littleclie

littleclie

Despite my penchant to write about economics quite a bit, my undergraduate degree was in History. It's rare for me to write in historical metaphors, but I'm always tempted to - this time, that impulse won.

One of the papers I wrote back in college was about the Treaty of Karlowitz, signed in 1699 to end the Great Turkish War, where a coalition of European powers defeated the Ottoman Empire (now Türkiye) and stopped their expansion further into mainland Europe.

Figure 1 (Derek Davison)

From then on, the Ottomans would never reach the size of their pre-1699 conquests, where they reached all the way to Vienna. Throughout the 18th and 19th centuries, the Ottomans continued to lose land to mainland powers until their defeat in World War I ended the empire for good.

During this centuries-long decline, politicians and newspapers began to describe the Ottomans using a phrase of somewhat dubious origins, "The Sick Man of Europe." This epithet was designed not only to humiliate the Ottomans but to describe a state in general decline.

Today, Europe has a new sick man: the United Kingdom.

I'll drop the history metaphor now, but if you'd like to read more about this event, I recommend Derek Davison's newsletter, Foreign Exchanges.

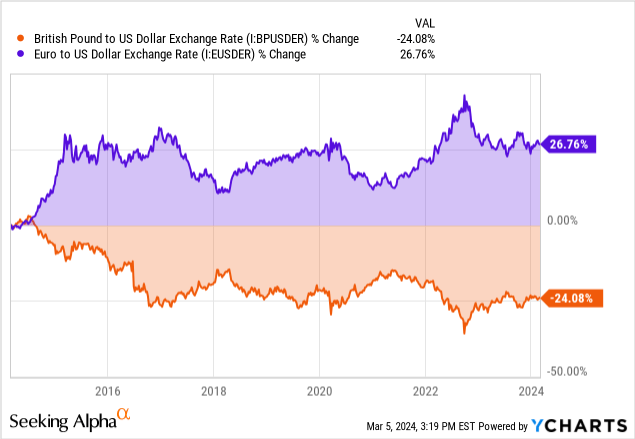

The UK got the worst of the 2022 stagflation crisis, with the British pound suffering against the dollar. The widening gap between the GBP exchange with the dollar and the EUR exchange has continued to grow and exacerbate in the last ten years.

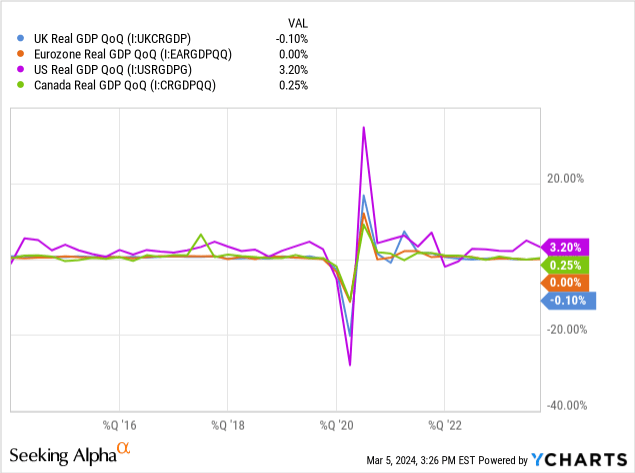

Not only did the UK experience lower GDP growth compared to their EU and North American peers, but they also experienced worse inflation. In this sample, the UK is even declining while the Eurozone stays flat, and North America reports growth.

