David Taljat/iStock Editorial via Getty Images

David Taljat/iStock Editorial via Getty Images

TotalEnergies (NYSE:TTE) is a major European oil & gas company, and its Q4 2023 Earnings call presentation supports its claim to be the most profitable major oil & gas company. The company has two contrasting pillars, one as an oil & gas producer (big focus on LNG), the other “Integrated power” which is a combination of renewable energy and CCGT (Combine Cycle Gas Turbines) power production.

The takeaway from recent announcements and actions by TotalEnergies is an enthusiastic embrace of LNG.

In checking what is going on in the world as it relates to changes in energy mix in different countries, I find Our World in Data has some interesting stats. The most recent data (2022) shows the changes in source of energy, and I give two tables below for China and the USA.

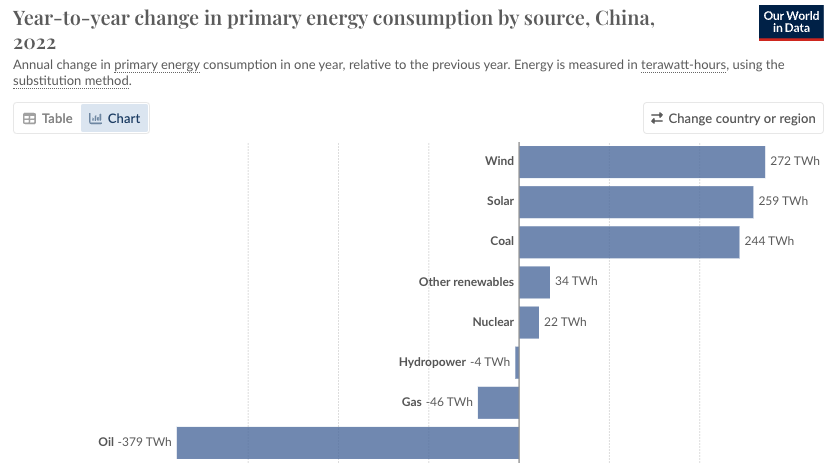

Change in energy consumption China 2022 (Our World Data)

China’s data shows that while coal use increased in 2022, new wind and solar produced more power than coal and there was a decrease in gas use and a more striking decrease in oil use.

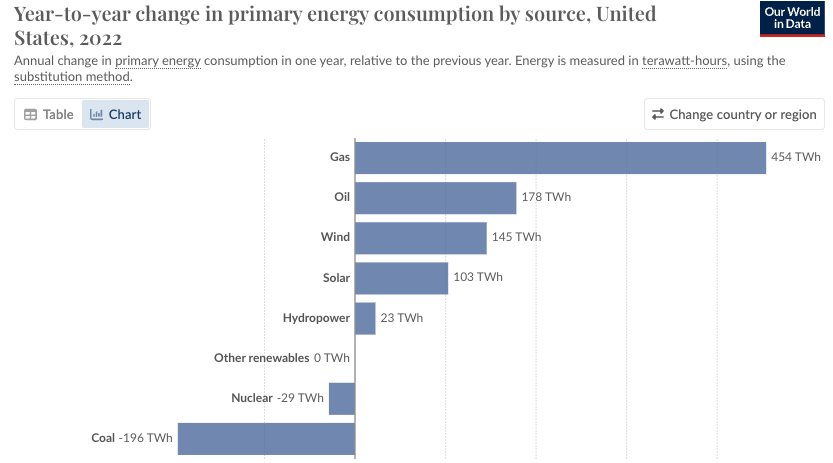

Change in energy consumption 2022 USA (Our World Data)

For the US, there was a dramatic increase in gas consumption, while coal use fell dramatically. I suspect that the results concerning gas for the US in 2022 may be what is influencing TotalEnergies’ and others enthusiasm about gas, especially LNG. The above US data on gas is striking and reflects the triumph by the gas industry in becoming a substitute for coal.

Recent data about total emissions (including methane release) suggests that the mantra that natural gas is cleaner than coal might not be true. It will be interesting to see whether gas (especially LNG) continues to be a market darling as renewables plus battery storage begin to compete with CCGT in head on competition. If that happens then TotalEnergies will find difficulty in both its oil & gas business (which is very dependent on the continued success of LNG) and also its CCGT business.

A recent Wood MacKenzie report addresses opportunities for gas as the world moves towards net zero by 2050. In a nutshell the Wood MacKenzie report makes clear that things are becoming challenging for the gas industry, even as the leading companies in this space (including TotalEnergies) push aggressively to expand their production. Wood Mackenzie thinks that there is a future for gas but it is in a world where CCS (Carbon Capture & Storage) is adopted. My take is that there is no evidence that CCS works other than in a very limited way. Dreams of an expanded gas industry making blue hydrogen or heating homes are just that as far as I can see. Wood MacKenzie acknowledges that the IEA sees a much diminished role for gas by 2050 compared with Wood Mackenzie’s projections.

