Julie Denesha

Julie Denesha

I’ve previously written about using the noise to your advantage with Boeing (BA), which has only become louder and louder since that article was published. While I still feel bullish on Boeing over the long term despite its current firestorm, does that also translate to Spirit AeroSystems (NYSE:SPR), a one-time part of Boeing based in Wichita that produces fuselages for major commercial aircraft companies? Spirit has a lot of the same characteristics as Boeing and some that are superior, such as benefitting from both parts of the Boeing/Airbus duopoly while also having no part in the two MAX plane crashes that were due to the faulty MCAS system. Would Spirit be a better way to play the commercial airplane space? I personally don’t believe so. While Spirit does not have all the same issues that Boeing does, it has other concerns that I’ll address in this article that do not make me want to buy the stock at this time. I don’t believe there’s enough upside to justify the risk at this point.

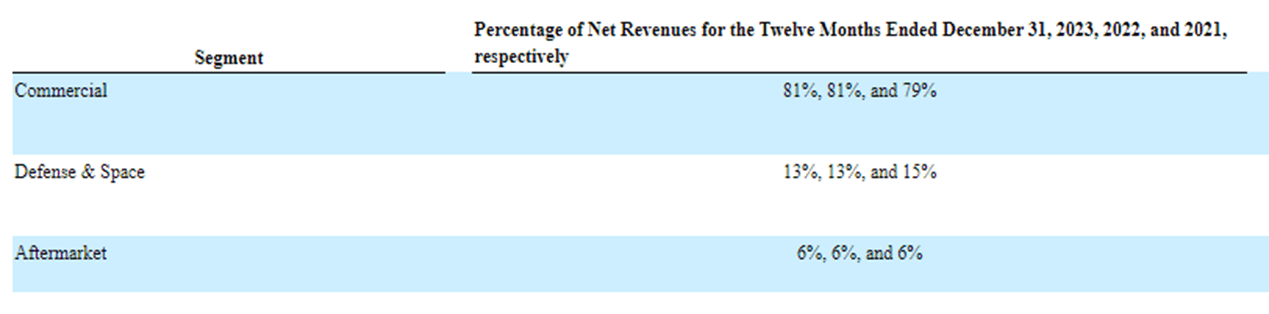

Spirit AeroSystems Holdings, Inc. is based in Wichita and is one of the largest manufacturers of structural aerospace parts and components in the world. Spirit's main products are fuselages, which is the main body of the aircraft, wings and wing components. In 2023 and 2022, 81% of Spirit’s revenues came from the commercial segment as seen below. Of that, 70% was from Boeing, while 23% came from Airbus (OTCPK:EADSY). Obviously, that’s a huge portion of the business as three-quarters of the Company’s total revenues come from the commercial airline duopoly. The remainder of its revenues are from the US government, as well as non-commercial aerospace revenues from Boeing and Airbus (Defense and Space and Aftermarket).

Spirit Sales by Segment (Spirit AeroSystems 2023 10-K)

Spirit has been mired in controversy ever since the Alaska Airlines (ALK) door plug blowout on January 5th. Even though it’s been more than two months since the incident, who remains primarily at fault between Boeing and Spirit still remains unclear. At the time of the event, Spirit was trading at highs not seen since the summer, but still well off its pre-pandemic highs.

Spirit AeroSystems 1 year Chart (SeekingAlpha Charts)

Since that time, the news cycle has been poor, with blistering reports of a failure in quality control systems. This negative noise could have been seen as an opportunity to buy Spirit if you truly believed the issues were fixable, as its stock price was down significantly in its wake. However, news that Boeing was in talks to acquire Spirit broke at the beginning of March, causing an immediate 15% increase to Spirit’s stock which makes the value proposition less compelling.

Spirit is not solely dependent on Boeing, as they also have a very large customer in Airbus. An investor could make the argument that betting on Spirit is a safer bet than Boeing, in case any of this smoke actually turns into fire for Boeing (some of you may already see the flames). By investing in Spirit, you get both parts of the duopoly. In my opinion, that isn’t really the case given how much Spirit depends on Boeing. I believe that because Boeing is so dominant as a percentage of Spirit’s revenue, Spirit is going to live or die with Boeing. It is important to note that Spirit has favorably renegotiated its terms with Boeing in the fall to help make this relationship more palatable, a feat that is not that easy for such a large customer.

One of the big problems I see is that it has not only been the current quality audit issues that have plagued Spirit in recent years. In April 2023, Spirit notified Boeing of a non-standard manufacturing processes for two fittings. A few months later in August, improperly drilled holes in the aft pressure bulkhead were reported to Boeing by Spirit. Both of these issues caused delays in Boeing’s production schedules and lead to an increasingly strained relationship between Spirit and its largest customer. This also comes after several disruptions in 2022 due to more quality issues and parts delays. Ultimately, these issues lead to the resignation of CEO Tom Gentile and appointment of Pat Shanahan in October 2023. Shanahan, a former Boeing executive has many investors feeling hopeful that he can turn some of these issues around.

