Daniel Boczarski

Daniel Boczarski

SoFi Technologies (NASDAQ:SOFI) has very good growth prospects in the fintech sector and its current valuation is attractive, making it an interesting growth play for long-term investors.

SoFi Technologies is a fintech company, combining financial services and technology offerings for its customers. The company was founded in 2011, named Social Finance, Inc., at the time focused on student loan refinancing activities, while it gradually expanded its product offering, to mortgages, consumer loans, and others throughout its history.

More recently, it became a public company in 2021, when it performed a SPAC merger and changed its name to SoFi Technologies. Currently, it has a market value of about $7.2 billion, being a relatively small company by this measure, and trades on the NASDAQ stock exchange.

SoFi's core business is financial services, focused on its digital capabilities, aiming to offer better customer service than competitors as a way to distinguish itself from other fintech players and banks in the financial industry, potentially leading to a competitive advantage over the long term.

Indeed, the company acknowledges that financial products are a commoditized offering, which means there isn't much distinction between the products of different companies, thus SoFi aims to use data and a simplified customer experience through its app, to offer better solutions and a better overall customer experience.

Therefore, its business strategy has been to vertically integrate digital and financial capacities in the company, through organic initiatives and acquisitions. For instance, an important acquisition was Galileo in 2020, which is a provider of a platform for technology services, both for financial and non-financial institutions, and provided SoFi with stronger digital capabilities than it had on its own.

Another important deal was its acquisition of Golden Pacific Bancorp, which provided it with a banking license, allowing it to offer deposits, which is a very important funding source for a sustainable financial business over the long term.

