Matteo Colombo

Matteo Colombo

Spire Global (NYSE:SPIR) grabbed my attention yesterday as the stock spiked by +30% intraday after news regarding collaboration with NVIDIA (NVDA). Digging deeper into details I found out that the stock price tripled over the last twelve months. However, as a small cap, SPIR is subject to massive shar price volatility and the company is at early innings of development. This means that it still burns cash, but there is a positive trend of shrinking losses as revenue grows. I could have been bullish about SPIR, considering bright prospects for the whole satellite data services market, but I have reservations about the company's balance sheet. The company is in the net debt position and still burns cash, meaning that the balance sheet is poised to continue deteriorating until sustainable positive free cash flows are achieved. Moreover, there is a big significant concern regarding a maturing in 2026 over $100 million in debt, which can be converted into stocks at a very low price. The 20% upside potential figured out by my valuation analysis does not look enough to me to outweigh all the risks and uncertainties and I give SPIR a "Hold" rating.

Spire Global is a relatively young company, founded in 2012 and went public in 2021. According to the latest 10-K report, SPIR is a global provider of space-based data and analytics that offers its customers unique datasets and insights about Earth. SPIR collects data through its proprietary constellation of multi-purpose nano-satellites.

SPIR's latest 10-K report

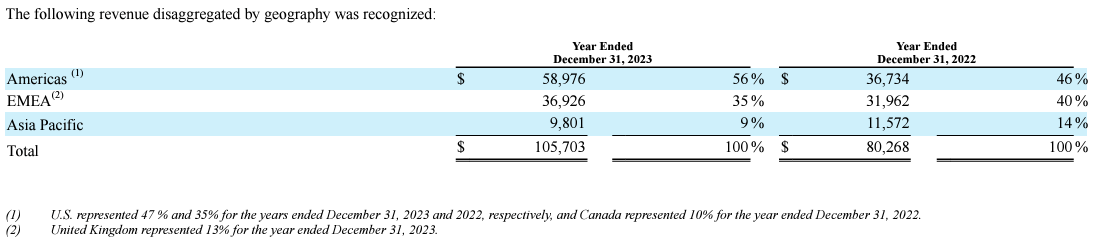

The company's fiscal year ends on December 31 and has only one reportable and operating segment. SPIR has plans to be present across diverse industries, but at the moment revenue is generated from four main solutions: Maritime [ship monitoring, safety, route optimization], Aviation [aircraft monitoring, safety, route optimization], Weather [forecasting], and Space Services [leveraging big data through its API infrastructure]. About half of the company's revenue is generated outside the U.S.

SPIR's latest 10-K report

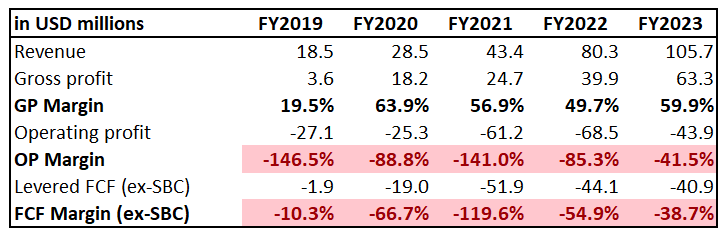

As usual, I am starting by zooming out and analyze key trends in financial performance over longer timeframes. Since SPIR went public relatively recently, the last five fiscal years is the longest available horizon. But it looks sufficient. Starting from a low base of below $20 million revenue in FY 2019, SPIR delivered a 55% topline CAGR. The gross margin is around 60% and the trend is positive. The operating loss is massive in relative terms, but the trend is also positive. It is also crucial to understand that operating in space industry means substantial investments in innovation and science.

Author's calculations

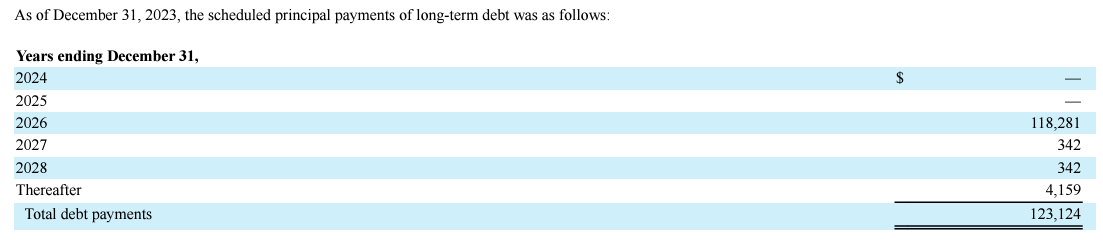

SPIR's free cash flow is deeply negative as well, and I want to emphasize more on the company's financial position. SPIR has a $118 million long-term loan maturing in 2026, which is expensive at around 13.6% interest rate as of December 31, 2023 [floating rate]. What potential investors should be aware of is that there is a credit agreement warrant which is exercisable for a total of around 1 million company's Class A shares at a per share exercise price of $5.44. This condition looks like posing big risks to the company's shareholders as it means that in case SPIR fails to repay the debt in 2026.

