Dilok Klaisataporn

Dilok Klaisataporn

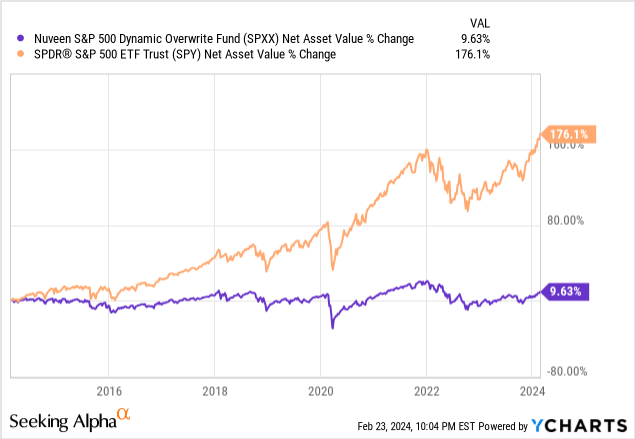

The Nuveen S&P 500 Dynamic Overwrite Fund (NYSE:SPXX) invests in S&P 500 components and writes covered calls on 35% - 75% of its holdings. Doing so boosts the fund's distribution yield to 7.6%, but moderately reduces potential capital gains. SPXX's strategy seems reasonably sustainable, with fund distributions and NAVs seeing positive growth since 2009, although both were down during the past financial crisis. SPXX's strong 7.6% distribution yield and compelling 9.2% discount to NAV make the fund a buy.

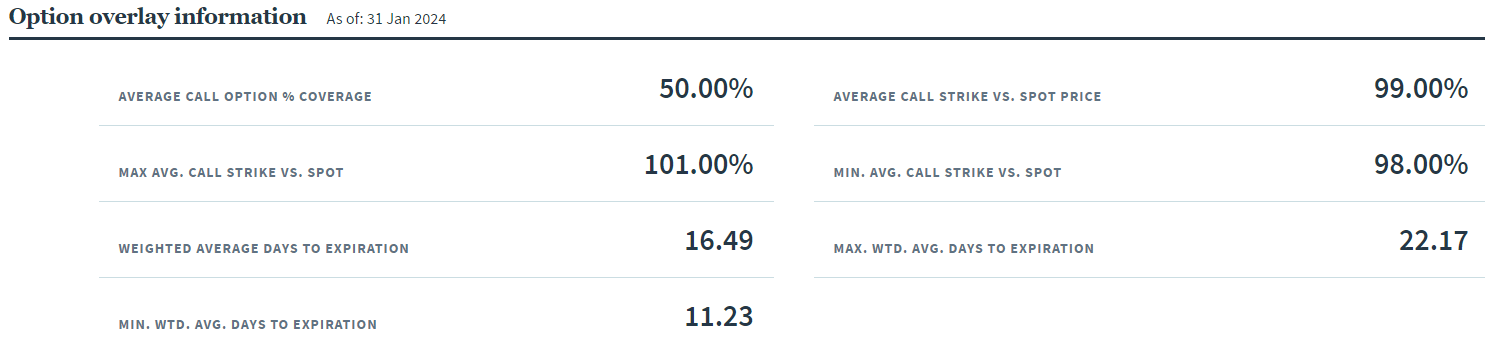

SPXX invests in all S&P 500 components and writes covered calls on 35% - 75% of its holdings, with a long-term target of 55%.

The S&P 500 is the most well-known U.S. equity index. SPXX's holdings are overwhelmingly large, blue-chip stocks with strong fundamentals, including well-known companies like Microsoft (MSFT), Johnson & Johnson (JNJ), and JPMorgan (JPM). Industry exposures are reasonably balanced, somewhat overweight tech, especially mega-cap tech.

What sets SPXX apart from simpler S&P 500 index, and from most other equity funds, is its covered calls. SPXX generally sells monthly calls with strike prices near the money, and with the fund overwriting around 50% of its portfolio. Specific figures are as follows.

SPXX

SPXX's covered call strategy has many important implications for the fund and its shareholders. Let's have a look at these.