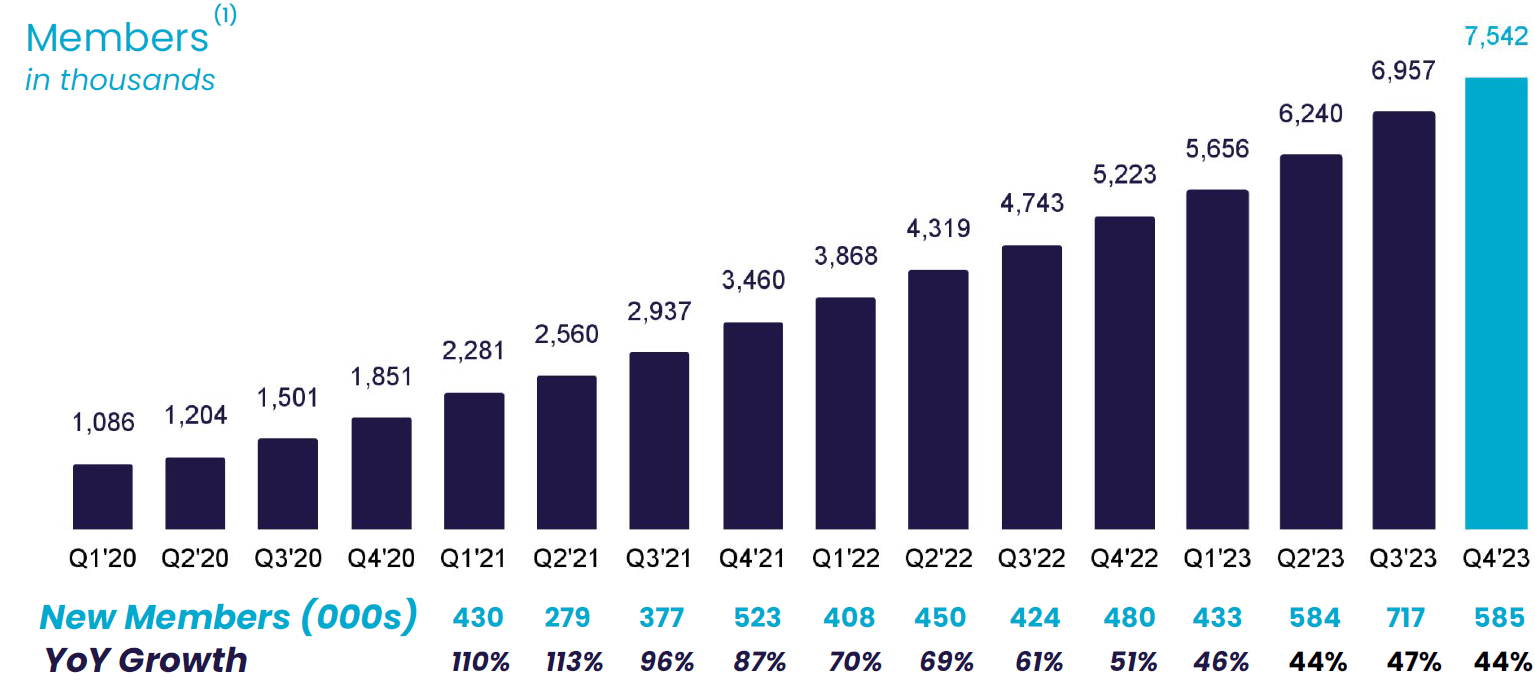

This strategy has been quite successful, given that it has consistently increased its total number of customers (what the company calls members), to about 7.5 million at the end of 2023, as shown in the next graph.

Customers growth (SoFi)

This is a very good growth history, showing that SoFi's customer proposition is good, leading to very good levels of customer acquisition over the past few years. While its growth rate has naturally decreased in recent quarters due to its larger size, it's still growing at around 45% YoY on a quarterly basis, boding well for growth ahead.

