imaginima

imaginima

In this article, we take a look at the recently launched Calamos CEF Income & Arbitrage ETF (NYSEARCA:CCEF). The idea behind the fund is to generate both high income and look for value opportunities such as closed-end funds, or CEFs, trading at wide discounts that could generate capital gains.

The idea is not new - funds-of-funds and, funds-of-CEFs specifically - have been around for a long while, and there are around a dozen of them now. CCEF is a very small fund and it may not survive for long; however, it does give us an opportunity to highlight some of the claims it shares with other similar funds as well as discuss this niche sector.

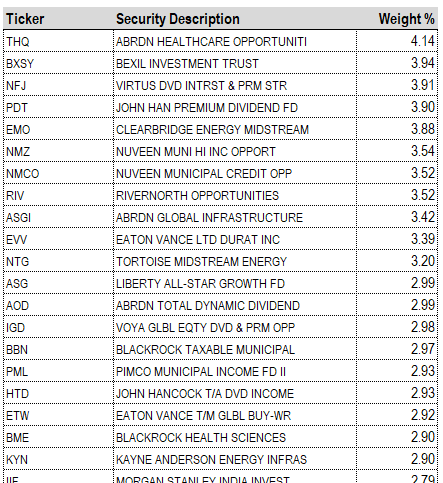

CCEF is an exchange-traded fund, or ETF, of CEFs. It has a fee of 0.74% and is about a month old. It has 35 CEF holdings as of this writing, with the largest shown below.

Calamos

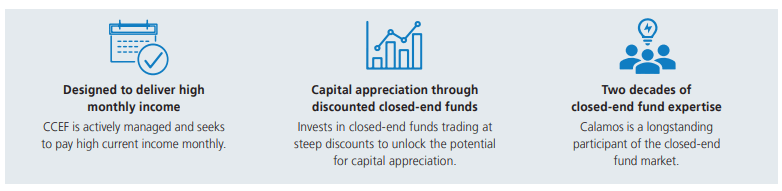

As expected, when funds are launched, managers highlight a number of advantages their fund will bring to investors or opportunities in the market that they will capture. In the case of CCEF, there are three main points listed in its launch sheet.

Calamos

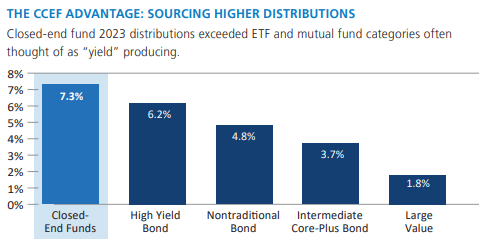

First, it is designed to deliver a high monthly income level. Calamos supports this by showing that CEFs deliver a higher income than the more traditional assets like high-yield bonds (by which they mean high-yield bond open-end funds like TFs).

Calamos

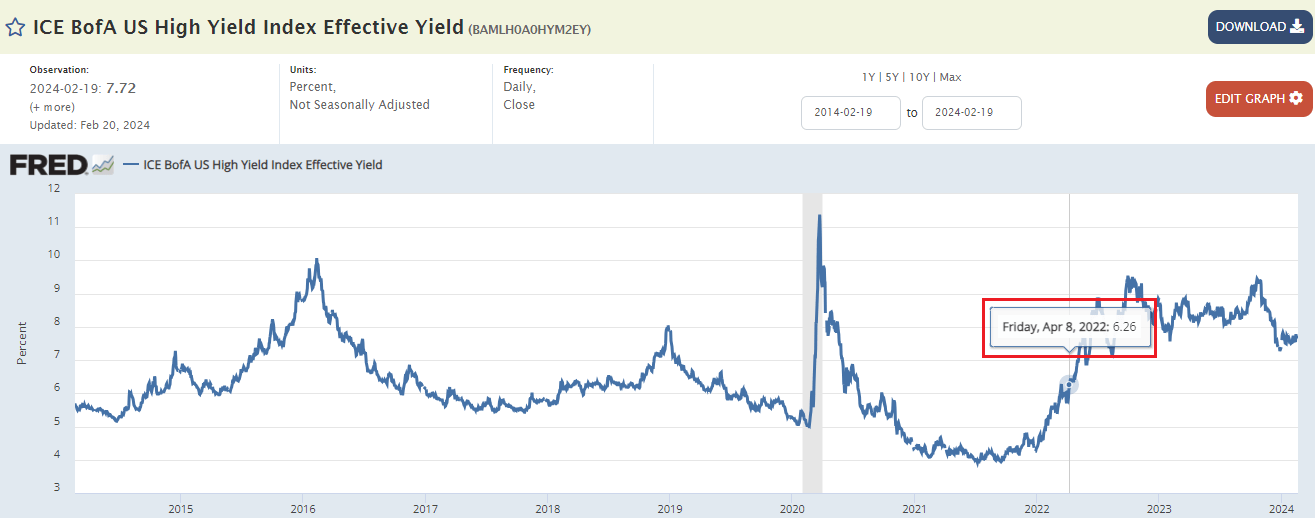

There are several issues with this yield representation. One, it's embarrassingly misleading to suggest that "High Yield Bond" yields are 6.2%. The last time this was the case was in April of 2022 - a bit out of date for marketing materials of a fund that launched this year. The legend should say "High Yield Bond ETFs," however, even this would be very misleading, as we discuss further.

