PM Images

PM Images

We're not even through Q1 of 2024, and what a year it's already been. The S&P 500 is up 8.81% YTD and reached an all-time intraday high of 5,242.92 before closing at an all-time high of 5,242.67. A few days ago, Citigroup (C) indicated that the S&P 500 could reach 5,700 in 2024 as technology, specifically AI and fintech, provides a runway for growth. The markets rallied to all-time highs as we are no longer fighting the Fed after commentary from Fed Chair Powell on Wednesday afternoon. While there is a lot of excitement and investors are looking forward to further capital appreciation in 2024, a whole segment of income investors is thinking about deploying capital in a lower-rate environment. The T-bill and chill methodology will disappear as rates start to decline, but the need to generate income will still exist for a segment of the investing population. I have continued adding to my position in the JPMorgan Nasdaq Equity Premium Income ETF (NASDAQ:JEPQ) going into the Fed meeting and feel it's a strong candidate to generate a combination of capital appreciation and income if the market continues higher and rates decline.

Seeking Alpha

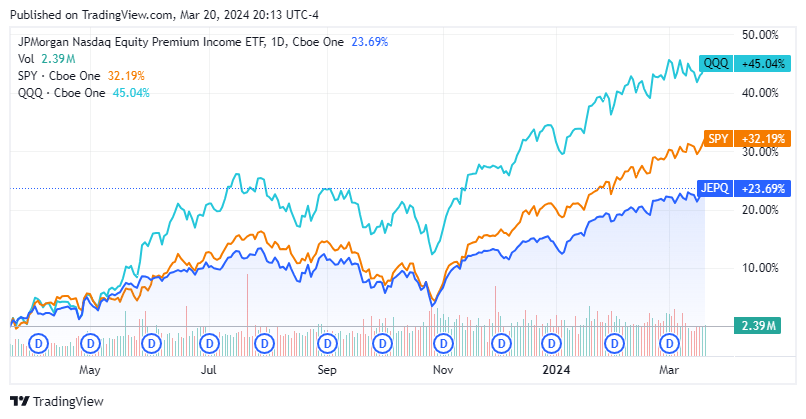

On December 15th, 2023 I wrote an article about why I was still very bullish on JEPQ (can be read here). Since then, the S&P 500 has appreciated by 10.83%, while JEPQ has increased by 7.86%. While JEPQ has trailed the market, its total return in this period has been 10.22%, which is just slightly behind the capital appreciation from the S&P 500. I discussed why JEPQ was one of my preferred income-generating vehicles and how the December Fed meeting could be a positive catalyst for the markets and JEPQ as a derivative play. Now that Fed Chair Powell has delivered what many are taking as a dovish message and outlined where the Fed sees things going in 2024, I wanted to update my investment thesis to reflect all of the new data we have.

Seeking Alpha

Every investment carries a level of risk, and some may carry more risk than others. While JEPQ doesn't carry the same risk as investing in an individual equity, it is subject to market volatility, and its distribution level fluctuates monthly. JEPQ invests in equities found within the Nasdaq 100 with 80% of its portfolio and leaves the other 20% open for equity-linked notes (ELNs) to generate income. The fund managers for JEPQ utilize an option overlay strategy through the ELNs, but the amount of income that is generated fluctuates monthly. There is always a risk that the premiums will compress due to less volatility in the market, making it hard to predict how much income JEPQ will actually generate. JEPQ isn't a hedge against market downtrends, and if the market sells off or if there is a macroeconomic event that impacts the market, JEPQ will likely follow the indexes lower than it did in 2022. JEPQ isn't a traditional ETF as it utilizes an advanced option strategy, so there is a risk that investors don't understand the product as well as they should prior to allocating capital toward JEPQ. Ultimately, JEPQ may not be an appropriate investment for some as it has a track record of trailing the market's returns, doesn't produce predictable income, and in a strong market, a portion of the returns are capped.