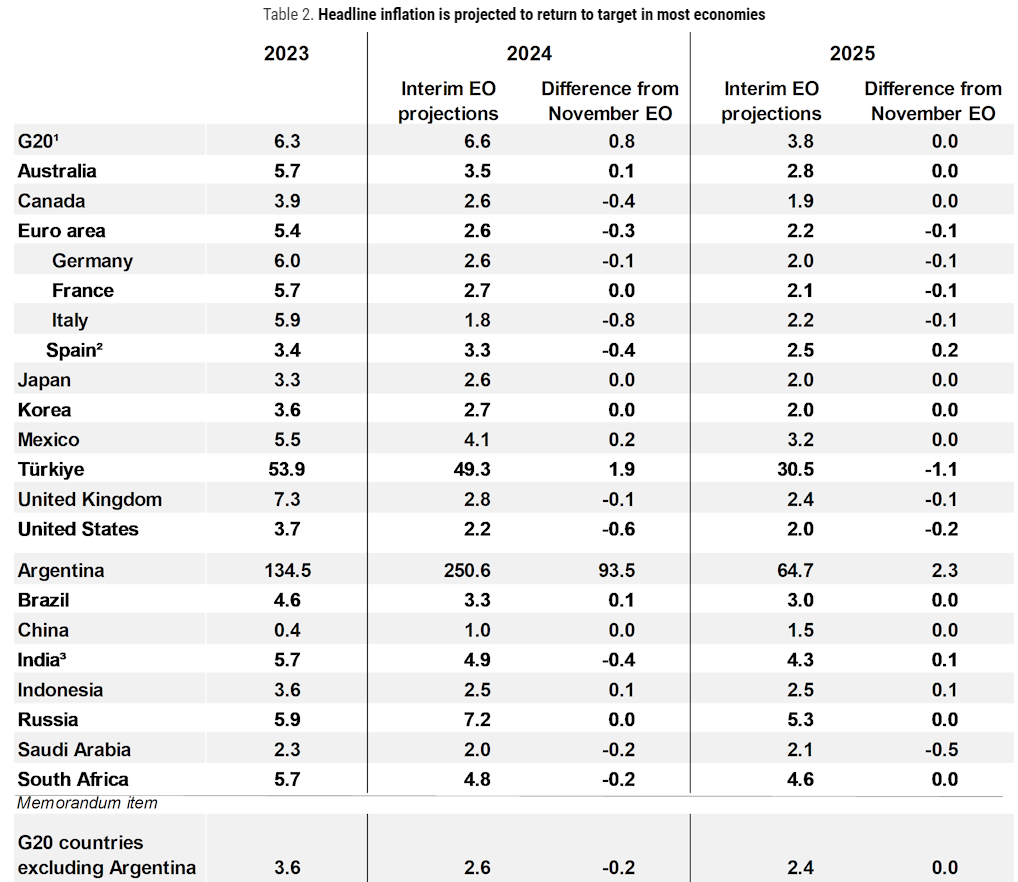

The UK's inflation in 2023 was double that of G20 averages, with no developed country in the bloc experiencing it worse. The average across G20 countries was 6.3%, with that falling to 3.6% if you exclude the outliers of Argentina and Türkiye.

Some things never change: Türkiye is still sick. That's for another article.

Figure 2 (OECD)

News rattled the OECD last month when the UK fell into a technical recession, with GDP figures declining for six straight months.

This hitch hasn't let up yet, and we will have to see in Q2 of this year how things shake out. For now, they are not looking great.

The actual damage that we need to worry about is the damage to the government that a technical recession presents. Currently, the Conservative Party ("the Tories") runs the show and has since 2019.

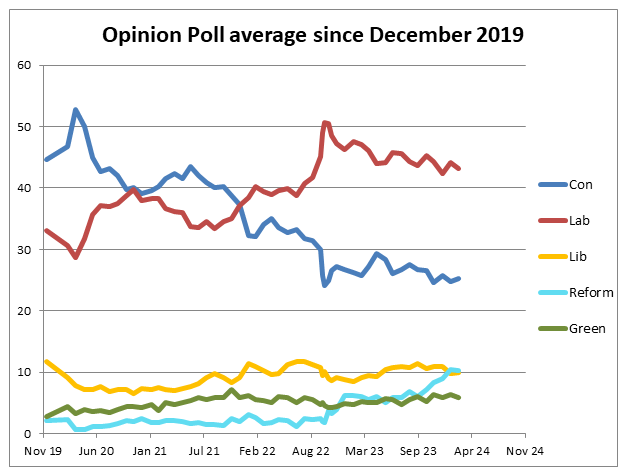

Public opinion regarding the conservative government's efficacy has fallen steadily after it peaked in the Summer of 2020. Stagflation and the subsequent recessionary economy that followed have tanked public opinion of the current regime.

