Wachiwit/iStock Editorial via Getty Images

Wachiwit/iStock Editorial via Getty Images

Following disappointing Q3 results for the Game and Network Services segment, Sony Group Corporation (OTCPK:SNEJF) (NYSE:SONY) stock has declined even as the rest of the business remains sound. There are possible catalysts that may improve the situation for this segment, such as the release of the PS5 Pro; however, it seems that there are also broader trends within the industry that Sony likely does not have full control over. Taking into account the performance of other segments, as well as possibilities for improvement in the G&NS segment, the drop seems overdone, presenting a possible entry point.

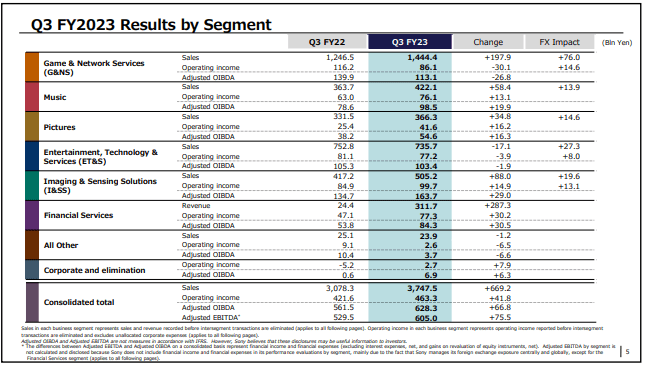

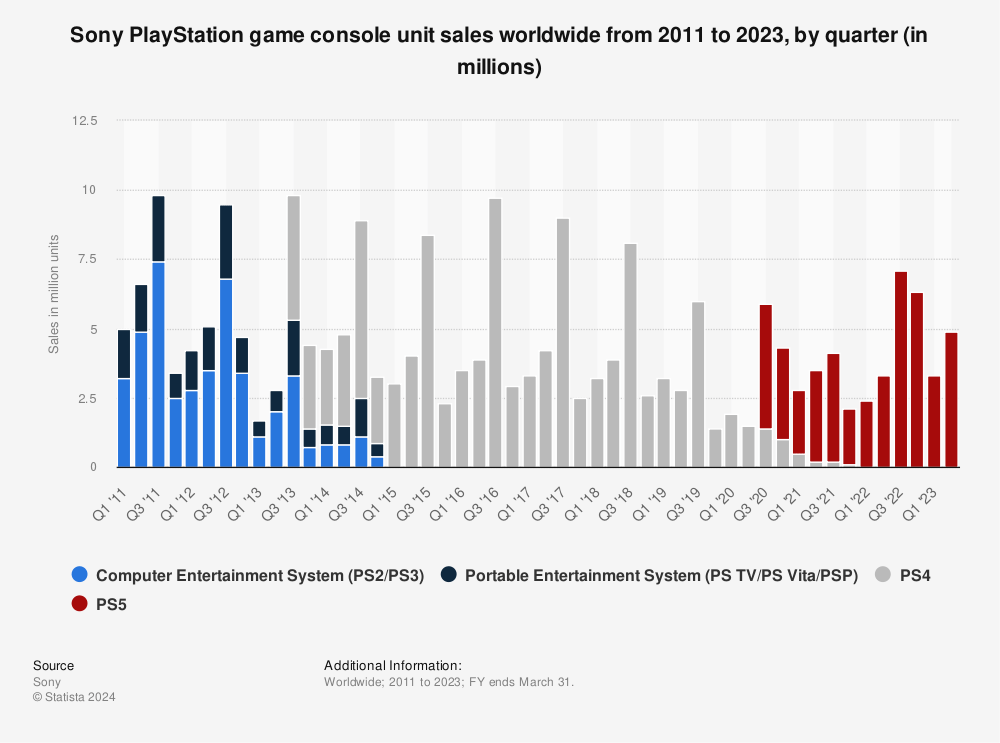

Overall, both sales and operating income for the quarter increased YoY, the former hitting ¥3,747.5 billion, up 22% and the latter ¥463.3 billion, up almost 10%. The G&NS segment had some underwhelming results, with 8.2 million PS5 units sold in Q3, lower than expected by about 1 million units. Furthermore, operating margin dropped to 5.96% for from over 9% last year despite growing sales. Sony only expects a slight increase next year in operating income in this segment, citing first-party profit declining, but being countered by more third-party growth.