After its oil & gas business (which is rapidly becoming its LNG business), the second major activity of TotalEnergies involves its role as a power producer. This involves a combination of renewable energy and power production from fossil fuel gas via CCGT. The renewable energy component gets attention because TotalEnergies has a really big presence in this space. The CCGT business involves TotalEnergies continuation of its fossil fuel business, and it is not small. For example, in Texas 2023 renewable power was less than 2 TWh and flexible generation (CCGT) was nil, while in 2024 the plan is for 2-3 TWh of renewables and substantially more than 3 TWh of flexible (CCGT) power generation.

An interesting aspect of the Integrated power business is TotalEnergies CEO, Patrick Pouyanne’s claim that renewable energy is more expensive than what Governments recognise. I find this claim odd because the consensus of all of the expert groups is that renewables are substantially cheaper than fossil fuel (or nuclear) power.

The thing that gets my attention is the massive overall cost of fossil fuel exploitation. Looking at TotalEnergies CAPEX of $16.8 billion for 2023, $11.8 billion of that CAPEX was spent on oil and gas (with focus on LNG) production. This happens EVERY year (see 2024 CAPEX of $17-$18 billion). Without it, there is no fuel to run the CCGT power plants or fuel the Internal Combustion Engine vehicle industry. The contrast with the renewable industry is stark, with just 35% of $5 billion ($1.75 billion) CAPEX spent on low carbon energies (presumably mostly solar PV and wind projects). Every dollar of the renewable energy investment builds an energy capture vehicle that has minimal costs once built and that lasts 20+ years.

TotalEnergies has a formidable global presence in mostly solar (but also including wind power) renewable power generation, with a network of affiliates. These include :

TotalEnergies is focused on France and French overseas territories, and it provides renewable power through wind, solar, hydropower and biogas.

SunPower is a leading US distributed solar power generation company. It develops rooftop systems for residential, industrial and commercial buildings as well as solar carport solutions.

Total Eren is a developer, builder and operator of solar and wind systems in Asia-Pacific, Africa and Latin America. The company is built on partnership with local developers.

Maxeon is a leading solar PV innovator and manufacturer, selling SunPower-branded solar panels in more than 100 countries, including in Africa, Asia, Oceania, Europe and North America.

The above companies are serious players in an industry in transition. They are not without their problems, as renewables have recently encountered challenges as interest rates have risen and the fossil fuel industry pushes back. The point is that renewable energy requires substantial capital investment upfront, but this investment serves energy production for 20+ years.

SunPower is a good example of a company that has struggled as the US domestic solar market has been challenged. The company has had an extraordinary percentage of its shares shorted. The fact the TotalEnergies is a controlling shareholder means that as long as TotalEnergies remains engaged, the company will survive. I remain optimistic about SunPower because rooftop solar has grown 10 fold over the past decade, but rooftop solar penetration is still a small fraction of that in Australia which has approximately one in three houses with rooftop solar and the size of rooftop solar additions keeps going up. An old (2016) report from the NREL suggested that rooftop solar potential in the US could involve producing 39% of US electricity needs. Given recent dramatic improvements in solar panels, I suspect an updated version of the NREL report would suggest the potential for rooftop solar PV in the US is substantially greater than 39%.

The fact is that in the US, actual rooftop solar PV penetration remains in the low single digit percentage overall (less than 4% in 2022). There is a lot of room for SunPower's business to grow.

This area is a continuation of TotalEnergies presence as a major fossil fuel industry player. I’m suspicious that calling out “expensive” renewables (which doesn’t seem factual) may be cover for TotalEnergies increasing focus on CCGT power provision (see Texas example above).

I’m a fan of quarterly earnings calls as one gets a chance to hear from senior management about how they perceive the progress of the company and what the key issues are.

The big news was that 2024 is TotalEnergies’ 100th anniversary year! It started as an oil explorer in Iraq, and today it has a two pillar strategy with oil & gas (mainly LNG) on one side and integrated power (renewables + CCGT gas) on the other.