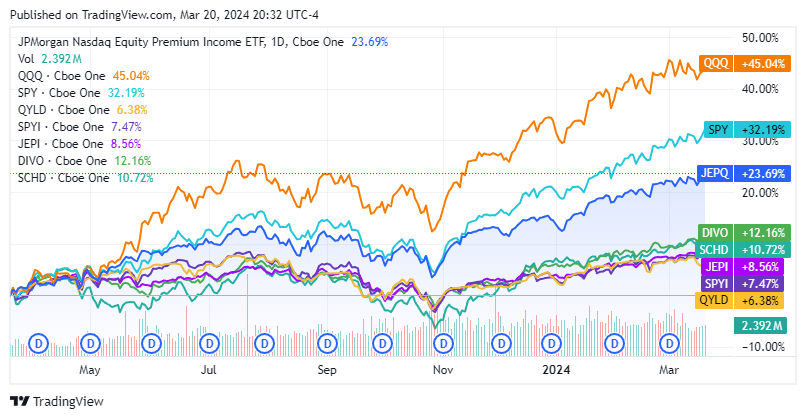

Each of the income-producing ETFs I used in the chart below I am invested in. I am not cherry-picking funds to try and make JEPQ look good. I used the Invesco QQQ Trust ETF (QQQ) as the Nasdaq tracker and the SDPR S&P 500 Trust ETF (SPY) as the S&P tracker. For the income-producing ETFs I used the following funds that I am invested in which include JPMorgan Equity Premium Income ETF (JEPI), Global X Nasdaq 100 Covered Call ETF (QYLD), NEOS S&P 500 High Income ETF (SPYI), Amplify CWP Enhanced Dividend Income ETF (DIVO), and the Schwab U.S. Dividend Equity ETF (SCHD). I am invested in all these funds because I like diversification, and each product fills a gap for me. I added SCHD as a straight equity ETF that focuses on income for the specific reason that it doesn't utilize a covered call strategy.

While all the ETFs have been in the black over the past year, JEPQ is the only one that has exceeded a 20% return prior to looking at the distributable income. While these products have different strategies, JEPQ and JEPI are very similar in structure, and the main difference is the underlying holdings. JEPQ has a 49.90% weighting toward technology, while JEPI's allocation toward technology is 19.03%. While all of the ETFs incur risk, the combination of JEPQ's structure and underlying holdings has allowed it to outperform JEPI and the other funds I compared it to over the past year. While it has underperformed the market, it has outperformed the income-focused ETF peer group I have selected without sacrificing yield. This is a rare feat, as many funds sacrifice much of the upside for immediate income, but that's not the case with JEPQ.

Seeking Alpha

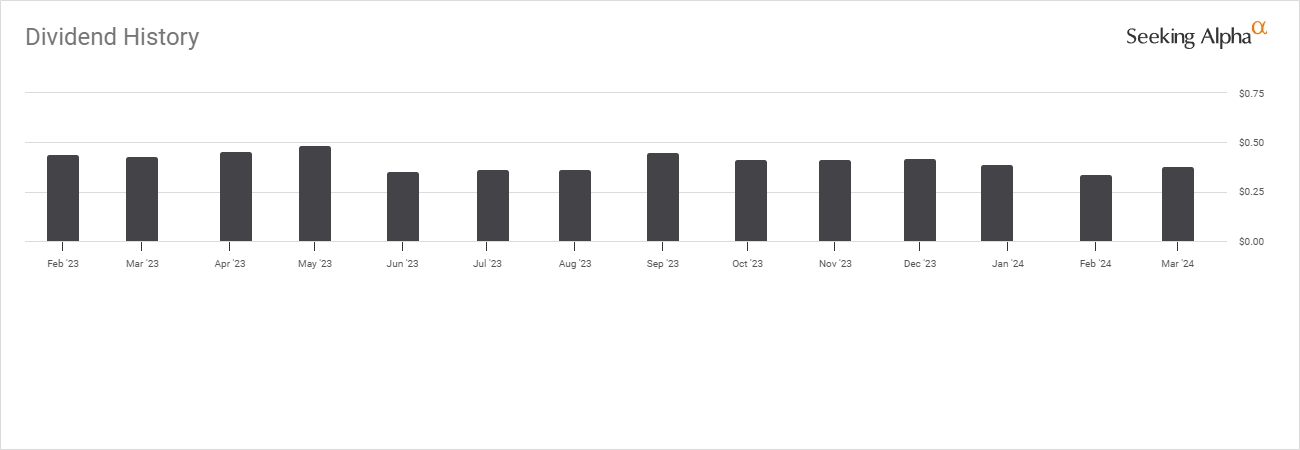

In addition to the 23.69% that JEPQ has appreciated over the past year, it also distributed $4.85 per share of income. JEPQ was trading at $43.60 at this time last year so the $4.85 in distributed income is a yield on cost of 11.12%. When the distribution yield is combined with JEPQ's appreciation over the past year, its total return actually exceeds the S&P 500 by just over 2.5%. While the amount of distributed income has fluctuated on a monthly basis, JEPQ hasn't sacrificed as much upside as its peers to generate a double-digit yield. JEPQ isn't a perfect fund, but I don't believe any investment is perfect. When the market retraces, JEPQ will follow it directionally, as we saw in 2022, but when a bull market is occurring, JEPQ will do a respectable job at generating capital appreciation while throwing off monthly income. I think that JEPQ is an investment that can satisfy both camps of investors and give income investors more upside exposure than other products during periods of appreciation.