Figure 3 (Electoral Calculus)

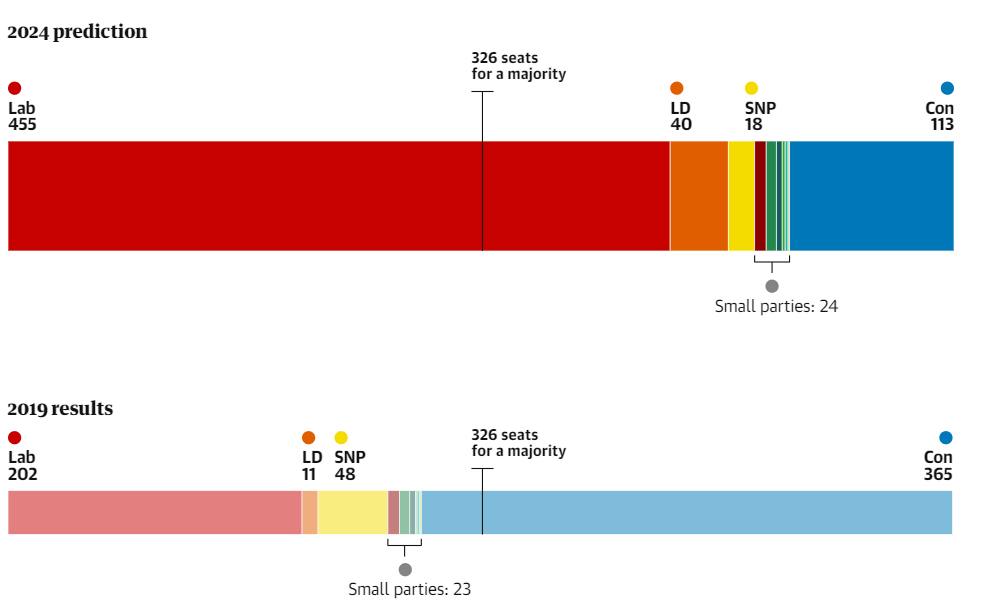

This has led to a shift in opinion that now favors the Labor Party, the primary opposition to the Tories. The shift is so great that projections for this year's election show Labor winning more seats than the Tories won back in 2019.

Figure 4 (Electoral Calculus)

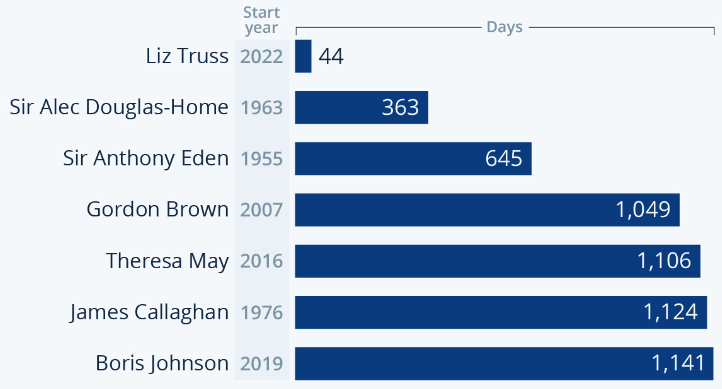

The Tories have had a tumultuous tenure since their majority rule was established in 2019. Since then, they have had three different prime ministers. Two of them, Boris Johnson and Liz Truss, rank in the shortest PM tenures in UK history (since 1945).

Figure 5 (Statista)

Rishi Sunak, the current PM, is on track to join that list, only having been in power since October 2022, and is predicted to lose this year when a Labor PM takes his place.

This has only added to the perceived weakness the Tories have and has all but cemented their loss this year.

So, can labor fix this? They say they can. Any political party in their position would.

The party's current stance on the economy falls in line with reality: it's bad and needs fixing. Here is a statement from their website:

The British economy has been growing at the slowest rate for two centuries under the Tories. And the small amounts of growth it has seen have not benefited the whole country. The result is the biggest fall in living standards in a generation.