FRED

Two, it ignores the distinction between current yield and yield-to-worst. Three, it does not address the fact that CEFs tend to overdistribute, while ETFs tend to under-distribute relative to their portfolio yield, particularly in the current environment when bonds are mostly trading below par. And four, it ignores the high fee of CCEF itself.

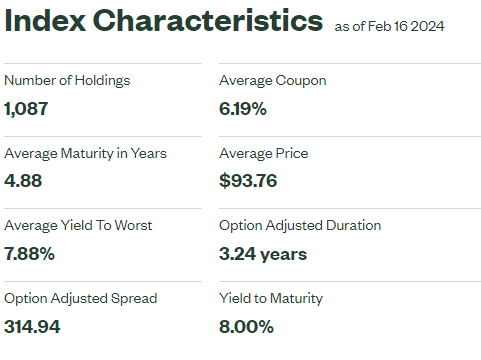

The high-yield corporate bond market looks roughly like the following table, taken from the index tracker SPDR Bloomberg High Yield Bond ETF (JNK). The fund has a distribution yield of 6.74%, which is roughly a function of its actual income, i.e., 6.19% / $93.76 x $100 = $6.60 before fees. However, its underlying yield is actually 7.88% yield-to-worst less the 0.4% fee or around 7.5% - well above its distribution yield. By focusing on ETF distributions rather than their underlying portfolio yield-to-worst, Calamos overstates the advantage of CEFs vs. ETFs for HY corporate bonds.

State St

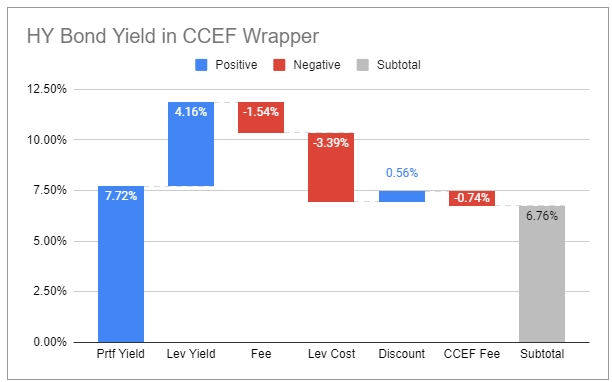

Let's have a look at what happens to a HY corporate bond inside a CCEF wrapper. We start off with the weighted-average HY corporate bond yield of 7.72% (taken from FRED which is slightly different from the 7.88% number shown by JNK due to timing and index differences) and assume standard CEF parameters of 35% leverage, 1% total fees (management fees + sundry expenses), 6.3% leverage cost (roughly SOFR + 1%), an average CEF discount and the 0.74% management fee of CCEF itself and end up with 6.76%. In other words, starting with an average HY corporate bond we lose 1% in yield by going through the CEF and then the CCEF wrappers.

Systematic Income

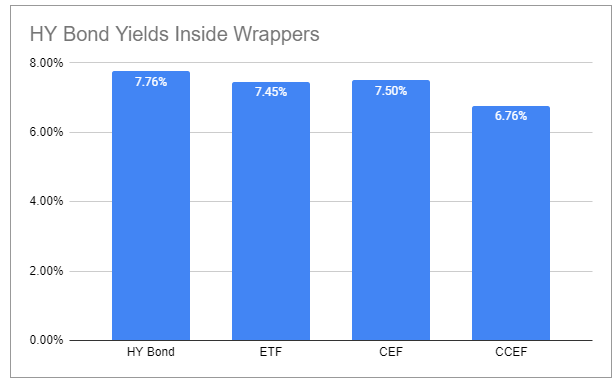

To summarize the situation, investors can hold HY corporate bonds in (at least) 4 different ways - individually (at a yield of 7.76% on average), via an ETF wrapper (at a yield of 7.45% assuming an average passive ETF fee of 0.31%), via a CEF wrapper (at a yield of 7.5% - see chart above prior to the -0.74% CCEF fee) and via CCEF (at a 6.76% yield). In other words, while Calamos implies in their chart that CCEF offers the highest-yielding option for HY corporate bonds, the situation is exactly reversed through a number of sleights-of-hand such as ignoring the fee of CCEF itself and conflating income, i.e., current yield (which ignores pull-to-par) and yield-to-worst.

