Gian Lorenzo Ferretti Photography

Gian Lorenzo Ferretti Photography

U.S. equity markets posted mixed performance while benchmark interest retreated for a second week as investors parsed cooler-than-expected employment data, relatively dovish central bank commentary, and renewed hints of renewed instability in the regional banking sector. Across two days of Congressional testimony, Fed Chair Powell commented that the central bank is "not far" from having enough data to ease policy and noted that cuts “can and will begin” this year, a relatively dovish policy stance that was supported by employment data this week showing a continued cooling across labor markets.

Hoya Capital

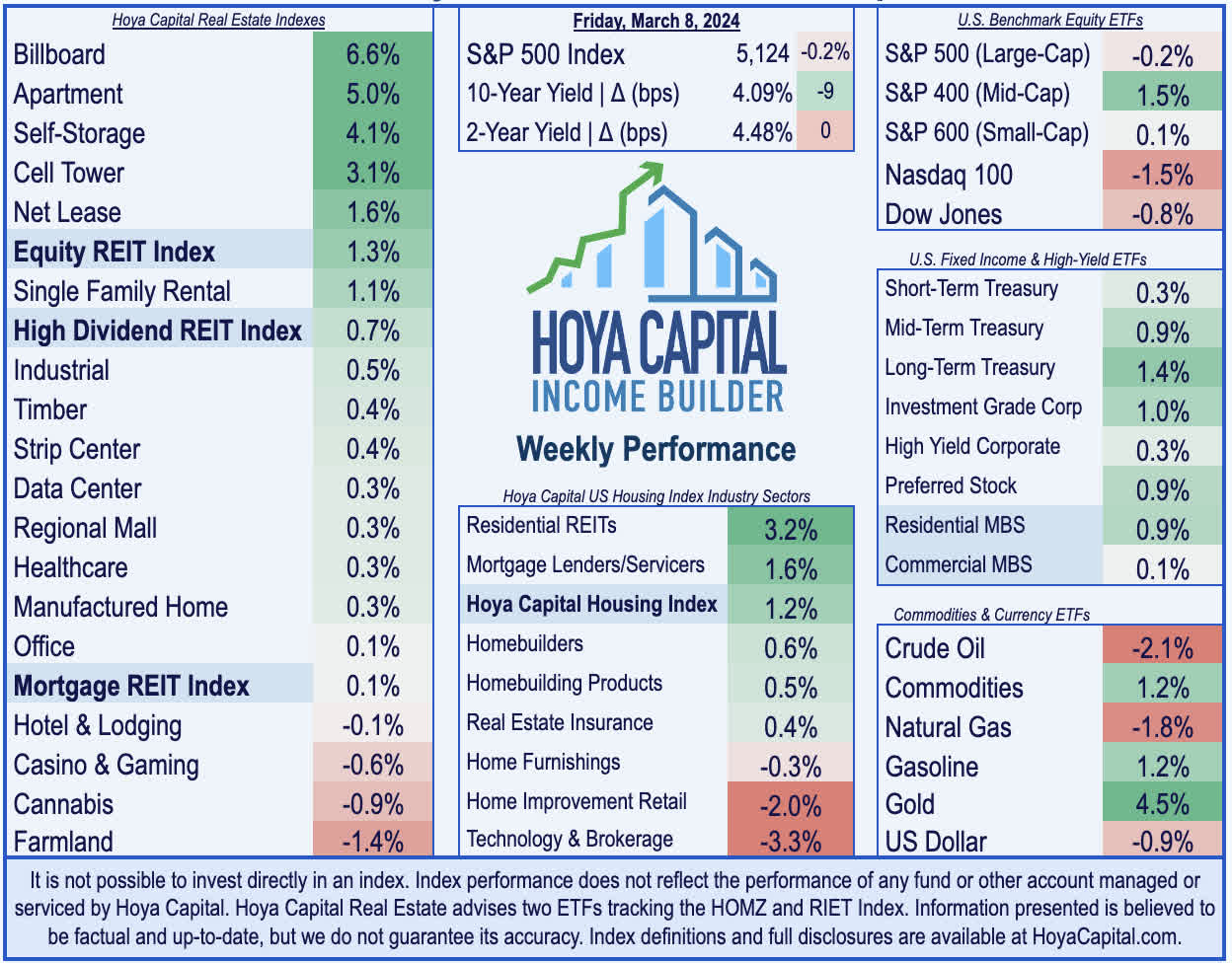

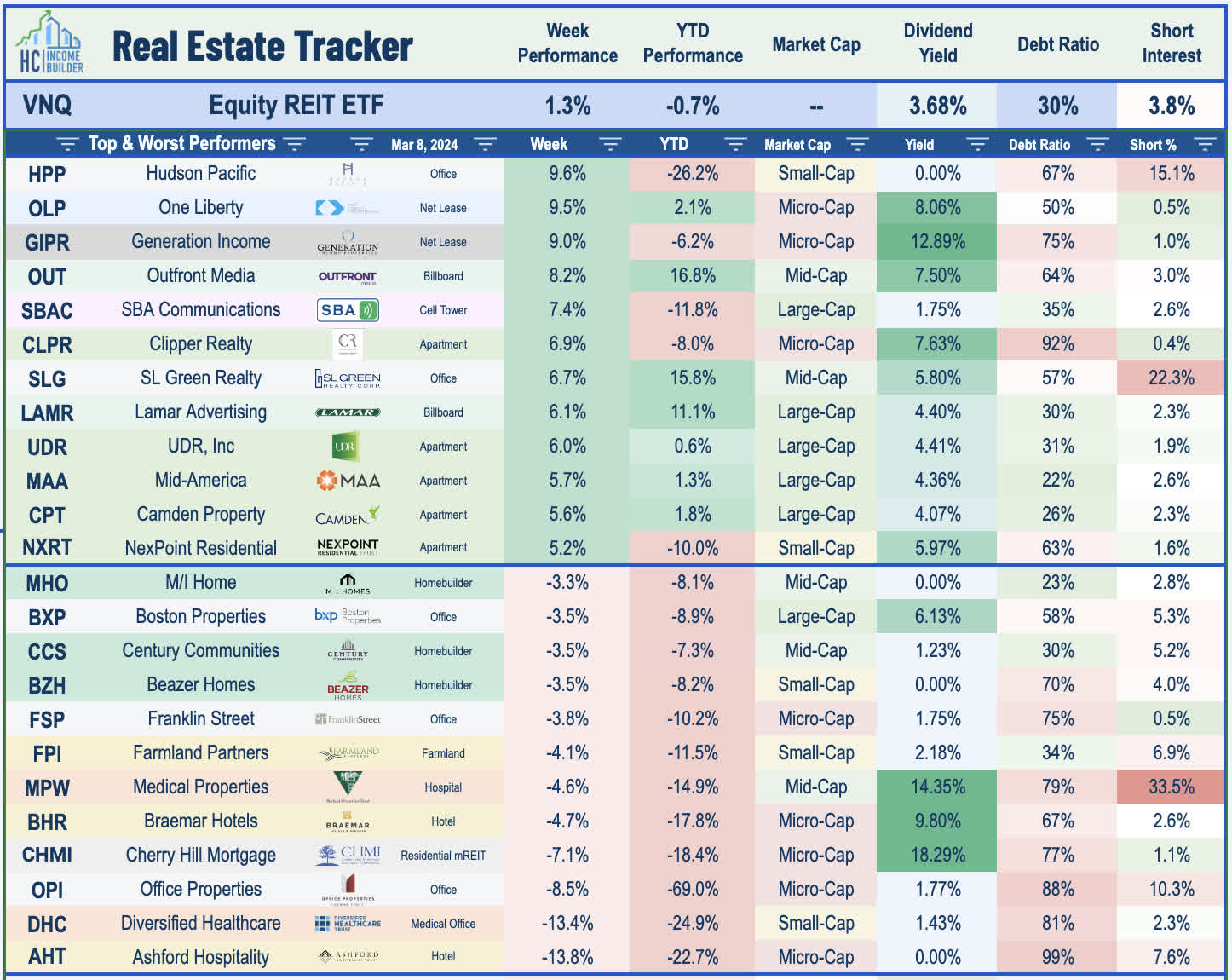

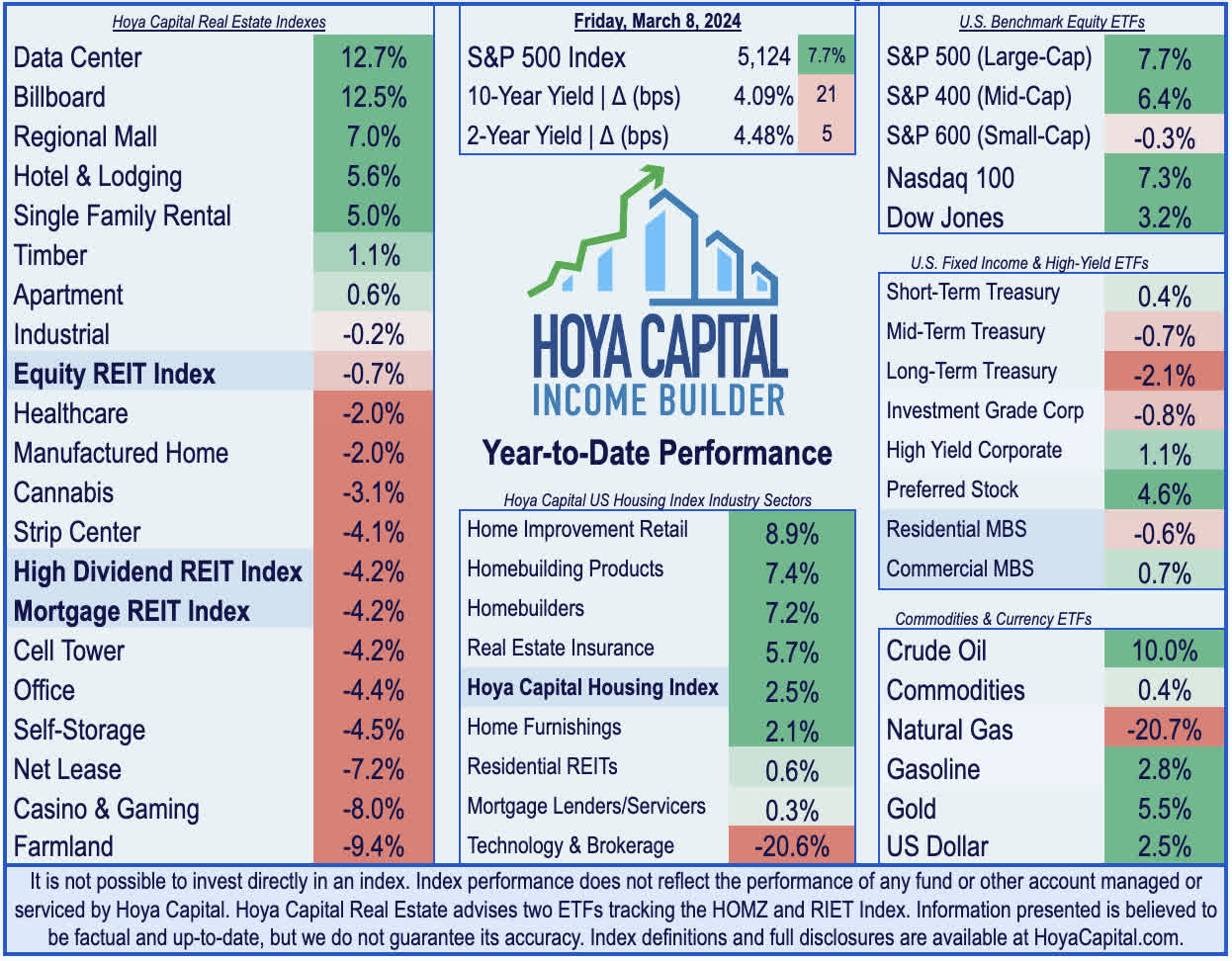

Declining for just the 3rd time in the past 19 weeks, tech-related weakness dragged the S&P 500 lower by 0.2% this week, but the Mid-Cap 400 posted gains of more than 1.5%. Reversing a bit of the historically wide performance spread between mega-cap and small-cap companies over the past year, the mega-cap-heavy Nasdaq 100 dipped 1.5% on the week, while the Small-Cap 600 finished modestly higher. Buoyed by the retreat in benchmark interest rates and a generally solid final stretch of REIT earnings season, real estate equities were among the leaders this week. Led by residential REITs, the Equity REIT Index