Sony Q3 Results (Sony Q3 earnings presentation)

Other segments generally performed better with Imaging & Sensing Solutions showing significant growth with sales growing 22% and operating income 17.5% respectively. The Music segment saw good growth, as did Pictures while ET&S saw a slight decline due to lower sales of televisions and a lack of expected growth from the North American region. The Pictures segment was impacted by the Hollywood strikes this year by about ¥20 million, but the effect is expected to peak next fiscal year. Crunchyroll (the anime streaming service) continues to drive growth in the Pictures segment, exceeding ¥13 million in revenue and averaging 23% growth annually since the 2021 acquisition.

Those PS5 sales numbers may be the eye-catching news, but the operating margin of 5.96% is at least as big a problem. So what caused it? Hiroki Totoki cited high hardware costs associated with chips and other components as an explanation, but I think software plays a large role in this. Simply put, the cost to create AAA titles has ballooned since the PS4 development cycle. A CMA report from last year revealed that many AAA titles now cost $200+ million to make, excluding hefty marketing budgets, which can boost that number much higher. Presumably to cut said costs, Sony just announced layoffs of 900 workers, amounting to 8% of the Interactive Entertainment unit.

Further, as highlighted below, there is potentially going to be a bit of a drought of big new titles next year.

Sadahiko Hayakawa, Q3 earnings call:

But while major projects are currently under development, we do not plan to release any new major existing franchise titles next fiscal year, like God of War Ragnarok and Marvel's Spider-Man 2.

This is a significant problem because, to an extent, software drives hardware sales. PS5 numbers are already underwhelming currently, this could increase the likelihood that next year continues that trend. For the G&NS segment, the performance is already negative and if there are no catalysts on the software side of things it is concerning.

Sony is not alone in cutting its workforce. In fact, currently it seems to be the norm, with Electronic Arts (NASDAQ:EA) cutting 5% of its workforce, Microsoft (NASDAQ:MSFT) cutting 1,900 and Unity (NYSE:U) 1,800. There is also a kind of phase change in the gaming industry away from the era of exclusive titles, with Sony and Microsoft increasingly porting their games to PC. The latest news is that Microsoft is now also bringing four exclusives to PS5. Hiroki Totoki highlights Sony's perspective on exclusivity below.

Hiroki Totoki, Q3:

And the other potential driver is the first-party title generation because in the past, as you all know, we wanted to popularize console. And title was something -- and the first-party title may purpose was to make the hardware or the console popular, right? It is true, right? But there is a synergy to it. So if we have a strong first-party content, not only with our console, but also other platform like computers. And the first-party can be grown with multi-platforms and that can help operating profit to improve.

Live service shooter game Helldivers 2 recently shipped on PS5/PC simultaneously, becoming the most successful PlayStation launch on PC ever. In many ways, this game epitomizes the new exclusivity approach, which tries to straddle the PS5 and PC markets. The numbers on PS5 remain to be seen, with the data for consoles always being more opaque, but Sony will likely be increasingly encouraged in the PC market.

However, this changing landscape for gaming generates some uncertainty. If the trend continues and true exclusivity is increasingly uncommon, what separates PlayStation as an ecosystem from Xbox or PC? There is a reason Nintendo still maintains exclusivity because it builds and maintains an ecosystem. An ecosystem that is accessible only through Nintendo hardware. The pivot away from exclusives, eventually maybe away from consoles, is certainly a way to drive profitability but may also erode Sony's moat in this segment. It is a balancing act, one which Sony is currently pulling off, but the trend suggests it may go too far.

On the plus side, as a result of the increasing third-party engagement, MAU was up significantly with total game play time up 13% YoY and a record 120 million active users on PSN. This was apparently not enough to drive profitability, although Sony could look to this as something that could in the future.