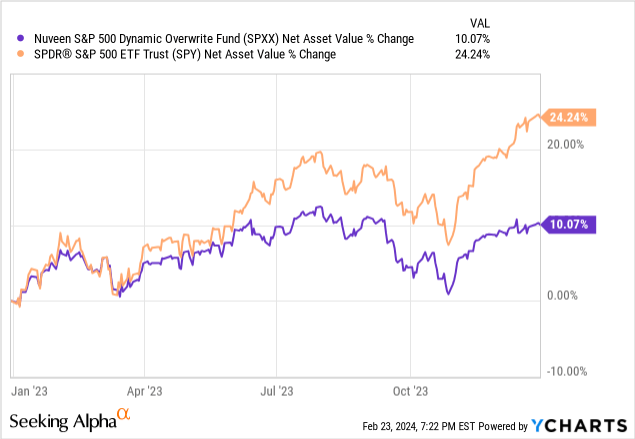

SPXX's covered calls serve to reduce any potential capital gains by around 50%. Specific figures do vary, especially during periods of heightened equity volatility, and long-term. As an example, SPXX's NAV per share increased 10.1% in 2023, during which the S&P 500 rallied 24.2%. Gains were somewhat lower than 50%, but results were still broadly in-line with expectations.

Data by YCharts

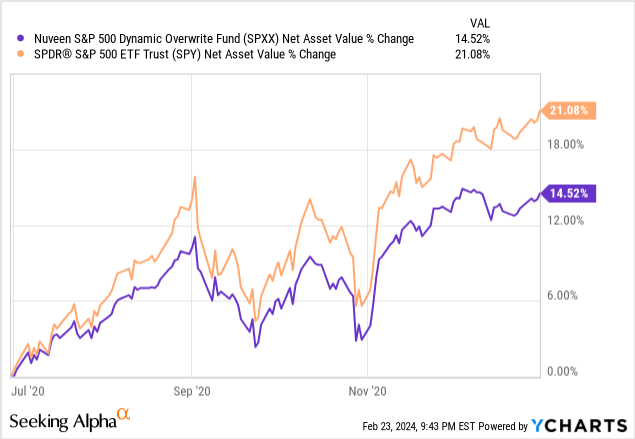

Corollary of the above is that SPXX should see much lower gains during recoveries. Although obvious, still important to explicitly mention. As an example, compare the fund's NAV per share rose by 14.5% during 2H2020, in which the S&P 500 rallied 21.1%. Gains were almost 70% those of the index, somewhat outperforming expectations.

Data by YCharts

Lower potential capital gains are a significant negative for the fund and its shareholders. As a small aside, I always include the word potential when discussing these issues because, well, capital gains are never certain, and equity prices could always remain flat for decades. If prices do increase, SPXX's price should increase by much less than the S&P 500, an important consideration for investors.

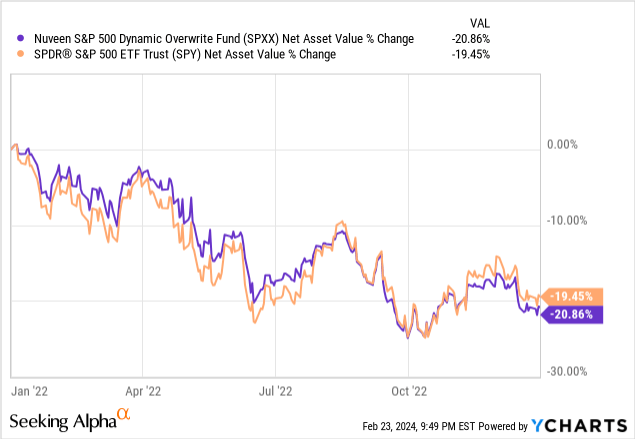

SPXX's covered call strategy has no impact on potential capital losses / share price reductions. Expect similar declines to NAVs per share as the S&P 500 when these occur, as was the case during 2022.

Data by YCharts

As SPXX's share price sees below-average gains, but average losses, long-term capital gains are anemic, at best. SPXX's NAV per share has slightly decreased since inception, increased these past ten years. I would expect broadly similar results moving forward: anemic long-term growth during long-lived bull markets, declines when volatility and losses are higher.

