Neilson Barnard

Neilson Barnard

I wrote about Squarespace (NYSE:SQSP) previously with a buy rating in December 2023, as I believed SQSP could continue to grow despite the macro headwinds as it continued to release new products and improve its up-selling capabilities. For this post, I still recommend a buy rating as I believe the business remains sound and that FY24 guidance seems too conservative.

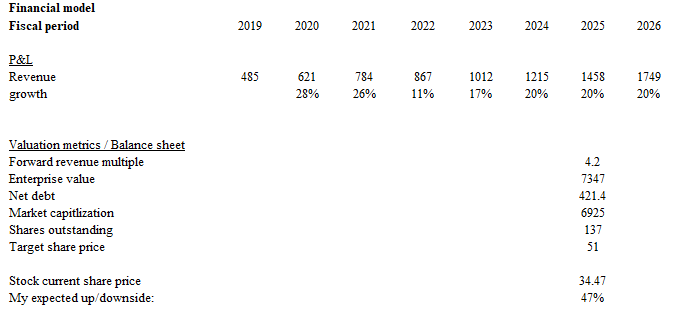

SQSP reported total revenue of $271 million, a growth rate of 18%, which beat both consensus and guidance expectations of 15% and 14.5% (midpoint), respectively. Although the top line beat, EBITDA came in line with the consensus expectation of ~$65 million (24% margin). The good news is that EBITDA flowed through to the free cash flow [FCF] line at a higher than expected conversion ratio, while SQSP generated $57 million of FCF, implying a 21% margin, beating consensus expectations of $51 million. Other underlying operating metrics also continue to point to good underlying momentum. For instance, 4Q23 net new annual recurring revenue [ARR] grew $92 million, which compares really well against peers like Wix (WIX), which saw 10% ARR growth in 4Q23, and GoDaddy (GDDY), which saw 8% ARR growth in 4Q23. In addition, bookings grew by 23%, accelerating from the previous quarter. SQSP ended the year with a net debt position of ~$422 million.

The 4Q23 earnings call shed light on the potential for further pricing growth ahead, which SQSP has been gradually implementing in FY22—a list price increase in 1Q22 and a legacy customer price increase in 3Q22. The results were great and apparent; post-price increase for legacy customers by 10-15% in 3Q22, it led to a strong revenue step-up over the next few quarters as legacy customers that renewed their contracts had to adopt the new pricing. This entire process took at least six quarters to come into effect. For numerical reference, 4Q23 ARPU is ~$228 vs. 3Q22 ARPU of $206, which is ~10% increase. Going forward, I believe pricing is going to be a key part of the growth equation, as the price increase has not really impacted customer churn rates at all. This tells me that customers are still perceiving the SQSP offering as below what it is worth (i.e., what they are willing to pay for). I am expecting management to continue raising prices, and with each increase, it would likely take 4 to 8 quarters of digestion before its effective ARPU will reflect this increase, as a large portion (70+% based on the 2Q21 earnings call) of SQSP subscriptions are on an annual basis.

Price increases across our subscription offerings contributed $39 million, representing approximately 27% of our top-line growth with renewal rates supporting strong cash retention. Company 4Q23 earnings call

I believe the SQSP FY24 guidance might be too conservative. Management is guiding for $1.18 billion of revenue at the midpoint, which implies ~17% growth, which is flat against FY23 growth of 17%. There are 4 reasons I think the guide is too conservative:

So as we go into 2024, 18% growth at the top end of the range is really driven, a combination of what we disclosed for Google Domains but that core business coming through, but we are lapping the pricing and so you will see that impact in the 2024 guide as well as, as I said in my opening remarks, we've built immaterial cross-sell for the Google Domains. Company FY23 earnings call

And so, insofar as we can get the list price higher for new customers sustainably, I think that we'll have an opportunity to modestly raise prices for existing customers again. Morgan Stanley's TMT conference

Note to those that are unfamiliar with the Google Domains background, I have quoted from my previous post:

I see the acquisition of Google Domains on 7th September as a major growth driver that should accelerate SQSP bookings and revenue growth. Generally, domains are annual plans, as it is unlikely for a business to buy 1-month-long domains. As such, upon the acquisition of Google Domains, SQSP would immediately see an increase in bookings that would be translated into revenue over the coming months and quarters. The negative aspect of this is that it is going to depress gross margin in the near term due to higher operations costs and an upfront payment related to domain registry fees associated with Google Domains acquisition. However, I expect gross margins to normalize over time as up-front registry costs start to be in line with subscription revenue

May Investing Ideas

Based on my research and analysis, my expected target price for SQSP is $51, an upgrade from my previous target price of $45.

Given that SQSP has a relatively short history of raising prices, we do not know the “cap” that customers are willing to pay. If the maximum price that a customer is willing to pay is, say, 10% away and SQSP raises the price above it, we could start to see churn metrics go up. If that happens, then the growth runway for SQSP shortens incredibly, as they must rely on cross-selling and unique subscriber growth to grow the business.

I give a buy rating for SQSP given that the business still shows strong fundamentals. I believe that the FY24 guidance is too conservative, given that it implies strong deceleration in the core business, includes no pricing and cross sell potential, and also assume massive churn from the Google Domains. My take is that growth will come above guidance, just like it did historically, and strong growth should persist forward. The key risk lies in customer price sensitivity. If price increases exceed customer tolerance, churn could rise, impacting growth.