Author's calculations

According to the latest 10-K report, there were around 22 million outstanding shares of Class A as of February 23, 2024. This means that almost 5% of the company's Class A shares are subject to the warrant with exercise price three times lower than the current share price, which is substantial.

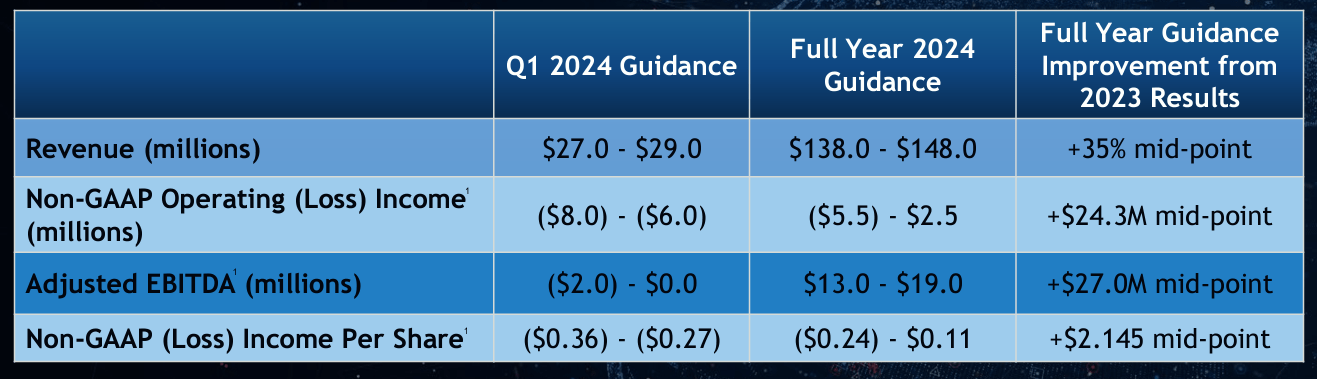

The maturing in 2026 large portion of the debt means the company has to accumulate a notable cash pile in 2024-2025 and I am quite uncertain about the ability to do it. Yes, the 2024 guidance has been upgraded during the latest earnings call, but a below $20 million adjusted EBITDA for the full fiscal 2024 still looks insignificant compared to the maturing in 2026 amount. Therefore, there is a substantial level of uncertainty regarding the ability to meet its obligations with cash in 2026. That said, there is a high probability that credit warrants will likely be exercised at much lower prices than the current levels.

SPIR's latest earnings presentation

Another significant risk that I see is that the company generates around 42% of its sales with governmental bodies. Thus, the lion's portion of the company's revenue is heavily dependent on governmental budgets and spending as well as changes in local administrations, for example. Moreover, working more with governmental bodies highly likely means greater scrutiny of SPIR's activities from regulators. This might mean elevated legal and compliance costs.

Overall, I have mixed opinion about SPIR. On the one hand, the company expands the top line with the massive pace and has solid trend in profitability metrics improvement. But the maturing in 2026 vast portion of debt is a big issue, especially considering warrants with a low exercise price.