finished higher by 1.3% on the week, with 14-of-18 property sectors in positive territory, while the Mortgage REIT Index gained 0.1%. Homebuilders were also among the leaders for a second week after mortgage market data showed solid indications of housing demand despite the recent rate rebound.

Hoya Capital

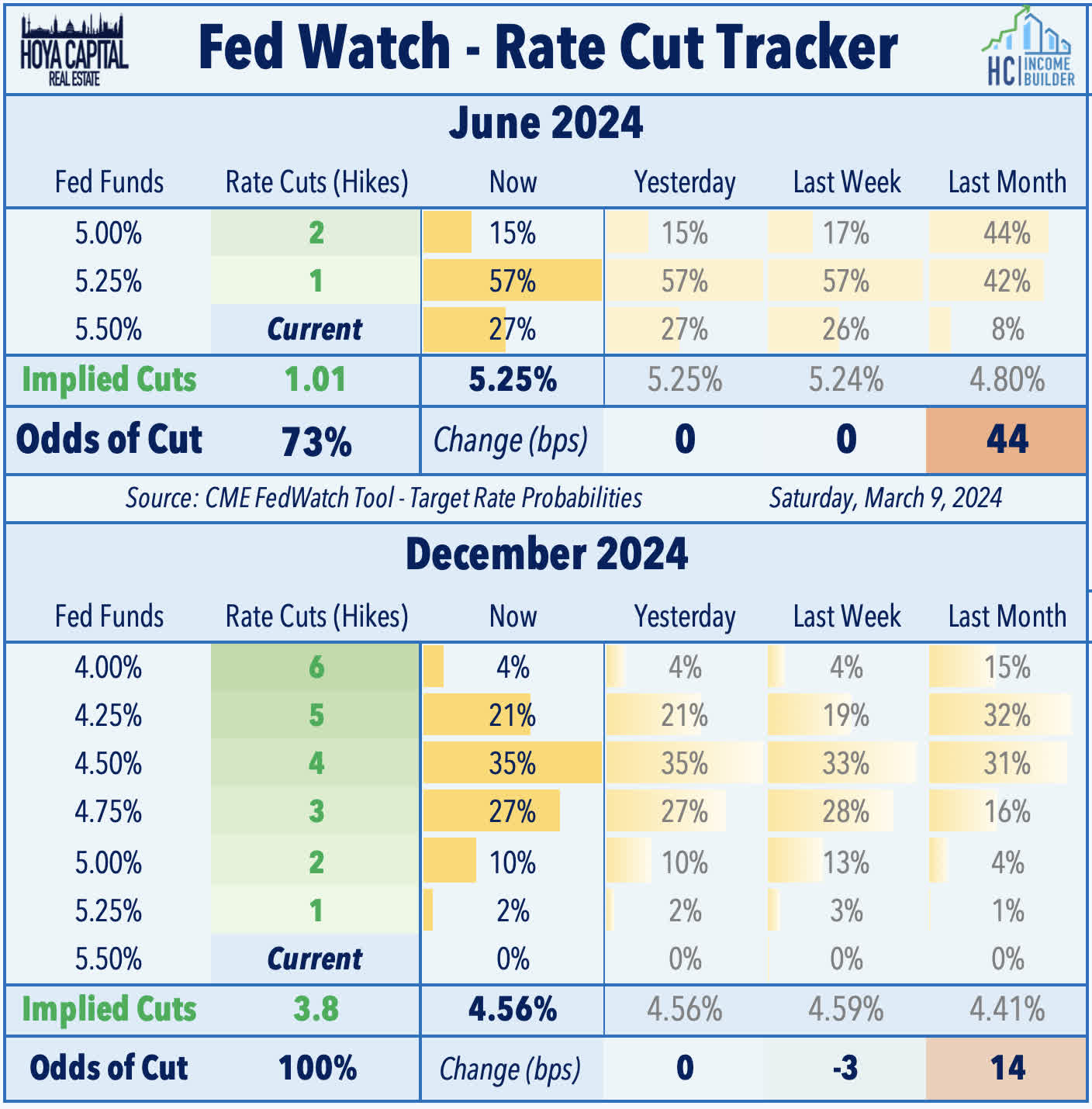

Softer-than-expected employment data and comments from central bank leaders on either side of the Atlantic buoyed rate-cut bets and pushed interest rates lower for a second week. Across the pond, European Central Bank President Lagarde also alluded to a June rate cut, as the ECB trimmed its inflation and growth forecasts to reflect expectations of near-zero-growth in the Eurozone this year. Meanwhile, investors monitored volatility in regional bank New York Community Bancorp (NYCB), which erased a 50% intraweek tumble on news it raised $1B in equity to stabilize the struggling lender. Swaps markets are now pricing in a 73% probability that the Fed will cut rates in June - up from odds of around 60% last week - and project 3.8 rate cuts this year - up from lows of around 3.0 earlier this month. The 10-Year Treasury Yield retreated by 9 basis points this week to 4.09% - down from recent closing highs of 4.33%. Rate-sensitive equity sectors - Utilities (XLU) and Real Estate (XLRE) - led to the upside this week, while Technology (XLK) stocks were laggards.