You can certainly make the argument that the issues with quality are similar, if not worse for Boeing, and yet I’m bullish on them and not on Spirit. I don’t believe that Spirit holds the same power in its position that Boeing does, though I certainly wouldn’t bet on another manufacturer taking the place of Spirit, despite its flaws. It is too integrated in the supply chain and design of these aircraft. My larger concern with Spirit is one of valuation and upside.

What is Spirit actually worth? Not an easy question as they haven’t made a profit in four years, not all that dissimilar to Boeing. Crucially however, they also haven’t had positive cash flow since 2019. That’s a major distinction from Boeing, that has had solid free cash flow since the second half of 2022.

To understand this more, I decided to look at the company’s historical metrics, given it hasn’t generated net income or cash from operating activities for a full year since 2019. I could look at a price or enterprise value to sales instead, but that’s not really my preferred metric. I believe that mature companies are about making money, not generating sales, and they need to be valued based on that. I’ll give Spirit the benefit of the doubt that the pandemic and related supply chain issues are temporary. My assessment will be based on what they would be worth if they return to normal profits.

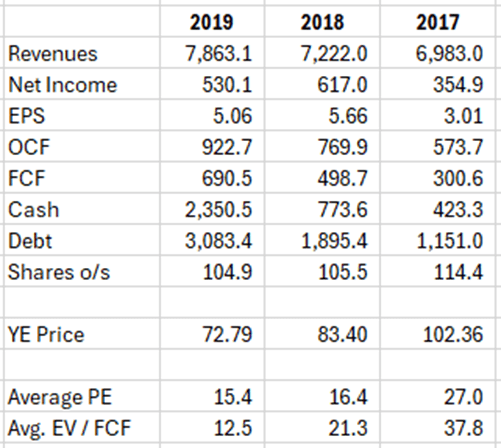

Looking at the three-year period ended in 2019, while valuations tend to jump around due to large swings in stock prices, after averaging those out, Spirit typically trades at multiples in the high teens for P/E and EV/FCF. Obviously there are outliers, which 2017 appears to be, but that higher than expected multiple appeared to be predicting the strong future results as the forward P/E was 18x.

SPR 2017-2019 Financial Data (Author Analysis derived from SeekingAlpha data)

Let’s invert what this is telling us. If Spirit typically trades at something like 17-19x, at the current price that would mean net income of about $200 million. Compared to where they were several years ago, that should be easy, right? Well, look at how interest expense has changed over that time.

SPR 2017-2023 Interest Expense (SeekingAlpha financial data)

This tells me that Spirit will essentially have to add another $200m in profit to that net income number in order to offset the large increase in interest expense. Can they do that? Maybe – if they can get back to that 2018 / 2019 operating income level, they will do it with a little upside. But that’s asking a lot from where we are at this point, and it certainly won’t happen within a year or two.

In the Q4 earnings call, CFO Mark Suchinski noted:

And then to address your first question around long-term. I don’t want to get into the prediction business. But when you think about what this business generated in the past, I think you’re referencing the 7% to 9% margins and $500 million to $600 million worth of free cash flow in the future. As we go up to the higher rates that will obviously help from a revenue and a profitability and a cash flow standpoint, I think we can get back to those levels. There are some headwinds as it relates to some of the inflationary pressures that we talked about before like the IAM contract. But I think the single biggest item that we need to work on to help us drive back up to those cash flows because I think the business is going to drive it is we’re carrying $4 billion of debt and $350 million, $325 million of cash interest. So over the next couple of years, we need to take that positive cash flow, pay down debt. Not only will that help our leverage from a balance sheet standpoint, but it will get the cash interest drag off the books. And if we can drive that interest back down to our historical measures, we can get back to similar to levels that we’ve had in the past."

Management appears to recognize this stumbling block to returning to past profitability. I don’t think it’s impossible, it will just take some time, all of which needs to be discounted appropriately, which hurts the valuation.

If the valuation isn’t currently compelling, what other catalyst could exist that could change my thesis? First, there is the possibility of the sale of the company which has been confirmed by Boeing and typically would offer a premium to the market value. But analysts are not certain that is the case here; any premium is likely to be limited or already reflected in the price after the Boeing announcement. And the other question is would the government even allow it? FTC chair Kahn recently said that Boeing was “too big to fail”. I’d be very skeptical that the current aggressive stance that the FTC has taken would allow Boeing to get even bigger. If the deal is off the table, there’s certainly some risk of downside to the stock.

The impact of new CEO Pat Shanahan could, and quite frankly should, help Spirit return to their more successful years. Shanahan is an engineer by trade and education, with a career at Boeing spanning three decades in various management positions. He even had a stint as the Acting Secretary of Defense during the Trump administration which is a huge strength in an industry where political power drives funding. I just believe the deck will be stacked against Spirit in the next several years and despite this impressive hire, it’s going to take too long to turn this around.

Based on the valuation, the expectation of a muted premium (if an acquisition were to take place), and the ongoing quality issues with the business, I just cannot see investing in Spirit AeroSystems at this time. I do feel that downside risk is somewhat protected by the possibility of the sale to Boeing however, which should provide a floor to the current stock price.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.