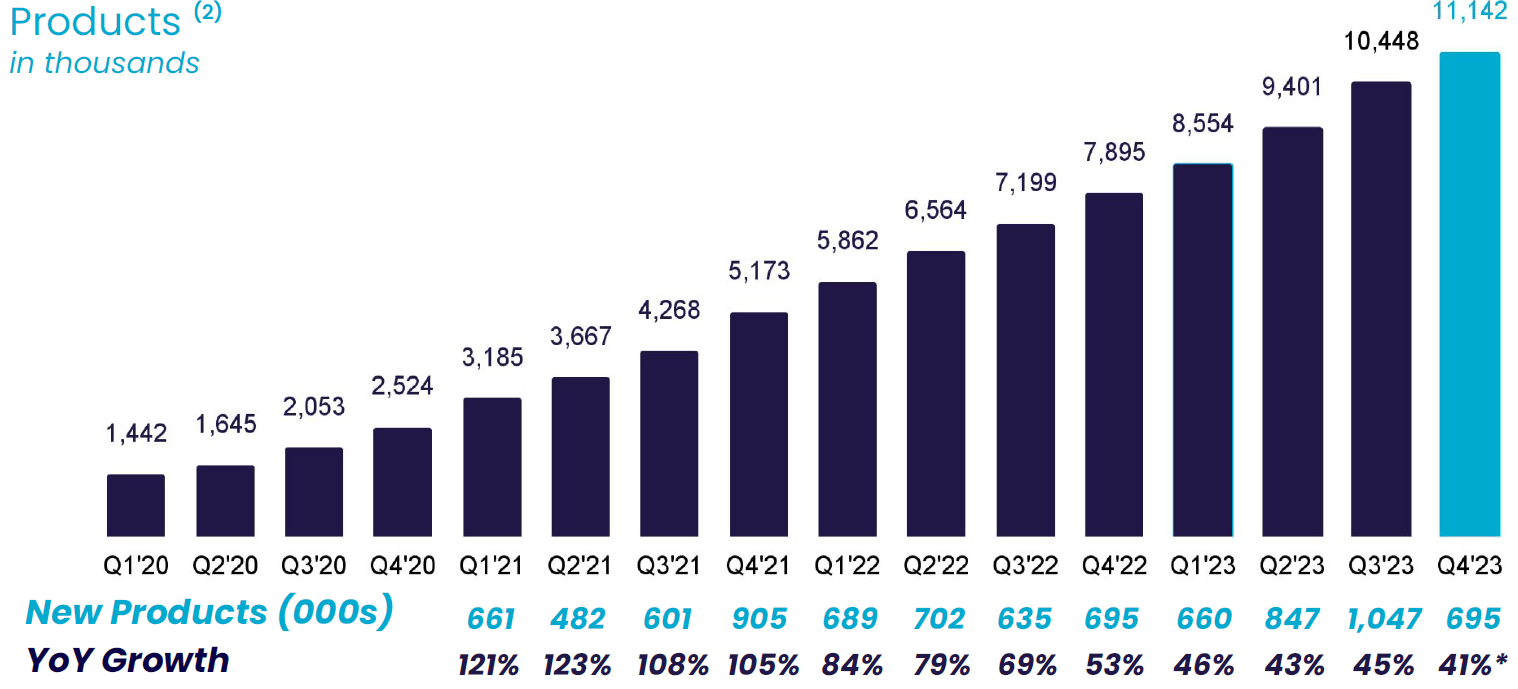

This growth is also explained by its strategy to become a one-stop shop for its customer's financial needs, as SoFi has expanded its product offering in recent years beyond traditional lending, including deposits, savings and investment products, trading services, and others.

This has led to higher customer engagement with SoFi, which can be seen in the total number of products held by its customers, which has increased to more than 11 million. This was driven in large part by strong growth in financial service products, which accounted for close to 9.5 million of total products at the end of 2023.

Products growth (SoFi)

This means that, on average, a customer only holds 1.48 products with SoFi, thus there is significant growth potential from higher customer engagement if the company can cross-sell more products to its existing customer base. Moreover, the ratio of financial services products to lending products has increased consistently in recent quarters, thus much of its product growth should continue to come from this segment.

On the other hand, in its technology platform service (Galileo), the total number of accounts has increased at a much modest pace in recent quarters, reaching 145 million at the end of 2023 (+11% YoY). This means much of SoFi's growth has been in the financial services segment, a trend that is likely to be maintained over the next few years.

Nevertheless, over the past year, SoFi's Lending segment was the largest one, representing some 62% of its total revenues, followed by Financial Services (20% of revenue) and Technology (17%). While this profile is not much different from previous years, its Financial Services segment is rapidly increasing its weight within the company and should continue to gain weight due to higher revenue growth than compared to Lending, which means its revenue profile is expected to gradually become more balanced over the next few years.

Going forward, SoFi's strategy is not expected to change much, remaining focused on developing its digital capabilities and offering its products and financial services through digital channels, being a key differentiating factor from traditional banks. While its growth strategy is mainly organic, SoFi can also continue to pursue acquisitions to improve its technology and competitive position in the fintech space, even though I don't expect large deals to happen in the near future.

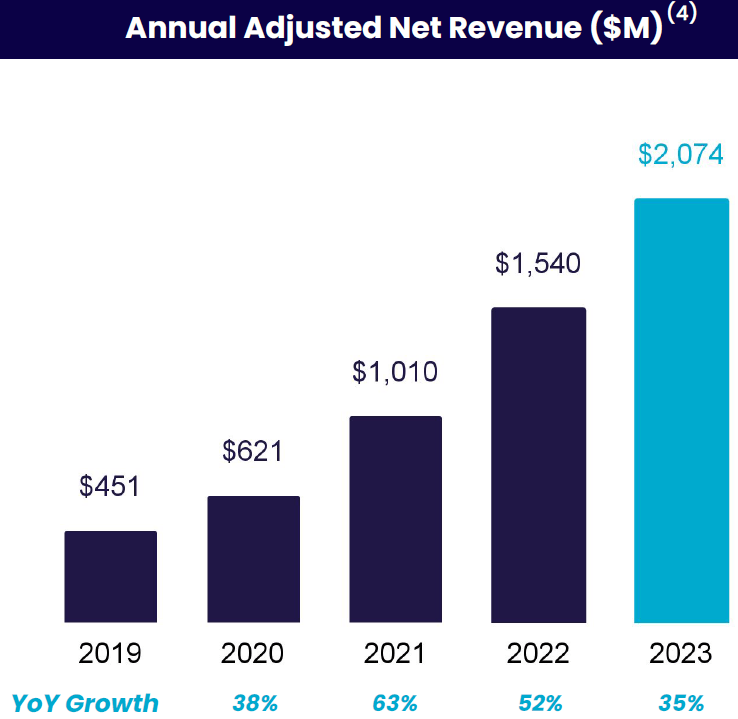

Regarding its financial performance, SoFi has a strong growth track record supported by a growing customer base, the expansion of its product and services offering in recent years, and acquisitions. Indeed, its revenue has doubled over the past couple of years, which is a remarkable outcome during a relatively short period of time.