Hoya Capital

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

Hoya Capital

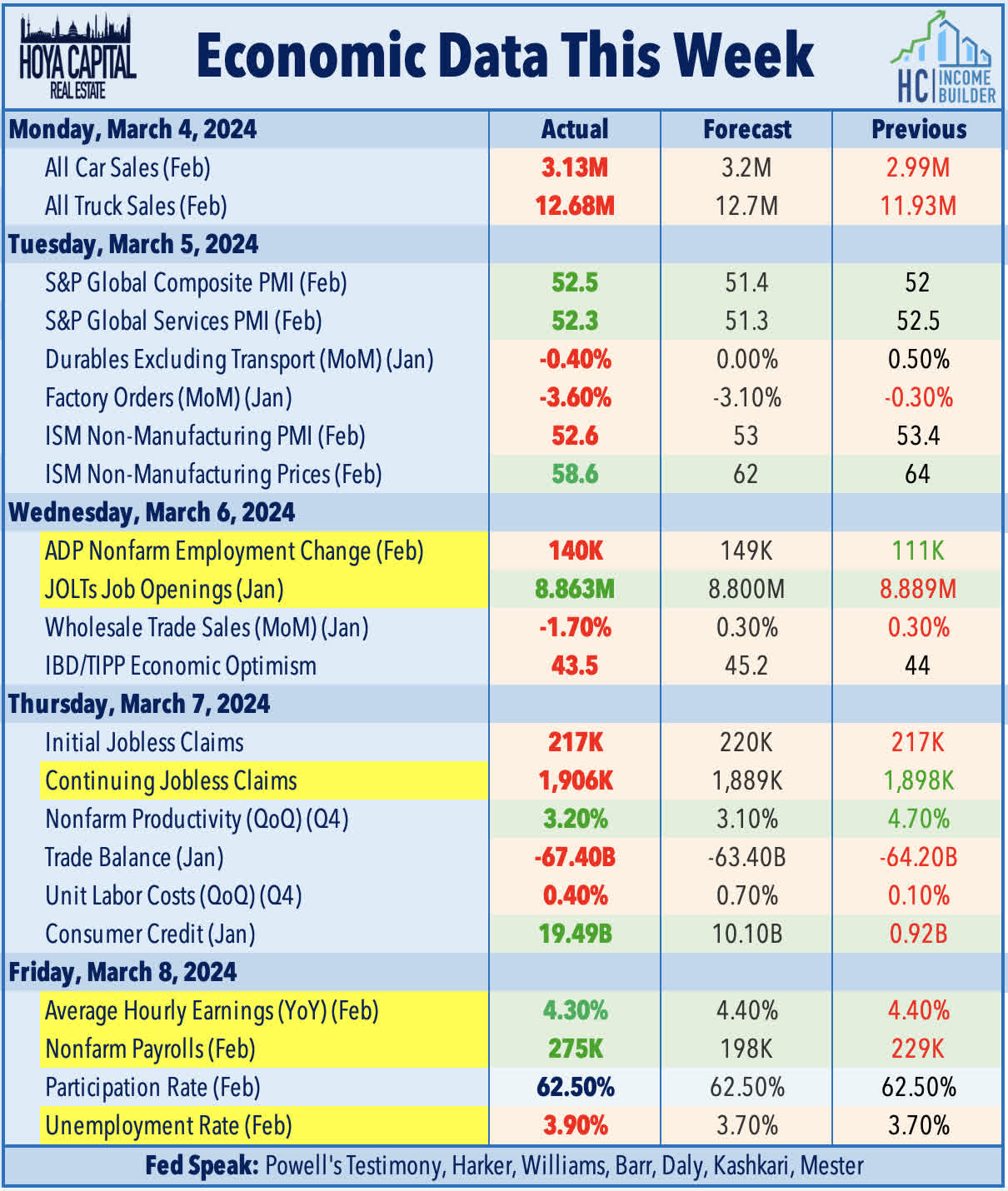

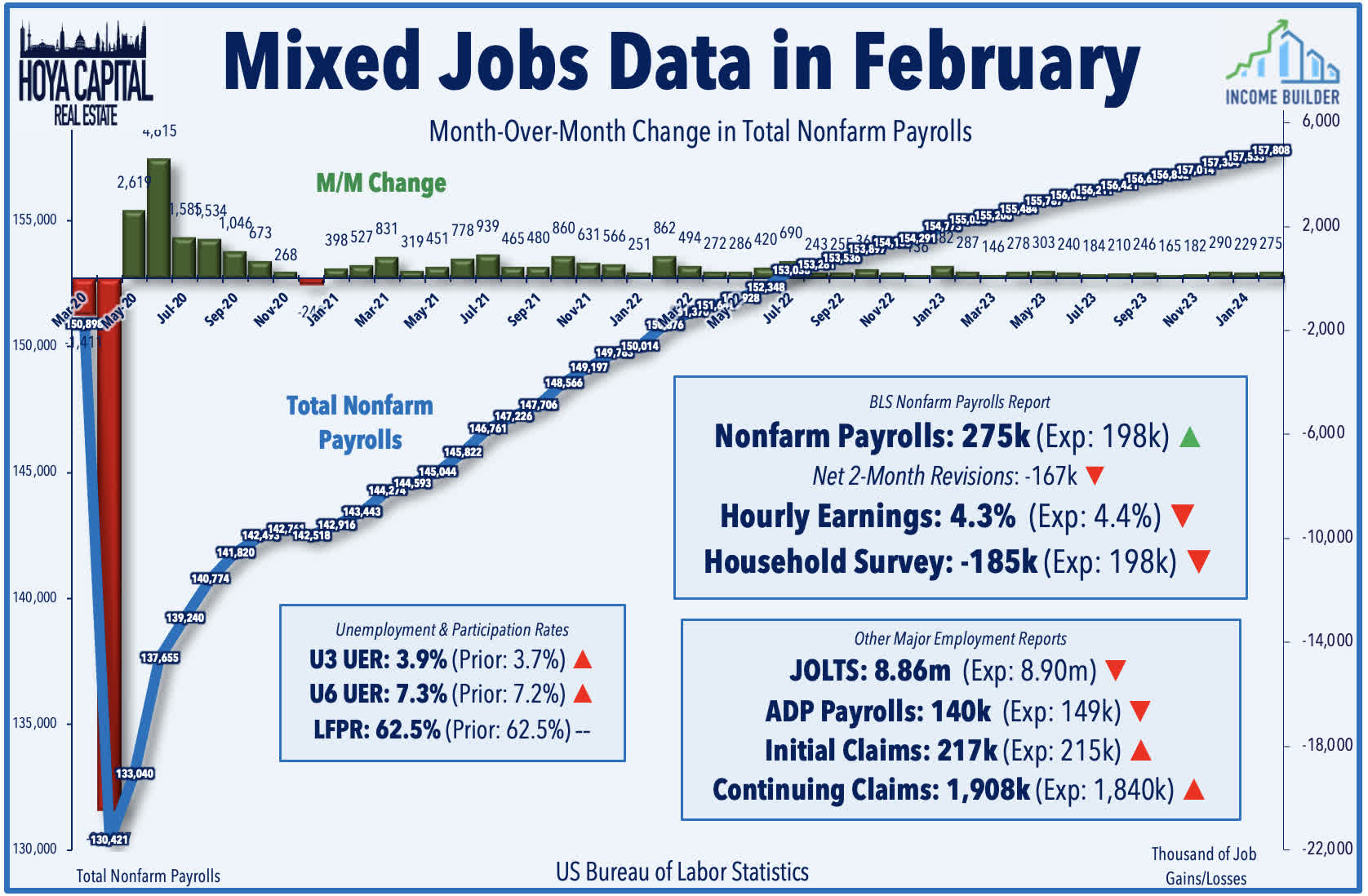

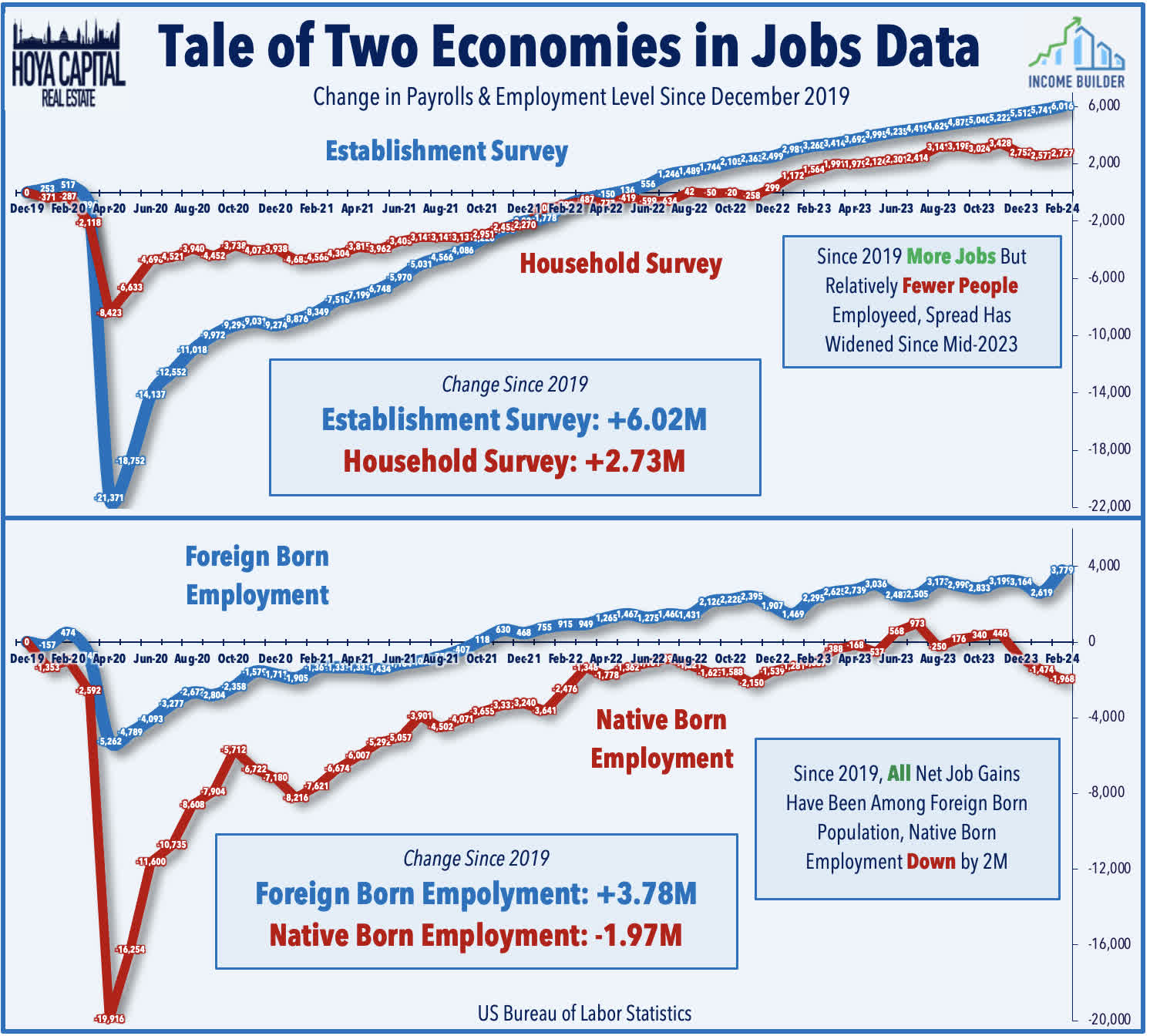

The long-awaited cooldown in labor markets - which most Fed officials have pinned their "pivot" upon - may finally be upon us, according to a critical slate of employment data this week. The critical BLS Nonfarm Payrolls report showed that the U.S. economy added 275k jobs in February - above consensus estimates of 198k - but consistent with the trend of past quarters, the report was quite a bit weaker under the surface than the headline metric would suggest. Net revisions subtracted 167k from the prior two months - the eleventh downward revision in the past thirteen reports. Earlier in the week, ADP reported that private payrolls rose by 140k in February, which was below the consensus of 150k. Jobless Claims data, meanwhile, showed that continuing claims rose to the highest level in two years. The JOLTS report, meanwhile, showed that job openings stood at 8.86M in January - roughly matching estimates, but the closely watched “Quit” rate dipped to 2.1% during the month - the lowest since 2018 excluding the pandemic dip in Q2 2020.