It should be the case that if you work hard and play by the rules, you will get on. But for millions of people that is simply not the case. People are working harder than ever but too often for less reward.

For too long we have lacked economic stability, an industrial strategy, or enough public and private investment to kickstart growth. There has not been a willingness to reform outdated planning laws that restrict the building of vital new homes and infrastructure.

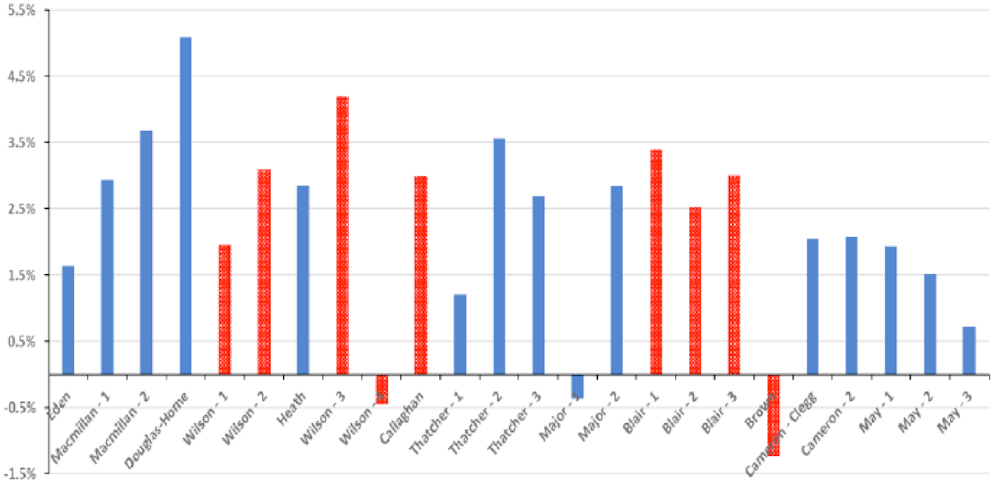

Has Labor been able to grow the economy in the past?

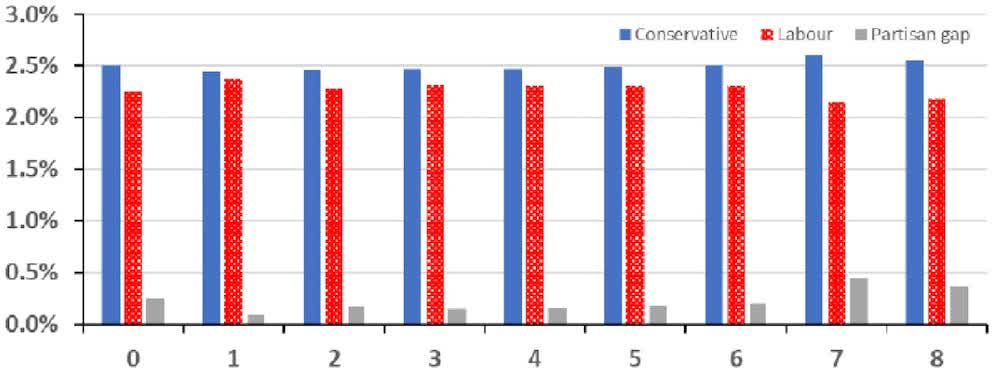

Historically, not much more than the Tories. Below, the blue bars are Tory governments, and the red bars are Labor governments going back to 1955 and ending with Theresa May's government that ended in 2019.

Figure 6 (Journal of Econ. & Business Letters)

Looking at lagged results does not end up much better for Labor, with a partisan gap emerging between Tory and Labor GDP growth. As you account for more and more time (lagging additional quarters), the partisan gap widens.

Figure 7 (Journal of Econ. & Business Letters)

The difference in GDP growth is miniscule, less than 0.5% in all cases. Labor doesn't have any better track record than Tory governments when it comes to the economy.

I have two trade ideas that come out of this analysis.