There is increasing consensus among analysts that the PS5 pro may be released in the latter half of this year. Although exact figures for PS4 Pro sales are hard to come by, as seen below, the release of the PS4 Pro in late 2016 helped sustain sales on a unit basis and the effect on revenue would have been greater because of the higher pricing. On that note, the PS4 Pro was $399 on release, but this time around will likely be over $499, the price of the base PS5. If Sony can position the PS5 Pro release correctly in time for the massively anticipated GTA VI, paired with a more premium pricing, that could be one way to turn things around.

Statista, Sony

It is now over a year since the PSVR2 released and was reported to have sold 600,000 units 6 weeks post release. Fast-forward to now and as part of the recent layoffs, the entire PlayStation London studio has been closed, which largely worked on VR titles. The pivot to PC continues here, too, with Sony having recently indicated PC support for the PSVR2 is coming sometime this year. Apart from that, Sony has been quiet as regards the PSVR2, which combined with their other actions suggests the latest moves are a strategy to improve profitability. Although VR hype has largely dissipated, there is still a possibility that new products like the Vision Pro reignite interest in the area.

The PS5 Pro and layoffs might not be enough though, and I suspect does not address the underlying problem. Underwhelming operating margin could become a persistent issue if the cost of AAA game development rises unchecked. Staff layoffs might ameliorate this if they are targeted in the right places, but I suspect this cost will prove sticky.

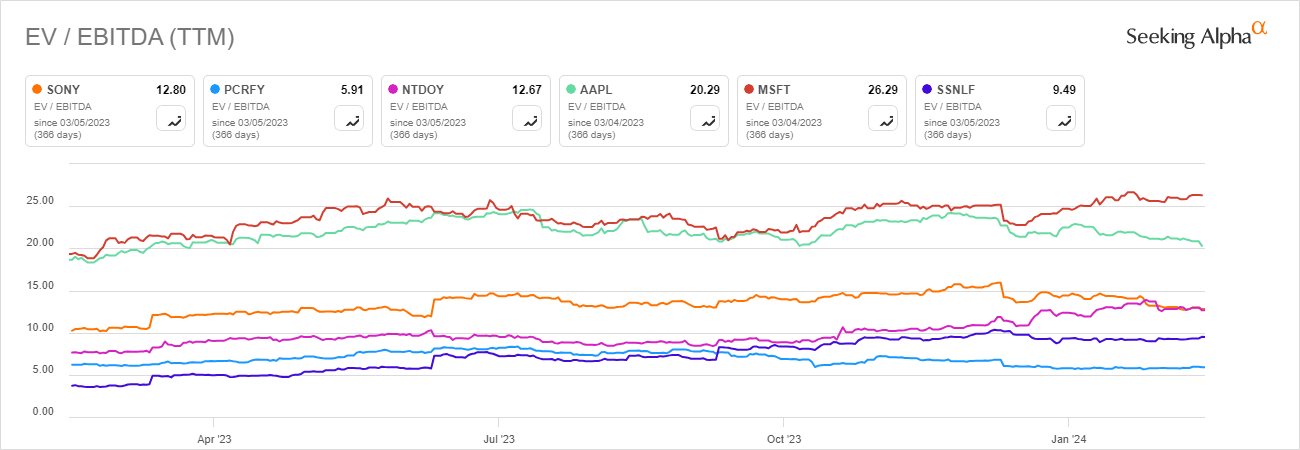

Looking at EV/EBITDA ratios, Sony trades right in the middle of the group chosen below, this could suggest a relatively fair price for the company, but really it is a product of Sony being a conglomerate with segments in many industries compared to the hardware-focused Panasonic (OTCPK:PCRFF) or the software focused Microsoft. Sony's EV/EBITDA of 12.80 on a trailing basis is quite elevated compared to the five-year average, by almost 30%, however switching to a forward basis it comes down to a much more reasonable 4.6% above the five year.