Hoya Capital

The Household Survey - which is used to calculate unemployment metrics - has been considerably weaker than the Establishment Survey - which is used to calculate the "headline" job gains. The Household Survey - which admittedly has been quite noisy and has given several "false alarms" - posted a third-straight month of declines, which led to a rise in the unemployment rate to 3.9% from 3.7%. The Household Survey also showed some rather remarkable splits in job gains between Native and Foreign-born workers. While it's again worth noting that the BLS' population-characteristics metrics are prone to large revisions, the report this week showed that the foreign-born employment level rose by 1.16M in February, while the native-born population level plunged by 494k during the month. Longer-term trends show that all of the net job growth since 2020 has come via foreign-born workers, while the native-born population has lost nearly 2 million jobs over the past four years.

Hoya Capital

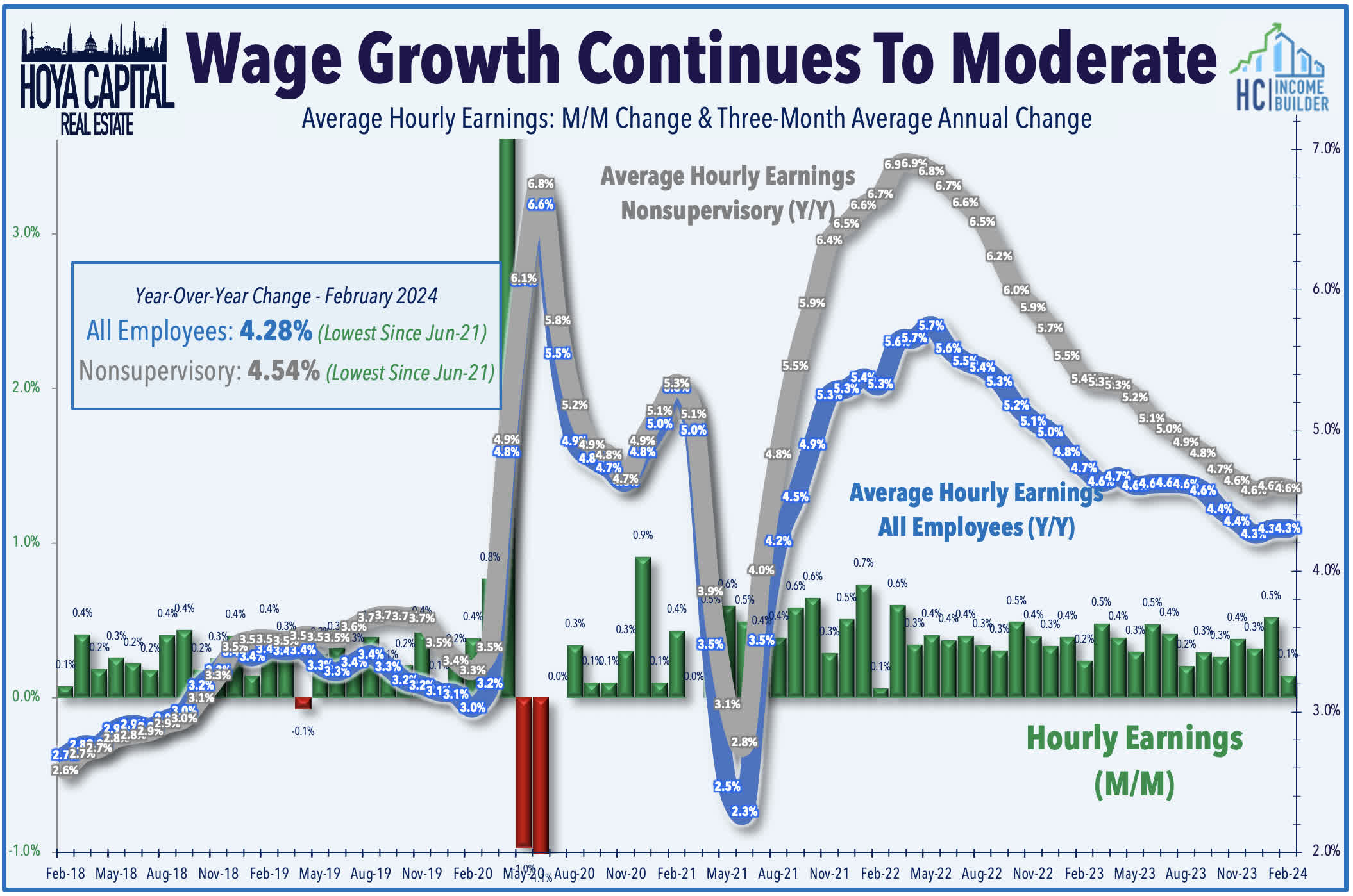

Average hourly earnings ("AHE") - a key inflation indicator - provided additional evidence of normalizing labor market conditions following pandemic-era shortages. AHE for all employees moderated to a 4.3% year-over-year increase in February - the softest since June 2021 - and moderated to 4.5% for nonsupervisory workers, down sharply from the peak of around 7% in early 2022. Since the start of 2023, AHE for all employees has averaged 4.0% on an annualized basis - which is still slightly above the 3.3% increase in 2019 in a year when CPI inflation averaged just 1.8%. ADP also reported that its measure of annual pay posted its smallest annual gain since September 2021 at 5.1%. Job changers, however, saw wage increases of 7.6% - up from 7.2% last month - which was the first acceleration in over a year.

Hoya Capital

Best & Worst Performance This Week Across the REIT Sector

Hoya Capital

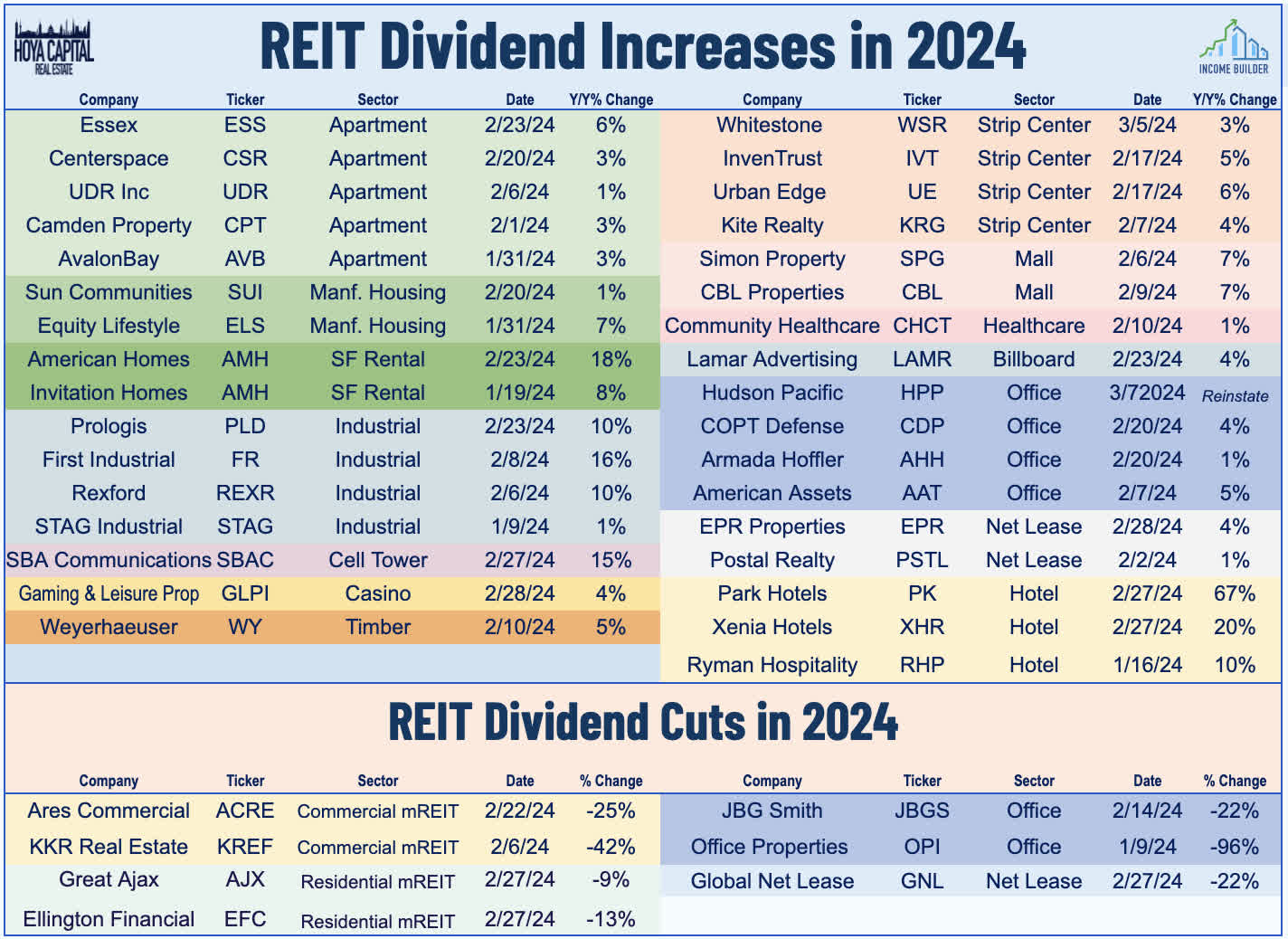

This week, we published Winners of REIT Earnings Season - Part 1 of our two-part REIT Earnings Recap. We noted that upside surprises this earnings season came largely from the service-oriented pro-cyclical property sectors - retail, hotel, and specialty REITs. An easing of expense pressures and stable tenant financial health lifted healthcare and cannabis REITs as well. Fittingly, in the "AI-generated" earnings season in which technology stocks bifurcated from the rest of the market, Data Center REITs delivered the strongest price returns despite mixed earnings results. The single most economically-sensitive property sector, billboard REITs have been beneficiaries of the so-called "No Landing" scenario of 3-4% inflation and economic growth. Positively, we've tracked more than two dozen REIT dividend hikes this earnings season, including a pair of increases this week. West Coast-focused office REIT Hudson Pacific (HPP) soared nearly 10% after it reinstated its dividend, which had been suspended since mid-2023 as it faced a double-whammy of office weakness and strike-driven shutdowns at its movie studio properties. HPP's declared a $0.05/share quarterly dividend (3.0% dividend yield). Strip center REIT Whitestone (WSR) also raised its monthly dividend by 3% to $0.04125/share (4.0% dividend yield). We've now seen 31 REIT dividend hikes this year, while seven REITs have reduced their dividends - most of which have resulted from office-related headwinds.

