hxyume/E+ via Getty Images

hxyume/E+ via Getty Images

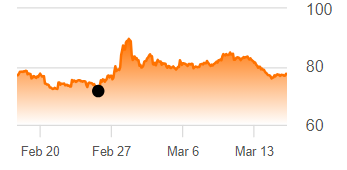

Normally, companies get hammered when they miss Wall Street estimates. This wasn't the case for Shift4 (NYSE:FOUR) when it released Q4 and FY 2023 results last month. Not only did the market give it a pass, but its ticker was up about 8%. And we're not talking about a small miss here. Q4 sales came at $705 million vs. $757 million estimate, while normalized EPS stood at $0.76, a whole 6% short of Wall Street's $0.81 consensus. To be fair, shares dipped during pre-market hours, but that's when Wall Street's wildcatters are swinging prices on low volumes. When the market opened, Shift4 recovered pre-market losses in less than an hour and continued an upward trend throughout the day.

Shift4 share price chart (Seeking Alpha)

The next day, Shift4's shares went up further on reports of a possible acquisition by Fiserv. Today (March 18,) shares are down 8% on news of a buyout fail. These rumour-fueled stock jumps and falls have been happening since Shift4's CEO put the company on sale last November. Now, these rumors might just be rumors. But it makes you wonder why the CEO is cashing out in the first place. I mean, the company just went public in 2020, and they've been expanding astronomically. Last quarter, the one in which Shift4 missed consensus, revenue was up more than 30%, while Adjusted EPS was up 61% YoY.

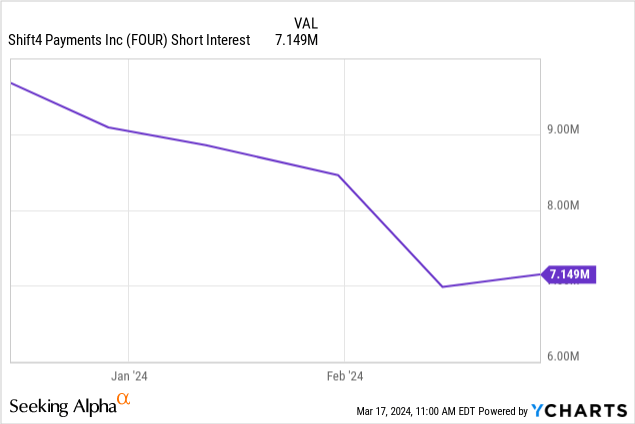

I think the CEO/Founder's desire to sell Shift4 is connected with the stock's bizarre reaction after the Q4 earnings release. You see, many people (or few people with a lot of money) are shorting Shift4, so the stock's surge that day could have been a short squeeze. The way I see it, short-sellers freaked out when the stock quickly recouped pre-market short-selling swings. Short-interest data are kind of laggy, but we can see a leg down in the number of shares shorted the days after the earnings release.

So, what's this got to do with the CEO wanting to sell? Short sellers keep the stock price low, which really frustrates any CEO. Shift4's boss is particularly fed up with it. Here is why.

Shift4 has been performing really well in terms of fundamentals. Management delivered on every Key Performance Indicator 'KPI' and every promise. Revenue more than tripled since the IPO. Net sales is up from $177 to $687 million while operating cash flow rose from $4 million to $388 million.

But Shift4's shares has been moving backwards. Sure, it doubled since the IPO, but in terms of valuation, it is cheaper than its IPO price.

You'd think the CEO would muscle through, staying at it until the market is convinced. But this short-selling is really getting to him. The guy owns a huge chunk of the company. Roughly a third. He started it as a teenager, made the cover of the Times Magazine, the 30-under-30 list, and all. The problem is, he's got expensive tastes. He flies his own fighter jet, went to space (and is planning a second trip). That stuff is not cheap. These hobbies might be why he's borrowing against his shares. I think he's pledged 15 million shares to the loan. When the stock goes down, the stress of getting a margin call on his loan is frustrating. There is a disclaimer about this in Shift4's annual report.

But here's the thing. Whether the CEO sells or not, Shift4 is a good buy. If the company is bought out, investors will likely make a quick profit. If it doesn't, we're buying a solid company at a so frustratingly low price that its own founder has lost hope in the market's ability to correctly value his business.

Chances are you've used Shift4 services without even realizing it. They offer the card payment devices you use to pay in a restaurant or a grocery store. These devices are called Point-of-Sale systems.

You might think,' Okay, these devices are everywhere, and they're probably mass-produced by dozens of manufacturers around the world,' and that's true. Shift4 itself likely sources its POS systems from a third-party manufacturer (notwithstanding their security-key injection facility in Pennsylvania. That's a software thing). My point is it's not just about the hardware. But it's about software integration and how their app (hosted on Android OS) integrates with the other devices and digital systems while at the same time making sure it all follows regulations.

