Kevin C. Cox/Getty Images News

Kevin C. Cox/Getty Images News

Since I first covered SPWH in September 2022, with a hold rating recommending against a purchase, the company's stock price has decreased by nearly 60%.

In this review, I find that the company now suffers from a negative cycle, a combination of several headwinds.

Although I like SPWH's market position for the long-term, and I agree with the company's new management strategy to weather the storm, I believe the company is currently too risky to invest in its equity. The reason is that an American recession would put SPWH's equity at risk, for which there is no sufficient discount at any price.

On the other hand, the stock could be part of a relatively diversified portfolio looking for appreciation in an optimistic/moderate scenario but with the understanding of the substantial risk of total wipeout of the equity in an adverse scenario.

SPWH is in an interesting market position.

The company caters primarily to hunters, representing 55% of its sales of firearms and ammunition. Further, its stores are concentrated in the west of the country, and the company has a strategy to open smaller stores in less densely populated areas.

The position is interesting because of this specific retailing type's competitive dynamics.

First, large retailers like Amazon and Walmart do not participate in the market, automatically clearing large competitors and almost eliminating a real challenge from e-commerce. Other outdoor retailers like Dick's Sporting Goods don't sell firearms either. The reason, I believe, is a mix of ESG commitments, brand coherence (firearms don't provoke a bucolical emotion in a lot of people), and the hassle involved in selling firearms. Having a retailer that does not compete with the big box chains is a huge tailwind.

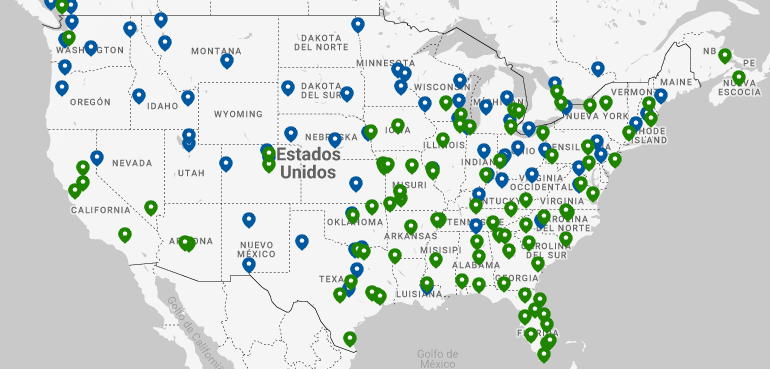

Second, the company's west-coast oriented store base (first image below) is not competing so much with other hunting retailers, like Academy Sports (second image below), Bass Pro, and Cabela's (third image below).

Location of Sportsman's Warehouse stores (SPWH website) Location of Academy Sports and Outdoors stores (Academy Sports and Outdoors website) Location of Brass Pro and Cabela's stores (Brass Pro's website)

Third, the firearms market is dispersed among mom-and-pop shops, with only 10% of firearms selling licenses in the hands of chains and a company's estimated 60% of outdoor specialty retailers being SMBs.

A retailer with these conditions is already interesting.

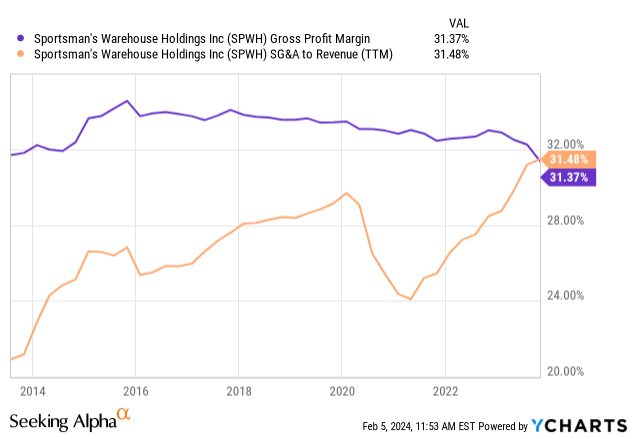

However, the company has not made use of this market power. In my previous article, I complained about SPWH not increasing its margins and allowing SG&A expenses to grow above gross profits by the end of the past decade.