Seeking Alpha

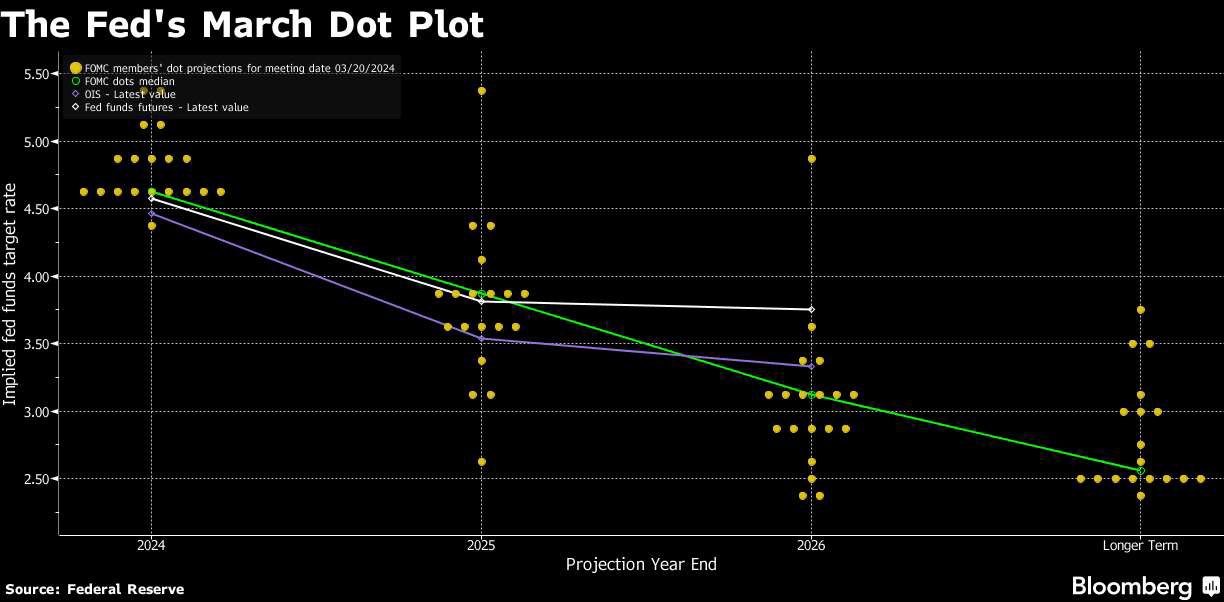

We're no longer fighting the Fed after today's meeting. Fed Chair Powell sounded very dovish today, and while he said that the Fed wants to see more evidence of inflation moving back to 2% before cutting and left the door open for rates to remain higher for longer, it doesn't seem like rates will remain over 500 bps for too much longer. The overwhelming feeling from the fed members is that we will see 3 rate cuts of 25 bps in 2024 to start the cycle, regardless of whether cuts start in June or September. The overall rate outlook increased a bit as the Fed had previously indicated that we would end 2026 at 2.9%, and now the Fed is looking more toward 3.1%. The market took the conference as a positive, and I think it's because we got more clarity on how the Fed sees rates unfolding, the Fed is predicting that 2024 GDP will come in above their previous projections while unemployment will be slightly lower than they expected. If the market didn't like the news, it would have sold off during the conference and fell further upon Fed Chair Powell's closing remarks.

Bloomberg

I think the market is going higher, and JEPQ will climb along with it. As rates start to come down, the wall of debt in the real estate market coming due in 2025 becomes less of an issue because it will be able to be refinanced at levels that work for both parties. The regional banks won't get stuck holding unwanted real estate assets as we will probably avoid a situation where the keys are turned over to the lenders, which would have probably caused the banks to sell the assets at discounted prices to get them off the books. I think part of the rally is because another regional banking crisis may be avoided over the next year or two. Also, as rates decline, the cost of capital will fall. This will take a burden off of the American population, unlock the housing market, and encourage borrowing from businesses. This should increase spending across all sectors, which will flow up to the largest companies held by JEPQ. If we are in a multi-year bull market cycle, as I believe we are in, then JEPQ should do well as the market goes higher.

There is currently $6.36 trillion sitting on the sidelines in money market accounts without taking into consideration capital tied to CDs and T-bills that will be maturing over the next year. The 2-year T-bill has already seen its yield drop from 5.49% to 4.59% since the fall of 2023, and we haven't even experienced a rate-cutting cycle yet. I think that capital is going to flow into the market as the Fed starts cutting rates, and income investors will look to recreate the yields they have become accustomed to. As tech plays a major role in the market, I think that some investors will look for investment products that allow them to participate in the upside while still generating a respectable amount of income. I think JEPQ will continue to gain popularity as it could continue to bridge the gap between investing for capital appreciation and investing to generate income. As a hybrid product, I am very bullish on its future prospects, and if the market goes higher, I think JEPQ will follow while generating monthly income.