Hoya Capital

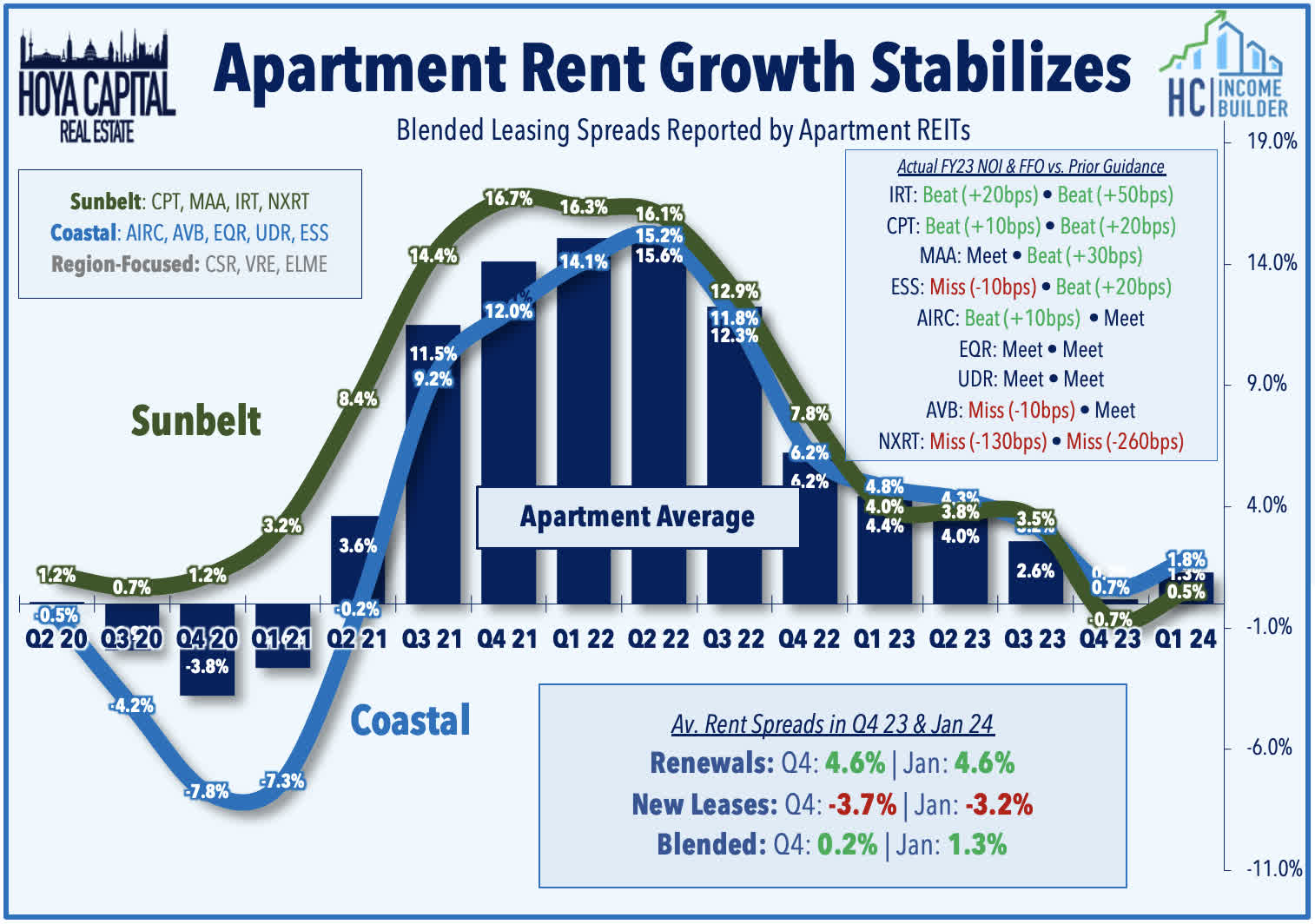

Apartments: Multifamily REITs were among the leaders this week with average gains of 5% after an encouraging slate of business updates presented at the Citi Global Property Conference showed a rebound in rent growth in early 2024 from the near-zero growth reported in Q4. Coastal-focused AvalonBay (AVB) rallied nearly 5% after it reported that blended leasing spreads accelerated in February to 2.4% - up from 1.3% in Q4 and in January - and noted that renewal offers for March and April 2024 are being delivered to residents at an average increase of 5.0%. Sunbelt-focused Camden Property (CPT) rallied 6% after it reported steady occupancy rates and a moderation in bad debt in early 2024, which offset relatively weaker leasing trends, with blended spreads of -2.0% in February - down from -0.5% in January and -0.8% in Q4. Camden noted that it would be even more aggressive on new lease pricing. Meanwhile, Independence Realty (IRT) rallied 5% after it announced that it earned an investment-grade credit rating from Fitch, which assigned it a ‘BBB’ rating with a stable outlook. An important milestone for small- and mid-cap REITs, IRT joins a cohort of seven larger apartment REIT peers that have an investment-grade credit rating.

Hoya Capital

Net Lease: We also heard earnings results from the final half-dozen equity REITs this week, which provided noteworthy insights into how small- and micro-cap REITs are faring. Small-cap One Liberty Properties (OLP) - which owns an industrial and retail-heavy net lease portfolio comprised of roughly 120 properties - rallied nearly 10% this week after it reported steady property-level performance and balance sheet improvements. OLP - which has remained a relatively "sleepy" small-cap REIT throughout its near-four-decade tenure - recorded FFO growth of 0.5% in 2023, which was roughly in-line with the broader net lease sector average. OLP was a net seller in 2023 - completing $47M in property sales - which it used to pay down debt and maintain balance sheet metrics that were quite solid given its small size. OLP noted that its occupancy rate stood at 98.8% at year-end, which was down slightly from the 99.8% rate a year earlier. Industrial properties account for roughly two-thirds of its rent roll, with the balance composed primarily of retail properties. Earlier this week, OLP held its dividends steady at $0.45/share (8.8% dividend yield), which marked its 125th consecutive quarterly dividend.

Hoya Capital

Hotel: Small-cap Sotherly Hotels (SOHO) - which owns 2,800 rooms across ten hotels under the Hilton and Hyatt brands - advanced 5% this week after it reported decent property-level performance across its Sunbelt-focused portfolio, but noted ongoing headwinds on corporate-level profitability as it struggles under the weight of its debt-heavy balance sheet. SOHO reported that its full-year Revenue Per Available Room ("RevPAR") increased 5.6% in 2023, driven by a 0.9% increase in Average Daily Rates ("ADR) and a 2.8% increase in occupancy. While SOHO noted that 2023 marked a completion of its "pandemic recovery" with same-store RevPAR that was 5.5% above 2019-levels, this performance remained rather disappointing compared to its peers. STR notes that industry-wide RevPAR was about 13% above 2019-levels in 2023. Surging interest expense and the effects of recent asset sales and refinancing activity weighed on SOHO's corporate-level metrics, and will continue to be a headwind in 2024. SOHO reported that its full-year AFFO dipped 21% in 2023, and it expects another 11.3% decline in 2024. By comparison, the average hotel REIT reported FFO growth of 5% in 2023, and guidance indicates that FFO will be roughly flat in 2024.

Hoya Capital

Cannabis: Small-cap cannabis-focused mREIT AFC Gamma (AFCG) gained 3% this week after reporting decent fourth-quarter results showing relatively modest deterioration in loan performance and progress in resolving loans to two operators in receivership. AFCG reported distributable EPS of $0.49 in Q4 - flat with the prior quarter - and covering its $0.48/share dividend. Operator issues were generally "status-quo" with last quarter: AFCG noted its second-largest borrower - Nature's Medicine (Private Company A) - has been actively liquidating assets, and has so far paid down $53 million in principle to AFC and syndicate partners. AFCG noted its third-largest borrower - Justice Cannabis (Subsidiary of Private Company G) - has agreed to a plan that requires Justice to install new operators at its two facilities in exchange for a reduced interest rate. While AFCG's distributable EPS remained steady, its Book Value did take a sizable hit in Q4 from an increase in credit loss reserves. AFCG reported that its BVPS stood at $15.64 at the end of Q4 - down 5.6% from Q3 - resulting from a $12M increase in its CECL. As of December 31, 2023, the CECL reserve was 8.7% of its loan book, up from 4% in the prior quarter.