The oil & gas business showed a red flag for me, with plans to grow its largely LNG oil & gas business by 2-3% annually. This comes at a time when the world is beginning to exit fossil fuels. Does this mean that TotalEnergies doesn’t accept the need to exit LNG? All of the discussion is about the reverse, with more LNG supply coming on line in 2026 and 2027 through a significant number of new projects. Something has to give with the climate emergency. There seems to be confidence that Asia will be the growing LNG market, which I find surprising because Asia suffered huge LNG price increases when Russia invaded Ukraine. Singapore is an Asian market to pay attention to, because it is 95% dependent on natural gas/LNG. Given the disaster of huge LNG price increases in 2022, my take is that Singapore is aggressively looking to renewables to hedge its bets (and also address the need to reduce emissions).

The whole earnings call and Q&A was about expansion of everything LNG, new projects, more LNG tankers etc. This is relevant to both the oil & gas pillar and the Integrated power pillar. CEO Patrick Pouyanne was ebullient about his LNG business. How is this compatible with the need to exit fossil fuels? There wasn’t a lot of attention given to the renewable assets or how they are planning to be developed. There was focus on intermittency and the need to address this, but no discussion of how this is being managed through batteries (although there is some investment in batteries), grid connectiveness (HVDC links), time switching of consumption and demand management. The oil & gas industry doesn’t like to acknowledge these approaches.

Seeking Alpha’s report of an interview with TotalEnergies CEO Patrick Pouyanne with the Financial Times gave further insight, this time into his views about the renewables side of the business. It is clear that the CEO does not accept what is clear, i.e. that renewables are a cheaper source of energy than fossil fuels. In this respect, his views align with those of Exxon Mobil CEO Darren Woods, who dismisses renewables as being incapable of replacing fossil fuels. The difference is that Patrick Pouyanne thinks that Governments are not being honest about the costs of adopting renewables.

Coverage of TotalEnergies on Seeking Alpha is consistent with neglect by US investors of European majors. Both Total Energies and Exxon Mobil have similar profiles, but the extent of coverage is very different.

TotalEnergies has three Seeking Alpha authors covering the stock in the past 90 days (two “buy”, one “hold”), while Exxon had 23 Seeking Alpha authors in the past 30 days (five “strong buy”, 13 “buy”, three “hold”, two “sell”). There were 10 Wall Street analyst rankings in the past 90 days for TotalEnergies (three “strong buy”, two “buy”, five “hold”) compared with 26 Wall Street analysts (10 “strong buy”, six “buy”, 10 “hold”). Both Seeking Alpha authors and Wall Street averaged a “buy” rating for both TotalEnergies and Exxon Mobil.

Seeking Alpha’s Quant rating is the same (“hold”) for both TotalEnergies and Exxon Mobil. This means that the Quant gave TotalEnergies no benefit for its investment in the energy transition. Exxon Mobil refuses to contemplate change, using obfuscation like CCS (Carbon Capture and Storage) as a defence.

When thinking about long term investment in the energy space, it is important to think about what is happening (electrification) and how quickly the shift will happen. The fossil fuel industry has been in charge for a long time, but the future is exit from fossil fuels. There is a small group of very large, profitable energy companies, and it is interesting to consider how they are approaching the end of their industry. Perhaps the company with the most extreme position is Exxon Mobil (XOM) which is doubling down on dramatic expansion of its oil & gas developments, while putting up a smokescreen with technology that doesn’t work (CCS, Carbon Capture & Storage). It is clear that Exxon management does not believe that the world can exit fossil fuels. At the other extreme is Orsted (OTCPK:DNNGY), which in an earlier life was DONG Energy. DONG stood for Danish Oil & Gas. Orsted decided some years ago to exit fossil fuels and has now left behind its fossil fuel past with a focus on being the world’s #1 offshore wind project developer.

TotalEnergies sits in the middle as a company that acknowledges that the world is exiting fossil fuels and that renewable energy (electrification) is coming. At least that is what I thought before the Q4 Earnings Call. Management commentary made clear that the core of the company is and will remain its enthusiastic adoption of a major place in the development of LNG. The renewables adventure seems more about exploiting and, as TotalEnergies management sees it, “expensive” option that the world is willing to pay for, rather than as a switch to a cleaner and less costly world. TotalEnergies clearly has a stake in a decarbonized future, but I’m no longer convinced that management is fully committed to the change. This makes me more cautious about the company than I have been in the past. The thing is, the change is coming fast, and it will mean cheaper, less volatile prices and with less sovereign risk than the fossil fuel-based world that is being left behind. TotalEnergies is clearly better equipped to make the change than is Exxon Mobil, but they are not as far down the track as is Orsted. Time will tell how TotalEnergies manages the change, but I’m cautious at this time.

I am not a financial advisor, but I follow closely the dramatic changes happening as the world begins to exit burning fossil fuels. I hope that my comments help you and your financial advisor as you consider investment in TotalEnergies.

Our world data

World data

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.