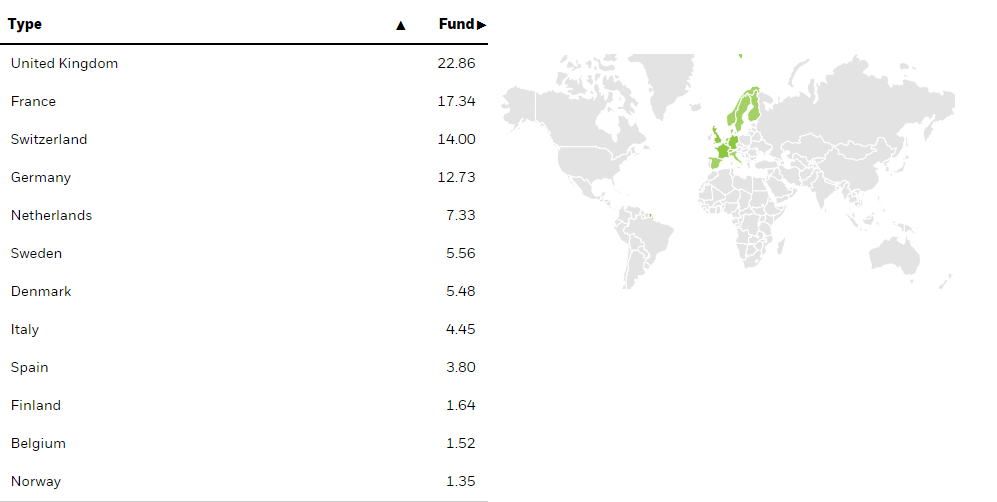

The goal of both of these trades is to avoid British exposure in your international exposure. When looking at European funds like the iShares Core MSCI Europe ETF (IEUR), it is dominated by UK corporations.

Figure 8 (iShares ETFs)

This fund is to be avoided, along with other international ETFs with heavy UK exposure like VEA.

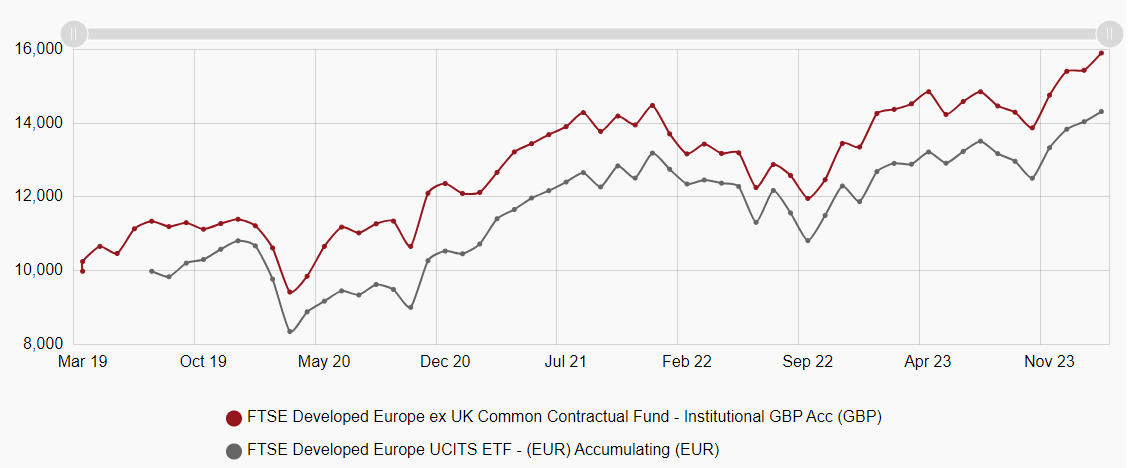

When we plot the returns of developed Europe with and without the UK, we see a stark and consistent gap in performance, led by lower UK growth compared to its European peers.

Figure 9 (Vanguard)

This leads to my first trade idea, and one I intend to initiate in the coming weeks.

I intend to take a pair trade with the UK against the wider Eurozone. I want to bank on the outperformance of the euro against the pound when paired against the dollar, as well as the outperformance of the wider Eurozone compared to UK companies.