Net revenue (SoFi)

As shown in the previous graph, while SoFi is still in a relatively early-growth phase, its annual revenues already surpassed $2 billion over the last year, which is a great outcome. Its annual growth was 35%, which is still quite strong.

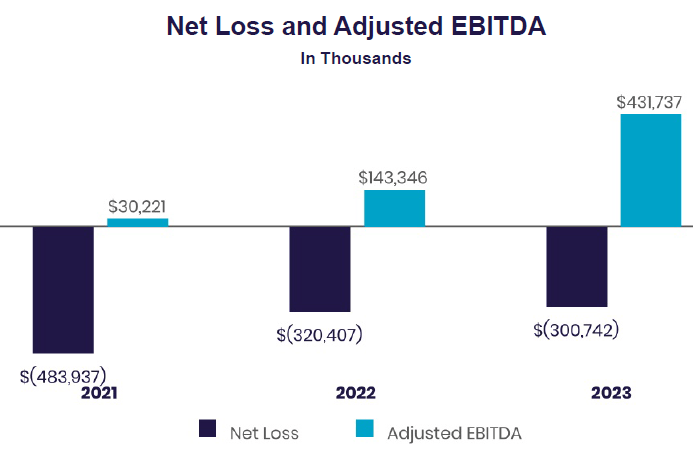

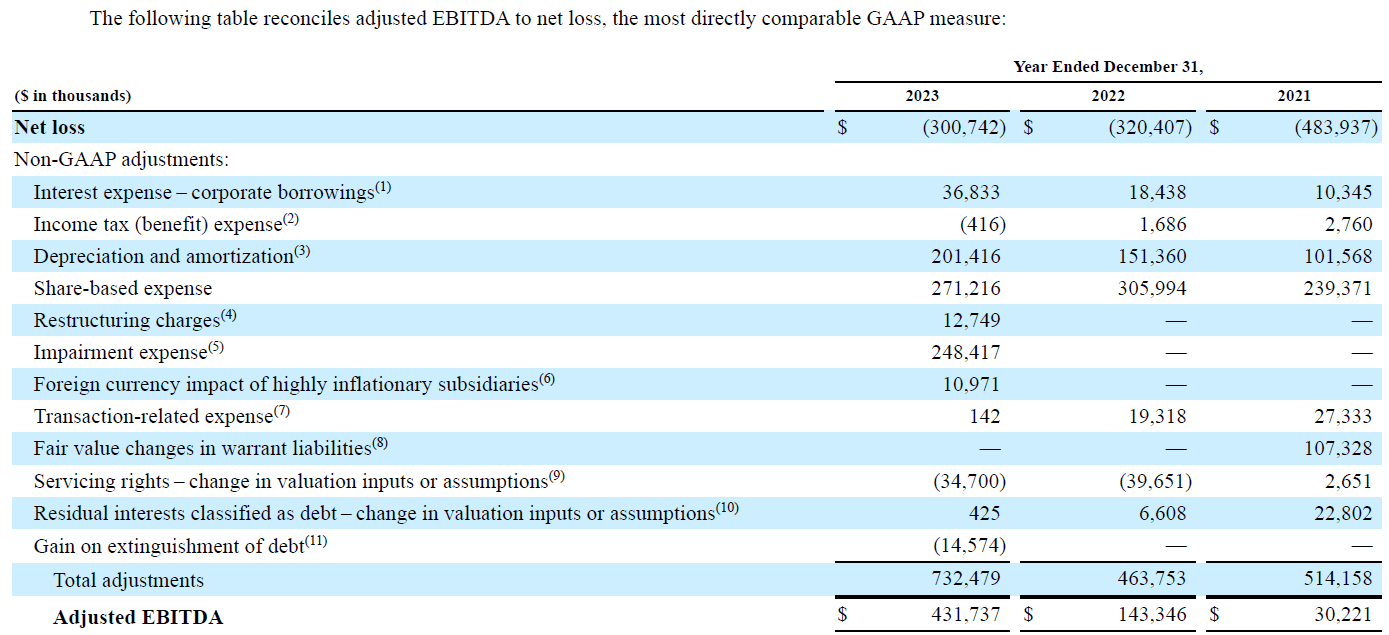

In addition to strong revenue growth, its larger size has enabled it to improve its efficiency and extract cost synergies from the integration of recent acquisitions, leading to a significant improvement in its profitability. Its adjusted EBITDA turned positive in 2021, and increased a lot over the past couple of years, to $432 million in 2023. This represents an adjusted EBITDA margin of 21%, which is quite good for a company like SoFi, which is still growing at a very strong pace.

These results were quite good and above the company's own guidance, showing that its operating momentum was strong in 2023, despite the more challenging market and economic environment.

However, on a GAAP basis, it reported a net loss of $300 million for the year, a small improvement from the loss of $320 million reported in the previous year. The major differences between the two metrics are depreciation & amortization and share-based compensation, thus I think investors should use adjusted EBITDA with some caution to analyze the company's profitability and to compare it with peers.

Profitability (SoFi)

In my opinion, investors should always use GAAP numbers to analyze the financial performance of any company because these metrics are standardized and less prone to management manipulation. Therefore, while SoFi has improved its profitability in recent years and has reported significant business growth, it's still reporting losses on a GAAP basis, which raises some questions about when it will be able to reach breakeven on GAAP net income.

Investors should also note that management adjustments in the past three years to reach adjusted EBITDA were between $463-732 million, which is a considerable amount and excludes a lot of expenses and charges, thus in my opinion the best metric to look at SoFi's 'true' profitability is its net loss.

Adjustments (SoFi)

Despite this, SoFi's guidance for 2024 implies strong growth in its Financial Services and Technology segments (50% or more), while in the Lending segment, it expects a decrease in annual revenue of about 5-7% compared to 2023. Its adjusted EBITDA should be between $580-590 million, and SoFi expects to report a net income (GAAP) of $95-100 million in 2024, which will be its first profitable year and an important milestone for the company.