Hoya Capital

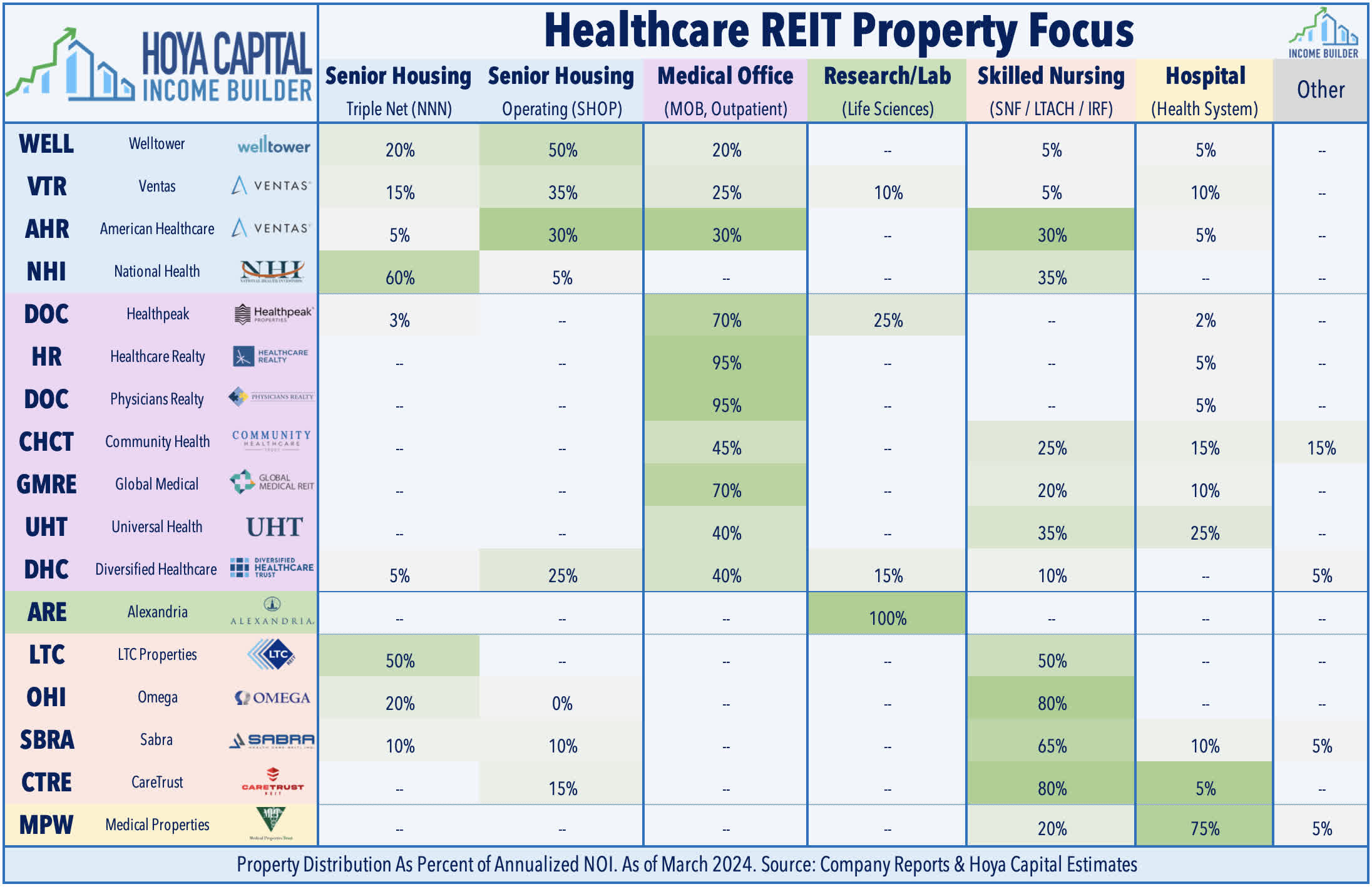

Healthcare: There's a new "DOC" in town. Healthpeak (DOC) officially closed its previously announced merger with Physicians Realty Trust, forming the largest Medical Office Building REIT and the third-largest healthcare REIT. While the combined companies will operate under the name “Healthpeak Properties, they will use the ticker symbol “DOC.” The merger creates a portfolio of about 52 million square feet of MOB and life sciences properties. Elsewhere in the healthcare space, Alexandria Real Estate (ARE) gained 2% this week as it announced that Takeda Pharmaceutical signed a 223k SF lease extension at its Kendall Square mega campus in the Cambridge submarket. Elsewhere, senior housing REIT Ventas (VTR) gained 1% after it announced a "mutual cooperation pact" with activist holder Land & Buildings Investment Management ("L&B"), and named two of L&B nominees to its Board of Directors. L&B initiated a campaign for management changes at Ventas in early 2022, seeking to close a “valuation and performance gap” with Welltower (WELL). Finally, skilled nursing REIT CareTrust (CTRE) gained 2% after it announced a $55.6M deal to buy three skilled nursing facilities in Texas and Missouri, which will be added to its master lease with PACS Group.

Hoya Capital

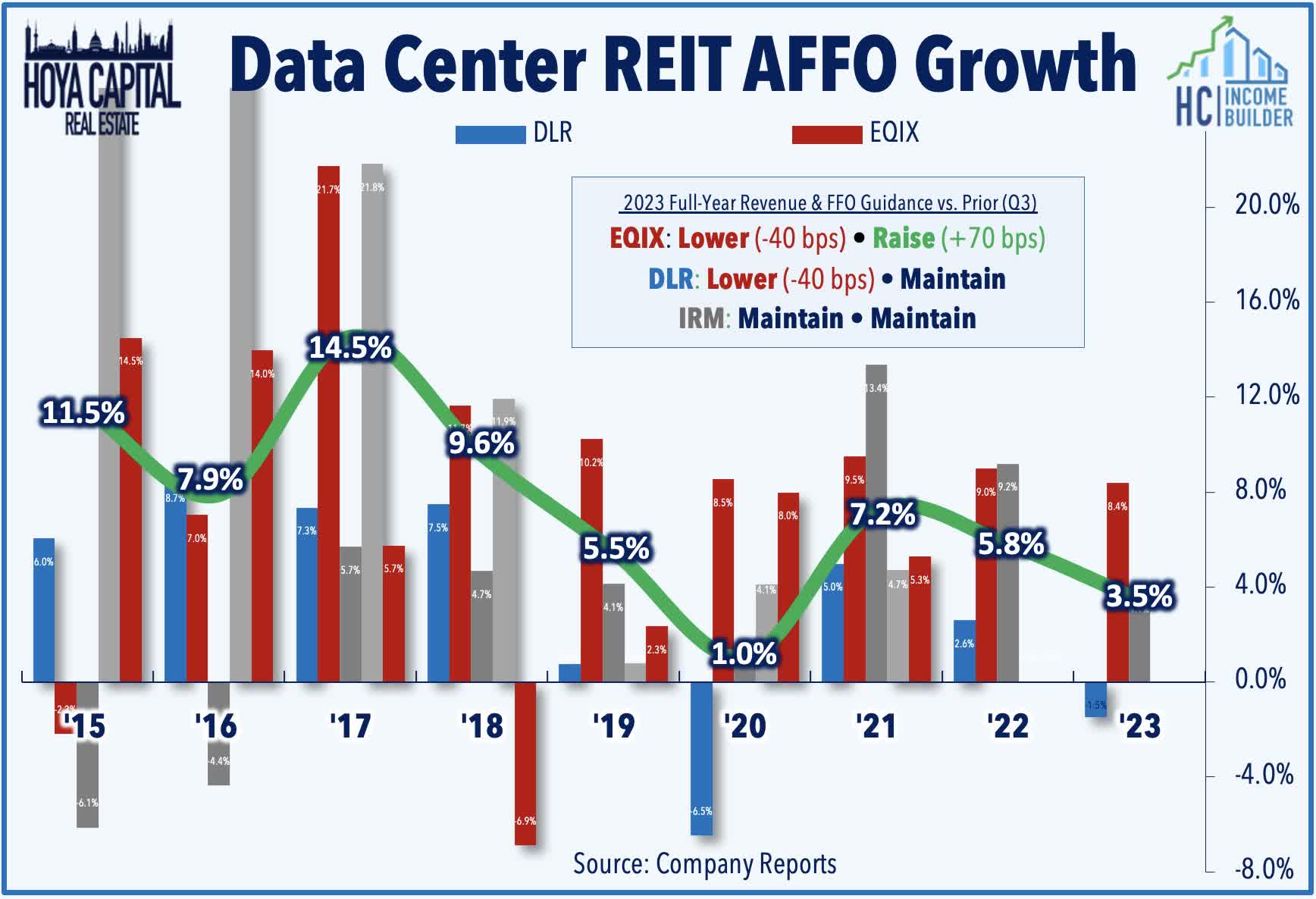

Data Center: Digital Realty (DLR) slipped 1% this week after it announced the formation of a joint venture with Mitsubishi Corporation to support the development of two data centers in the Dallas metro area, which are 100% pre-leased. Digital Realty sold a 65% interest in the property to Mitsubishi for an initial contribution of approximately $200M, while Digital Realty maintains a 35% interest and will manage the development and day-to-day operations of the joint venture, for which it will receive customary fees. Each partner will fund its share of the remaining $100M estimated development cost for the first phase of the project, which is slated for completion and commencement in late 2024. For DLR, the move follows similar joint ventures with Blackstone (BX) and Realty Income (O), in which DLR has monetized properties as part of a deleveraging strategy. As noted in our Earnings Recap, DLR reported that its full-year FFO declined -1.6% in 2023 as otherwise impressive revenue growth of 17% and record-high "same capital" NOI growth of 7.5% was fully negated by a combination of higher interest expense and deleveraging through asset sales and stock issuance. The outlook for 2024 calls for FFO growth of just 1.3% as further deleveraging activities are expected to again offset an otherwise strong year of property-level performance.