I would go long a fund like the iShares MSCI Eurozone ETF (BATS:EZU) and short the iShares MSCI United Kingdom ETF (NYSEARCA:EWU).

That would look like 100% EZU, -100% EWU, with the proceeds of the short sale held in cash.

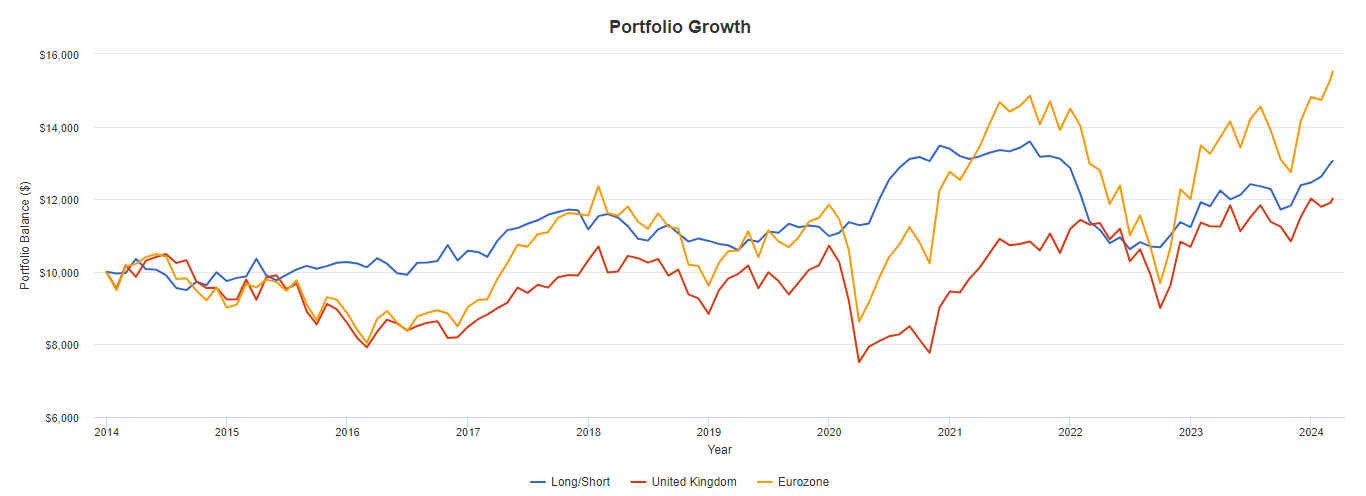

In the last four years, this trade would've done very well from a risk/reward standpoint.

Figure 10 (Portfolio Visualizer)