However, investors should take into account that this guidance may be too optimistic because as the company's loan book increases, its credit losses are also expected to rise. This was already visible in 2023, given that its net charge-offs amounted to nearly $500 million, compared to just $122 million in the previous year, mainly related to personal loans. Its ratio of net charge-offs to total loans doubled in the year, to 2.66% in 2023.

This is still an acceptable ratio given that SoFi has significant exposure to student and personal loans, but if there is an economic slowdown in 2024 or if the Federal Reserve maintains rates at a relatively high level for longer than expected, this may be a headwind for credit quality in the coming quarters and can lead to higher net charge-offs and lower profitability levels than the company is expecting over the coming quarters.

This doesn't seem to be currently expected by the street given that current analysts' estimates expect to SoFi report a net profit of $101 million in 2024, in line with the company's guidance. In future years, current expectations are for strong growth, as net income is expected to be around $300 million in 2025, and above $500 million in 2026, which seems to be quite optimistic and may be revised downwards in the coming months.

Regarding its valuation, the fact that SoFi operates both in the financial and technology segments makes it somewhat tricky, but given that most of its revenues and profits come from lending and financial services, I think a valuation more similar to banks is appropriate.

Therefore, a price-to-book value multiple seems to be a good approach to value its shares. SoFi is currently trading at 1.4x book value, very close to its historical average of 1.3x book value over the past couple of years, which seems somewhat undemanding for a company that is growing quite rapidly and is expected to report profits on a GAAP basis this year.

SoFi Technologies has a very good growth history and its business strategy seems to be quite good, being therefore an interesting option for investors compared to 'traditional' banks. Its current valuation seems to be relatively undemanding for a company that is growing quite fast, even though there is some risk that a potential economic recession could hurt its top-line growth and profitability levels in the near future.

Nevertheless, I see SoFi as an attractive growth play in the fintech sector for investors with a long-term time frame, as its shares are quite volatile in the short term.