SPWH is currently undergoing a mix of bad news.

First, the COVID-induced shopping spree that led to the company's revenues growing so fast in 2021 generated a long-lasting demand decrease in 2022 and 2023. While most people expected the trend to stabilize, SPWH's sales continue falling YoY.

Second, being long-lasting items, most people can delay the purchase of a tent, firearm, or related equipment until things improve. As inflation hits middle to low income families more, they have become more wary and delay spending on their hobbies.

Third, the US winter was especially harsh in 2023, particularly in several areas where snow records were broken (in California or Utah). Harsh winters are not a good factor for hunters because they cannot expose so much on the outside.

These are all external, cyclical factors that could potentially turn-around. Some winters will be milder, and people's economic confidence might increase. In that case, why isn't SPWH a contrarian buy?

I believe the reason is the company's lack of strength, which compounds the cyclical risk at the equity level.

First, like any retailer, SPWH's margins are razor-thin, which means that a small increase or decrease in sales disproportionately affects operating income (this is called operating leverage). If the company had managed its SG&A expenses better, it could have a wider margin, it could have weathered such a cyclical circumstance better.

Even assuming historical gross margins of 33% and fixed SG&A of $400 million going forward, the difference between breakeven and $50 million in operating losses or earnings is less than 10% of revenues ($1.2, $1.05, and $1.36 billion, respectively).

Second, the company took a lot of debt to finance store openings and the inventories that these require. From zero debt at the end of 2021, the company increased its credit facility to $200 million in 3Q23, just before the holiday season. The company has no cash cushion to repay these debts and weather a further decrease in sales.

Fortunately, the company's management (with a new CEO announced in September) is working in the right direction: repaying the debts and decreasing SG&A expenses.

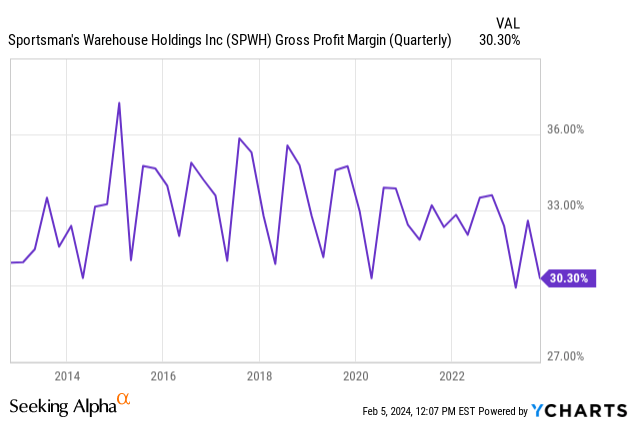

First, the company started aggressively discounting its products. Gross margins fell from an average of 33% historically to less than 31% in the last reported quarter, and management has guided for a 28% or 26% level for 4Q23. They argue that they want to reduce inventories by $100 million and use the proceeds to decrease debts by half.

Second, SPWH announced that it will not open stores in 2024 after opening more than 10 stores per year for the past four years. This should significantly decrease the company's CAPEX expenditures and save as much as $75 million compared to 2023.

Third, management is concentrated on reducing SG&A expenses, and has shown signs of accomplishing this. The company's SG&A did not grow YoY. However, the company had 10% more stores than during the same period in 2022. SPWH also announced on its 3Q23 10-Q that per-store payroll expenses decreased 22%, a considerable margin.

This points in the right direction: repay the debt, build a cash cushion, and build margins. This is necessary to insulate the company from cyclical ups and downs so that shareholders and management can concentrate on the company's long-term potential.

I believe SPWH is undervalued for a moderate to optimistic scenario but that it is risky for a downturn scenario.

The reason is that because of operational leverage, a small cash cushion, and not so much equity, the company is at subsistence risk if an economic downturn lasts two years or more. This puts the potential recovery at stake.

Assuming that the company can return to average gross margins in 2024 thanks to its inventory rightsizing program (which is already a bullish statement), it would require about $1.2 billion in revenues to break even (covering $400 million in fixed SG&A expenses).

