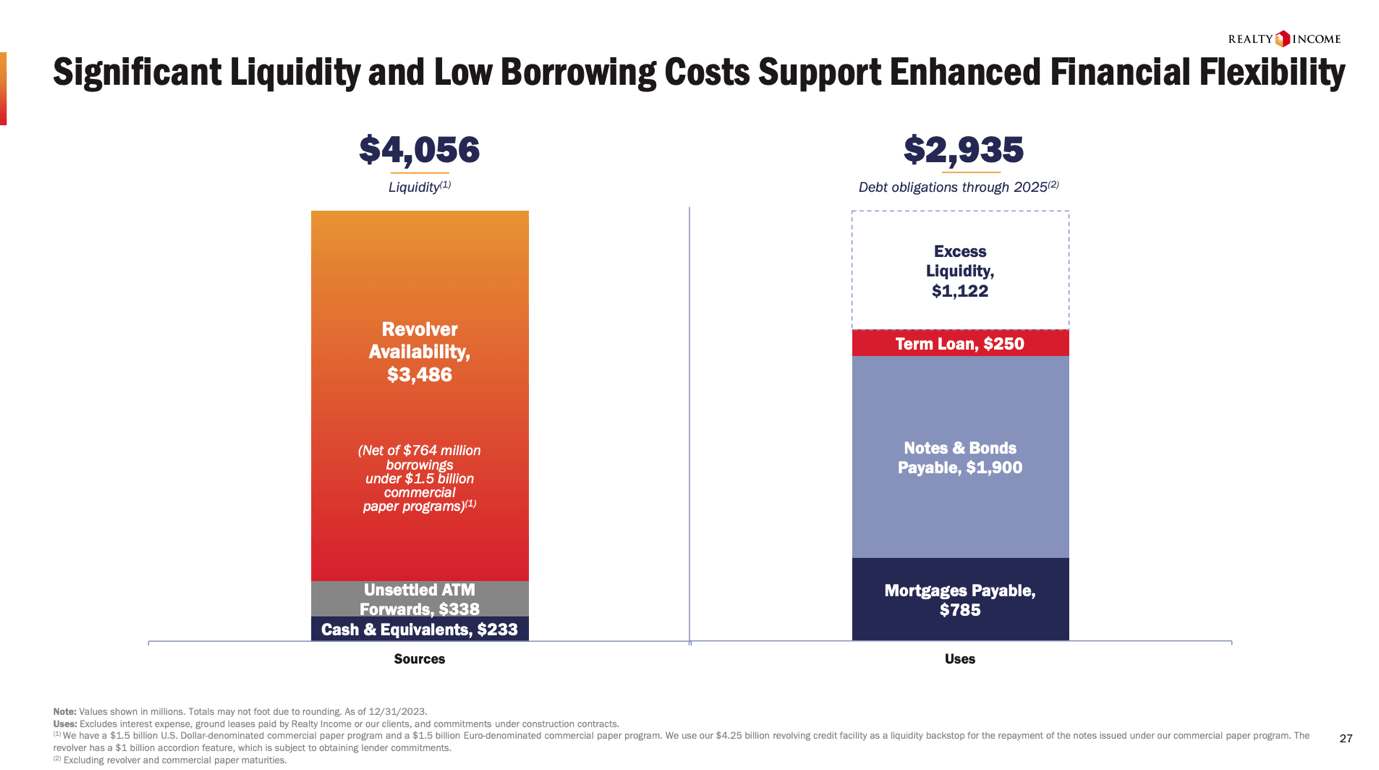

Moreover, and as we already briefly discussed, with approximately $4 billion in liquidity available at year-end and minimal exposure to variable rate debt, the company is well-positioned to support its growth objectives without the need for additional capital.

Realty Income

So far, we are dealing with a company that sees consistent AFFO growth, has a healthy balance sheet with access to attractive borrowing conditions, significant long-term benefits from a highly fragmented market, sale-leaseback tailwinds, and no need for incremental capital in 2024.

This bodes very well for its investors.