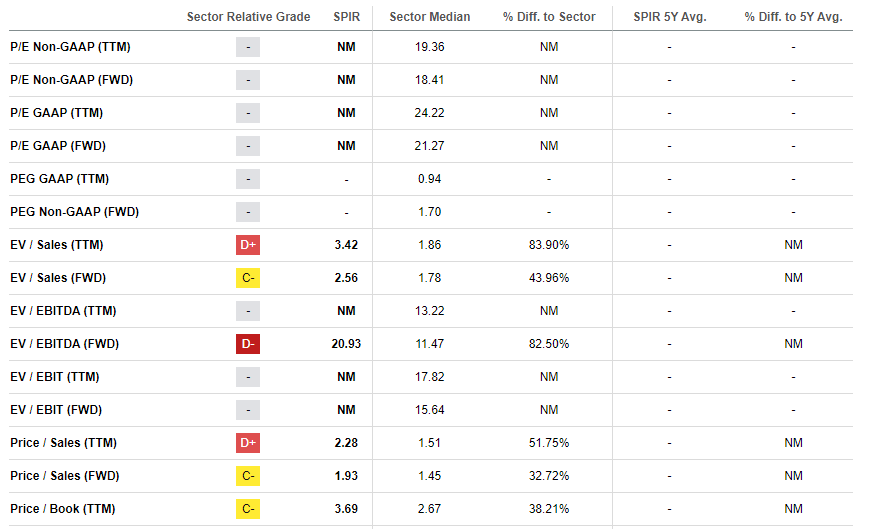

SPIR almost tripled in price over the last twelve months and doubled since inception of 2024. Most of the valuation ratios are unavailable since the company is not profitable yet. However, I must emphasize that Price/Sales ratio does not look very high given the company's rapid revenue growth. This might indicate undervaluation, but I also must simulate the discounted cash flow [DCF] model for more conviction.

Seeking Alpha

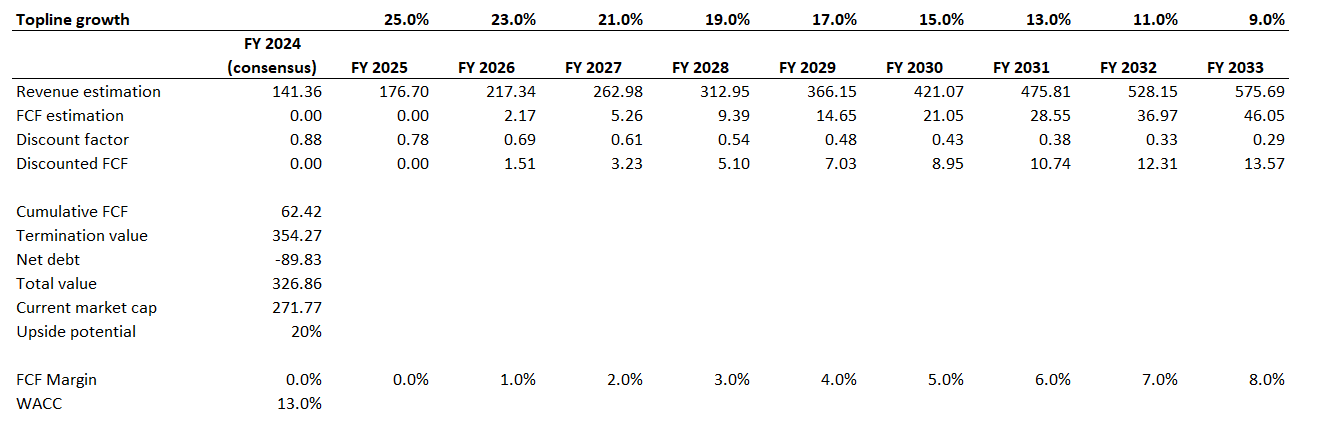

Due to the company's size and substantial level of uncertainty regarding profitability timing I am using an elevated 13% WACC. I use FY 2024 revenue consensus estimates, project a 25% revenue growth in FY 2025 with further two percentage points yearly deceleration. All in all, the next decade's CAGR is projected at 17%, which looks fair considering the 55% CAGR over the last five years. I expect zero FCF margin for FY 2024-2025 and the metric to start expanding by one percentage point yearly starting from FY 2026. I also subtract the net debt figure from my fair value calculations.

Author's calculation

According to my DCF simulation, the fair value of the business is around $327 million. This is 20% higher than the current market cap but this upside potential does not look attractive enough to me considering all the risks and uncertainties.

Investing in small caps, especially that are not yet profitable, is extremely risky. Small caps tend to be much more volatile than stocks of larger companies. For example, the fact that yesterday the stock spiked by 30% after headlines about partnership with NVIDIA. Since it looks like everything NVIDIA touches nowadays becomes gold, this rally due to the partnership with NVDA might sustain for longer. There are not much details regarding the collaboration yet, but only having NVDA mentioned in the same headlines with SPIR helps the stock to spike.

SPIR operates in a hot industry, and I might be missing the new "next big thing" with my excessive caution. According to Straits Research, the satellite data services market is projected to compound with a 27.7% CAGR between 2023 and 2021, which is a massive industry tailwind behind SPIR's back.

Strategic partnership with the cutting-edge AI company like NVDA multiplied by industry tailwinds might be a robust blend to build long-term value for shareholders. Even in case the stock drops massively as a result of credit warrants exercised by the lender at $5.44 per share, this does not mean that SPIR can potentially become an x-bagger on a multidecade horizon.

To conclude, SPIR might become a new superstar in the thriving industry. But the company is so young that it is difficult to have high conviction here. Moreover, there is a big red flag in the company's balance sheet. All in all, I give SPIR a "Hold" rating.