If the company does not break even, things start moving in the wrong direction. Even at average margins, with $1.1 billion in revenues, the company would generate $35 million in operating losses, which in significant part are cash losses. Without cash reserves, the company would need to fill the gap via debt, slowing down the deleveraging process. Every year of a downturn and every $100 million in lost revenues, debt increases by $35 million. All of this assumes the company can return to average gross margins, which is clearly not certain under a recessionary scenario.

With a book value of $270 million, the company has some strength to sustain the hit but not a lot of cash or liquidity. The company's working capital facility allows for about $300 million in borrowing, which is only $100 million more than the company borrowed this year to prepare for the holiday period. This is equivalent to 3 years of small losses only or even less of more significant losses.

Further, a prolonged downturn period (for example, caused by a one or two-year recession) would put the company in shrinking mode, closing stores, which would trigger more considerable cash-based losses from resigning to its lease contracts. This would further shrink equity.

On the other hand, in a moderate scenario, with only $1.3 billion in revenues and average gross margins, the company would generate $35 million in operating profits.

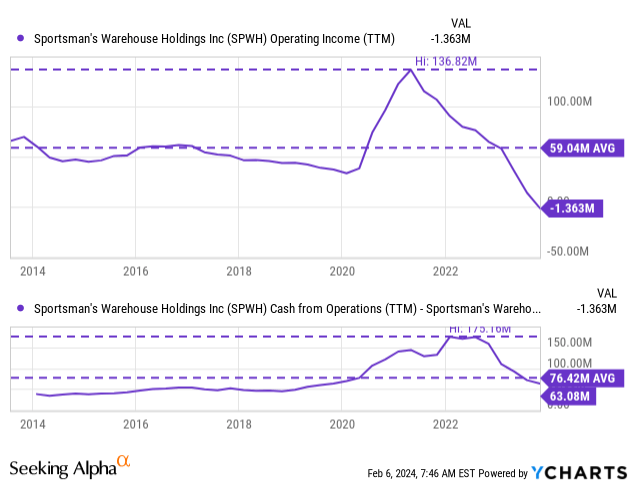

Further, the company could reduce holiday inventories by $50 million (one-time cash inflow) and generate approximately $50 million from operating cash flows from working capital, given that this measure has generally been a little above operating income in the past (chart below). Because the company will only need to do maintenance CAPEX in the order of $20 million (no new stores opening).

This means a one-time reduction in debt of $50 million plus $30 million yearly, from the current $200 million levels down to $150 million by 1Q24, and from then on down $30 million every year. For this scenario, we only need revenues to stop falling and margins to recover, which is optimistic but not crazy optimistic. In this scenario, the company would generate $35 million in operating income and pay about $9 million in interest in FY24 (SOFR + 1.5% on a $135 million average working capital facility). That would become $20 million in net income after taxes, which more than handsomely compensates for a $140 million market cap today. Further, as debt is repaid, more interest moves to net income, and the equity value grows.

Considering an optimistic scenario where the company can reach its 2021 revenue levels, the stock could be a five-bagger. On fixed SG&A of $400 million and 33% gross profit margins, the company could be producing $70 million in net income by 2025 without debts, which, after applying a 10x multiple, implies a market cap of $700 million.

Which one of the three scenarios is more likely? I do not know where the economy is heading. However, I speculated above that a 15% fall in sales from current levels can put SPWH in a very flimsy position. I believe that a 15% fall in sales from today's levels is not crazy, considering the company has been losing revenues at that speed for two years already. If the US economy hit a significant problem and people curtailed spending, a 15% decrease in a hobby like hunting seems normal.

That constitutes the main problem for SPWH. The stock could have no bottom in a recessionary environment because there is no large equity cushion to prevent further leveraging and eventual lease cancellations.

Therefore, I cannot recommend a position in SPWH. This goes against Buffet's only rule: 'Never lose money.' If SPWH had a cushion, then we could patiently wait for a recovery and not (permanently) lose money, but under the current circumstances, time is not on our side.

Again, I like the company's positioning, and the fact that it has upside, but I'm concerned with downside risk here.