Hoya Capital

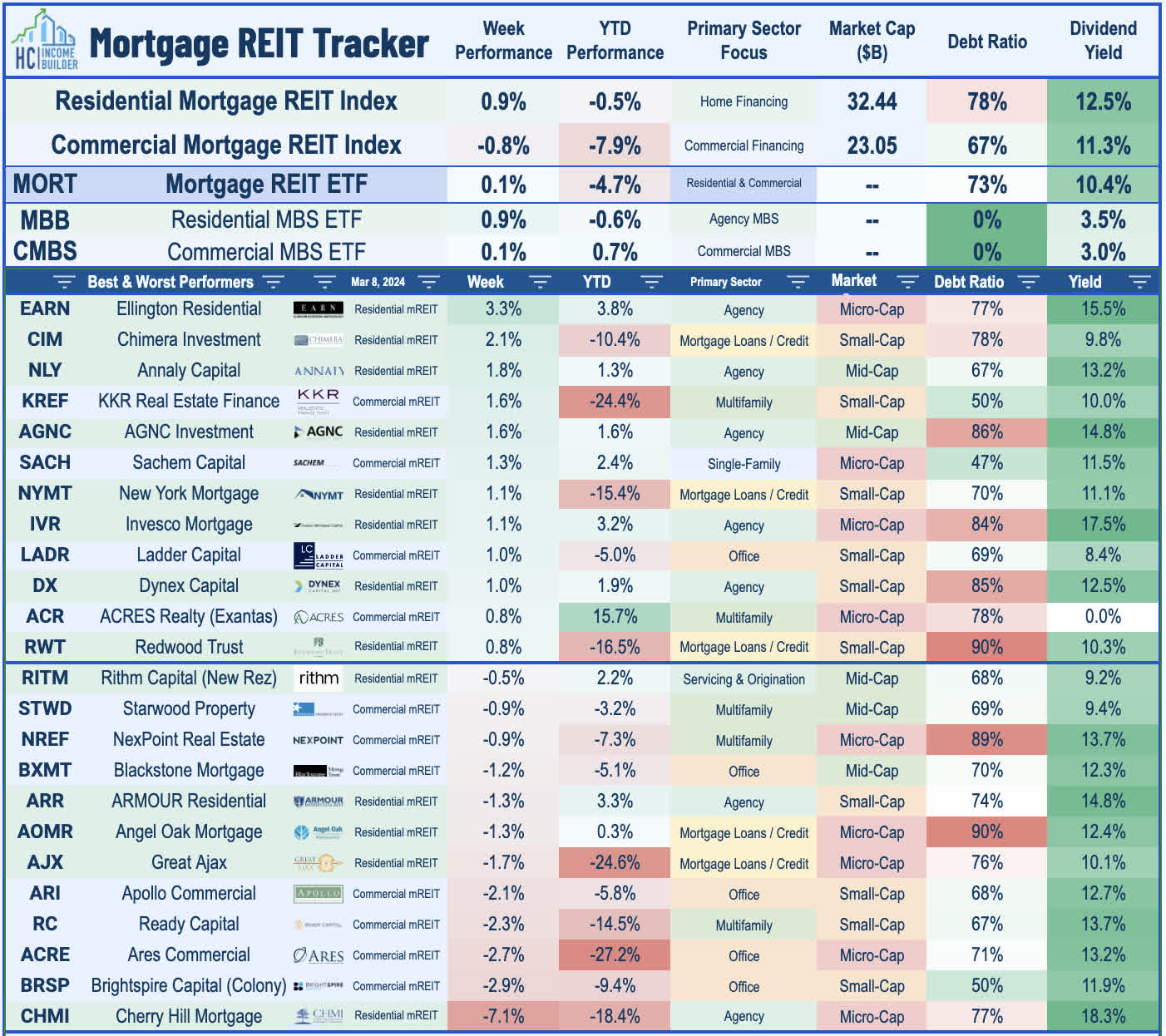

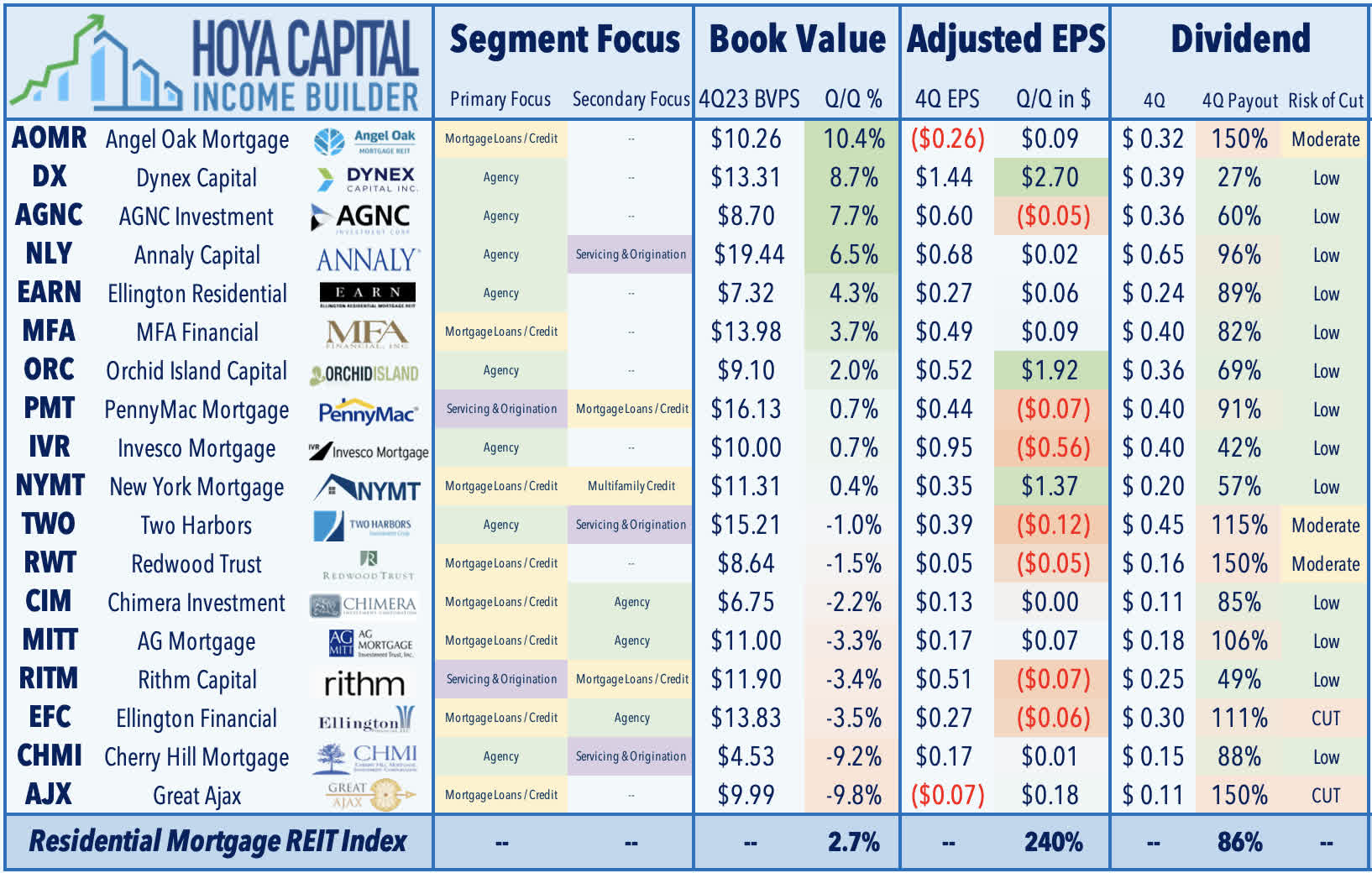

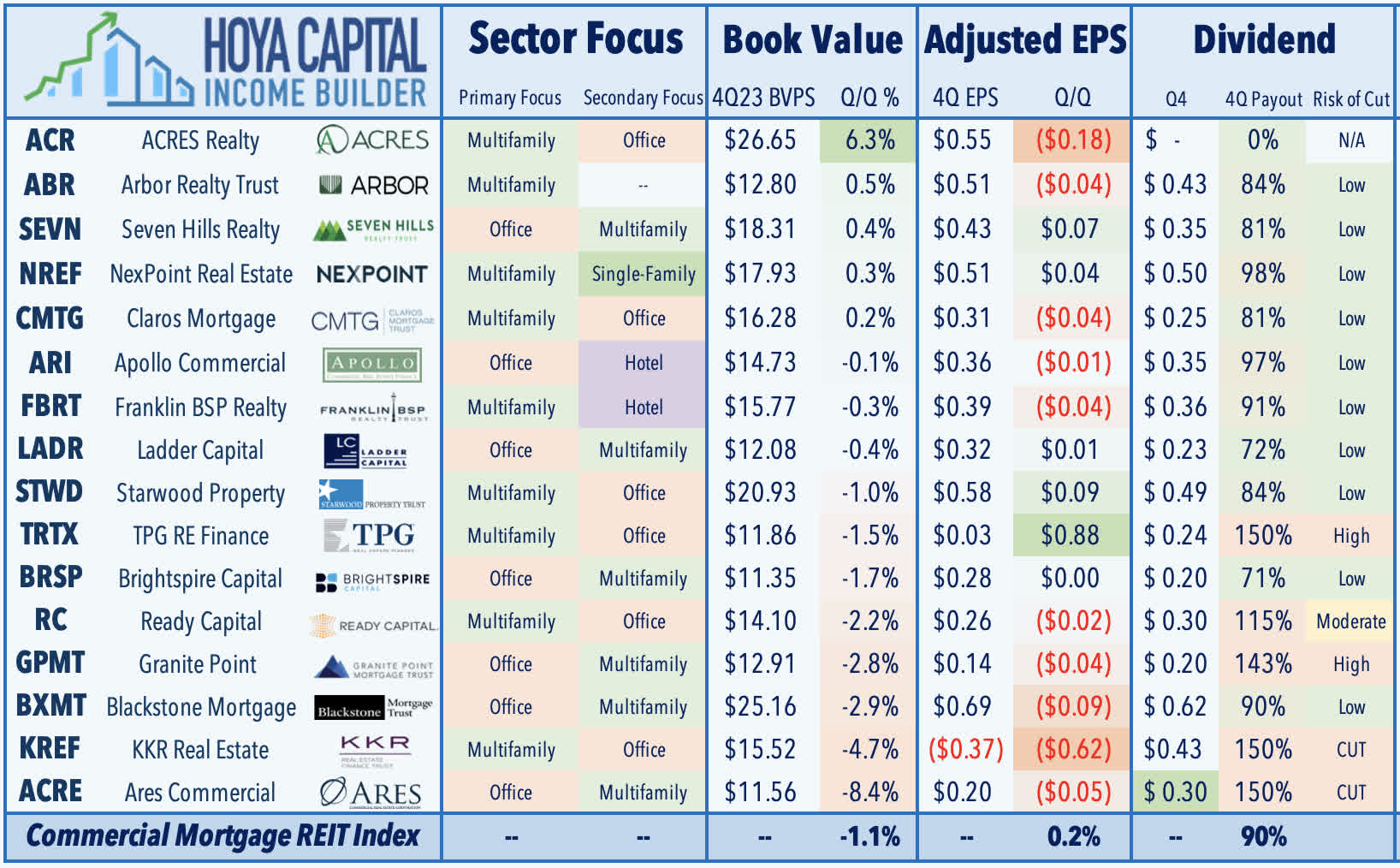

Mortgage REITs were mixed this week as earnings season wrapped up with the final half-dozen reports, with the iShares Mortgage REIT ETF (REM) advancing 0.1%. On the upside this week, residential mREIT Ellington Residential (EARN) rallied 3% after reporting better-than-expected results, highlighted by a 4.3% increase in its Book Value Per Share ("BVPS") in Q4, which was the 5th strongest among residential mREITs this earnings season. Citing outperformance from its agency RMBS portfolio and positive spread movement in its credit-sensitive portfolio, EARN noted that its distributable EPS rose to $0.27 in Q4 - up from $0.21 in the prior quarter - and once again covering its $0.24/share quarterly dividend. EARN - which has historically been an agency-focused mREIT - highlighted its recent push into the corporate CLO market that it initiated last year, which now comprises about a fifth of its portfolio. EARN explained that diversifying into CLO allows it to more efficiently and cheaply hedge the interest rate risk inherent in agency MBS compared to traditional delta hedges, which incur costs and cut into book value over time.

Hoya Capital

On the downside this week, Cherry Hill (CHMI) dipped 7% after its results showed the potential downside and cost of traditional interest rate hedges if and when rates move sharply in the opposite direction. CHMI noted that it was positioned for a "higher for longer rate environment" with a negative duration portfolio and was "surprised by the Fed's sudden shift in policy" towards rate cuts in 2024. Despite the positive performance in its underlying RMBS book, CHMI reported that its BVPS dipped 9.2% in Q4 - the second-worst among mREITs this earnings season. Positively, CMHI did report that its distributable EPS rose to $0.17 - up from $0.16 last quarter - which covered its $0.15/share quarterly dividend. CHMI also indicated that it has benefited from the reversal in the rate movement in early 2024 which "aligns with how we initially positioned our portfolio."

Hoya Capital

Elsewhere, Angel Oak (AOMR) declined 1% this week after noting that it has been on the other side of that trade. AOMR - which focuses on non-agency residential credit -reported that its BVPS surged 10.4% in Q4 - the strongest in the mREIT sector this quarter - but noted that its BVPS has declined about 3.5% so far in Q1 "given recent rate and spread movements." AOMR called 2023 a "pivotal year" after it endured short-term pain in late 2022 as it "derisked" its portfolio by selling assets and reducing its dividend in 4Q22. AOMR sees tailwinds in the back half of 2024 as the Fed begins to cut interest rates, commenting, "if this happens, we would expect earnings to increase due to lower financing costs and improved securitization execution." As we'll discuss in Part II of our Earnings Recap this weekend, residential mREITs reported decent results in Q4 with an average increase in BVPS of 3% while distributable EPS more-than-doubled from Q3, while commercial mREITs reported an average decline in BVPS and EPS of around 1%.