A lot of businesses still rely on older technology. Shift4 has been around since 2000, so they're experts at making their products work with that older stuff while keeping up with new payment standards. If you are a small hotel owner needing a POS, you'll never hear Shift4 engineers saying, 'Oh, you need a new server for us to connect the POS.' That's why they're popular in the restaurant and hospitality sector, where most of the players are SMEs that don't have the resources to keep up with Silicon Valley's latest creations.

This was their big push when they went public. It was like 'Hey, restaurants like us.' But they also made sure that everyone knows that they're not stuck with mom-and-pop diners. They list the likes of Burger King, TGI Fridays, Popeyes, (owned by Restaurant Brands (QSR)), Applebee's (part of Dine Brands (DIN)), Cold Stone Creamery (a subsidiary of MTY Food (MTY:CA), and many others as their customers.

Shift4 also kept its promise to branch out. Today, they have the dominant market share in nearly all the markets they operate in, including Restaurants, Hotels, Casinos, and Entertainment Venues. And check this out. They're the payment provider for SpaceX. I mean, the last one is more like an honorary position, given the niche market of space ticket sales, which also likely sidesteps Shift4's POS card swipe/tap service for a good old bank wire transfer.

This success in growing into new verticals also touches on their market position. Shift4 philosophy is to offer simple solutions to complex problems. They don't do the sophisticated, out-of-this world software solutions like Block/Square (SQ) does. They keep it simple, and thus, affordable. So, price and product design is another advantage and they proved their strategy works. We have more to say about growth.

There is something special about Shift4's acquisitions. Their M&A fuels organic growth. They pick companies serving customers who might benefit from Shift4's POS. This helps the sales team cross-sell high-margined POS service. I emphasize the word service because Shift4 actually gives away its hardware for free, making money on the transactions going through. That's a story for another time.

Now, I don't regret calling its M&A strategy special. I understand that 'cross-selling' is a common M&A pitch, and from experience, the concept is used loosely by investment bankers trying to sell a deal. But Shift4 has a proven track record of doing this really well. So, while an M&A-based growth strategy might sound risky, Shift4 is pulling it off spectacularly. There is a good reason for that. Here is why.

The payments industry is fragmented, partly because the supply chain for processing a payment is complex. Different fintechs provide different services along the supply chain. Customers have to navigate through this complex web of providers to set up a POS system.

In 2019, Shift4 bought Merchant Link, which offered a 'gateway service,' one of the many functions within the card payments supply chain. Merchant Link didn't make big profits, but it came with something priceless: a direct line to potential new customers. Shift4 wasted no time, reaching out to these businesses with an offer: a bundled Gateway and POS services at a discount, kind of a "buy one, get the second at half price" deal. And it's not that customers weren't buying these two services anyway. It was just that the POS system they were using wasn't Shift4's. Many customers shifted from gateway-only to a discounted (but high-margined) 'end-to-end' service. Shift4 was making more money and saving customers' at the same time. If that's not the perfect business model, I don't know what is.

Shift4 didn't stop with Merchant Link. They continued executing their M&A game plan, but this time, they acquired a different link in the supply chain - Finaro, known for its Merchant Banking service. The deal, which closed last quarter, not only adds to the list of customers ripe for cross-selling but also broadens the horizon internationally because Finaro is an EU-regulated 'bank.' I think this is a huge opportunity. Merchant Banking is also a low-margined business. But imagine the sales pitch "buy two, get one for free," saving the customer more money and making higher margins at the same time. And here is the kicker. Europeans mostly use cash, but more and more are starting to use cards. This means that Shift4 can ride this wave on Finaro.

Even without tapping into Europe or Finaro, Shift4 already had a solid growth engine. The company's gateway-only US customers accounted for $150 billion in transaction volumes as of December 2023. If we assume Shift4 charges a 6 cents fee on every dollar processed (which is the "take-rate" Shift4 expects in 2024), this $150 billion would add $9 billion in annual sales. Assuming Visa (V) and Mastercard (MA) and other folks higher up in the supply chain take their 65% share, that still leaves Shift4 with $3.15 billion in potential net sale opportunity. Also, the Federal Reserve is thinking about putting a limit on what Visa, MasterCard, and banks can charge for card processing, which means higher margins for Shift4. Now, speaking of take-rates, one might point out that it decreased in 2023. Here's the deal. Shift4 has been boarding some really high-profile customers in the past twelve months, with pretty high volumes, such as Westmont Hospitality Group, which runs more than 500 hotels and resorts, and Yankee Stadium, which attracted 3.3 million visitors last year. These customers get a discounted take-rate compared to smaller businesses. Companies like these are now the primary target market of Shift4, so don't panic if you see take-rates decline a bit in 2024.

I think Shift4 is ready for a credit rating upgrade from Moody's. Their current Ba3 rating (3 notches below investment grade) was given back in 2020, right when the pandemic hit the hospitality industry the hardest. Plus, they weren't GAAP-profitable at the time.

Now, I understand that the company raised more debt afterwards, but that debt was used to make some really good acquisitions throughout the pandemic and afterwards. Also, this debt came at appealing rates, with a weighted average interest of just 1.4%.