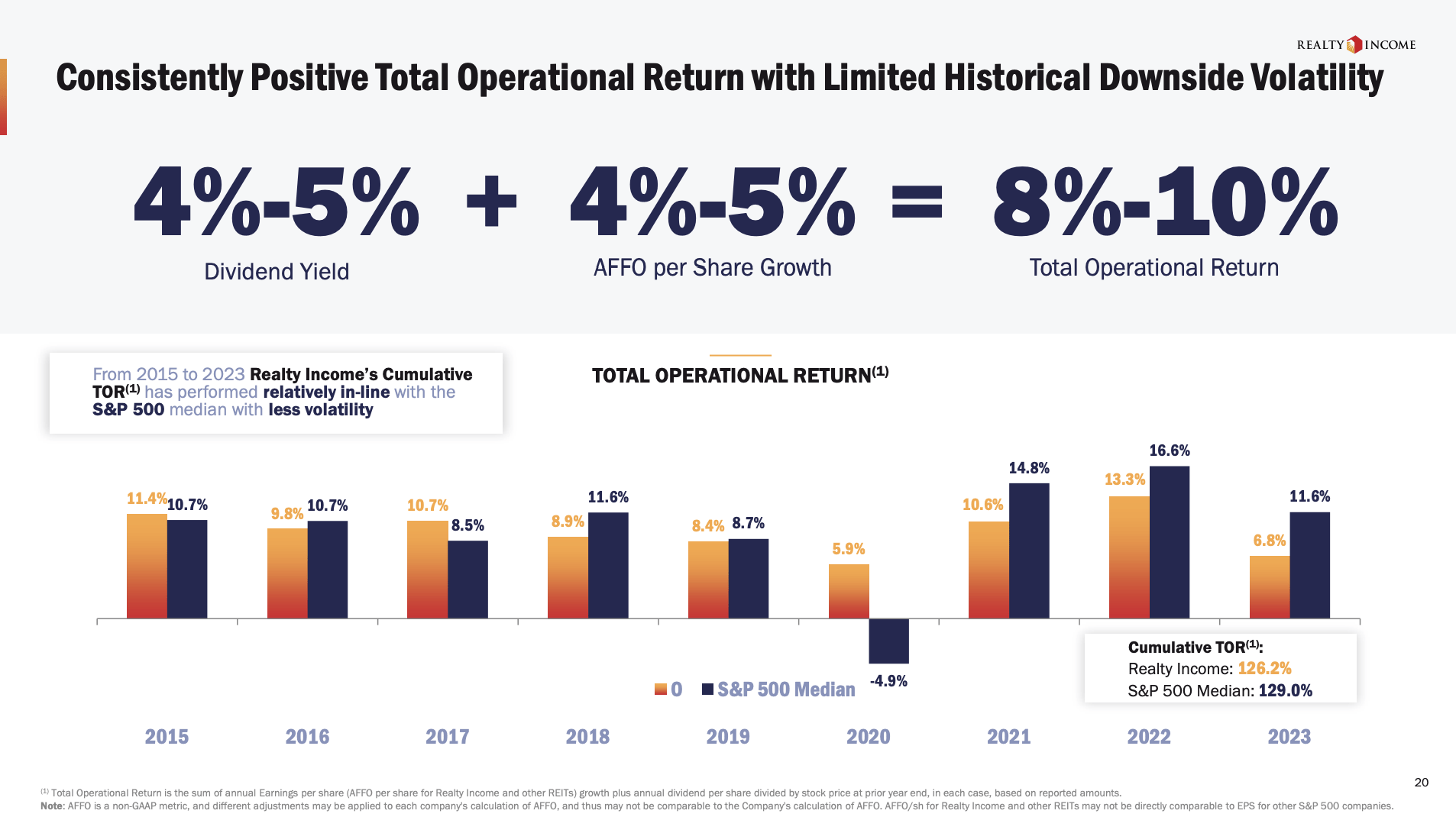

For example, the company makes the case for 8-10% annual returns. This could consist of its 4-5% dividend yield and 4-5% annual AFFO per share growth.

Realty Income

While the five-year dividend CAGR of 3.7% is not high, it’s more than decent for a yield of almost 6% and a business model of moderate but consistent growth.

Analysts agree with Realty Income. They are even a bit more upbeat than the company, expecting 5% AFFO growth in 2024, potentially followed by 4% growth in 2025 and 3% growth in 2026.

While these numbers are obviously subject to change, they indicate a continuation of the uninterrupted AFFO growth streak since 2009.