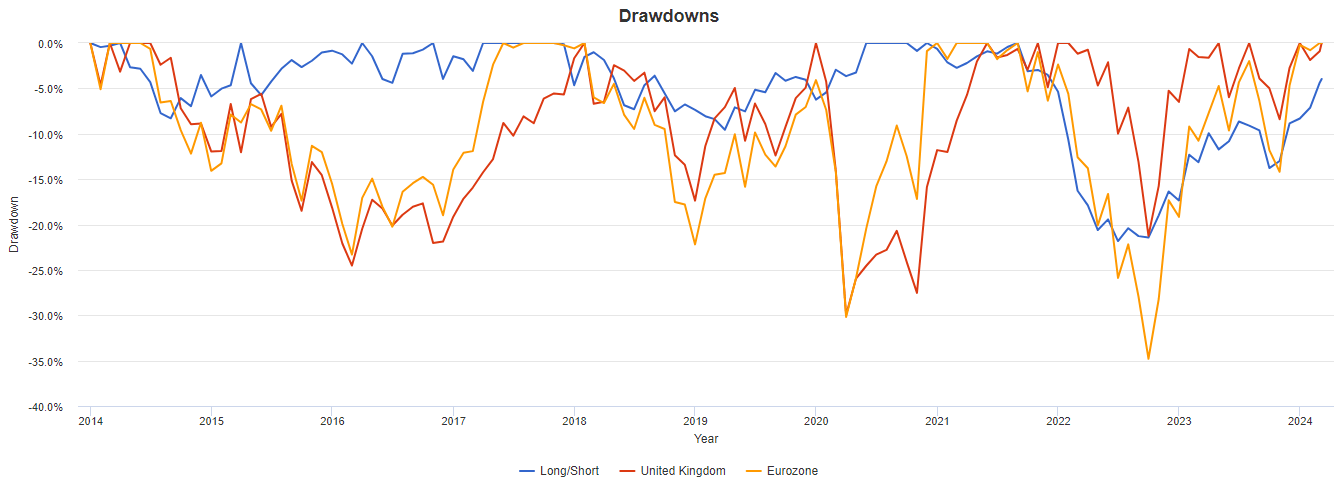

Of course, when you take a pair trade, you will typically underperform a long-only index on the upside and outperform on the downside. This is better demonstrated with this trade's drawdowns against the long-only ETFs.

Figure 11 (Portfolio Visualizer)

Despite the Eurozone's reputation as being uncompetitive on the business front with US firms, I believe there is still growth left in the larger cap companies that have dominated large swaths of the market.

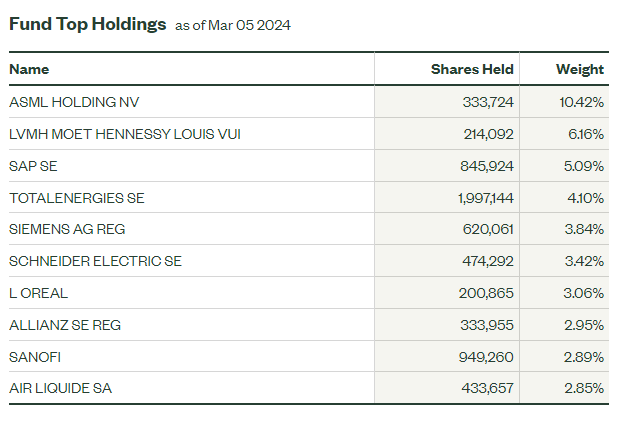

To this end, my second trade idea is to focus on the Eurozone's largest companies, which are conglomerates and global brands like ASML Holding (ASML), Louis Vuitton (OTCPK:LVMHF), SAP SE (OTCPK:SAPGF), etc.

The SPDR EURO STOXX 50 ETF (FEZ) is the perfect candidate for this. It has no holdings in the UK, Switzerland, or Sweden, which have economic partnerships with the European Union but do not use the euro.

Figure 12 (SPDR)

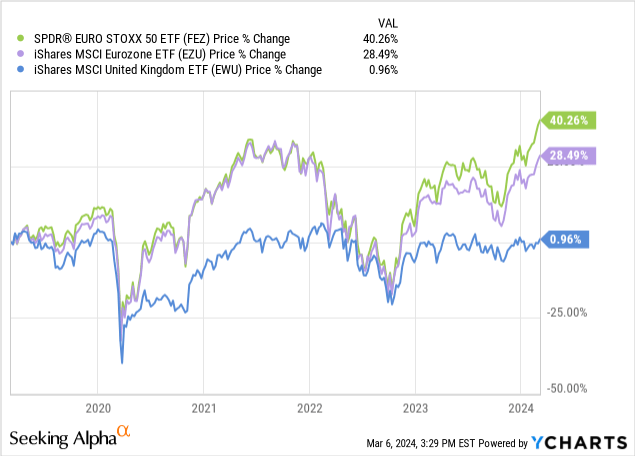

It has performed admirably in the last few years, especially when put against its UK counterpart.

Europe's new sick man is the UK. Since its economy has been ravaged by the pandemic, Brexit, and a string of weak governments, the UK has failed to materialize much of the same drive that companies in the Eurozone have. The pound is in trouble and has been left behind by the euro and the dollar.

My two trade ideas are to take a long-only position in the EURO STOXX 50 via FEZ and to take a pair-trade of going long the Eurozone via EZU and short the UK via EWU at a 1:1 rate, isolating general market risk and benefiting from just the differences in currency and idiosyncratic business development.

I would love to hear other trade ideas in the comments.

Thanks for reading.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.