Data by YCharts

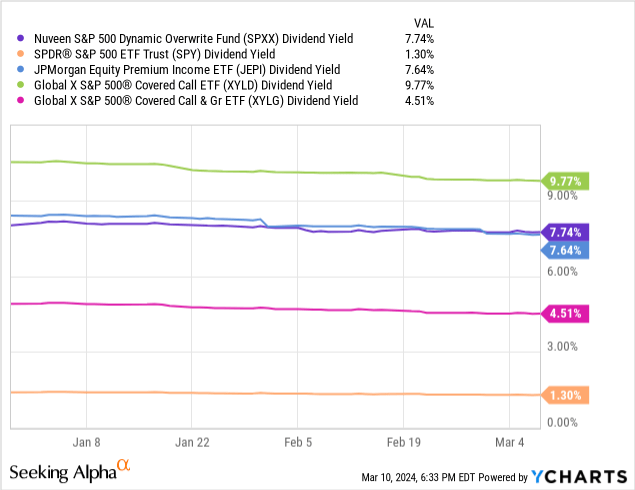

SPXX's covered call strategy generates significant amounts of option premiums, which are then distributed to shareholders. The end result is a 7.6% distribution yield, quite high on an absolute basis, and much higher than the S&P 500's 1.3%. On the other hand, the fund's yield is about average for a covered call ETF, slightly lower than that of JPMorgan Equity Premium Income ETF (JEPI), one of the largest, most popular funds in this space.

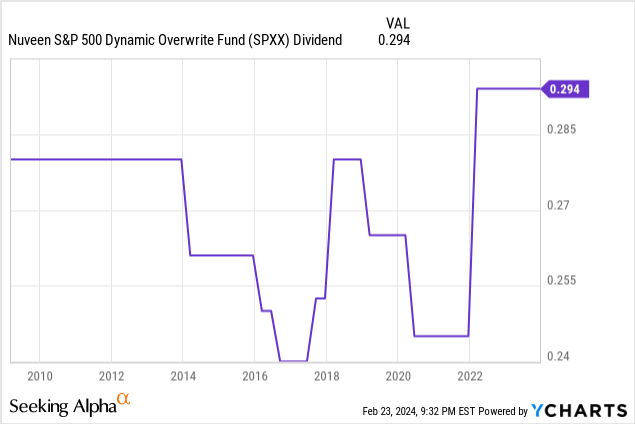

SPXX's distributions are dependent on many factors, including option prices / premiums, equity volatility, underlying S&P 500 dividends, asset prices, and NAV per share. The long-term sustainability of these is somewhat unclear, due to being impacted by so many factors. Distributions have seen positive growth since early 2009, so since the financial crisis / housing bubble.

Data by YCharts

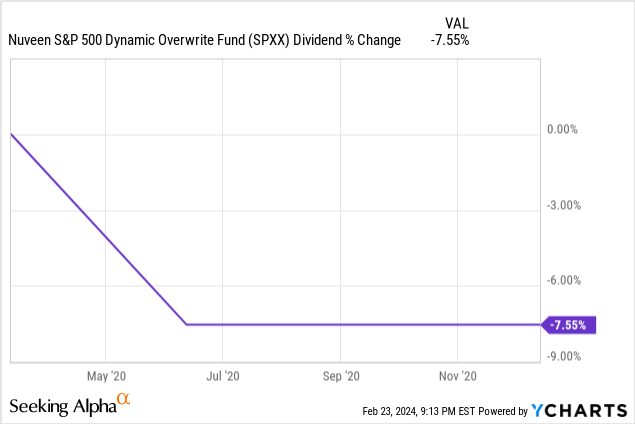

Distributions should also decline during downturns and recessions, as was the case during 2020, due to the pandemic.

Data by YCharts

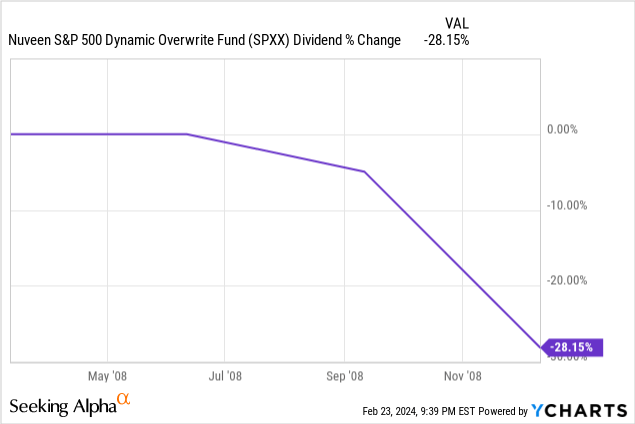

Distributions declined by 28.2% during 2008, when the financial crisis hit. At a glance, distributions seemed unsustainable before, so a significant cut seemed warranted.

