Future Publishing/Future via Getty Images

Future Publishing/Future via Getty Images

Sonos, Inc. (NASDAQ:SONO) reported its earnings on February 6, which was warmly welcomed news by the market that sent the stock up around 20% in two days. After our first coverage of Sonos in 2022, the stock is still down 28%. At that time, we expected strong topline growth to continue supported by the high brand premiumization of their customer base, which, however, did not materialize. We remain confident in the quality of this company and its products and believe that the worst is now behind us.

Indeed, management reiterated guidance for 2024 and announced a significant product launch that will likely reshape the entire offering of Sonos to its loyal customer base.

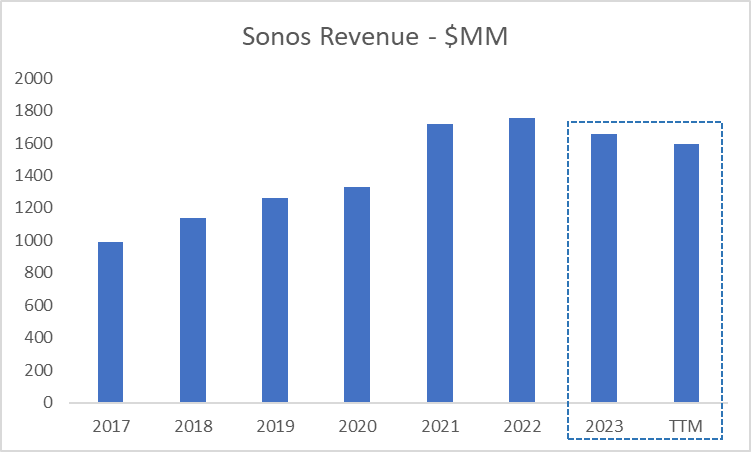

For Sonos, highly dependent on the spending of millennials and aficionados of its brand, it could have been a better year. The company reported weak quarters with flat or slightly negative topline growth YoY, which translated into losses at the bottom line as costs remained high. We believe this was caused by a mix of a slowdown in demand and a tough comparable period, which was the strong years of 2021 and 2022, in which the company experienced record profits.

Sonos Revenue (Seeking Alpha)

This slight decline in 2023 and for the last 12 months (fiscal year ends in September) have weighed on the valuation multiples.

EV/Sales (Seeking Alpha)

From the high multiple of around 3x times sales during the high-growth period, the company fell back to a more conservative 1.2x. We believe that this re-rate is partially unjustified and will gradually revert to a higher valuation and stock price. While it is hard to find actual comparables - because Amazon and Google speakers' financials cannot be disaggregated - we will show that our estimates on 2024 results will have the potential to force this re-rate.

The results for the three months between September and December 2023 have been aligned with the other quarters in terms of YoY growth. Profits also came slightly below last year's $86 million, to around $80 million. This quarter is by far the most important for the company in terms of cash generation and revenues, as the holidays bring significant spending towards SONO products.

We take some highlights from the earnings call to better reflect the sentiment of management and that of analysts.

As we have discussed in the past, the home theater category has not yet recovered and remains subdued across all of our geographies. This is in part due to a slow market for TV purchases as well as difficult economic conditions in parts of EMEA and APAC. We saw some modestly improved performance in the streaming audio category, though the market remains highly competitive.

This is a comment from the CEO, which signals where weak demand is originating. We can notice that the bulk of the slowdown is thus systemic to the entire sector, as the high sales of the pandemic period likely saturated the low-end segment of the speakers market.

Now for guidance, which is unchanged from what we outlined last quarter. Revenue. We expect revenue in the range of $1.6 billion to $1.7 billion, roughly flat year-over-year at the midpoint. Embedded in this guidance is the key assumption that we will generate more than $100 million of revenue from new product introductions in FY 2024. The lion's share of which will come in the second half of the year from the new multibillion-dollar category that we will be announcing and shipping in Q3.

This is the key passage. The guidance is unchanged, but the company signals that a significant launch in the second half of the year, in a category yet to be announced, will be the key driver of 2024 results. We remain positive on this note as it signals that the engine of innovation at SONO has not stopped, and the significant R&D spending of the last years may be set to pay off.

Last but not least, an important commentary on the Google litigation, which we reported extensively in our previous article.

Typically, I end with commentary about our Google litigation. There's not a lot to report this quarter as we continue to drive - as we continue our drive to defend and monetize our IP. We are waiting for the Federal Circuit to decide the appeals stemming from the case we had won at the ITC. When that appeals process finishes, we will restart our damages lawsuit for infringement of the valuable appeals - of the valuable patents involved in that case.

There is an ongoing case at the Federal Circuit that is about to issue a ruling on a previous win that SONO had at the ITC, which banned certain Google products from the market. This case has some similarities with the recent win of Masimo against Apple at the ITC for the infringement of its patents for certain Apple Watch features. If SONO is successful, this case can easily translate into considerable royalties coming from Google or a rich settlement.

Of course, there are also risks involved. We particularly classify two major risks that would affect our thesis: (1) execution risk associated with product launches and innovation in general, and (2) demand for speakers. The first risk can be seen as idiosyncratic as it focused specifically on Sonos' ability to deliver on its promises, both to investors and most importantly to customers, the real drivers of financial results.

The second risk equally affects competitors and is thus of a systemic nature. The market where the company operates is particularly sensitive to macroeconomic factors, and most importantly is negatively affected by recessions.

Since so much change is set to occur, we want to evaluate SONO based on the EBITDA that we expect at the end of 2024. We will then compute a reasonable multiple based on three scenarios that take into account different expected growth rates.

We saw how sensitive the stock is to changes in the growth rate by seeing a re-rate that brought the EV/EBITDA multiple down by around ⅔ given a shift of growth from +5/10% to -10% between the 2021-2022 period and 2023. As for the EBITDA figure, we feel comfortable taking the upper end of management guidance as we expect the product launch to have room to surprise on the upside, as per management commentary. So $180 million of EBITDA by September 2024, with $115 million of that already accomplished in the first quarter that ended in December.

The three scenarios look like this:

Bear case: growth continues to be challenged by a weak demand environment, 2025 and beyond is expected in the mild 2-3% per year range. The associated EV/EBITDA is around 8x times.

Base case: growth will get back on its historical track of generating high single digits to low teens topline expansion, boosted by innovation and promotional efforts. This deserves a multiple of around 15x times.

Bull case: growth will continue at the pandemic-period-like rate, in its high double digits, driven by new launches that are significantly better than competitors' and a comeback of strong demand for this niche market. A multiple in this scenario is likely around 20x times.

Now, the three fair prices and the attached probabilities look like this: (1) $13.5 per share, probability of 20%; (2) $23.5 per share, probability of 70%; (3) $30 per share, probability of 10%. We also skewed the outcomes to the downside to be more conservative and reflect the significant execution risk that is attached to the product launches described above.

The aggregate fair price is around $22, which represents an upside potential of around 22% from the current price.

Sonos is a great company with a super product offering and a loyal customer base. However, in recent years the company suffered from weak demand that affected its entire sector, and that caused a significant valuation re-rate. We now believe that SONO is back on track with exciting product launches that should bring back growth and a higher valuation. We think a fair price is around $22 per share.