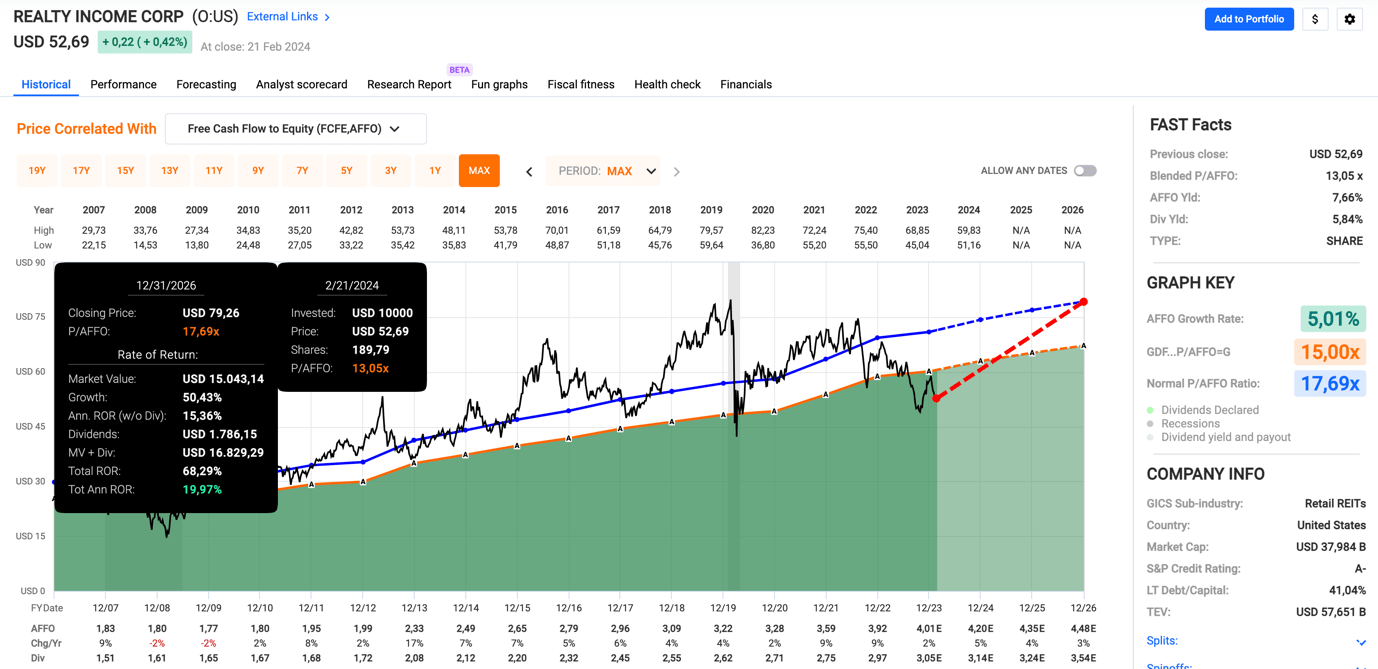

Moreover, using the data in the chart below, Realty Income currently trades at a blended P/AFFO ratio of 13.1x, which is well below its long-term normalized valuation multiple of 17.7x.

While it may take a while until investors are willing to apply a 17.7x multiple again, it does indicate a fair price target of roughly $80, which is 50% above its current price.

FAST Graphs

Even a 15x AFFO multiple would result in a $67 fair stock price and an implied 14% annual return through 2026.

Again, while this depends on various factors, including the Fed’s interest rate path, economic growth, and inflation, the company is trading at an attractive valuation for long-term investors looking for high-quality real estate exposure and top-tier income.

Despite recent market volatility, Realty Income stands out as a resilient investment opportunity, supported by its robust business model, strategic initiatives, and secular growth benefits.

With a track record of consistent growth and a focus on shareholder returns, including a strong dividend yield and steady AFFO growth, the company presents compelling value for long-term investors.

Despite near-term challenges, including inflation concerns and elevated interest rates, Realty Income's proactive approach to capital deployment and strategic partnerships position it well for continued success in the years ahead.

For investors seeking high-quality real estate exposure with attractive income potential, Realty Income remains an enticing option at its current valuation.

Pros:

Cons:

Let me know what you think about this new feature:

iREIT® iREIT® iREIT® iREIT® iREIT® iREIT® iREIT®