Data by YCharts

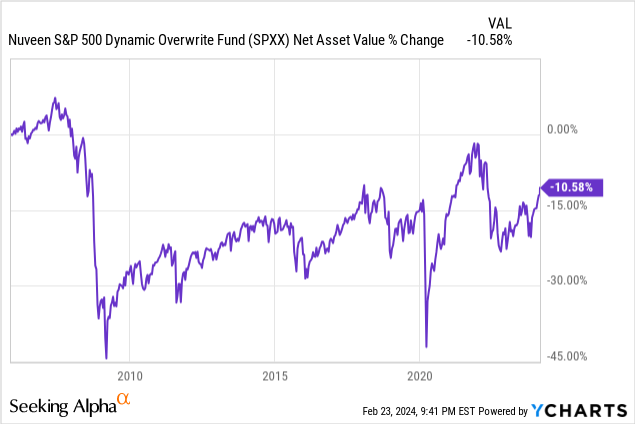

As mentioned previously, SPXX's NAV is down since inception, entirely due to losses during the past financial crisis. NAVs are up since 2010, and since the pandemic.

Data by YCharts

Overall, SPXX's distributions seem long-term sustainable. Distributions are down since inception, but these seemed unsustainable during 2007 and 2008, so a cut was to be expected. SPXX has experienced a recession, the pandemic, and a bear market, 2022, since, without any significant or long-lasting fallout. NAVs seem reasonably stable too, so no evidence of unsustainable / ROC distributions there either. I would expect distributions to remain broadly stable from here on out, long-term at least.

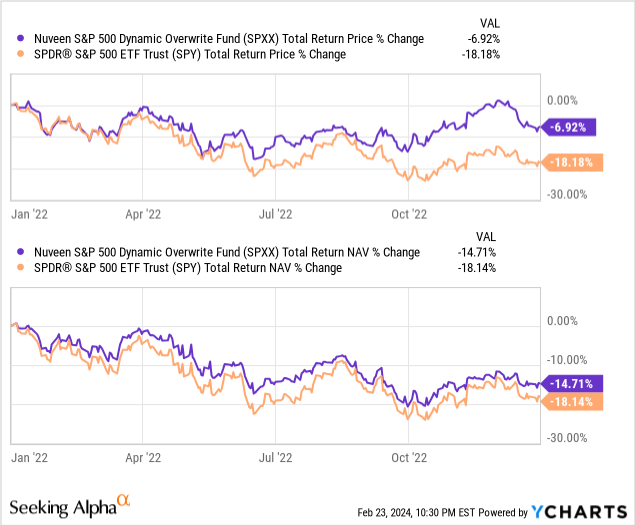

SPXX's strong distributions are particularly impactful during flat and bear markets, leading to outperformance during those periods. As an example, the fund outperformed the S&P 500 on both a price and NAV basis during 2022, when equities were down by almost 15%. SPXX saw similar capital losses, but its higher distributions led to higher total returns.

Data by YCharts

The above is an important benefit for SPXX and its investors.