Hoya Capital

Through ten weeks of 2024, real estate equities have lagged the broader equity benchmarks following a powerful year-end rebound in 2023. The Equity REIT Index is lower by -0.7%, while the Mortgage REIT Index is lower by -4.2%. This compares with the 7.7% gain on the S&P 500, the 6.4% gain for the S&P Mid-Cap 400, and the -0.3% decline for the S&P Small-Cap 600. Within the REIT sector, 7 of the 18 property sectors are higher for the year, led on the upside by Data Center, Billboard, and Regional Mall REITs, while Net Lease and Farmland REITs have lagged on the downside. At 4.09%, the 10-Year Treasury Yield is higher by 21 basis points on the year, while the 2-Year Treasury Yield has risen 5 basis points to 4.48%. Following a late-year rally in the final months of 2023, the Bloomberg US Bond Index is lower by -0.5% this year. WTI Crude Oil is higher by 10.0% this year, lifting the broader Commodities complex higher by 0.4% on the year.

Hoya Capital

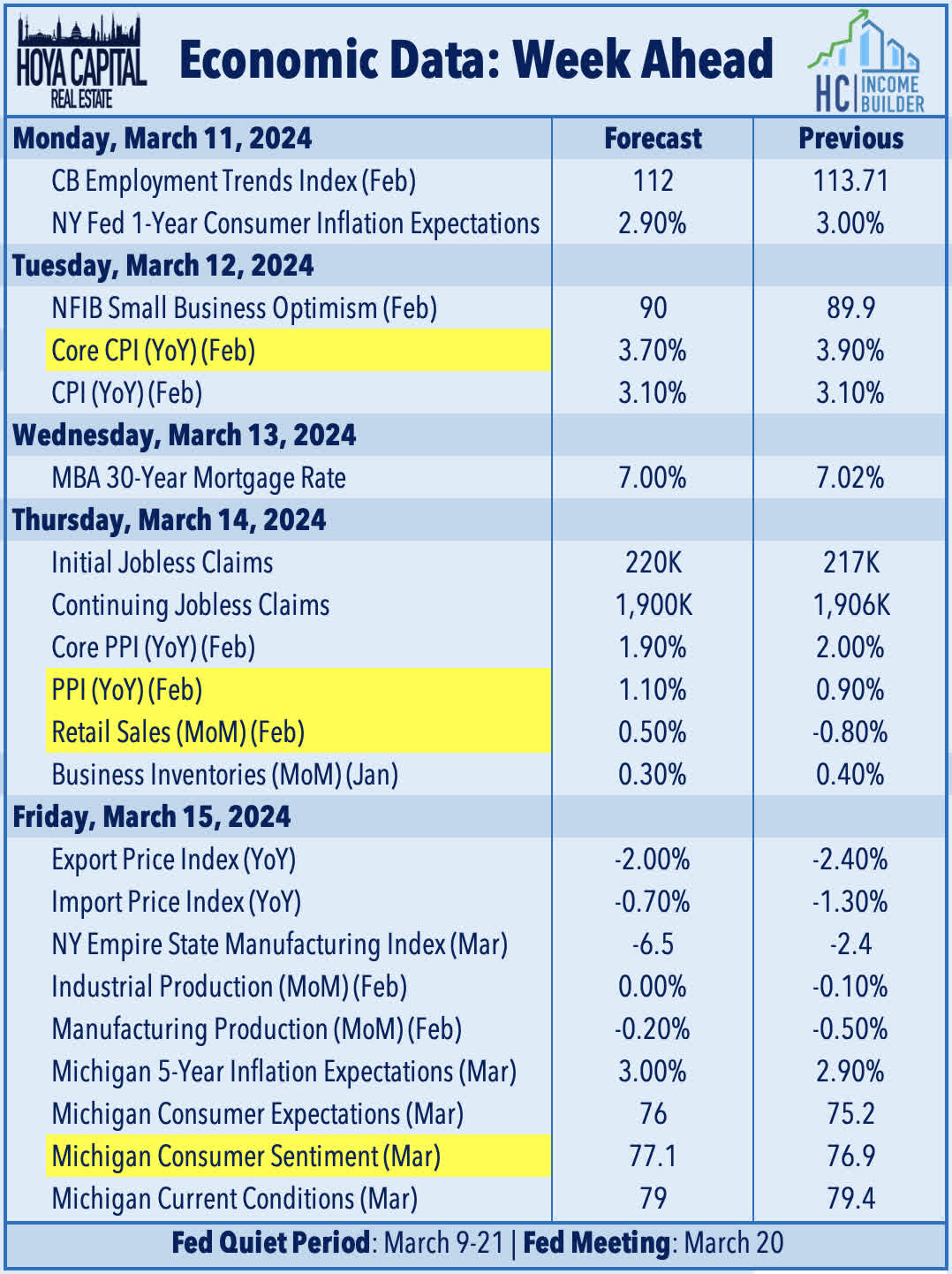

A critical slate of inflation data highlights the economic calendar in the week ahead as the Federal Reserve enters its "quiet period" ahead of its March 20th interest rate decision. The main event comes on Tuesday with the Consumer Price Index for January, which investors are hoping will show a cooling of inflationary pressures after a slightly hotter-than-expected report last month. The Core CPI is expected to moderate to a 3.7% year-over-year rate - down from 3.9% last month. While we'll likely see some moderation in the critical shelter component, gasoline prices - which remain the key "swing" inflation input - were higher by 4% during February compared with the prior month, on average, and have risen about 10% since bottoming in late January. On Thursday, we'll see the Producer Price Index, which has generally shown more encouraging disinflation trends in recent months compared to the CPI report because of its skew towards goods-oriented inputs. Core PPI is expected to show a 1.9% inflation rate - remaining below the Fed's 2% policy objective for a fourth straight month. We'll also see Retail Sales data on Thursday, which is expected to show an uptick in March after a surprisingly weak report in February. We'll also get our first look at Michigan Consumer Sentiment data for March, which includes a closely watched inflation expectations survey.

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Mortgage, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.