Maskot

Maskot

My recommendation for Sprout Social (NASDAQ:SPT) is still a buy rating as the business momentum continues to be sound, and the market appears to have looked past the customer churn issue, based on the valuation that SPT is trading at today. My expectation ahead is that SPT will continue to grow at a very healthy pace, with the potential to beat guidance. Note that I previously gave a buy rating for SPT as the business fundamentals remained sound and that investors were simply focusing on the wrong metric. My contrarian view to continue staying bullish paid off as the stock rallied from the lows in November ’23 to the current share price of around $64.

Looking at SPT's performance in 4Q23, I am still bullish. Revenue growth maintained its impressive pace of >30%, reaching 34.3%. Subscription solutions revenue grew by 33.3% year-over-year, while professional services revenue grew by 174.7%. This impressive performance was fueled by strong upmarket trends and the ongoing success of premium module cross-sell initiatives. Together with the robust top-line outperformance, the 60-bps increase in gross margins to 79.3% resulted in an adjusted EBITDA of $1.7 million and a margin of 1.8%.

My view is that growth is going to continue at this strong pace, at the ~high 20% level, in line with management's guidance. In fact, I think SPT could even continue to grow at a low 30 percent, as management tends to be conservative on its revenue guidance. Since 3Q20, SPT has always beat its guidance (at the midpoint) by an average of 2% (they only fail to meet guidance once in 4Q22). The fundamental drivers of the company also paint a very positive outlook. Take, for example, SPT's success in penetrating the upmarket segment. It added 147 customers with >$50,000 in ARR (annual recurring revenue), which is a growth of 43.9% year-over-year and brings the total to 1,399. This demonstrates strong traction in moving upmarket for SPT. The company additionally saw an increase of 578 customers with >$10,000 ARR, bringing the total to 8,689 and indicating a growth of 30.6%. The organic growth drivers—cross-selling—were the main force behind this impressive expansion. As an example, premium module attach rates increased to 30%, a 300-bps sequential increase from 27% in 3Q23, thanks to these efforts. My view is that this proves its cross-selling was successful. Combining both aspects together, this led to a remarkable growth in aggregate ACV (annual contract value), reaching $12,299 (~43%) over the past 2 years.

We could also potentially see bookings and growth acceleration in SPT as the business benefits from the Salesforce (CRM) partnership and improved sales team productivity. Management did not reveal the precise amount of new logos added in Q4 from the partnership, but they vaguely mentioned new logos comparable to 4Q22, but with 40% more new ARR. This suggests that ARR/logo is significantly higher, which supports my optimistic belief that SPT is successfully penetrating the upper market. If this trend continues, we could see FY25 with a higher ARR/logo, which will result in growth acceleration. Regarding the point about sales team productivity, I believe Tagger will be a potential growth driver for 2024 in this regard, since Sprout has recently finished training their whole sales team on it and integrations are generally going smoothly with the platform. Because Sprout plans to market Tagger in the same way as its other premium modules—such as analytics and social listening—I am confident that the company will continue to reap incremental benefits from it well into 2024. The 30% attach rate achieved during the quarter is proof of premium module sales success.

Author's valuation model

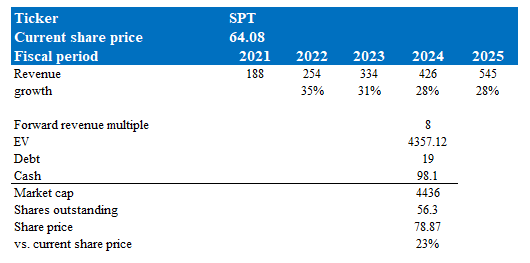

According to my model, SPT is valued at $79 in FY24, representing a 23% increase. This target price is based on my growth forecast of 28% for FY24 and FY25. FY24 growth is based on the high end of management FY24 revenue guidance, which I think is easily achievable given the business momentum so far. As for FY25, I assume the same 28% growth rate, as I don’t see any potential slowdown in growth, especially with FY25 macro conditions potentially turning better relative to FY24. The last time I wrote about SPT, it was trading at 7x forward revenue, and with SPT showing that the shrink in customer count is not a growth headwind, the market has re-rated the stock up to 8x forward revenue. As SPT sustains its high-20% growth, I believe this multiple is justified.

My new concern with SPT is that dollar-based net retention [DBNR] continues to trend lower. DBNR fell to 107% in FY23 vs. 109% in FY22. While I anticipate an improvement in this metric throughout FY24 with the company having churned through the majority of its non-core customer base, if this continues to trend lower and dip below 100%, it could signify that the underlying health of the upsell/cross-sell motion is not as good as I believed.

I maintain my buy rating for SPT. The company continues to demonstrate strong business momentum, exceeding expectations on revenue and profitability. Reviewing the latest 4Q23 results, SPT maintains impressive top-line growth, exceeding 30% in 4Q23. This momentum is driven by strong upmarket trends, successful cross-selling initiatives, and increasing average contract value. Looking ahead, I believe SPT has the potential to beat its conservative guidance and achieve low 30% growth, considering its historical record of exceeding expectations. Moreover, the recent Salesforce partnership and improved sales team productivity through Tagger implementation position SPT for further growth acceleration. While the declining DBNR is a concern, I expect it to improve as the company moves past its non-core customer churn. Nevertheless, continued deterioration below 100% could signal a challenge in upselling and cross-selling, warranting reevaluation.