edwardolive

edwardolive

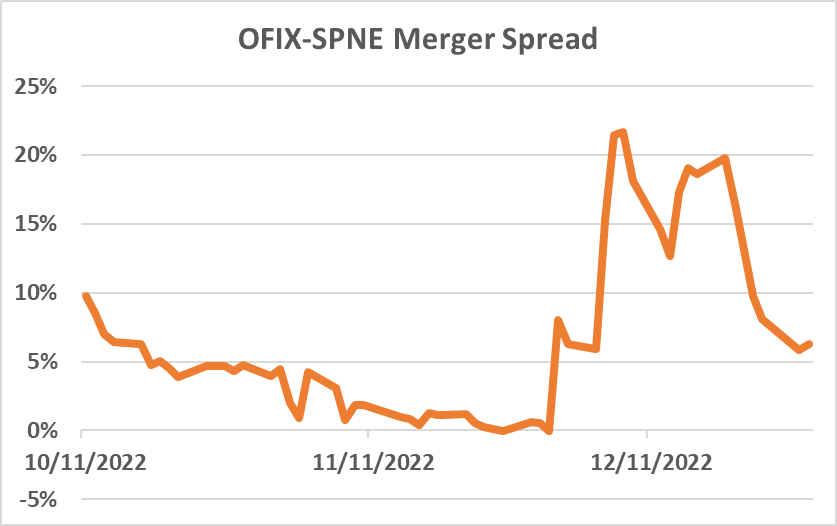

This is an interesting situation that I highlighted to Special Situation Investing subscribers in early December when the merger spread was at 21%.

In October, spinal implant and bone growth therapy device producer SeaSpine (NASDAQ:SPNE) entered into a strategic merger of equals with peer Orthofix (NASDAQ:OFIX). SPNE shareholders are set to receive 0.4163 shares of OFIX per each SPNE. The merger will require shareholder approvals from both OFIX and SPNE, with shareholder meetings set for January 4. Transaction closing is expected in Q1'23. Borrow is widely available at a 0.41% annual fee. Shortly after the merger announcement, in November, the spread settled at only 1-2%.

Author's calculations

The spread, however, increased substantially this month as private equity firms have shown interest in acquiring the buyer OFIX itself and the market seemed to price in the risk of the initial merger breaking. In early December, a consortium of two PE firms filed a non-binding $23/share offer to acquire OFIX. The offer was rejected by OFIX's management. PE buyers promptly followed up with another bid at $24/share (24% premium to current levels), however, Orthofix's management did not budge and reiterated initial SPNE merger plans. Nevertheless, OFIX-SPNE merger spread remained elevated at 21% at the time of my initial highlight.

Since then, however, the spread has narrowed to the current 6%. This market reaction seems to be justified. The offer from a consortium of PE buyers comes at a rather opportunistic time as OFIX trades close to a 10+ year low impacted by recent macroeconomic headwinds (-40% YTD). Two rejected bids show that OFIX's management will not sell the business at a depressed share price. Moreover, two acquisition offers from a consortium of PE firms came within less than a week. Given that OFIX has not reported any other bid for close to a month now, another offer might be unlikely.

The situation now appears to have turned into a straightforward merger arb. Fortunately, there is still some meat left on the bone here for arb investors. The only thing that could derail the ongoing merger seems to be buyer's shareholder approval. Notably, upon the announcement of the merger with SPNE, OFIX share price dropped 19%. Having said that, it seems that the equity holders might eventually support the transaction:

It is also worth noting that during the sale process, SPNE attracted other acquisition interests. Merger proxy notes that in Sep'22 SPNE received another all-stock transaction proposal from an undisclosed company valuing SPNE at $8.60/share (versus current price of $7.54). Meanwhile, since September US medical device market has gone up (IHI ETF has risen 8%), suggesting the previous suitor might still be interested. This could potentially limit the downside on the long leg of the trade in the unlikely case the merger with OFIX breaks. Notably, however, the downside could still be sizable on the short leg.