Systematic Income

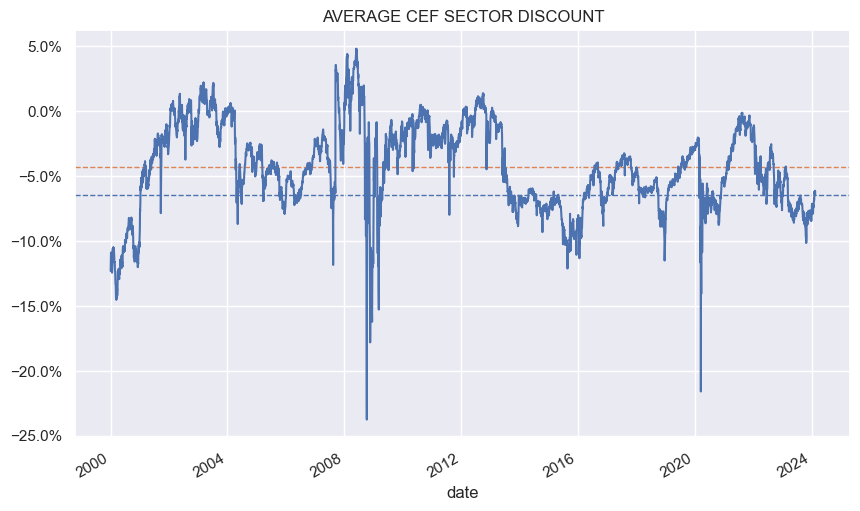

The second selling point of the fund is "Capital appreciation through discounted closed-end funds." The idea seems to be that CEFs trading at a wide discount could drive gains through the tightening of the discount. It's true that CEF discounts are pretty wide, however, they are not that wide relative to history. As the following chart shows, the average CEF sector discount is only a couple of percentage points wider of its historic average.

Systematic Income

As many CEF investors know, CEF discounts are driven by risk sentiment and leverage costs, among other factors. Leverage costs are due to fall, which should tighten discounts somewhat. However, risk sentiment is very strong, so it's unlikely this factor will be instrumental in pushing discounts much tighter from here. In fact, the risk is that sentiment falls from its very high level, pushing discounts wider.

The third selling point of the fund is that "Calamos is a long-standing participant of the CEF market, with two decades of CEF expertise." However, it's important to highlight that being a long-standing participant in the CEF market and CEF expertise are not quite the same thing. We are all long-standing participants in the grocery shopping business, but few of us are experts in the grocery business itself.

As far as its CEF involvement, Calamos mostly manages convertible bonds in CEF wrappers, which is not the same thing as managing diverse CEFs across different sectors. There are two leaps of faith here - one, that convertible bond expertise translates to sectors other than convertible bonds such as legacy residential mortgages or utility stocks, and two, that managing portfolios of individual securities translates into managing a portfolio of CEFs.

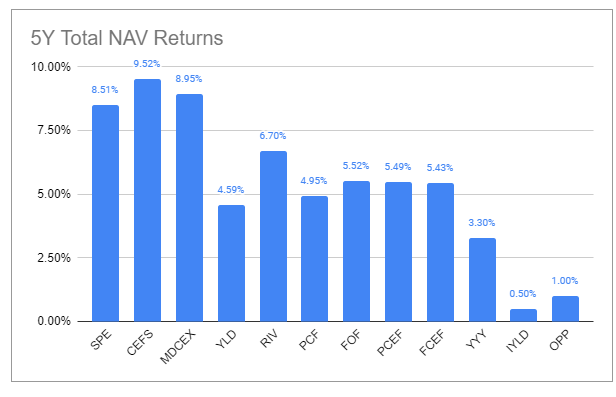

There is wide variation in the fund-of-CEFs space across investment vehicles, strategies, holdings and returns. The chart below shows the 5Y total return of the funds we track. Some of these funds don't exclusively hold CEFs such as Special Opportunities Fund (SPE), however, most do.

Systematic Income

The advantage of the CEF structure over the ETF and mutual fund counterpart is the presence of a discount as well as locked-in capital, which means the given fund doesn’t need to trade the underlying positions in line with its flows.

Interestingly, the best performers in this part of the market have been the ETF CEFS, CEF SPE and mutual fund Matisse Discounted Closed-End Fund Strategy Inst (MDCEX). Not only are the best performers in different types of investment vehicles, but their strong performance is also for different reasons.

CEFS is run by the best-known CEF activist Saba. Its performance has been strong because of a small number of concentrated CEF bets as well as their actual CEF activism. The performance of SPE has been strong because of its partial allocation to BDCs and SPACs. BDCs have significantly outperformed CEFs over the last few years, while SPACs have been relatively resilient. The performance of MDCEX has been strong in large part because of its relatively high equity CEF allocation.

In this article, we interrogated some of the key selling points of a new ETF of CEFs. Although CCEF itself may not last, understanding some of the claims funds-of-funds make can help investors get a better understanding of this market niche. Overall, we continue to like the trio of CEFS, SPE and MDCEX in the fund-of-CEF sector. Investors who like the activist / concentrated bet portfolio of CEFS should have a look at Calamos CEF Income & Arbitrage ETF, while those who want a more balanced fixed-income / equity portfolio should have a look at MDCEX.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.