Here is a breakdown of Shift4's $1.8 billion debt as of December 2023:

The first set of notes, the 2025 convertible ones, are particularly interesting. They pose the most immediate risk to liquidity and refinancing needs. With a current share price hovering around $77, it's likely that, by their maturity date in December 2025, the share price will have surpassed the conversion threshold of $80. In this scenario, opting for a conversion is a no-brainer. Sure, this will dilute shares, but it also means less stress over repaying debt with cash or refinancing at a higher interest. Plus, this money was used to fuel a solid growth strategy that also allowed Shift4 to buy $105 million worth of shares last year and budget a $250 million share buyback program through 2024.

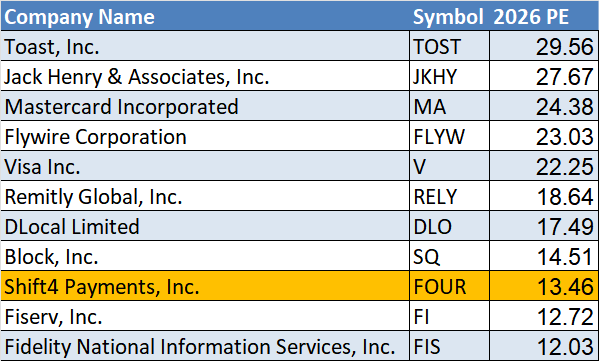

When you think about Shift4's valuation, incorporating growth is pretty important. Right now, Shift4's FWD Adjusted-PE ratio is around 21x, which is perhaps fair. But here's the thing. Growth compounds over time. When looking at Shift4's prospects in Europe, including cross-selling, cash-to-card conversion, and Merchant Banking to End-to-end conversion trends, you are talking about a multi-year growth engine that will take years to exhaust. So, when we look at Wall Street analysts' long-term EPS estimates, PE drops to around 13.5x for 2026. That's below that of peers, especially Toast (TOST), its closest competitor. This shows that the market puts less value on Shift4's growth than it does on other companies.

Seeking Alpha. Table created by the author

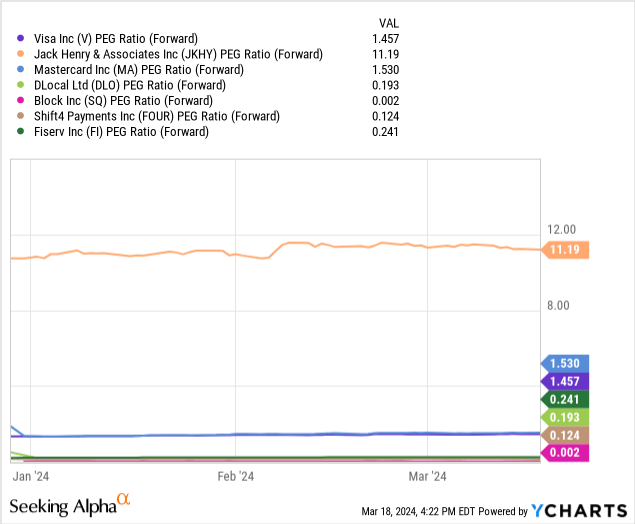

Again, when you look at FWD PEG ratio, you find Shift4 at the bottom of the list, again showing that Shift4's peers are being rewarded more for each incremental EPS growth forecasted going into 2024.

I hope I'm not wrong on Shift4. I think they have a very attractive and reliable growth business model. If things stay the same in the industry, I think this is a winning horse. But that's the thing. No one likes the way the payment industry is, its status quo. Not Congress, not the Federal Reserve, not the Merchants, and even providers are complaining. The system is just too expensive to run. Sure, it is kind of safe, but can't humanity do better? There was a period when there was some hype over Blockchain tech, (the one that powers cryptocurrencies like Bitcoin (BTC-USD). It is cheap and reliable. Not too safe, though. But then, we have the Federal Reserve banks around the world experimenting with official, government-sponsored digital currencies. Shift4 does have some experience with cryptocurrencies. A few years back, they bought The Crypto Block, a company that facilitates digital currency donation and money transfer. But what about their POS, SkyTab? Finaro Merchant Banking service? Their gateway service? Cross-selling? Sure, this is not an immediate risk going into 2024. But in the long run, even increased public discussion about these topics can bring shares down.

So, here we are, with Shift4's rollercoaster rides through Wall Street's expectations, acquisition rumors, and a CEO with a lot to lose who's just tired of it all. So, what do we do? That's up to each investor to decide, according to their own financial goals. What I will say is that Shift4 has many cards to play. Going into 2024, they have:

Most importantly, all this is because of a cost-effective, simple, but powerful payment solution that proved it could compete with the likes of Block (SQ) and PayPal (PYPL). As a wise man once said, in business, there's no such thing as 'winner takes all.' But it's important to make it clear that Shift4 is not some underdog story. Shift4 is the major player here. They have half of the casinos on the Las Vegas Strip, top sports stadiums, and a third (video: 2:35) of US restaurants and hotels, including some of the most sophisticated, and all this has happened in the past few years, even with the fierce competition.