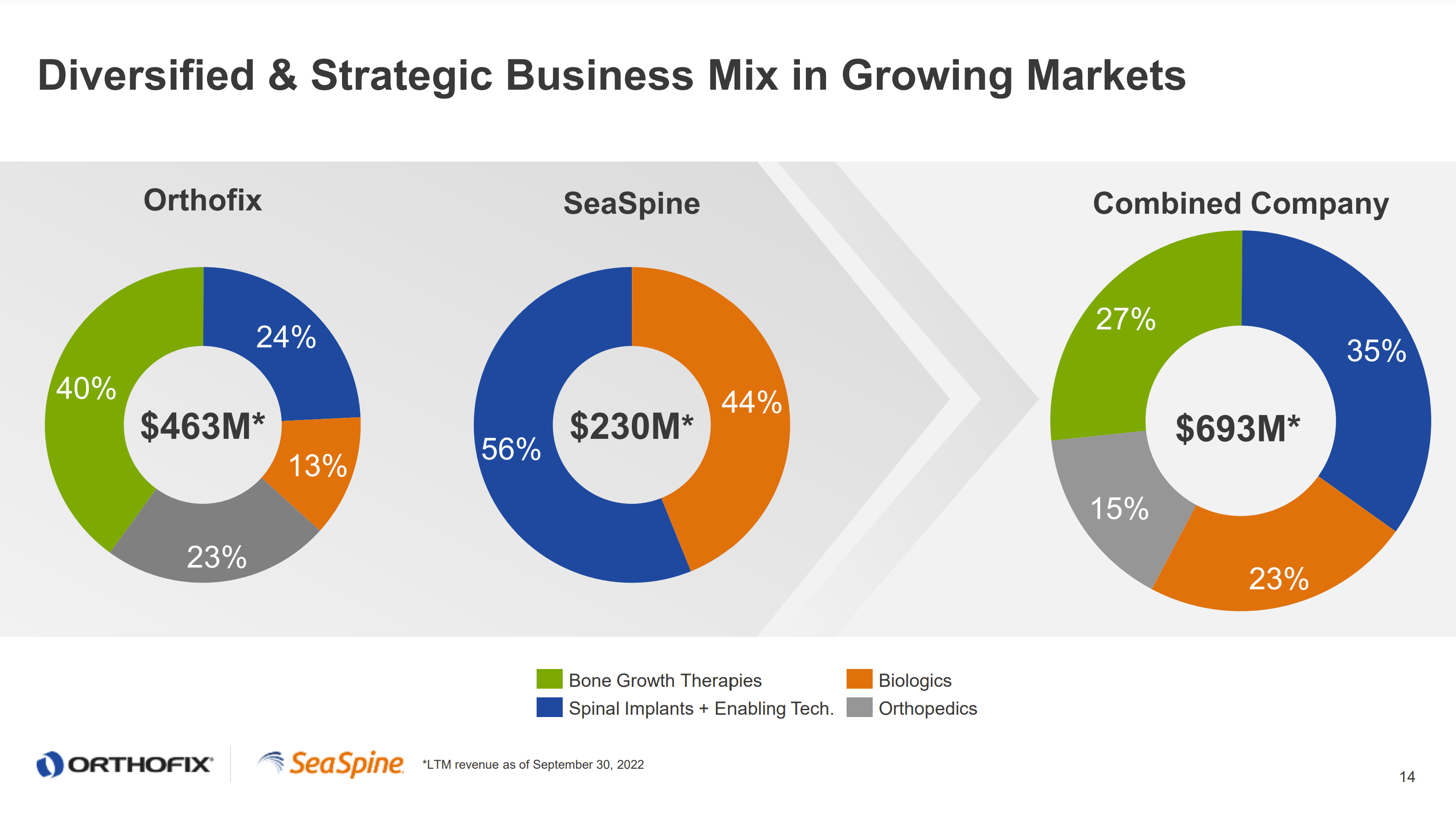

OFIX produces medical devices, with a focus on the spine (bone growth therapies, spinal implants and biologics, 77% of revenues) and orthopedics (i.e. fixation systems, 23%). 78% of total revenues are generated in the US. OFIX's growth has been rather stagnant in recent years, with sales staying at the same $460m-$470m range since 2019 other than a COVID-induced through in 2020 ($407m).

SPNE's offerings include orthobiologics (48% of sales) and spinal implants (52%). Orthobiologics offerings comprise bone graft substitutes intended to improve bone fusion rates. 90% of SPNE's sales come from the US. Unlike OFIX, SPNE has displayed a quite sizable growth, with sales expanding at 10% CAGR from 2018 through 2021, fueled by launches of new products and acquisitions (such as 7D Surgical).

Orthofix and SeaSpine Merger Presentation, November 1, 2022

Both companies have noted that the merger is intended to help the entities reach scale in the large $20bn TAM orthopedics medical device space. More specifically, management teams of both OFIX and SPNE have been confident about expanding in the fast-growing segments - making $7bn TAM out of the total $20bn - including enabling technologies, motion preservation, long bone stimulation therapies and pediatrics. Among other segments, the companies have emphasized combined enabling technology offerings where the combined entity is expected to possess a full continuum of surgical care offerings post-merger. SPNE's CEO has also highlighted the importance of combined company offerings in the pediatrics space.

With the current spread of 6% and likely closing in Q1'23, the ongoing OFIX-SPNE merger appears to be an interesting setup. Given sound strategic rationale for the buyer, I expect OFIX shareholders to approve the merger. Meanwhile, the downside on the long leg of the trade might potentially be limited by previous acquisition interests in SPNE.