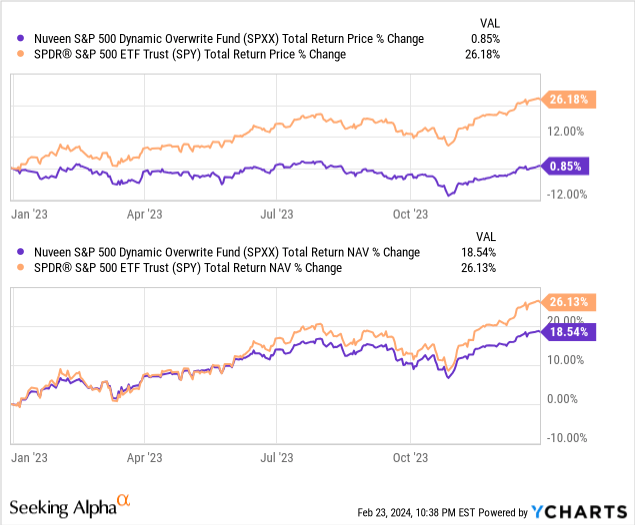

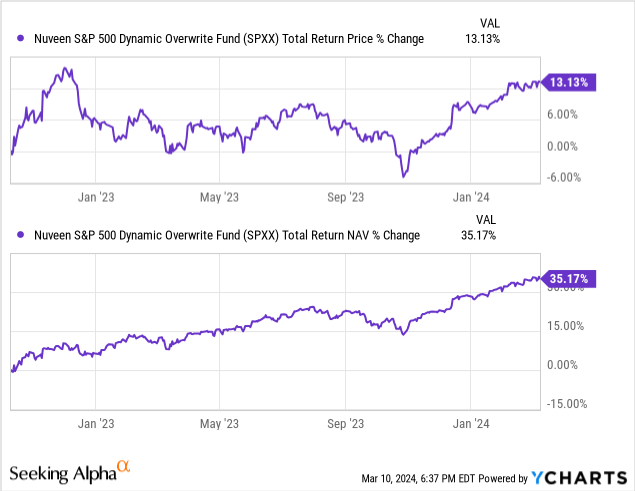

SPXX's reduced potential capital gains are particularly impactful during bull markets, for obvious reasons. Expect the fund to underperform during these periods, as was the case during 2023. SPXX's share price increased by much less than the S&P 500, and although the distributions made up for some of the difference, the gap was simply too large.

Data by YCharts

The above is a significant negative for SPXX and its investors. Do remember that bull markets are a bit more common than flat or bear markets, stocks mostly go up, so SPXX should underperform more often than not.

SPXX's covered call strategy is actively managed, with the fund attempting to focus on options with particularly good prices and characteristics, varying the amount / percentage sold according to market conditions, and doing so in a tax-efficient manner. From prior coverage, it seems that the fund avoided a massive special distribution in 2021, which might have had favorable tax implications for some investors.

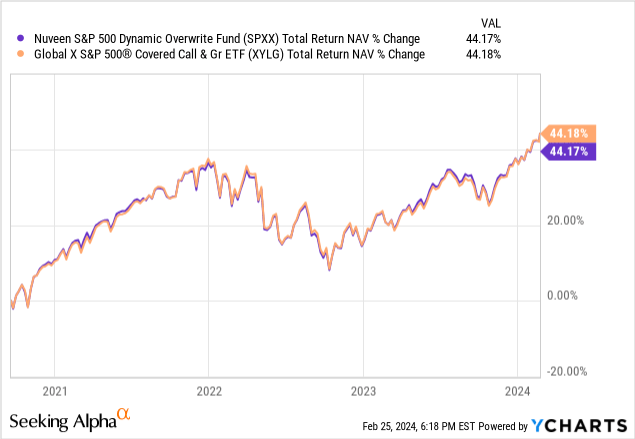

Besides this, it does not seem that the fund's covered call strategy has any tangible impact on its performance, as it has performed almost identically to the Global X S&P 500 Covered Call ETF (XYLG), an ETF with a similar strategy, but without the active management.

Data by YCharts

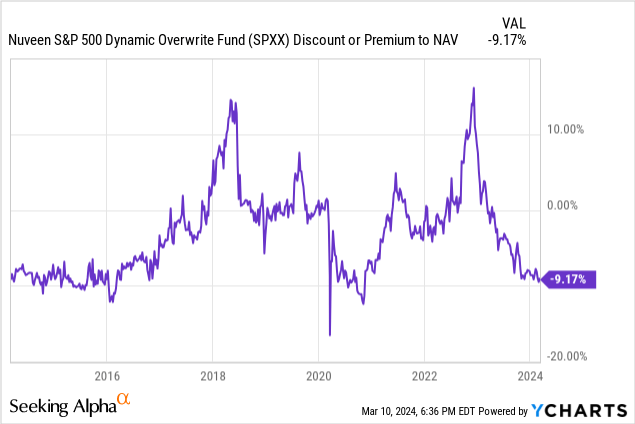

As a final point, SPXX currently trades with a 9.2% discount to NAV. It is a wide discount on an absolute basis, and much higher than the fund's long-term average.

Wide discounts mean higher yields and potential gains from discounts narrowing, both important benefits for the fund and its shareholders.

As a final point, I last covered SPXX in late 2022. At the time, SPXX traded with an atypical 8.5% premium to NAV, which I argued was excessive. SPXX was a reasonably good fund, but not a buy at those prices and premiums.

Since then, SPXX's price returns have significantly lagged behind its NAV returns, as its premium turned into a discount. Avoiding the fund was the right choice at the time, it seems.

SPXX's strong 7.6% distribution yield and compelling 9.2% discount to NAV make the fund a buy.