Seeking Alpha

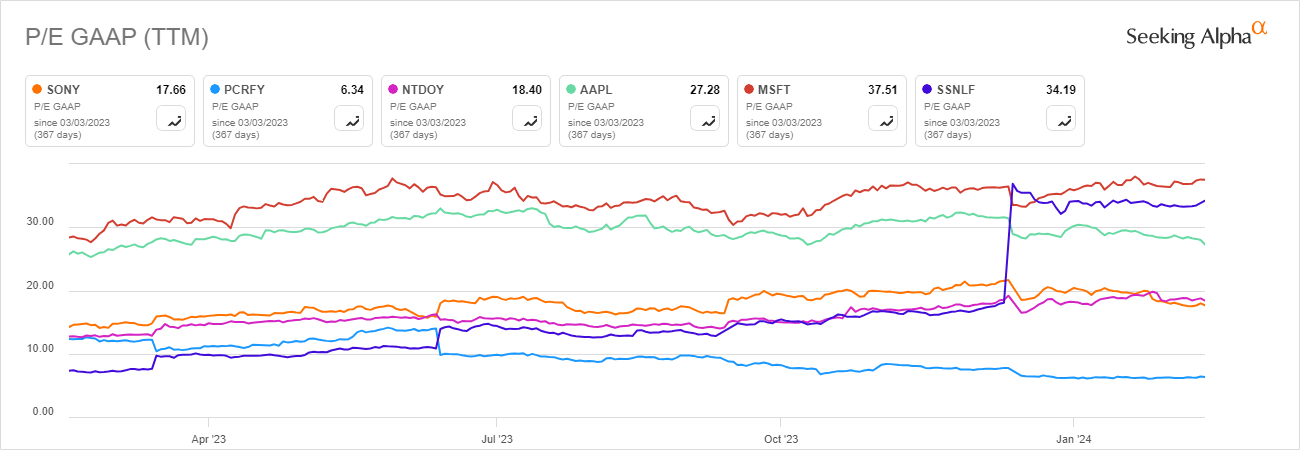

P/E ratios meanwhile tell a similar story, with Sony again in the middle of the grouping, though technically second lowest currently and a tad lower relatively.

Seeking Alpha

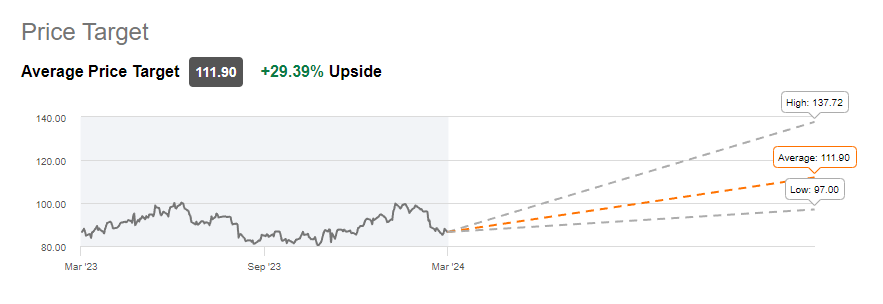

Taking a look at Wall Street targets, all represent reasonable returns if bought at current prices, with even the lowest at over 10% upside. Of seven analysts covering the stock, 4 rate it a strong buy, 2 a buy and 1 a hold.

Seeking Alpha

Aside from the uncertain nature of where gaming and the G&NS are headed, there are a couple of other risks. Looking at financials, Sony has a current ratio of 0.69, for comparison, Nintendo's (OTCPK:NTDOY) is 4.76 while Panasonic is at 1.39. This is a bit low, but for a company like Sony should not be too problematic as they can easily cover interest on debt with their current levels of income.

AI could definitely constitute a risk as it is poised to disrupt both music and movies, with Adobe previewing a gen AI tool for music generation just last week and OpenAI's Sora displaying the relatively early stages of video generation. Important to note, as with many companies now, AI isn't solely a risk but could also bring benefits to these segments of the business. However, Sony is a company that has been seen as slow to adapt at times, perhaps a concern in the context of AI.

The pressing concern for Sony's future is where the gaming industry is heading and to what degree they can steer it. PS5 sales stagnating are the tip of the iceberg, and while expansion towards the PC market and third-party titles can mitigate some profitability concerns, it also somewhat shifts Sony's role and place within the industry. If taken too far, this could weaken the ecosystem Sony has developed. However, the rest of the Sony business segments continue to perform well, there are ways to address the G&NS issues, which are also likely priced in after the latest drop. Therefore, my position is (tentatively) positive.